Global Air Separation Plant Market Size, Share, Growth Analysis By Process Type (Cryogenic Air Separation, Non-Cryogenic Air Separation), By Gas Output (Oxygen, Nitrogen, Argon, Others), By Capacity TPD (1,000 TPD), By End-Use Industry (Iron & Steel, Chemicals, Healthcare, Oil & Gas, Food & Beverage, Electronics, Pulp & Paper, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Mar 2026

- Report ID: 180410

- Number of Pages: 253

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

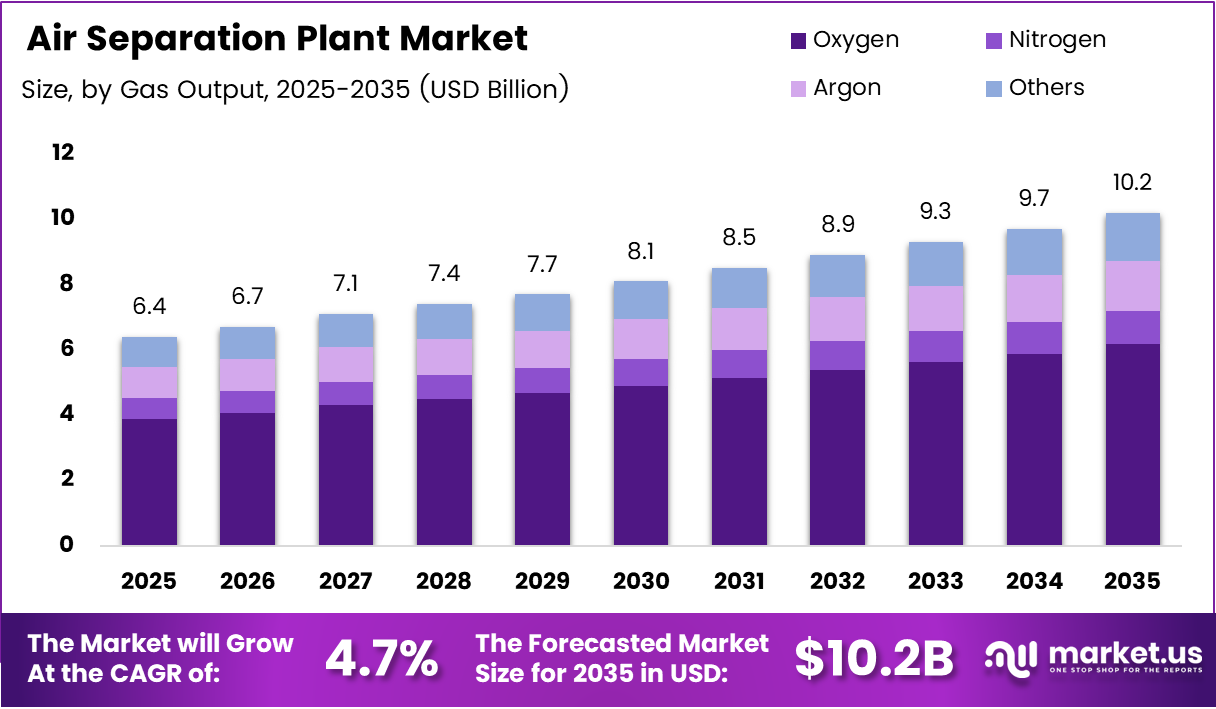

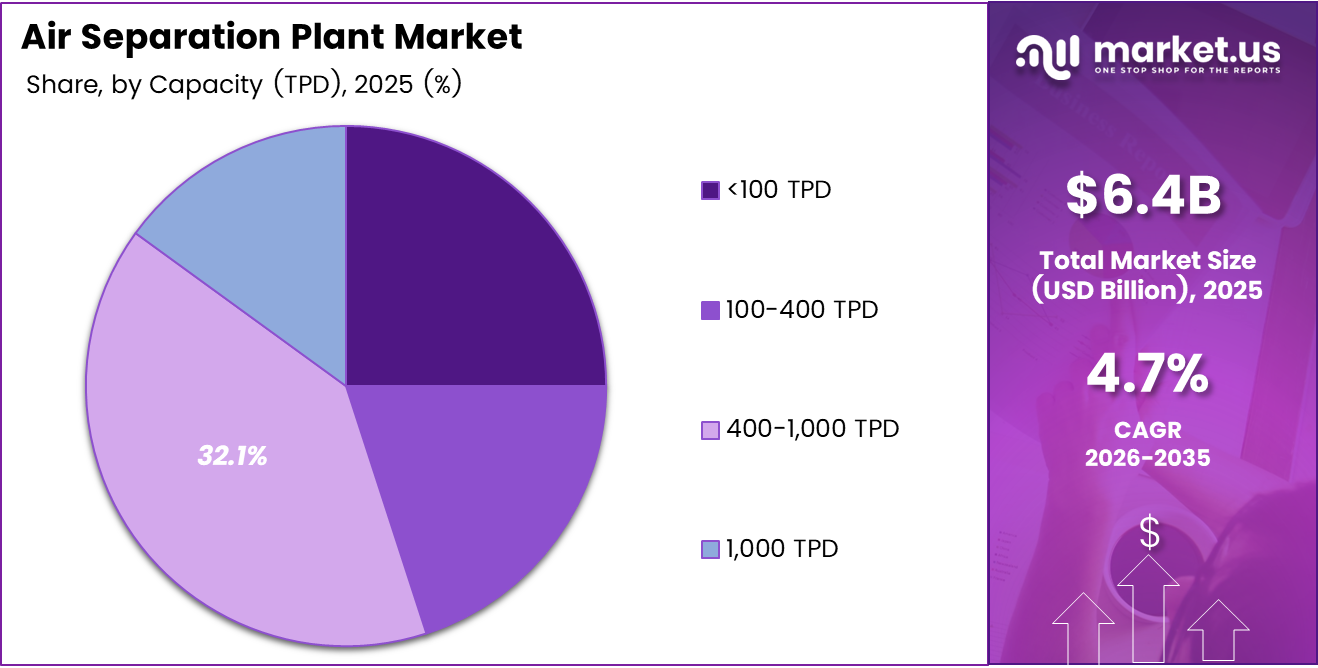

Global Air Separation Plant Market size is expected to be worth around USD 10.2 Billion by 2035 from USD 6.4 Billion in 2025, growing at a CAGR of 4.7% during the forecast period 2026 to 2035.

Air separation plants separate atmospheric air into its primary components — oxygen, nitrogen, and argon — through cryogenic distillation or non-cryogenic techniques. These industrial gas production systems form the backbone of oxygen supply for steelmaking, chemical synthesis, healthcare oxygen networks, and semiconductor fabrication. Without them, large-scale industrial processes simply cannot operate.

The 4.7% CAGR reflects a market where replacement cycles and capacity expansions are converging simultaneously. Steel producers are upgrading oxygen injection systems, chemical manufacturers are scaling gas consumption, and healthcare networks in emerging economies are building centralized oxygen infrastructure for the first time. Each of these forces creates multi-year procurement cycles.

Iron and steel manufacturing anchors demand at 34.1% of end-use consumption. This dominance signals that air separation plant investments are tightly coupled to steel capex cycles. When steelmakers expand blast furnace or electric arc furnace capacity, air separation unit orders follow — often with multi-decade supply contracts attached.

Asia Pacific leads the global market with a 42.1% share, valued at USD 2.69 Billion. The region’s industrial density, combined with active steelmaking and chemical complex expansions, creates structural demand that other regions cannot match at the same scale or velocity.

Cryogenic air separation holds 60.2% process-type share, reflecting the technology’s unmatched efficiency at high output volumes. Large integrated industrial complexes consistently prefer cryogenic units because their cost-per-unit-gas output drops sharply at scale — a structural advantage that makes alternative technologies economically viable only in niche applications.

According to a 2025 study published in Applied Energy, a proposed coupled liquid air energy storage system with an air separation unit achieves comprehensive electricity consumption of 0.268 kWh/Nm³, representing a 51.25% decrease compared to conventional ASUs. This level of efficiency improvement fundamentally changes the operating cost calculus for large industrial buyers evaluating new plant investments.

Additionally, in September 2024, Linde entered an agreement with Tata Steel to acquire two 1,800 TPD air separation units from the Kalinganagar Phase 2 project in India, adding 3,600 TPD of capacity. This move illustrates a consolidation pattern where leading gas suppliers absorb captive industrial assets — converting them into merchant supply nodes that serve broader regional markets.

Key Takeaways

- The Global Air Separation Plant Market was valued at USD 6.4 Billion in 2025 and is forecast to reach USD 10.2 Billion by 2035.

- The market advances at a CAGR of 4.7% during the forecast period 2026 to 2035.

- By Process Type, Cryogenic Air Separation leads with 60.2% market share in 2025.

- By Gas Output, Oxygen dominates with 60.6% share, reflecting its central role in steelmaking and healthcare.

- By Capacity, the 400–1,000 TPD segment holds 32.1% share, representing the preferred scale for large industrial complexes.

- By End-Use Industry, Iron and Steel leads with 34.1% share, anchoring air separation unit procurement to steel capex cycles.

- Asia Pacific dominates regionally with 42.1% share, valued at USD 2.69 Billion in 2025.

Process Type Analysis

Cryogenic Air Separation dominates with 60.2% due to superior output volumes and lower per-unit gas cost at scale.

In 2025, Cryogenic Air Separation held a dominant market position in the By Process Type segment of the Air Separation Plant Market, with a 60.2% share. Large-scale industrial buyers — steelmakers, refineries, and chemical producers — favor cryogenic units because output efficiency scales non-linearly. Moreover, the technology produces all three primary gases simultaneously, giving operators maximum product flexibility from a single plant asset.

Non-Cryogenic Air Separation serves applications where flexibility and lower capital commitment outweigh peak volume efficiency. Pressure swing adsorption and membrane separation systems allow operators to deploy rapidly and adjust output without the engineering lead times cryogenic units require. However, unit economics favor cryogenic technology at any output above a few hundred tons per day, which structurally limits non-cryogenic adoption to distributed or smaller-scale use cases.

Gas Output Analysis

Oxygen dominates with 60.6% due to indispensable role in steelmaking, chemical oxidation, and medical applications.

In 2025, Oxygen held a dominant market position in the By Gas Output segment of the Air Separation Plant Market, with a 60.6% share. Oxygen demand is structurally non-discretionary across its top three end markets — blast furnaces require continuous oxygen injection, chemical oxidation reactions depend on consistent purity grades, and hospital networks need uninterrupted medical-grade supply. This multi-sector dependency creates demand resilience that other gas outputs do not share.

Nitrogen carries the broadest application base among secondary gas outputs, spanning food packaging, electronics fabrication, and chemical blanketing. Its role in semiconductor manufacturing is particularly strategic — ultra-high purity nitrogen is non-substitutable in wafer processing environments. According to Air Liquide Engineering and Construction, integrated ASU advancements for ultra-pure nitrogen generators in electronics applications reduce energy consumption by approximately 30%, which makes on-site nitrogen production increasingly cost-competitive versus merchant supply for large fabs.

Argon differentiates through its premium pricing position within the air separation output mix. Argon constitutes less than 1% of atmospheric air, yet serves critical roles in specialty welding, stainless steel refining, and flat-panel display manufacturing. Its low atmospheric concentration means argon yield is entirely dependent on oxygen and nitrogen production volumes — making it a high-margin co-product rather than a standalone output target.

Others includes rare gases such as krypton, xenon, and neon, which are extracted in trace quantities during the cryogenic separation process. These gases command extreme price premiums in specialty lighting, semiconductor lithography, and medical imaging. Though volumetrically minor, their revenue contribution per unit is disproportionate — creating an incremental monetization opportunity for operators who invest in rare gas extraction columns.

Capacity (TPD) Analysis

400–1,000 TPD dominates with 32.1% due to alignment with large industrial complex oxygen requirements.

In 2025, the 400–1,000 TPD capacity segment held a dominant market position in the By Capacity segment of the Air Separation Plant Market, with a 32.1% share. This output range matches the operational requirements of mid-to-large steel mills, chemical complexes, and refinery projects. Consequently, new capacity announcements from major industrial gas companies tend to cluster in this range — balancing supply flexibility with capital efficiency.

Below 100 TPD units serve the modular and distributed deployment segment, where on-site gas production replaces merchant cylinder supply. These units suit healthcare facilities, smaller food processing operations, and remote industrial sites where pipeline supply is unavailable. The commercial case rests on eliminating logistics costs and supply disruption risk — not on achieving volume efficiency.

100–400 TPD units occupy the mid-market space between modular flexibility and large-scale efficiency. Buyers in this range typically include regional chemical producers, mid-size steel fabricators, and industrial parks requiring shared gas infrastructure. This segment benefits as emerging market industrial clusters develop before they reach the scale needed to justify larger ASU investments.

Above 1,000 TPD units represent the highest-capital, highest-commitment tier of the market. These plants anchor major petrochemical complexes, integrated steel mills, and world-scale refinery projects — often structured under long-term take-or-pay contracts spanning 15 to 20 years. The investment threshold filters buyers to a small number of global industrial majors and national energy companies, creating a market where contract wins are infrequent but transformative in revenue scale.

End-Use Industry Analysis

Iron and Steel dominates with 34.1% due to continuous, high-volume oxygen consumption in blast and electric arc furnaces.

In 2025, Iron and Steel held a dominant market position in the By End-Use Industry segment of the Air Separation Plant Market, with a 34.1% share. Steel production requires oxygen injection at multiple process stages — basic oxygen furnaces consume hundreds of tons per day at a single facility. Therefore, when steelmakers expand capacity or retrofit aging plants with oxygen-enriched processes, air separation unit orders are a direct and predictable consequence.

Chemicals represents the second major demand center, where oxygen and nitrogen serve as feedstocks and process gases across synthesis, oxidation, and blanketing applications. Large-scale chemical plants typically operate captive or dedicated ASUs to guarantee supply purity and continuity. This structural dependency makes chemical industry capex cycles a reliable leading indicator for air separation plant order activity.

Healthcare end-use has shifted from a secondary market to a strategic priority following global recognition of centralized medical oxygen infrastructure gaps. Governments across Asia, Africa, and Latin America are investing in hospital-grade oxygen generation systems to reduce cylinder dependency. This shift creates a durable procurement channel separate from industrial gas demand cycles.

Oil and Gas applications include gasification processes, enhanced oil recovery oxygen injection, and refinery hydrogen production. The integration of ASUs with low-carbon ammonia and clean hydrogen projects is extending oil and gas sector demand beyond traditional refining — connecting the air separation market to the energy transition investment pipeline.

Food and Beverage producers use nitrogen for modified atmosphere packaging and freezing applications. Nitrogen’s role in extending shelf life and preventing oxidation makes it a process-critical input — not a discretionary purchase. Growth in packaged food production across Asia Pacific directly translates into new nitrogen supply contracts.

Electronics manufacturing demands the highest purity grades of nitrogen and argon available from air separation systems. Semiconductor wafer fabrication and flat-panel display production require near-zero contamination environments — a requirement that commodity merchant supply cannot reliably meet at scale. This purity constraint drives dedicated on-site ASU installations at major chip and display manufacturing facilities.

Pulp and Paper operators use oxygen in bleaching processes as a substitute for chlorine-based chemicals. The shift to oxygen delignification and ozone bleaching reduces chemical costs and environmental compliance exposure. However, this end-use remains volumetrically modest relative to steel and chemicals, limiting its share contribution to the overall air separation plant market.

Others encompasses glass manufacturing, aerospace testing, water treatment, and specialty metal processing. These applications share a common characteristic: they require gas on a continuous, uninterrupted basis where supply failure carries immediate production consequences. This operational criticality, rather than volume alone, drives on-site ASU investment decisions in smaller-volume specialty sectors.

Key Market Segments

By Process Type

- Cryogenic Air Separation

- Non-Cryogenic Air Separation

By Gas Output

- Oxygen

- Nitrogen

- Argon

- Others

By Capacity (TPD)

- <100 TPD

- 100–400 TPD

- 400–1,000 TPD

- >1,000 TPD

By End-Use Industry

- Iron & Steel

- Chemicals

- Healthcare

- Oil & Gas

- Food & Beverage

- Electronics

- Pulp & Paper

- Others

Drivers

Steel, Chemical, and Healthcare Sectors Drive Structural Demand for Industrial Gas Production Capacity

Iron and steel manufacturing consumes oxygen at a scale no other single industry matches. Oxygen injection in basic oxygen furnaces and electric arc furnaces improves combustion efficiency, reduces coke consumption, and shortens heat cycle times. These process economics — not regulatory pressure — make air separation unit investment an operational necessity for any competitive steelmaking operation. In July 2024, Air Products announced plans to build two new air separation units in Georgia and North Carolina to replace older units and add capacity, targeting a 2026 onstream date.

Chemical manufacturers depend on oxygen and nitrogen as primary feedstocks for oxidation reactions, synthesis gas production, and inert blanketing. Large petrochemical complexes require guaranteed supply at consistent purity grades — a requirement that forces dedicated on-site ASU investment rather than reliance on merchant deliveries. Additionally, semiconductor and electronics manufacturing requires ultra-high purity nitrogen and argon. Any contamination at the parts-per-billion level compromises wafer yields, making on-site production from dedicated high-purity ASUs non-negotiable at scale.

According to a 2025 technical comparison published in the Energy journal, an externally compressed ASU integrated with the Allam cycle achieves specific energy consumption of 0.497 kWh/kg O₂, which is 5.2% lower than the internal compression model at 0.524 kWh/kg O₂. This efficiency differential matters to industrial buyers evaluating multi-decade plant investments — a 5% operating cost reduction compounds significantly over a 20-year asset life, directly influencing technology selection and vendor choice at the procurement stage.

Restraints

High Capital Costs and Energy Intensity Create Adoption Barriers for Large-Scale Cryogenic Air Separation Investment

Large-scale cryogenic air separation units demand capital outlays measured in hundreds of millions of dollars before a single cubic meter of gas is produced. Engineering, procurement, and construction timelines extend from 18 to 36 months for world-scale plants. This combination of front-loaded cost and delayed revenue generation restricts new ASU deployment to buyers with strong balance sheets and secured long-term off-take contracts — creating a structural barrier that limits market entry to a narrow pool of industrial majors.

Energy consumption represents the dominant ongoing cost in air separation plant operations. Cryogenic separation is an energy-intensive process — electricity costs typically account for 50% to 70% of total operating expenses for large ASUs. According to a 2025 study published in Applied Energy, decoupled integration of liquid air energy storage with ASU reduces gas production energy consumption during the energy release stage by 42.91% under optimized air supply ratios. However, this technology is still in advanced development — meaning most operating plants today carry the full energy burden of conventional separation processes.

Continuous gas separation processes cannot be paused for maintenance without interrupting supply to downstream customers who depend on uninterrupted delivery. This operational constraint forces operators to maintain parallel redundancy systems, adding capital and complexity beyond the base plant investment. Consequently, smaller industrial buyers who cannot absorb these fixed costs remain dependent on merchant supply — limiting on-site ASU adoption to large-scale operations where volume justifies the full cost structure.

Growth Factors

Green Hydrogen, Medical Oxygen Infrastructure, and Modular ASU Deployment Open New Revenue Channels

Green hydrogen production requires large volumes of high-purity oxygen as a co-product of electrolysis processes. However, projects coupling hydrogen production with low-carbon ammonia synthesis demand dedicated nitrogen and oxygen supply at scale — a requirement that positions air separation plants as infrastructure assets for the energy transition. In June 2025, Air Liquide invested up to USD 200 million to modernize and connect an air separation unit to its Louisiana network to support industrial growth and a long-term contract renewal with Dow, targeting completion in early 2027.

Medical oxygen infrastructure development across Asia, Africa, and Latin America creates a procurement pipeline distinct from traditional industrial gas cycles. Governments are deploying hospital oxygen generation systems to replace cylinder supply chains that proved unreliable during health crises. According to a 2025 academic paper published in Energies (MDPI), a novel integrated system coupling an externally compressed ASU with liquid air energy storage achieves an electrical round-trip efficiency of 55.3% — with energy storage capacity of 31.32 MWh per 10⁴ Nm³ O₂. This efficiency milestone makes on-site oxygen generation more viable for mid-scale healthcare applications where grid reliability is uncertain.

Small and modular air separation units address the market segment that large cryogenic plants cannot serve economically. Industrial clusters in emerging markets, remote mining operations, and distributed manufacturing zones need on-site gas production without the capital commitment of full-scale ASUs. Modular units ship as pre-assembled skid-mounted systems, reducing installation time and site preparation costs. This delivery model expands the addressable buyer base beyond the tier-one industrial majors who have historically driven market volume.

Emerging Trends

Automation, Energy-Efficient Distillation, and Compact Systems Reshape Air Separation Plant Deployment Models

Digital monitoring and automation technologies now allow air separation plant operators to optimize separation efficiency in real time. Advanced process control systems adjust compression ratios, flow rates, and distillation column parameters based on live operational data — reducing energy waste and improving output consistency. This shift from scheduled to predictive maintenance reduces unplanned downtime, which for large ASUs can disrupt entire industrial complexes dependent on continuous gas supply.

According to a 2025 technical insights report cross-verified against process-specific data, modern air separation plants using energy-efficient structured packing in distillation columns achieve specific power consumption below 0.45 kWh/Nm³. This performance benchmark matters because energy cost reduction directly improves plant economics without requiring additional capital investment — making efficiency retrofits a financially attractive alternative to building new capacity. Additionally, in June 2025, Linde signed a long-term agreement and committed more than USD 400 million to build a world-scale ASU in Louisiana to supply oxygen and nitrogen for a major low-carbon ammonia project, with startup expected in 2029.

Compact and skid-mounted air separation systems are enabling deployment in locations where traditional large-scale plants are neither practical nor economical. These systems reduce the capital threshold for on-site gas production, opening the market to pharmaceutical manufacturers, regional food processors, and smaller electronics fabricators. Strategic partnerships between industrial gas companies and heavy manufacturing industries further accelerate adoption — bundling long-term supply agreements with technical support that reduces buyer risk during the transition from merchant supply to on-site generation.

Regional Analysis

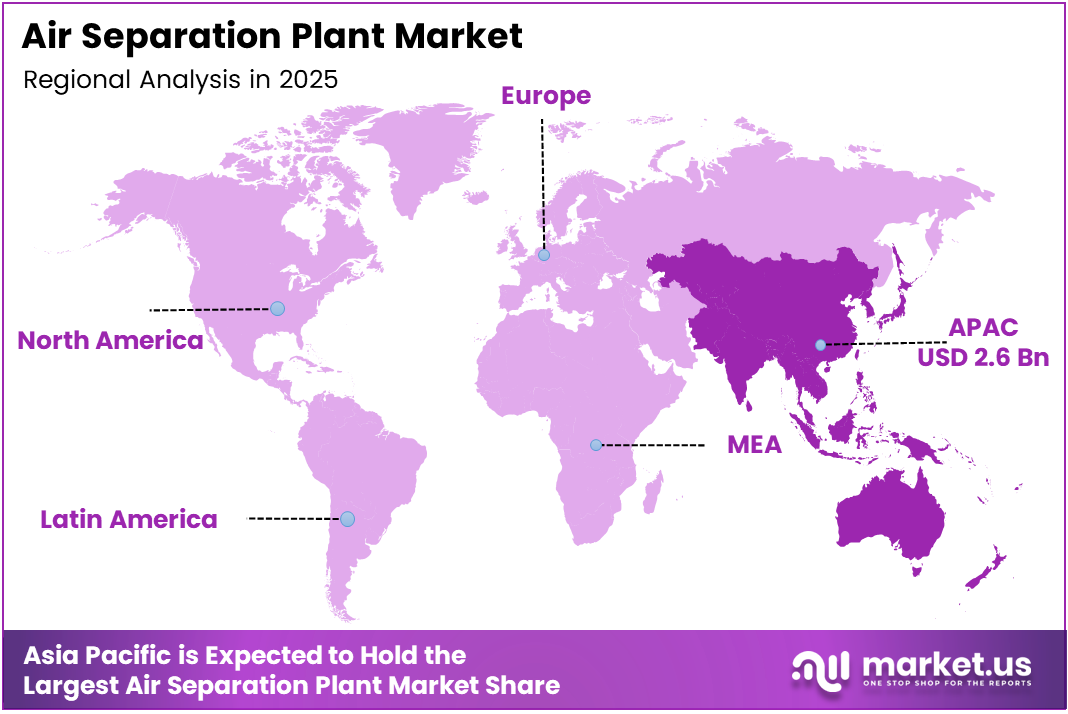

Asia Pacific Dominates the Air Separation Plant Market with a Market Share of 42.1%, Valued at USD 2.69 Billion

Asia Pacific commands 42.1% of the global Air Separation Plant Market, valued at USD 2.69 Billion in 2025. China’s massive integrated steel and chemical complex infrastructure drives the majority of this share. Moreover, semiconductor manufacturing expansion in South Korea, Taiwan, Japan, and India is adding high-purity gas demand on top of existing industrial volumes — reinforcing the region’s structural lead over all other geographies.

North America Air Separation Plant Market Trends

North America benefits from a combination of mature industrial gas infrastructure and active reinvestment in new capacity. Major producers are committing billions of dollars to new and upgraded ASUs across the U.S. Gulf Coast and industrial Midwest. The region’s integration of air separation plants into clean energy and low-carbon chemical projects adds a forward-looking growth dimension to what was previously a replacement-cycle-driven market.

Europe Air Separation Plant Market Trends

Europe’s air separation plant demand reflects the region’s industrial restructuring toward lower-carbon manufacturing processes. Steel decarbonization through hydrogen-based direct reduction and oxygen-enhanced electric arc furnace operation both require significant gas volumes. Additionally, specialty chemical and pharmaceutical manufacturing in Germany, France, and the Netherlands sustains consistent demand for high-purity nitrogen and argon at existing facility scales.

Middle East and Africa Air Separation Plant Market Trends

The Middle East concentrates air separation plant investment around petrochemical complex expansions and refinery upgrades, where large-volume oxygen and nitrogen supply underpins process economics. Africa’s trajectory differs — healthcare oxygen infrastructure development and nascent industrial zone construction create early-stage demand. Both subregions are building ASU capacity from a lower base, which means percentage growth rates exceed the global average even as absolute volumes remain smaller.

Latin America Air Separation Plant Market Trends

Latin America’s air separation plant market advances through two distinct channels: mining and metals processing in the Andean and Brazilian industrial belts, and healthcare oxygen infrastructure development driven by government investment programs. Brazil and Mexico anchor regional demand, with steel and chemical sector expansion providing the most predictable volume growth. The region’s infrastructure gaps also create demand for modular and distributed ASU solutions where pipeline connectivity is limited.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Linde plc holds the strongest global network position in the air separation plant market, combining engineering expertise with an expanding merchant and on-site supply portfolio. Linde’s strategy of acquiring captive industrial ASUs — such as the 3,600 TPD Tata Steel units in India — converts competitor assets into Linde-controlled supply nodes. This approach grows capacity without building from zero, shortening time-to-revenue while eliminating a potential competing supply source.

Air Liquide S.A. is executing a capital deployment strategy centered on large modular ASU clusters in key U.S. industrial corridors. The company’s concentration of new capacity along the Gulf Coast positions it to capture long-term contracts from petrochemical, clean energy, and low-carbon chemical producers simultaneously. Air Liquide’s investment in pipeline network expansion alongside new ASU construction creates logistical advantages that standalone plant operators cannot replicate without equivalent infrastructure spend.

Air Products and Chemicals Inc. focuses on replacing aging assets with higher-efficiency units while simultaneously adding merchant market capacity. This dual objective — improving unit economics on existing supply while expanding addressable volume — allows Air Products to defend margin on legacy contracts while competing for new customers at lower cost structures. The company’s geographic spread across U.S. industrial markets reduces regional demand concentration risk.

Taiyo Nippon Sanso Corporation leverages deep integration with Japanese and broader Asian electronics and semiconductor manufacturing ecosystems. This positions the company in the highest-purity, highest-margin segment of the industrial gas market. Asian semiconductor fab expansion directly translates into new ultra-high purity ASU contracts for Taiyo Nippon Sanso — a demand channel that is structurally insulated from commodity industrial gas pricing pressure.

Key Players

- Linde plc

- Air Liquide S.A.

- Air Products and Chemicals Inc.

- Taiyo Nippon Sanso Corporation

- Messer Group GmbH

- The Nikkiso Clean Energy & Industrial Gases Group

- Universal Industrial Gases, Inc. (UIG)

- SIAD Macchine Impianti S.p.A.

- Ranch Cryogenics Inc.

- Oxyplants

- AMCS Corporation

- Technex Ltd.

- MOS Techno Engineers

- Hangzhou Fortune Gas Cryogenic Group Co., Ltd.

- Sanghi Oxygen

- Other Key Players

Recent Developments

- July 2025 – Linde announced major investments to support the U.S. commercial space sector, including expansion of its Mims, Florida facility and construction of a new air separation unit in Brownsville, Texas. The new ASU targets Q1 2026 startup to supply liquid oxygen, nitrogen, and argon.

- January 2025 – Messer announced a strategic investment of over USD 70 million to build a new air separation unit in Berryville, Arkansas, expected onstream in the second half of 2026, complementing existing regional facilities.

- September 2025 – Air Products commissioned a new air separation unit in Cleveland, Ohio, supplying oxygen, nitrogen, and argon to an on-site customer and the regional merchant market, with reinvestment to extend the life of its existing ASU and liquefaction plant.

- October/November 2025 – Air Liquide inaugurated its new Geismar 4 Large Modular Air Separation Unit in Geismar, Louisiana, significantly increasing production capacity along the U.S. Gulf Coast to support regional industrial expansion.

- October 2025 – Air Water Gas Solutions broke ground on a new air separation unit at Eastman Business Park in Rochester, New York, targeting 2026 operational startup to supply high-purity liquid nitrogen, oxygen, and argon under a long-term agreement.

Report Scope

Report Features Description Market Value (2025) USD 6.4 Billion Forecast Revenue (2035) USD 10.2 Billion CAGR (2026-2035) 4.7% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Process Type (Cryogenic Air Separation, Non-Cryogenic Air Separation), By Gas Output (Oxygen, Nitrogen, Argon, Others), By Capacity TPD (<100 TPD, 100–400 TPD, 400–1,000 TPD, >1,000 TPD), By End-Use Industry (Iron & Steel, Chemicals, Healthcare, Oil & Gas, Food & Beverage, Electronics, Pulp & Paper, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Linde plc, Air Liquide S.A., Air Products and Chemicals Inc., Taiyo Nippon Sanso Corporation, Messer Group GmbH, The Nikkiso Clean Energy & Industrial Gases Group, Universal Industrial Gases Inc. (UIG), SIAD Macchine Impianti S.p.A., Ranch Cryogenics Inc., Oxyplants, AMCS Corporation, Technex Ltd., MOS Techno Engineers, Hangzhou Fortune Gas Cryogenic Group Co. Ltd., Sanghi Oxygen, Other Key Players Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Air Separation Plant MarketPublished date: Mar 2026add_shopping_cartBuy Now get_appDownload Sample

Air Separation Plant MarketPublished date: Mar 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Linde plc

- Air Liquide S.A.

- Air Products and Chemicals Inc.

- Taiyo Nippon Sanso Corporation

- Messer Group GmbH

- The Nikkiso Clean Energy & Industrial Gases Group

- Universal Industrial Gases, Inc. (UIG)

- SIAD Macchine Impianti S.p.A.

- Ranch Cryogenics Inc.

- Oxyplants

- AMCS Corporation

- Technex Ltd.

- MOS Techno Engineers

- Hangzhou Fortune Gas Cryogenic Group Co., Ltd.

- Sanghi Oxygen

- Other Key Players

Our Clients

- 180410

- Mar 2026