Global Agricultural Calcium Market Size, Share, And Industry Analysis Report By Type (Calcium Carbonate, Calcium Sulfate, Calcium Nitrate, Calcium Chloride, Calcium Oxide and Hydroxide, Calcium Citrate, Calcium Phosphate, Natural Mineral), By Form (Powder, Granules and Grits, Liquid, Pellets, Others), By Application (Agriculture, Animal Feed), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: March 2026

- Report ID: 180081

- Number of Pages: 208

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

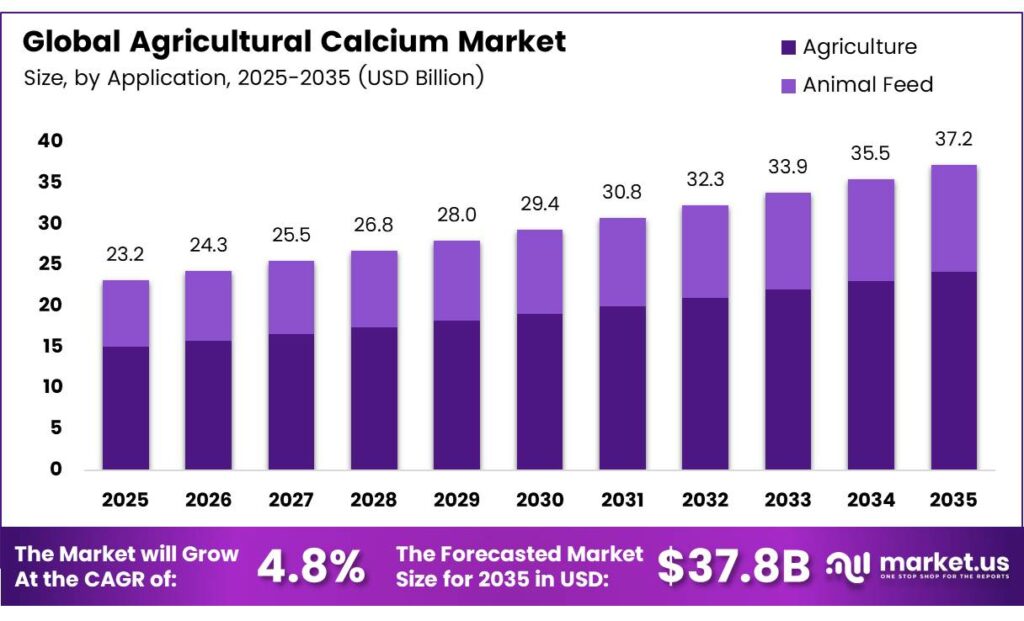

The Global Agricultural Calcium Market size is expected to be worth around USD 37.2 billion by 2035 from USD 23.2 billion in 2025, growing at a CAGR of 4.8% during the forecast period 2026 to 2035.

Agricultural calcium covers a wide range of mineral-based inputs used in crop production and animal nutrition. These inputs include calcium carbonate, calcium sulfate, calcium nitrate, and several other compound forms. Farmers and agribusinesses apply these products to manage soil health, correct pH imbalances, and improve crop output.

The market plays a critical role in global food production systems. Calcium inputs support stronger cell walls in plants, reduce blossom-end rot, and enhance fruit quality. Moreover, they improve soil structure by promoting water retention and reducing compaction, which directly supports higher agricultural yields.

- United States lime production reached 16,000,000 tons in 2024, valued at approximately USD 3,200,000,000. This production scale reflects strong domestic demand for calcium-based soil amendments across North American agricultural markets.

- China’s lime production reached 310,000,000 metric tons in 2024, representing the largest national output globally. This volume highlights how Asia Pacific leads in both calcium mineral processing and agricultural application demand, supporting the region’s dominant market position.

Opportunities in specialty crop segments and controlled environment agriculture also contribute to market expansion. Greenhouse operators and high-value fruit growers increasingly rely on precision calcium applications. Additionally, regenerative agriculture programs worldwide are integrating calcium inputs as a core component of long-term soil restoration strategies.

Key Takeaways

- The Global Agricultural Calcium Market is valued at USD 23.2 billion in 2025 and is projected to reach USD 37.2 billion by 2035, at a CAGR of 4.8% during the forecast period from 2026 to 2035.

- The Calcium Carbonate dominates with a 52.4% share in 2025.

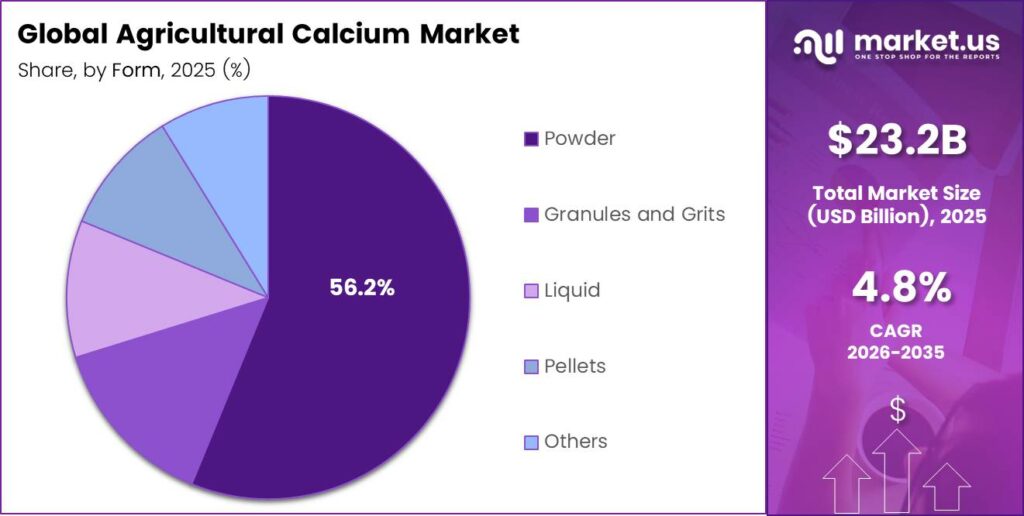

- Powder leads the market with a 56.2% share in 2025.

- Agriculture accounts for the largest share at 82.3% in 2025.

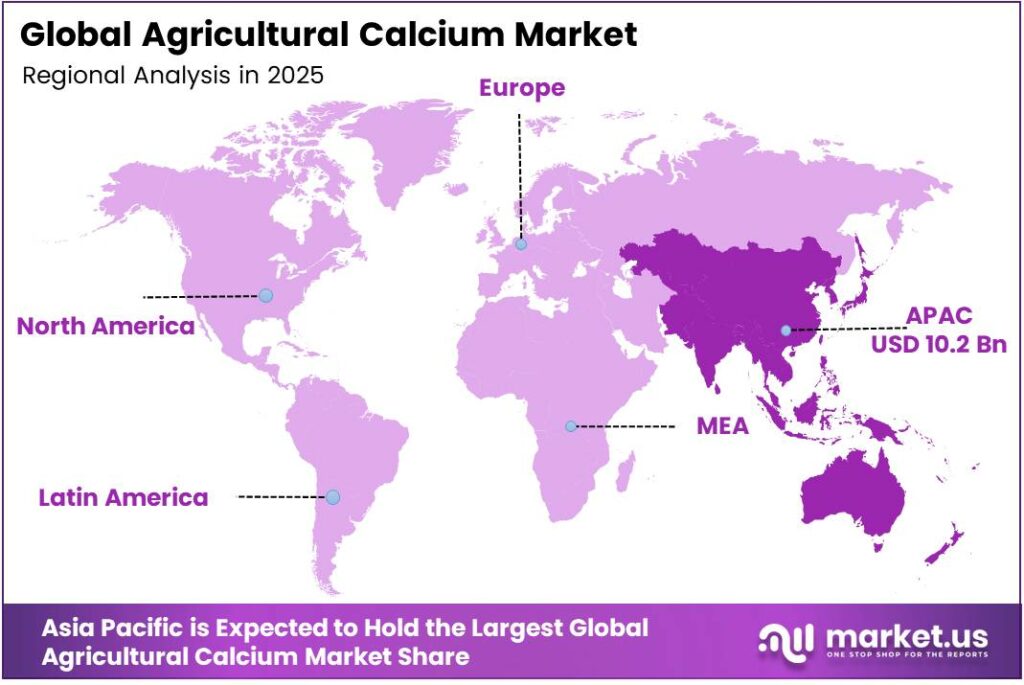

- Asia Pacific leads all regions with a 44.1% market share, valued at USD 10.2 billion in 2025.

By Type Analysis

Calcium Carbonate dominates with 52.4% due to its wide availability, cost efficiency, and proven effectiveness in soil pH correction.

In 2025, Calcium Carbonate held a dominant market position in the By Type segment of the Agricultural Calcium Market, with a 52.4% share. Farmers widely use this compound for liming acidic soils and improving nutrient absorption. Its abundance in natural limestone deposits makes it the most cost-effective calcium source for large-scale crop production.

Calcium Sulfate, commonly known as gypsum, serves as a key soil conditioner in agricultural systems. It improves soil structure without significantly altering pH levels. Moreover, it supplies both calcium and sulfur simultaneously, making it valuable for sulfur-deficient soils in cotton, peanut, and vegetable growing regions.

Calcium Nitrate provides dual-nutrient benefits by supplying both calcium and nitrogen in a single application. Greenhouse growers and fertigation-based crop producers favor this form for its rapid solubility. Additionally, it reduces tip burn in leafy vegetables and blossom-end rot in tomatoes, commanding premium pricing in specialty crop segments.

Calcium Chloride, Calcium Oxide and Hydroxide, Calcium Citrate, Calcium Phosphate, and Natural Mineral forms address niche applications. Natural mineral rock dust is gaining traction in regenerative farming programs. These forms collectively serve specific soil chemistry, animal feed, and organic certification requirements across diverse agricultural markets.

By Form Analysis

Powder dominates with 56.2% due to ease of mixing, cost efficiency, and compatibility with both soil application and compound feed formulations.

In 2025, Powder held a dominant market position in the By Form segment of the Agricultural Calcium Market, with a 56.2% share. Powder forms integrate easily into broadcast spreading equipment and feed mixing systems. Their fine particle size ensures faster soil incorporation and nutrient release, making them the preferred choice for both crop and livestock applications.

Granules and Grits offer handling advantages in field operations due to their reduced dust generation and easier flow through spreading equipment. Farmers in large-scale grain and oilseed production prefer granular calcium products for their precision application and reduced environmental dispersion during mechanical spreading.

Liquid calcium forms support fertigation systems in high-value crop production. Drip irrigation operators apply liquid calcium directly to root zones for maximum uptake efficiency. Pellets serve specialty horticulture markets where controlled-release behavior is desired. Others include slurry and suspension forms used in customized soil amendment programs.

By Application Analysis

Agriculture dominates with 82.3% due to widespread use of calcium inputs across soil conditioning, crop nutrition, and pH management programs globally.

In 2025, Agriculture held a dominant market position in the By Application segment of the Agricultural Calcium Market, with an 82.3% share. Field crop production, horticulture, and specialty crop farming all rely on calcium inputs for soil health management. Additionally, mandatory nutrient management programs in key agricultural nations continue to drive systematic calcium application across commercial farmland.

Animal Feed represents the secondary application segment and serves the poultry, dairy, and livestock nutrition industries. Feed-grade calcium products improve bone density, eggshell quality, and milk production in commercial livestock operations. Furthermore, rising quality standards in poultry and dairy production are expanding demand for high-purity calcium additives in compound feed formulations.

Key Market Segments

By Type

- Calcium Carbonate

- Calcium Sulfate

- Calcium Nitrate

- Calcium Chloride

- Calcium Oxide and Hydroxide

- Calcium Citrate

- Calcium Phosphate

- Natural Mineral

By Form

- Powder

- Granules and Grits

- Liquid

- Pellets

- Others

By Application

- Agriculture

- Animal Feed

Emerging Trends

Natural Mineral Inputs and Precision Tools Transform Agricultural Calcium Deployment

Farmers are shifting toward natural mineral rock dust and trace-element calcium products for eco-friendly soil remineralization. Organic and regenerative farming programs increasingly specify these inputs for certification compliance. Moreover, this trend is opening premium market channels for natural mineral calcium suppliers targeting sustainability-focused agricultural operations worldwide.

- Precision soil diagnostics and digital farming tools enable optimized, site-specific calcium deployment across commercial farms. Agronomists use sensor data and soil mapping platforms to prescribe calcium applications at variable rates. Brazil’s lime production reached 8,100,000 metric tons in 2024, signaling strong regional demand for calcium inputs in one of the world’s fastest-expanding agricultural markets.

Value-added calcium co-products tailored for fertigation and functional livestock nutrition are gaining traction among commercial producers. Manufacturers are developing calcium blends that deliver both soil and crop nutrition benefits in a single application. Additionally, the dominance of powder and granule forms continues to support cost-efficient mixing in both soil conditioning and compound feed systems.

Drivers

Precision Agriculture Adoption and Livestock Production Growth Drive Sustained Demand for Agricultural Calcium

The global shift to sustainable precision agriculture accelerates the mandated use of mineral calcium inputs for soil and crop optimization. Governments and agribusiness organizations worldwide promote calcium-based soil management as part of national food security programs. SigmaRoc plc completed acquisitions worth GBP 548,600,000 net of cash in FY2024, reflecting accelerating consolidation in the mineral calcium supply chain.

- Intensifying commercial livestock production prioritizes preventive calcium nutrition for enhanced bone strength and productivity. Poultry and dairy operations apply feed-grade calcium products to meet rising quality benchmarks in egg and milk production. India’s lime production reached 17,000,000 metric tons in 2024, demonstrating robust calcium mineral supply capacity in a major agricultural economy.

Widespread soil acidification and nutrient depletion from intensive farming drive urgent pH correction and restoration demand. Farmers in high-intensity crop production regions face compounding soil health challenges requiring systematic calcium intervention. Consequently, agricultural extension programs and agrochemical distributors are increasing calcium product education and supply access across affected farming communities.

Restraints

Regulatory Limits on Calcium Mining and Competition from Alternative Inputs Restrain Market Growth

Strict environmental regulations and ecological limits on calcium mining and quarrying restrict raw material supply chains globally. Regulatory agencies in the European Union and North America impose stringent controls on quarry expansion, dust emissions, and land rehabilitation requirements. These compliance costs increase production expenses for calcium mineral processors and limit supply capacity in regulated markets.

Intense competition from alternative soil amendments and synthetic fertilizers erodes market penetration in cost-sensitive regions. Farmers in emerging economies often select lower-cost chemical alternatives over traditional calcium inputs when budget constraints tighten. Moreover, aggressive pricing strategies from synthetic fertilizer manufacturers make it difficult for calcium product suppliers to compete on cost alone in price-sensitive agricultural markets.

Supply chain fragmentation also presents a structural challenge for global calcium input distribution. Many small-scale calcium producers lack the logistics infrastructure to serve remote farming communities efficiently. Consequently, inconsistent product availability and quality variation across supply regions limit adoption rates among farmers who require reliable and consistent calcium input supplies throughout the growing season.

Growth Factors

Specialty Crops, Organic Farming, and Climate-Smart Agriculture Accelerate Agricultural Calcium Market Expansion

Explosive expansion of specialty crops and controlled environment agriculture creates targeted demand for high-purity calcium applications. Greenhouse vegetable and fruit producers require precise calcium management to prevent physiological disorders and maximize crop quality. The United States gypsum apparent consumption reached 44,000,000 tons in 2024, reflecting strong North American demand for calcium sulfate in both agricultural and industrial applications.

The surge in organic and non-GMO certified animal feed additives opens premium channels for natural mineral calcium sources. Feed manufacturers targeting health-conscious and sustainability-focused end markets increasingly specify certified mineral calcium products. Furthermore, Nordkalk, a leading European calcium carbonate producer, operates approximately 50 locations across Europe as of 2024, supporting expanded distribution reach for agricultural calcium inputs across diverse farming regions.

Integration of calcium into climate-smart and regenerative farming systems supports long-term soil resilience worldwide. Governments and international development organizations fund soil health restoration programs that prioritize calcium-based interventions. Additionally, the rapid crop export and agribusiness boom in South America fuels mandatory calcium use across diverse farming climates, creating new volume growth opportunities for global calcium input suppliers.

Regional Analysis

Asia Pacific Dominates the Agricultural Calcium Market with a Market Share of 44.1%, Valued at USD 10.2 Billion

Asia Pacific leads the global agricultural calcium market with a 44.1% share, valued at USD 10.2 billion in 2025. China’s massive lime production of 310,000,000 metric tons and India’s extensive farming base drive this regional dominance. Moreover, government-mandated soil health programs across China, India, and Southeast Asia create consistent institutional demand for calcium mineral inputs.

North America maintains a strong position in the agricultural calcium market, supported by advanced precision farming infrastructure and large-scale commercial crop production. The United States operates 73 primary lime plants across 28 states, ensuring broad domestic supply coverage. Additionally, widespread adoption of soil testing and variable-rate application technology drives systematic calcium input use across the region.

Europe demonstrates steady demand for agricultural calcium products, driven by EU soil health regulations and organic farming expansion. Germany, France, and Poland serve as major consumption markets within the region. The European Union’s Farm to Fork strategy actively promotes reduced synthetic input use, consequently increasing interest in mineral calcium-based soil amendments among European commercial farmers.

The Middle East and Africa region shows emerging growth potential in agricultural calcium, supported by food security initiatives and irrigation-based farming expansion. Gulf Cooperation Council nations invest in agricultural infrastructure to reduce food import dependency. Additionally, South African commercial farming and East African smallholder development programs are gradually increasing calcium input adoption.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Yara International is a global leader in crop nutrition solutions, offering a comprehensive portfolio of calcium nitrate and mineral-based fertilizers for both field and specialty crop markets. Yara’s global distribution network and agronomic advisory services strengthen its position as a preferred calcium input supplier for commercial growers worldwide.

Omya International AG operates as a leading producer and distributor of calcium carbonate and dolomite products for agricultural and industrial applications. The company maintains an extensive global mining and processing footprint, enabling consistent supply to agricultural markets across Europe, the Asia Pacific, and the Americas. Omya’s focus on product purity and particle size customization positions it well to serve precision crop nutrition and soil amendment programs in high-value farming segments.

EuroChem Group develops and supplies a broad range of mineral fertilizers, including calcium nitrate and complex nutrient blends for global agriculture. The company operates large-scale mining and chemical processing facilities that integrate calcium production into wider fertilizer supply chains. EuroChem’s investment in integrated nutrient management solutions and its expanding distribution platform support growing demand for calcium-enriched crop inputs across emerging agricultural markets.

Imerys is a global specialty minerals company offering high-purity calcium carbonate and functional mineral products for agricultural, feed, and industrial applications. The company leverages advanced mineral processing technologies to deliver consistent product quality across multiple particle size specifications. Imerys serves agricultural input manufacturers and compound feed producers who require precisely graded calcium mineral ingredients for formulation efficiency and regulatory compliance.

Top Key Players in the Market

- Yara International

- Omya International AG

- EuroChem Group

- Imerys

- Saint-Gobain Formula

- Carmeuse

- Coromandel International Ltd.

- Minerals Technologies Inc.

- Graymont

- Kemin Industries, Inc.

- CALC Group

- Sibelco

- GLC Minerals, LLC.

- Huber Engineered Materials

- Lhoist

Recent Developments

- In 2025, Yara signed a binding 10-year offtake agreement with ATOME for the entire output of low-carbon calcium ammonium nitrate (CAN) from ATOME’s Villeta project in Paraguay. The deal includes an option to extend and supports Yara’s distribution of low-carbon calcium-based fertilizers into key South American agricultural markets (Brazil and Argentina). This aligns with Yara’s focus on lower-carbon-footprint calcium nitrate products for crop nutrition.

- In 2025, Omya’s joint venture Vereinigte Kreidewerke Dammann (VKD) hosted the first Lime Symposium in Germany. Experts highlighted regular liming with calcium carbonate as essential for climate-resilient agriculture: it corrects soil acidity, improves pH and nutrient uptake, enhances soil structure via calcium-ion flocculation, reduces nitrogen leaching, boosts drought/flood resistance, and supports higher yields in crops such as barley and sugar beet.

Report Scope

Report Features Description Market Value (2025) USD 23.2 Billion Forecast Revenue (2035) USD 37.2 Billion CAGR (2026-2035) 4.8% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Type (Calcium Carbonate, Calcium Sulfate, Calcium Nitrate, Calcium Chloride, Calcium Oxide and Hydroxide, Calcium Citrate, Calcium Phosphate, Natural Mineral), By Form (Powder, Granules and Grits, Liquid, Pellets, Others), By Application (Agriculture, Animal Feed) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Yara International, Omya International AG, EuroChem Group, Imerys, Saint-Gobain Formula, Carmeuse, Coromandel International Ltd., Minerals Technologies Inc., Graymont, Kemin Industries, Inc., CALC Group, Sibelco, GLC Minerals, LLC., Huber Engineered Materials, Lhoist Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)  Agricultural Calcium MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample

Agricultural Calcium MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Yara International

- Omya International AG

- EuroChem Group

- Imerys

- Saint-Gobain Formula

- Carmeuse

- Coromandel International Ltd.

- Minerals Technologies Inc.

- Graymont

- Kemin Industries, Inc.

- CALC Group

- Sibelco

- GLC Minerals, LLC.

- Huber Engineered Materials

- Lhoist

Our Clients

- 180081

- March 2026