Global AI Road Debris Detector Market Size, Share and Analysis Report By Component (Hardware, Software, Services (Installation & Integration, Data Labeling & Model Training, Managed Services & Monitoring)), By Deployment (On-Vehicle, Roadside Infrastructure), By Technology (Vision-Centric AI, LiDAR/Radar Fusion Systems, Thermal Imaging Integration, Others), By End-User (Automotive OEMs, Government Agencies, Fleet Operators, Others), By Regional Analysis, Global Trends and Opportunity, Future Outlook By 2025-2035

- Published date: Feb. 2026

- Report ID: 179097

- Number of Pages: 203

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

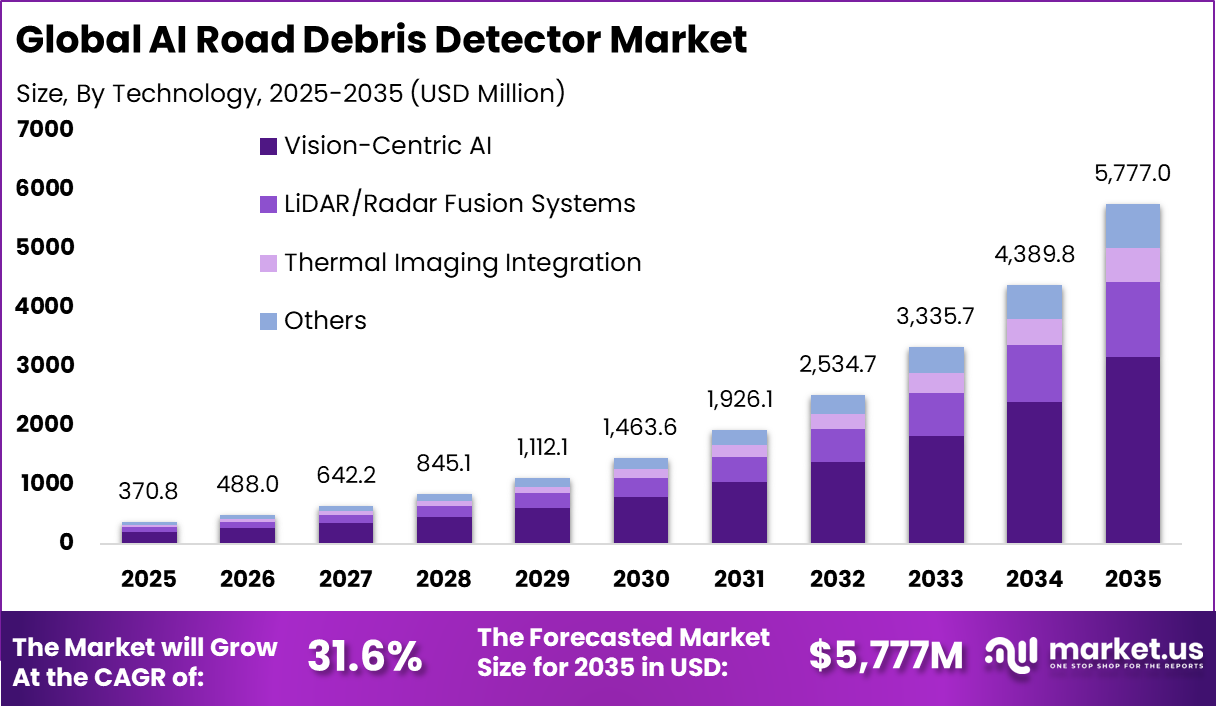

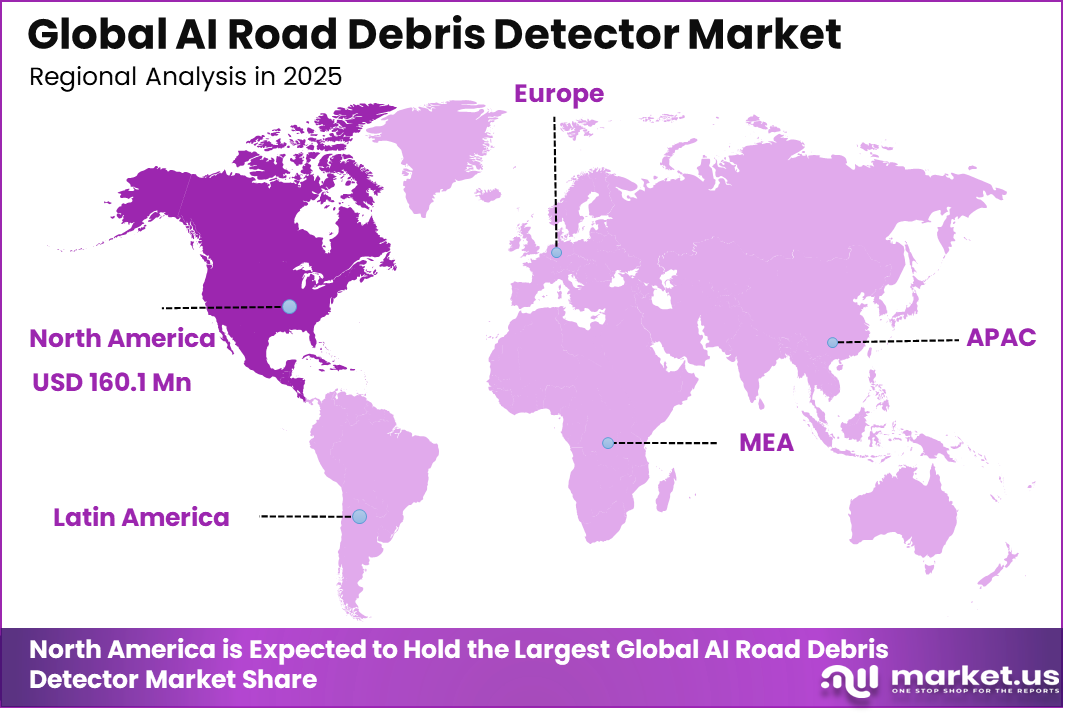

The Global AI Road Debris Detector Market size is expected to be worth around USD 5,777.0 Million By 2035, from USD 370.8 Million in 2025, growing at a CAGR of 31.6% during the forecast period from 2026 to 2035. North America held a dominant Market position, capturing more than a 43.2% share, holding USD 160.1 Million revenue.

The AI Road Debris Detector Market refers to the segment of intelligent transportation and road safety systems where AI is deployed to detect, classify, and alert authorities or drivers about debris present on highways and urban roads. These systems rely on advanced sensors, edge computing, and machine learning algorithms to identify obstacles such as tire fragments, fallen cargo, rocks, or vehicle parts in real time. The objective is to reduce collision risk, improve traffic flow, and support faster response from road maintenance teams.

AI road debris detection solutions are typically integrated into fixed roadside infrastructure, connected vehicles, or smart traffic management networks. With increasing road congestion and higher vehicle speeds, even small objects on highways can cause severe accidents. As governments invest in intelligent transportation systems and connected road infrastructure, automated debris detection is being positioned as a preventive safety layer within broader smart mobility frameworks.

AI-based road debris and anomaly detection solutions are demonstrating strong performance levels, with accuracy rates for identifying pavement defects such as potholes and cracks frequently surpassing 90% to 95% under controlled conditions. These platforms commonly rely on advanced computer vision techniques, including Convolutional Neural Networks and YOLO models, to analyze road imagery with high precision.

The shift from manual inspection methods to automated, real-time monitoring is supporting faster identification of hazards and more proactive maintenance planning. In several implementations, the adoption of these systems has been associated with accident reductions of up to 50%, highlighting their potential contribution to road safety and infrastructure management.

Top Market Takeaways

- In the AI Road Debris Detector market, Services accounted for 58.1% share, reflecting strong demand for installation, maintenance, monitoring, and system integration support.

- Roadside Infrastructure based fixed deployment led with 65.3% share, supported by integration with highways, toll roads, and smart traffic management systems.

- Vision-centric AI technology captured 54.9% of the market, driven by camera-based object detection and real-time image analytics capabilities.

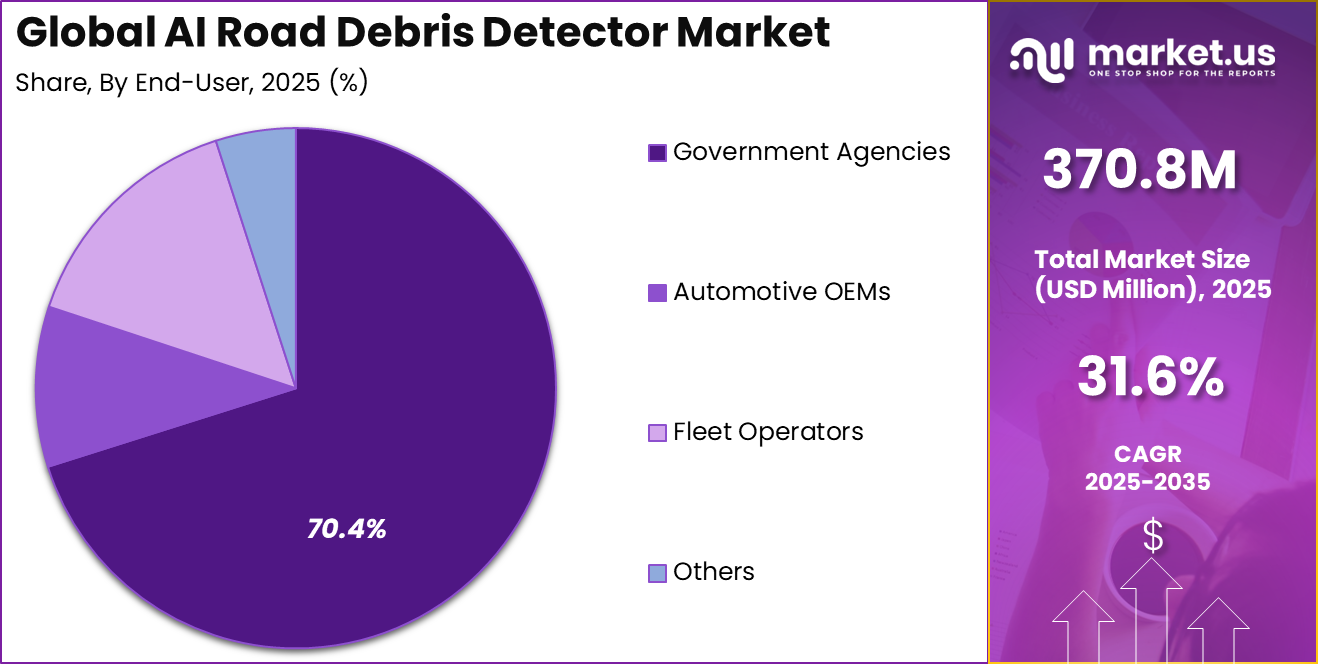

- Government agencies represented 70.4% of total demand, as public authorities prioritize roadway safety, accident prevention, and infrastructure monitoring.

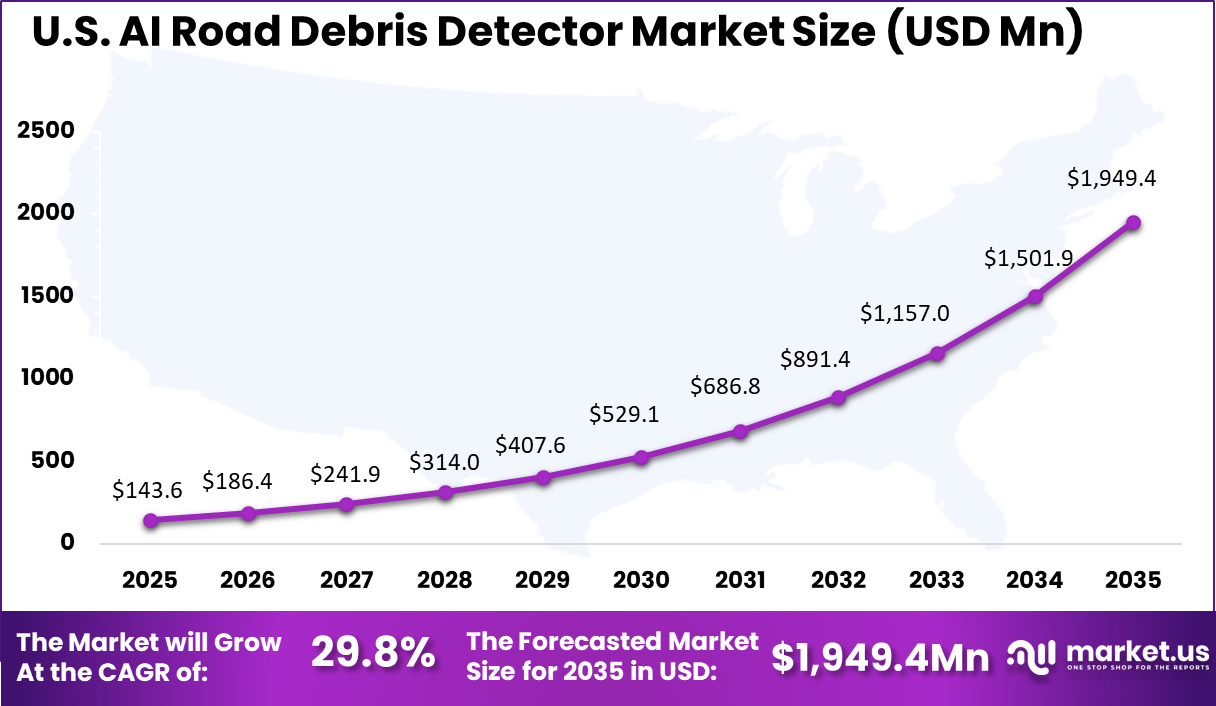

- North America held 43.2% of the global market, with the United States generating USD 143.6 million in revenue and expanding at a 29.8% CAGR, supported by smart transportation investments and highway safety modernization programs.

Key statistics

- AI algorithms used for general road anomaly detection demonstrate average accuracy rates between 86.3% and 97.8%, reflecting high reliability in identifying debris and surface irregularities.

- Specialized deep learning models for potholes and cracks have achieved 91.86% precision and 97.54% mean Average Precision, indicating strong dataset-level validation performance.

- In real-time environments, advanced object detection models have recorded 89.5% precision while identifying more than 1,100 potholes in live field conditions.

- Optimized small object detection systems can identify debris as small as 2 cm, achieving 100% accuracy at low speeds and 91.1% accuracy in complex scenarios at 36.3 frames per second.

- Under ideal lighting and weather conditions, AI systems can exceed 95% detection accuracy. However, performance may decline in low visibility or heavy rainfall environments.

- AI-based monitoring of road hazards and driver behavior has contributed to more than 50% reduction in accident rates, improving roadway safety outcomes.

- Pilot deployments of AI-driven traffic management systems have demonstrated a 17% reduction in primary crashes and a 43% decrease in secondary crashes, strengthening incident response efficiency.

- Advanced AI models reduce data size by 80% to 84% compared to traditional processing approaches while maintaining strong object identification accuracy of approximately 65% for roadway fixtures.

- AI-enabled drone and vehicle inspection systems have lowered infrastructure maintenance costs by 40% to 60%, supporting cost-efficient roadway monitoring programs.

By Component

In 2025, Services accounting for 58.1% indicate that system integration, maintenance, monitoring, and analytics support are central to market value creation. Road debris detection systems require continuous calibration, software updates, and operational oversight to maintain accuracy in varying environmental conditions.

Governments and transport agencies typically rely on specialized service providers for deployment and lifecycle management. Ongoing data analysis and performance optimization are also part of service-driven revenue. AI models must be retrained to improve object classification accuracy across changing road conditions.

This creates recurring service demand rather than one-time hardware sales. Additionally, long-term infrastructure contracts strengthen the services share. Public sector buyers often prefer managed service agreements that ensure uptime and compliance with road safety regulations.

By Deployment

Roadside infrastructure holding 65.3% reflects the practicality of fixed monitoring systems on highways and major transport corridors. Fixed cameras and sensors mounted on gantries or poles provide continuous monitoring across high-risk zones such as tunnels, bridges, and high-speed expressways.

This deployment model allows centralized control and integration with traffic management centers. When debris is detected, automated alerts can trigger digital signage updates or dispatch road clearance teams. Fixed installations also support large-area coverage without requiring every vehicle to be equipped with detection technology.

Infrastructure-based systems are often prioritized in national smart road initiatives. Governments can implement detection solutions across high-traffic corridors as part of broader digital road modernization programs.

By Technology

Vision-centric AI representing 54.9% highlights the dominance of camera-based detection systems. High-resolution cameras combined with deep learning algorithms can classify debris types with increasing precision. These systems are cost-effective compared to multi-sensor alternatives and are easier to scale across road networks. Camera-based AI benefits from rapid advancements in computer vision and edge processing hardware.

Improved image recognition enables detection of small objects under varying lighting conditions. Continuous improvements in neural network architectures are enhancing detection speed and reliability. Another advantage is compatibility with existing traffic camera infrastructure. Many road networks already have surveillance systems installed, which can be upgraded with AI modules rather than replaced entirely.

By End-User

Government agencies accounting for 70.4% demonstrate that public authorities are the primary adopters of AI road debris detection systems. Road safety and traffic management fall under public sector responsibility in most countries, making government procurement central to market expansion. Investment is often tied to accident reduction programs and smart city initiatives.

Governments aim to reduce secondary collisions caused by unexpected road obstacles. AI detection systems support faster response and measurable safety improvements. Public funding also supports pilot programs and phased rollouts. Large-scale highway networks require structured deployment strategies, which further reinforces the role of government-led implementation.

Regional Analysis

North America holding 43.2% reflects strong investment in intelligent transportation infrastructure and advanced automotive technologies. The region has a high concentration of connected vehicle initiatives and smart highway projects. Federal and state-level safety programs have increased interest in AI-driven monitoring systems.

The ecosystem also benefits from collaboration between technology firms, automotive suppliers, and public agencies. Research partnerships and pilot programs contribute to faster commercialization of AI-based road safety solutions.

The United States contributing USD 143.6 Mn with a CAGR of 29.8% as per the provided inputs indicates strong growth momentum. Expansion is being driven by increasing focus on reducing highway fatalities and improving traffic incident management efficiency.

High vehicle density and extensive interstate highway networks create demand for automated monitoring systems. As infrastructure modernization funding increases, AI road debris detection is being incorporated into broader transportation digitization strategies.

Emerging Trends Analysis

A major emerging trend is the integration of debris detection with broader smart traffic management systems. Instead of functioning as standalone tools, detection platforms are increasingly connected to digital signage, navigation systems, and emergency response networks. This integration improves response time and situational awareness.

Another trend is the movement toward edge computing deployment. Processing images locally at roadside units reduces latency and bandwidth usage. Faster processing supports real-time alert generation, which is critical for high-speed traffic environments.

Key Market Segments

By Component

- Hardware

- Software

- Services

- Installation & Integration

- Data Labeling & Model Training

- Managed Services & Monitoring

By Deployment

- On-Vehicle

- Roadside Infrastructure

By Technology

- Vision-Centric AI

- LiDAR/Radar Fusion Systems

- Thermal Imaging Integration

- Others

By End-User

- Government Agencies

- Automotive OEMs

- Fleet Operators

- Others

Regional Analysis and Coverage

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of Latin America

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Driver Analysis

The primary driver is increasing road safety concerns linked to debris-related accidents. Even minor road obstacles can lead to severe incidents, especially at highway speeds. AI detection systems offer preventive identification before accidents occur.

Another driver is government investment in intelligent transportation systems. Infrastructure modernization programs are allocating budgets toward digital monitoring and automation technologies. This funding environment accelerates adoption across major transport corridors.

Restraint Analysis

One restraint is the high initial installation cost of roadside AI infrastructure. Fixed camera systems, edge processors, and integration with traffic control centers require capital-intensive investment. Budget limitations in some regions can slow deployment.

Another restraint is environmental variability. Weather conditions such as heavy rain, fog, or snow can affect detection accuracy. Maintaining performance consistency across seasons remains a technical challenge.

Opportunity Analysis

A key opportunity lies in integration with connected vehicle ecosystems. When debris detection alerts can be transmitted directly to vehicles, the safety impact increases significantly. This opens pathways for collaboration between infrastructure providers and automotive manufacturers.

Another opportunity is expansion into emerging markets investing in smart highways. As developing economies upgrade road networks, AI-based monitoring can be embedded from the design stage, reducing retrofitting costs.

Challenge Analysis

A major challenge is ensuring high detection accuracy while minimizing false positives. Excessive false alerts can reduce trust in the system and create operational inefficiencies. Continuous algorithm training and validation are required.

Another challenge is interoperability between multiple technology providers. Standardization across hardware, software, and communication protocols is essential for large-scale deployment across national highway systems.

Competitive Analysis

Competition in the AI Road Debris Detector Market is structured around automotive technology leaders, semiconductor firms, and advanced sensor developers. Bosch, Continental AG, Valeo, ZF Friedrichshafen, Magna International, and Denso Corporation leverage their automotive electronics expertise to integrate detection capabilities within advanced driver assistance systems and roadside infrastructure.

Technology-focused companies such as NVIDIA, Renesas Electronics, Ambarella, Mobileye, and LeddarTech contribute high-performance processors and vision AI platforms that enable real-time image analysis. Their strength lies in scalable computing architectures optimized for automotive and edge environments.

Autonomous mobility and sensor innovators including Waymo, Tesla, Aptiv, Innoviz Technologies, and Luminar Technologies influence the market through advancements in perception systems and sensor fusion. These players drive improvements in object recognition, lidar integration, and AI-driven road awareness, indirectly accelerating the development of specialized debris detection solutions.

Top Key Players in the Market

- Bosch

- Valeo

- Mobileye

- NVIDIA

- Waymo

- Tesla

- Aptiv

- Continental AG

- Magna International

- ZF Friedrichshafen

- Denso Corporation

- Renesas Electronics

- Ambarella

- Innoviz Technologies

- LeddarTech

- Luminar Technologies

- Others

Recent Developments

- January 2026, Qualcomm: Qualcomm highlighted expanded Snapdragon Digital Chassis momentum and positioned “agentic AI” as a next step in in-vehicle intelligence. For road debris detection vendors, this strengthens the case for running more perception and event classification directly at the edge, reducing cloud dependence and improving response time.

- April 2025, MediaTek: Dimensity Auto Cockpit Platform C-X1 and Dimensity Auto Connect MT2739 were unveiled as OEM-ready platforms. While positioned for cockpit and connectivity, the practical impact for AI road debris detection is that higher on-device AI compute and stronger in-vehicle networking make it easier to share sensor feeds and run additional safety analytics inside the vehicle architecture.

Report Scope

Report Features Description Market Value (2025) USD 370.8 Mn Forecast Revenue (2035) USD 5,777 Mn CAGR (2026-2035) 31.6% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue forecast, AI impact on Market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends Segments Covered By Component (Hardware, Software, Services (Installation & Integration, Data Labeling & Model Training, Managed Services & Monitoring)), By Deployment (On-Vehicle, Roadside Infrastructure), By Technology (Vision-Centric AI, LiDAR/Radar Fusion Systems, Thermal Imaging Integration, Others), By End-User (Automotive OEMs, Government Agencies, Fleet Operators, Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA Competitive Landscape Bosch, Valeo, Mobileye, NVIDIA, Waymo, Tesla, Aptiv, Continental AG, Magna International, ZF Friedrichshafen, Denso Corporation, Renesas Electronics, Ambarella, Innoviz Technologies, LeddarTech, Luminar Technologies, Others Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  AI Road Debris Detector MarketPublished date: Feb. 2026add_shopping_cartBuy Now get_appDownload Sample

AI Road Debris Detector MarketPublished date: Feb. 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Bosch

- Valeo

- Mobileye

- NVIDIA

- Waymo

- Tesla

- Aptiv

- Continental AG

- Magna International

- ZF Friedrichshafen

- Denso Corporation

- Renesas Electronics

- Ambarella

- Innoviz Technologies

- LeddarTech

- Luminar Technologies

- Others

Our Clients

- 179097

- Feb. 2026