Quick Navigation

Report Overview

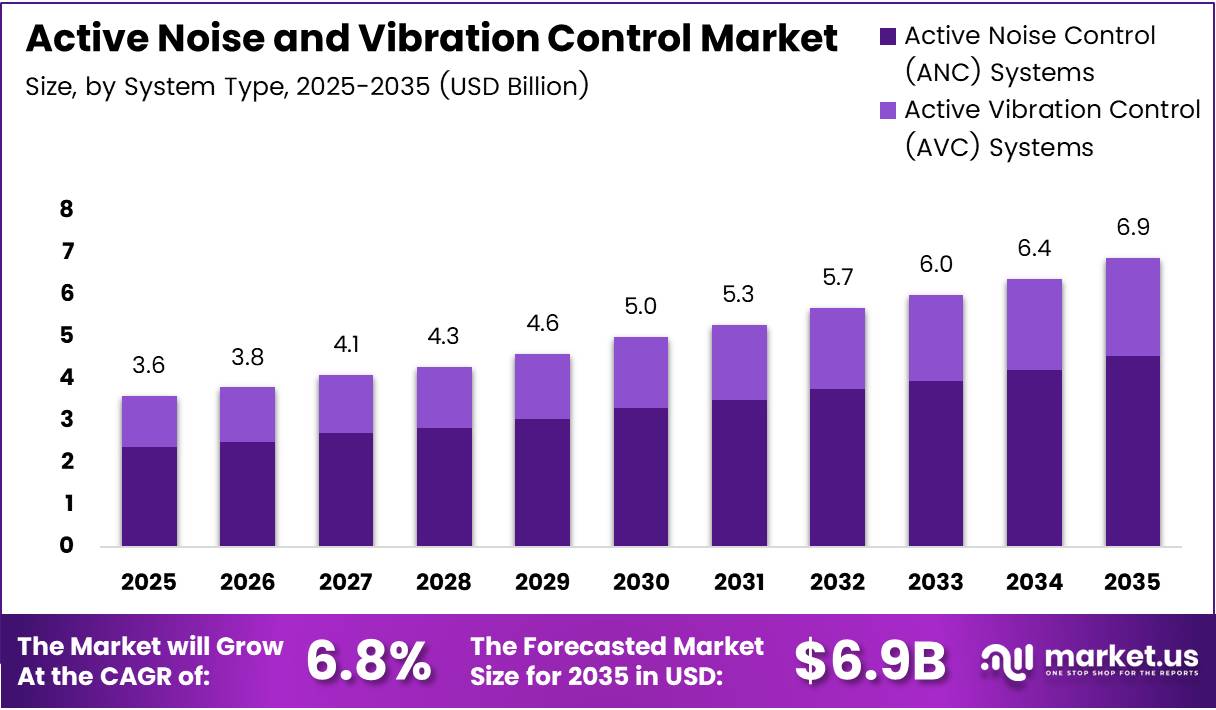

Global Active Noise and Vibration Control (ANVC) Market size is expected to be worth around USD 6.9 Billion by 2035 from USD 3.6 Billion in 2025, growing at a CAGR of 6.8% during the forecast period 2026 to 2035.

The active noise and vibration control market covers systems and components that detect, measure, and cancel unwanted sound and mechanical oscillation in real time. These solutions span aircraft cabins, industrial machinery, automotive platforms, and smart infrastructure. The market serves both OEM integration and retrofit applications across commercial and defense sectors.

Aviation remains the most structurally significant end-use platform. Aircraft manufacturers and MRO operators face tightening certification requirements that directly mandate noise reduction performance. This regulatory pressure transforms ANVC from a comfort feature into a compliance necessity — shifting procurement decisions from discretionary to obligatory across commercial fleets.

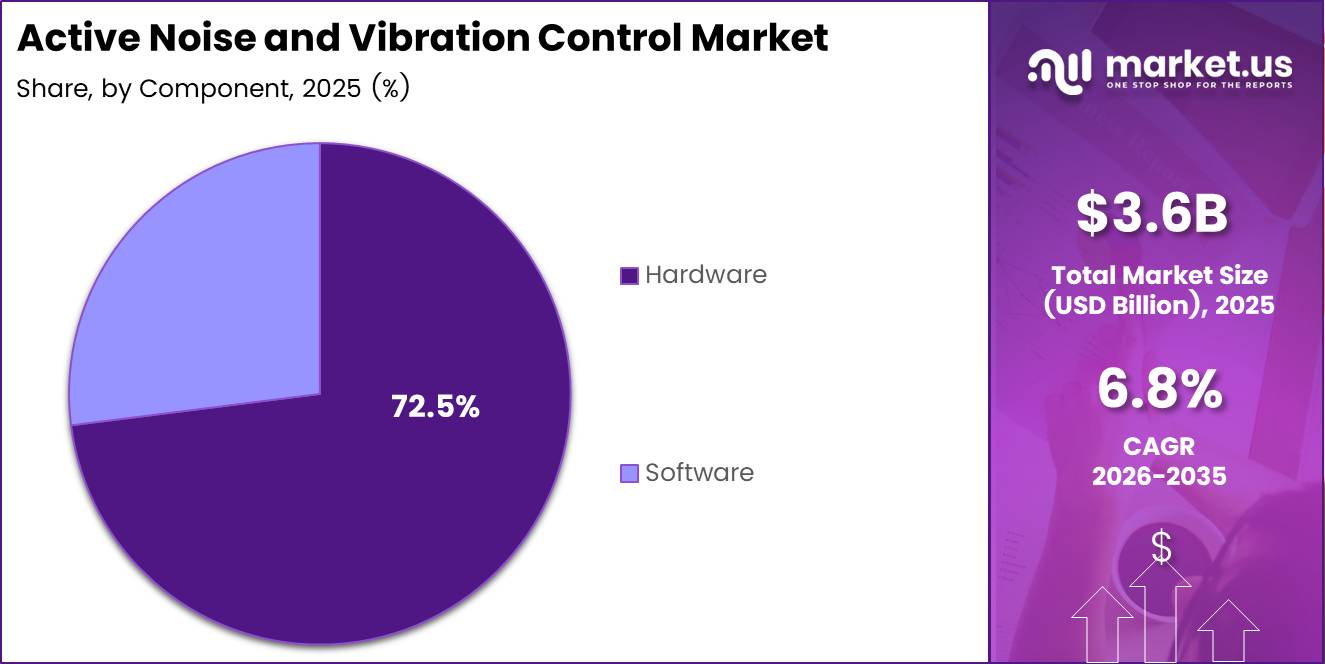

Hardware dominates the component mix, accounting for 72.5% of market revenue. This reflects the physical reality of noise and vibration suppression: actuators, sensors, and control units must be embedded into platforms at the design stage. Software-only upgrades cannot substitute for structural integration, which means hardware renewal cycles drive sustained revenue for systems providers.

Active Noise Control (ANC) systems hold 65.9% of the system type segment, confirming that acoustic management — not mechanical vibration — remains the primary buyer priority. Aviation passengers and urban commuters have set a new baseline expectation for cabin quiet, and that expectation now flows upstream into procurement specifications for aircraft, rail, and automotive platforms.

In March 2025, DLR published results from the LNATRA project showing that targeted noise reduction retrofits on a live A320 test aircraft reduced individual source noise by up to 6 dB and overall flyover noise by 3 dB — equating to approximately 30% perceived noise reduction for people on the ground. This finding matters because it validates retrofit as a commercially viable path, not just a design-stage solution.

Experimental ANC cabin testing presented at DAGA 2024 demonstrated a noise attenuation of 16.9 dB at the primary microphone position at 200 Hz. This level of low-frequency suppression is significant because 200 Hz aligns with engine and structural vibration modes that passive materials cannot efficiently address — confirming the performance ceiling of active systems over conventional approaches.

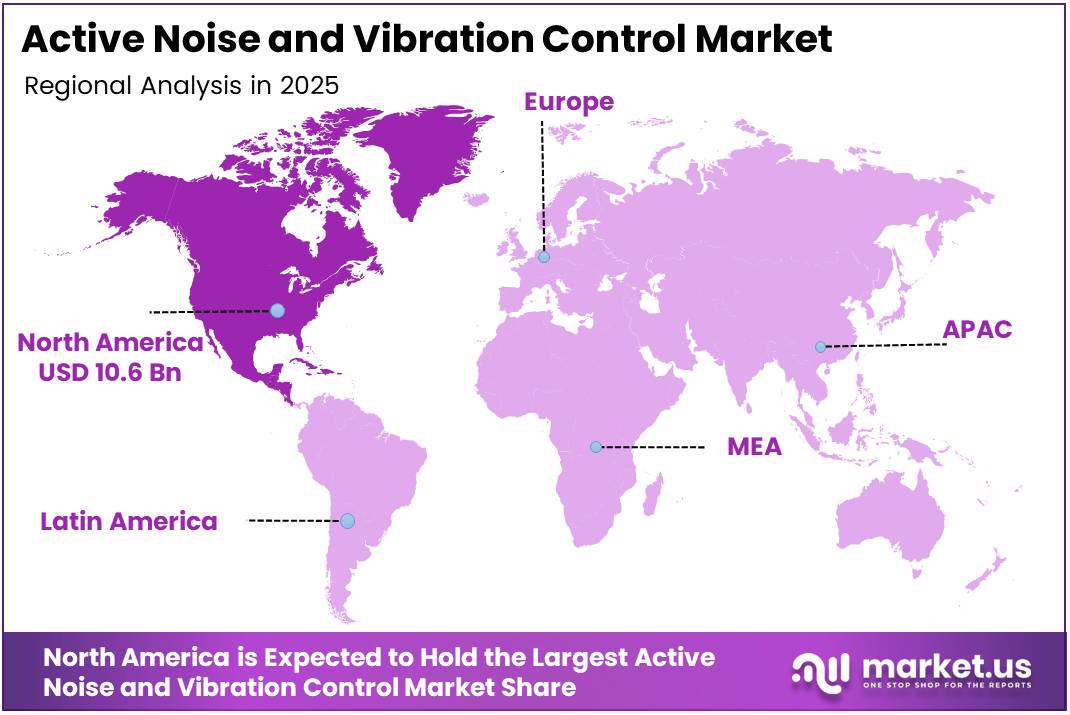

North America leads with a 43.80% share valued at USD 1.5 Billion, driven by dense commercial aviation infrastructure and early DoD mandates for low-signature platforms. This concentration of both commercial and defense demand in a single geography creates durable procurement pipelines for established systems integrators and positions the region as the benchmark for regulatory-driven adoption elsewhere.

Key Takeaways

- The global ANVC market reaches USD 3.6 Billion in 2025 and is forecast to reach USD 6.9 Billion by 2035.

- The market grows at a CAGR of 6.8% between 2026 and 2035.

- Active Noise Control (ANC) Systems lead by system type with a 65.9% share.

- Hardware leads the component segment with a 72.5% share.

- Commercial Aviation dominates the platform segment with a 56.3% share.

- North America holds the largest regional share at 43.80%, valued at USD 1.5 Billion.

System Type Analysis

Active Noise Control (ANC) Systems dominate with 65.9% due to mandatory cabin noise compliance requirements.

In 2025, Active Noise Control (ANC) Systems held a dominant market position in the By System Type segment of the Active Noise and Vibration Control Market, with a 65.9% share. Acoustic suppression addresses the most immediately measurable passenger experience metric — cabin decibel levels — which directly appear in aircraft certification documentation and airline procurement criteria. This linkage between acoustic performance and regulatory compliance entrenches ANC as the priority system type.

Active Vibration Control (AVC) Systems serve as the structural counterpart to acoustic management, targeting mechanical oscillation that originates in engines, rotors, and drivetrain components. AVC adoption is highest in rotorcraft and industrial machinery, where persistent vibration accelerates fatigue failure and increases maintenance intervals. However, AVC procurement typically follows ANC investment rather than preceding it, which explains its secondary position in the current revenue mix.

Component Analysis

Hardware dominates with 72.5% due to mandatory physical integration into platform structures.

In 2025, Hardware held a dominant market position in the By Component segment of the Active Noise and Vibration Control Market, with a 72.5% share. Sensors, actuators, and control electronics must be structurally embedded during aircraft manufacture or MRO overhaul — they cannot be retrofitted through software updates. This physical dependency creates long-tailed, platform-specific hardware procurement cycles that generate recurring revenue across the fleet lifecycle.

Software carries the highest growth potential within the component mix, as AI-driven adaptive algorithms increasingly replace fixed-parameter controllers. Software upgrades allow operators to improve noise suppression performance without hardware replacement, which reduces the cost of system improvement over time. However, software revenue currently remains subordinate because it flows through licensing agreements attached to hardware contracts rather than as standalone procurement.

Platform Analysis

Commercial Aviation dominates with 56.3% due to scale of fleet deployment and certification mandates.

In 2025, Commercial Aviation held a dominant market position in the By Platform segment of the Active Noise and Vibration Control Market, with a 56.3% share. Large commercial fleets — numbering in the thousands of frames — require ANVC systems across every aircraft, creating volume procurement that dwarfs other platform categories. Certification bodies in the US and EU mandate noise performance thresholds that OEMs must meet at type certification, locking in ANVC as a non-negotiable system.

Widebody aircraft represent the highest per-unit ANVC spend within commercial aviation because their larger cabins, more powerful engines, and longer routes set stricter acoustic performance expectations. Airlines position widebody cabin quiet as a premium differentiator on long-haul routes, which gives manufacturers commercial motivation — beyond regulatory compliance alone — to invest in advanced noise suppression architectures.

Narrowbody aircraft drive total ANVC unit volume because they represent the largest share of global commercial fleet count. While per-unit system complexity is lower than widebody, the sheer number of narrowbody frames in service and on order means narrowbody retrofits and OEM installations constitute the largest addressable volume segment within commercial aviation.

Regional Jets present a distinct ANVC challenge: smaller fuselage cross-sections concentrate engine and propeller noise closer to passenger seats, requiring targeted suppression solutions adapted to constrained installation space. This creates a specialized sub-segment with different technical requirements than mainline jets, supporting demand for purpose-engineered ANC solutions.

Military Aviation sources ANVC demand from requirements that go beyond passenger comfort — low acoustic and vibration signatures directly affect mission survivability and crew performance under sustained operational conditions. Defense procurement cycles are longer than commercial ones, but contract values per platform are substantially higher, and system specifications are classified, limiting competitive transparency.

Combat aircraft prioritize vibration suppression for avionics protection and pilot fatigue reduction during high-g maneuvers. Cockpit noise levels in fast jets exceed those of any commercial platform, making AVC systems mission-critical rather than comfort-oriented equipment.

Transport aircraft in military fleets carry personnel and cargo over extended missions, where crew fatigue from sustained noise and vibration exposure directly degrades operational effectiveness. Military transport operators face the same pressure as commercial airlines to reduce cabin noise levels, but procurement follows defense budget cycles rather than airline fleet renewal timelines.

Special Missions aircraft — including ISR, electronic warfare, and maritime patrol platforms — carry sensitive sensor arrays that require structural vibration isolation to maintain operational accuracy. ANVC systems on these platforms protect equipment performance, not just crew comfort, which positions them as mission-critical infrastructure rather than an amenity.

Helicopters in military service operate in the most acoustically hostile rotorcraft environment, with main rotor, tail rotor, and gearbox noise combining to produce broadband vibration across the entire airframe. Active vibration control is more structurally embedded in helicopter design than in fixed-wing platforms, making it a higher-value and more technically complex sub-segment.

General Aviation represents a smaller but structurally distinct demand pool, where buyers are private operators and charter companies who treat cabin noise performance as a product differentiation tool rather than a regulatory requirement. Consequently, ANVC adoption in general aviation is buyer-preference driven, making it sensitive to economic conditions in ways that commercial and military segments are not.

Business Jets carry the highest ANVC specification standards within general aviation because their operators use cabin quietness as a direct competitive selling point in aircraft marketing. Ultra-long-range business jet buyers increasingly specify acoustic performance benchmarks in purchase contracts, pulling ANC system requirements upstream into aircraft design decisions at OEM level.

Commercial Helicopters serving oil and gas, medical evacuation, and urban air taxi roles face growing pressure to reduce external and internal noise, particularly as urban operating licenses become tied to acoustic compliance thresholds. This regulatory dynamic in urban air mobility is beginning to converge with the ANVC requirements historically associated with fixed-wing commercial aviation.

Key Market Segments

By System Type

- Active Noise Control (ANC) Systems

- Active Vibration Control (AVC) Systems

By Component

- Hardware

- Software

By Platform

- Commercial Aviation

- Widebody

- Narrowbody

- Regional Jets

- Military Aviation

- Combat

- Transport

- Special Missions

- Helicopters

- General Aviation

- Business Jets

- Commercial Helicopters

Drivers

Tightening Noise Certification Standards and Passenger Comfort Expectations Compel Mandatory ANVC Investment

Aircraft manufacturers face certification requirements that set hard noise performance thresholds at the type approval stage. The Airbus A350 achieved certification at 22 EPNdB below ICAO Chapter 4 requirements and delivered a 50% noise footprint reduction versus previous-generation aircraft, according to Airbus. This performance level now functions as a competitive benchmark that OEMs across all commercial aircraft categories must demonstrate to buyers.

Passenger comfort expectations have consolidated around measurable cabin quiet as a baseline expectation on mainline routes. Airlines treat low cabin noise as a retention and premium pricing lever, which drives aircraft purchasers to specify ANVC system performance in fleet procurement contracts. This commercial pressure reinforces regulatory mandates, creating dual demand from both compliance requirements and buyer preference.

In March 2025, DLR validated that retrofitting eight noise reduction technologies onto a live A320 — including engine exhaust nozzle edge profiles, porous flap-edge materials, and partial landing gear fairings — reduced individual source noise by up to 6 dB. This retrofit validation expands the addressable ANVC market beyond new-build OEM programs to include the existing global fleet, adding a significant and previously underserved revenue segment for systems providers.

Restraints

High System Costs and Integration Complexity Limit ANVC Penetration Beyond Large Commercial and Defense Platforms

Active noise and vibration control systems require embedded sensors, actuators, and real-time processing hardware that add material cost to every platform installation. For smaller operators in general aviation and regional transport, this cost-benefit calculation frequently does not close — particularly when passive noise treatments offer partial acoustic improvement at a fraction of the investment required for full active systems.

Technical integration with existing mechanical and structural architectures creates a second barrier that cost alone does not capture. Retrofitting active control systems into airframes designed before these technologies matured demands structural analysis, certification re-approval, and often custom engineering for each platform variant. These engineering overheads multiply total project cost and extend timelines, reducing the commercial attractiveness of retrofit programs for smaller operators.

Together, these two constraints concentrate ANVC adoption among large commercial airlines, defense procurement agencies, and premium business aviation buyers — organizations with both the capital and the institutional engineering capacity to absorb integration complexity. This structural concentration limits total addressable market and creates ceiling effects on growth rates outside the core aviation and defense buyer segments.

Growth Factors

Electric Vehicle Platforms and EU Aviation Decarbonization Targets Create New Mandatory ANVC Demand Pools

Electric and hybrid vehicle powertrains eliminate combustion masking noise — the broadband engine sound that previously obscured higher-frequency motor and road noise in conventional vehicles. Without this masking effect, EV cabins expose passengers to noise signatures that conventional passive treatments cannot adequately suppress. This acoustic physics problem makes active noise cancellation a structural design requirement for EV platform comfort rather than an optional upgrade.

The EU Commission has set a target of reducing aircraft noise by 65% by 2050 compared to 2000 levels, according to DLR. This long-range policy commitment creates a 25-year demand pipeline for ANVC technology development and deployment across European aviation. For systems providers, this target converts regulatory aspiration into program-level engineering investment with defined performance milestones — a more durable demand signal than market preference alone.

Smart building and urban infrastructure applications add a third growth pathway outside transportation entirely. Acoustic comfort requirements in commercial real estate are now appearing in green building certification criteria, creating demand for IoT-integrated vibration monitoring and noise suppression systems in HVAC, mechanical plant, and structural isolation applications. This expansion into built environment use cases broadens the ANVC addressable market well beyond its aviation origins.

Emerging Trends

AI-Driven Adaptive Algorithms and Urban Air Mobility Standards Reshape ANVC System Architecture

Artificial intelligence integration replaces fixed-parameter noise controllers with systems that adapt in real time to changing acoustic environments — shifting altitude, varying payload, and evolving engine wear profiles. Adaptive algorithms learn platform-specific noise signatures and adjust suppression parameters continuously, delivering superior performance over the service life of the aircraft compared to controllers calibrated at certification. This shift moves ANVC software from static firmware to a managed, updatable asset.

In November 2025, AltoVolo unveiled an eVTOL aircraft designed to operate over 80% more quietly than conventional helicopters, with active vibration and noise minimization integrated into its core design. This development is significant because eVTOL operators must satisfy urban operating license requirements tied to acoustic thresholds — meaning noise performance is a market access condition, not a comfort feature. Early eVTOL designs that embed ANVC at the architecture level will set de facto standards that followers must match.

Piezoelectric actuator technology and lightweight noise control materials are reducing the mass penalty of active vibration suppression, which has historically constrained adoption on weight-critical platforms. Lighter ANVC system architectures make integration commercially viable for narrowbody aircraft and regional jets where every kilogram of system weight carries a direct fuel cost. This weight reduction trend progressively opens platform categories that previously could not justify the mass trade-off of full active systems.

Regional Analysis

North America Dominates the Active Noise and Vibration Control Market with a Market Share of 43.80%, Valued at USD 1.5 Billion

North America holds a 43.80% share of the global ANVC market, valued at USD 1.5 Billion. This position reflects a combination of the world’s largest commercial aviation fleet, mature FAA noise certification requirements, and concentrated DoD procurement for low-signature military platforms. These structural conditions sustain durable demand across both commercial and defense buyer segments simultaneously.

Europe Active Noise and Vibration Control Market Trends

Europe drives ANVC development through the EU Commission’s long-range aviation noise reduction mandate and active aerospace R&D investment via institutions including DLR. The LNATRA project — which validated 6 dB source noise reduction on a live A320 — was funded under this policy framework. European aviation OEMs embed ANVC requirements into aircraft programs at the design stage, creating sustained demand from both regulatory compliance and platform competitiveness objectives.

Asia Pacific Active Noise and Vibration Control Market Trends

Asia Pacific represents the fastest-expanding geography for ANVC demand, driven by fleet growth across China, India, and Southeast Asia, and by India’s expanding aircraft maintenance sector. In November 2025, ASI Global and Tata Projects signed an exclusive MoU to develop noise and vibration-compliant MRO hangars across India — a direct response to the country’s commercial, business aviation, and defense maintenance pipeline. This infrastructure investment signals that ANVC compliance requirements are now embedding into Asia Pacific MRO standards.

Middle East and Africa Active Noise and Vibration Control Market Trends

The Middle East sustains ANVC demand through Gulf carrier fleet expansion and defense procurement programs across Saudi Arabia and the UAE. Gulf airlines operate mixed widebody and narrowbody fleets on long-haul routes where cabin acoustic performance is a premium product differentiator. Defense spending across the region supports military aviation programs where ANVC systems serve operational rather than comfort functions.

Latin America Active Noise and Vibration Control Market Trends

Latin America represents an emerging ANVC market where adoption is primarily driven by fleet renewal at major Brazilian and Mexican carriers replacing older-generation narrowbody aircraft with current-production types that embed active noise systems as standard. Regulatory alignment with ICAO noise standards across the region progressively raises the certification floor for aircraft operations, pulling ANVC system requirements into fleet procurement decisions.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Moog Inc. positions itself at the intersection of precision motion control and active vibration suppression, supplying actuation systems to both commercial and defense aviation platforms. Its advantage in this market derives from decades of flight-critical hardware qualification — a certification history that creates high switching costs for OEM customers and structurally limits competition from newer entrants lacking equivalent regulatory track records.

Parker-Hannifin Corporation applies its motion and control systems expertise across the full ANVC value chain, integrating sensors, actuators, and electronic controllers within broader aircraft and industrial system architectures. Its strategic edge lies in systems-level integration capability: Parker can bundle ANVC components with hydraulic, pneumatic, and electromechanical subsystems, offering OEMs a consolidated supplier relationship that reduces integration complexity and program risk.

Ultra Precision Control Systems focuses on high-precision active vibration control for demanding platform environments where standard commercial solutions cannot meet specification requirements. Its positioning in specialist defense and aerospace applications insulates it from cost-driven displacement by broader industrial suppliers, but also concentrates its revenue in long-cycle defense programs that require sustained R&D investment to maintain technical differentiation.

Bosch General Aviation Technology GmbH brings Bosch’s electronics and sensor manufacturing scale to the general aviation ANVC segment, where cost per system carries greater procurement weight than in commercial or defense markets. Its competitive positioning centers on delivering aviation-grade noise and vibration control performance at cost structures compatible with the economics of business aviation and commercial helicopter operators — a value proposition that distinguishes it from defense-pedigree competitors.

Key Players

- Moog Inc.

- Parker-Hannifin Corporation

- Ultra Precision Control Systems

- Bosch General Aviation Technology GmbH

- Faurecia Creo AB

- HUTCHINSON S.A.

- Sensata Technologies, Inc.

- Analog Devices, Inc.

- Terma A/S

- Quiet Flight, LLC

Recent Developments

- 2024 (published 2025) — Experimental Active Noise Control testing in aircraft cabin settings, presented at DAGA 2024, demonstrated noise attenuation of 16.9 dB at the primary microphone position at a frequency of 200 Hz. This result confirms that active systems can address low-frequency engine and structural vibration modes that passive materials cannot resolve, establishing a performance benchmark for next-generation cabin ANC architectures.

- November 2025 — AltoVolo unveiled an electric vertical take-off and landing (eVTOL) aircraft designed to operate over 80% more quietly than conventional helicopters, with active vibration and noise minimization integrated into its core design. This development directly shapes acoustic standards for urban air mobility platforms seeking operating licenses in noise-restricted urban environments.

- November 2025 — ASI Global and Tata Projects signed an exclusive MoU to develop aircraft maintenance facility infrastructure across India, including noise and vibration-compliant MRO hangars. The agreement responds to India’s fast-growing aircraft maintenance demand across commercial aviation, business aviation, and defense sectors, embedding ANVC compliance requirements into the country’s expanding MRO infrastructure.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 3.6 Billion |

| Forecast Revenue (2035) | USD 6.9 Billion |

| CAGR (2026-2035) | 6.8% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By System Type (Active Noise Control Systems, Active Vibration Control Systems), By Component (Hardware, Software), By Platform (Commercial Aviation: Widebody, Narrowbody, Regional Jets; Military Aviation: Combat, Transport, Special Missions, Helicopters; General Aviation: Business Jets, Commercial Helicopters) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Moog Inc., Parker-Hannifin Corporation, Ultra Precision Control Systems, Bosch General Aviation Technology GmbH, Faurecia Creo AB, HUTCHINSON S.A., Sensata Technologies Inc., Analog Devices Inc., Terma A/S, Quiet Flight LLC |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |

Market")