Quick Navigation

- Report Overview

- Key Takeaways

- Role of Generative AI

- Investment and Business Benefits

- Regional Analysis

- Component Analysis

- Deployment Mode Analysis

- Application Analysis

- End-User Analysis

- Discipline Analysis

- Key Market Segments

- Emerging Trends

- Growth Factors

- Market Dynamics

- Key Players Analysis

- Recent Developments

- Report Scope

Report Overview

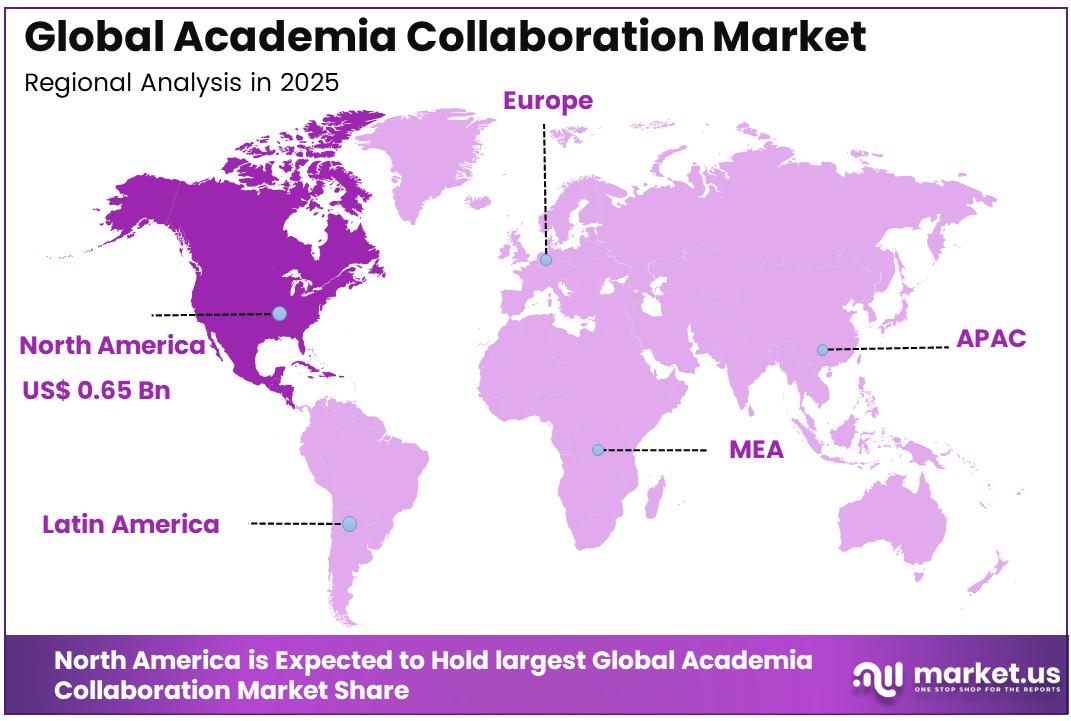

The Global Academia Collaboration Market size is expected to be worth around USD 5.82 billion by 2035, from USD 1.45 billion in 2025, growing at a CAGR of 14.9% during the forecast period from 2025 to 2035. North America held a dominant market position, capturing more than a 45.3% share, holding USD 0.65 billion in revenue.

Academia Collaboration refers to partnerships between universities, research institutions, and external organizations such as industries, government bodies, or nonprofits. These collaborations focus on shared research, knowledge exchange, skill development, and innovation. They help combine academic expertise with practical experience, improving learning outcomes, advancing research quality, and supporting real-world problem-solving across various sectors.

Top driving factors include rising pressure for demand-driven research and closer alignment with real industry problems. There is an increasing focus on resilient infrastructure and modern laboratories. Joint projects strengthen engineering facilities and innovation capacity, often improving capabilities by over 50% in several disciplines through shared equipment, advanced tools, and collaborative technical expertise.

The market for Academia Collaboration is driven by the growing need to connect education with real-world industry requirements and innovation goals. Institutions are focusing on practical learning, joint research, and skill development to improve outcomes. Increasing digital adoption, demand for interdisciplinary work, and support from public initiatives are also encouraging stronger partnerships across universities, research bodies, and organizations.

Demand is driven by widening skills gaps, where employers seek graduates with strong practical exposure. Academic and industry collaborations enable internships, co-created curricula, and applied research projects. These initiatives improve employability and job readiness, with institutional reviews indicating performance gains of more than 30% in graduate outcomes across several technical and professional fields.

For instance, in January 2026, Digital Science underscored the role of Figshare in open‑science collaboration, noting that new publisher partnerships make it easier for authors to share datasets alongside articles. This improves discovery, citation, and reuse of research outputs, which are all core to more open and collaborative academic ecosystems.

Key Takeaways

- In 2025, the Software/Platforms segment held a dominant market position, capturing a 78.3% share of the Global Academia Collaboration Market.

- In 2025, the Cloud-based segment held a dominant market position, capturing a 87.4% share of the Global Academia Collaboration Market.

- In 2025, the Research Project Management segment held a dominant market position, capturing a 41.7% share of the Global Academia Collaboration Market.

- In 2025, the Universities & Research Institutions segment held a dominant market position, capturing a 65.8% share of the Global Academia Collaboration Market.

- In 2025, the STEM segment held a dominant market position, capturing a 68.9% share of the Global Academia Collaboration Market.

- The U.S. Academia Collaboration Market was valued at USD 0.60 Billion in 2025, with a robust CAGR of 12.54%.

- In 2025, North America held a dominant market position in the Global Academia Collaboration Market, capturing more than a 45.3% share.

Role of Generative AI

Generative AI is becoming a routine academic tool, like education tool, with over 80% of university students now using it for coursework, compared with less than 10% before early 2023. Surveys show more than 86% of students rely on AI in studies, while nearly a quarter use it daily.

In research environments, generative AI is used to summarise literature, draft early sections, and organise data efficiently. It reduces time spent on repetitive tasks but raises concerns about originality. While it supports idea generation, it still lacks higher-level reasoning, keeping human judgment essential in research design.

Investment and Business Benefits

Investment opportunities are expanding in digital platforms, joint research centres, and specialised training programs. Shared funding for laboratories, testbeds, and pilot deployments reduces financial pressure on individual institutions. This collaborative approach can shorten innovation cycles by nearly 40% while also improving scalability, research efficiency, and the faster translation of ideas into commercial or industrial applications.

Business benefits from academia collaboration include faster innovation cycles and access to niche technical expertise. Companies gain a reliable talent pipeline, supporting productivity and competitiveness. Sponsored research and joint labs allow cost-efficient testing of technologies, while universities secure diversified funding and align education with evolving market needs, creating long-term ecosystem resilience.

Regional Analysis

In 2025, North America held a dominant market position in the Global Academia Collaboration Market, capturing more than a 45.3% share, holding USD 0.65 billion in revenue. This dominance is due to strong university research systems, well-established industry partnerships, and consistent public funding support. The region benefits from advanced digital infrastructure and a high focus on innovation, which encourages collaboration across institutions, startups, and enterprises, supporting continuous knowledge development and practical research outcomes.

For instance, in April 2025, Dropbox advanced its position in supporting higher‑education collaboration with enhancements to its Dash and education offerings, using AI to help research teams search, summarize, and organize fragmented content across apps, and building on Dropbox Education’s role in enabling universities to share datasets, co‑author papers, and manage research workflows securely across institutions.

U.S. Academia Collaboration Market Size

The market for Academia Collaboration within the U.S. is growing tremendously and is currently valued at USD 0.60 billion. The market has a projected CAGR of 12.54%. The market is growing due to stronger industry and university partnerships, rising focus on applied research, and increasing need for skilled graduates with practical experience. Institutions are investing in digital platforms, shared labs, and joint programs, which improve innovation outcomes and support workforce readiness across multiple sectors.

For instance, in February 2026, Slack continued to deepen its role in academic collaboration through educator-driven communities such as Remote Academia, which connects thousands of faculty and over 500 universities, including leading North American institutions like UC Berkeley and the University of Washington, to share best practices and coordinate remote and hybrid teaching and research workflows.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Component Analysis

In 2025, the Software/Platforms segment held a dominant market position, capturing a 78.3% share of the Global Academia Collaboration Market. This dominance is due to the growing reliance on digital tools that support communication, data sharing, and structured research workflows across institutions. Software platforms allow teams to collaborate in real time while managing documents, timelines, and outputs in one place, improving coordination and consistency in academic projects.

Software solutions also help institutions streamline administrative processes and maintain compliance with research standards. They support transparency, reporting, and knowledge exchange between departments and external partners. As collaboration becomes more complex, these platforms provide a stable foundation that supports efficient and organised academic partnerships.

For instance, in October 2024, Elsevier deepened its collaboration with Times Higher Education, supplying data from Scopus and SciVal to support new ranking and evaluation products for universities. These kinds of integrated platforms help institutions analyse collaboration patterns and research performance in the same ecosystem where they plan and manage projects, lifting demand for software-centric solutions.

Deployment Mode Analysis

In 2025, the Cloud-Based segment held a dominant market position, capturing a 87.4% share of the Global Academia Collaboration Market. This dominance is due to the increasing need for flexible access to systems that support remote collaboration and distributed research teams. Cloud-based models allow users to access platforms from any location, making it easier for institutions to connect researchers, students, and partners across different regions.

Cloud deployment also reduces dependency on physical infrastructure and simplifies system maintenance for universities. It supports faster updates, scalability, and secure data sharing, which are important for ongoing research activities. This approach aligns well with the digital transformation seen across modern academic environments and collaborative learning systems.

For instance, in February 2025, Microsoft continued to enhance its cloud collaboration stack with AI-powered features across Microsoft 365 and Teams, including smarter meeting summaries and tighter links between chat, storage, and project spaces. For academic users, these improvements make cloud-based tools more attractive than older on-campus systems, especially when teams are split across locations.

Application Analysis

In 2025, the Research Project Management segment held a dominant market position, capturing a 41.7% share of the Global Academia Collaboration Market. This dominance is due to the growing complexity of academic research projects that involve multiple stakeholders, timelines, and compliance requirements. Project management tools help organise tasks, track progress, and ensure that research activities remain aligned with objectives and institutional standards.

These systems also improve accountability and communication among research teams. They allow better monitoring of deliverables, resource use, and reporting processes. As collaborations increase across institutions and disciplines, structured project management becomes essential for maintaining efficiency and achieving successful research outcomes.

For instance, in May 2025, updates across the Microsoft ecosystem, including Planner, Project, and integrations with Teams, focused on clearer timelines, automation, and better support for complex projects. Research offices can use these tools to track tasks, deliverables, and communication in one place, so collaboration platforms that embed project management become more appealing.

End-User Analysis

In 2025, the Universities & Research Institutions segment held a dominant market position, capturing a 65.8% share of the Global Academia Collaboration Market. This dominance is due to the central role of universities and research institutions in generating knowledge and leading collaborative initiatives. These organisations bring together faculty, students, and external partners, creating an environment where research and innovation can develop through shared expertise and resources.

They also manage funding, infrastructure, and academic programs, which requires strong coordination and collaboration systems. Their responsibility for research output and education makes them the primary users of collaboration platforms, ensuring that projects are well managed and aligned with both academic and industry needs.

For instance, in January 2024, Elsevier also partnered with Cactus Communications so millions of article abstracts could be surfaced through a mobile discovery app used by researchers worldwide. Easier discovery feeds back into how academics collaborate, pushing universities to invest in tools that connect literature search, networking, and shared workspaces for their research communities.

Discipline Analysis

In 2025, the STEM segment held a dominant market position, capturing a 68.9% share of the Global Academia Collaboration Market. This dominance is due to the strong focus on innovation, experimentation, and problem-solving within the science and engineering fields. STEM disciplines often require access to specialised equipment, technical knowledge, and collaborative research environments, making them highly dependent on structured academic partnerships.

These fields also address complex global challenges that require interdisciplinary approaches and shared expertise. Collaboration in STEM supports faster discovery, improved research quality, and practical application of knowledge. As a result, these disciplines naturally lead to adopting and expanding academic collaboration models.

For instance, in August 2024, the US National Science Foundation highlighted new initiatives around emerging STEM areas, including integrating AI and advanced methods across disciplines. These programs often require cross-team and cross-institution collaboration, which nudges STEM groups to adopt digital platforms that can handle complex, data-rich projects.

Key Market Segments

By Component

- Software/Platforms

- Services

By Deployment Mode

- Cloud-based

- On-premises

By Application

- Research Project Management

- Academic Writing & Co-authoring

- Data Sharing & Management

- Virtual Conferences & Networking

- Grant & Funding Collaboration

- Others

By End-User

- Universities & Research Institutions

- Individual Researchers & Faculty

- Academic Societies & Associations

- Government & Public Research Bodies

- Others

By Discipline

- STEM (Science, Technology, Engineering, Mathematics)

- Humanities & Social Sciences

- Interdisciplinary Research

- Others

Emerging Trends

Universities are increasingly adopting AI-supported personalised learning systems that adjust pace, difficulty, and feedback for each student. Around 30–55% of institutions already use adaptive learning tools and AI tutors. These systems are improving engagement and learning outcomes, encouraging broader acceptance among faculty and academic administrators.

Another trend is the expansion of AI-driven services beyond classrooms, including chatbots, automated grading, and learning analytics. Current adoption levels for these solutions range between 25–50% across institutions. These tools help universities streamline operations while improving student experience and enabling early identification of at-risk learners.

Growth Factors

The rapid adoption of generative AI is supported by its ease of use and accessibility. Many students see it as a low-effort, high-utility tool that complements their work. When AI tools are perceived as time-saving and supportive, continued usage increases, driving steady and organic growth across academic institutions.

The shift from less than 10% to over 80% student usage within a short period highlights strong peer influence in academic settings. As faculty introduce AI literacy programs and institutions integrate AI into learning platforms, adoption barriers continue to reduce, supporting long-term growth and wider institutional acceptance.

Market Dynamics

Drivers - Rising Need to Bridge Skills and Innovation Gaps

Academic collaboration is expanding because industries need graduates who can work with practical knowledge, technical confidence, and problem-solving ability. Universities are responding by building closer ties with external partners. These collaborations help connect classroom learning with real work settings, making education more relevant to changing economic and research needs.

It also supports innovation by allowing researchers, students, and industry experts to work together on shared challenges. This creates stronger links between ideas and application. Institutions can improve learning outcomes while helping businesses access fresh thinking, research support, and a more prepared future workforce.

For instance, in April 2024, Elsevier worked with Eindhoven University of Technology to explore the idea of a fourth-generation university that is deeply integrated with its regional innovation ecosystem. The collaboration focuses on how universities can link education, research, and industry partners more tightly, helping students gain practical skills while supporting local companies with advanced knowledge and data insights.

Restraint - Institutional Misalignment

A major restraint in this market is the difference in priorities between academic institutions and external partners. Universities often focus on long-term knowledge creation, while businesses usually seek faster outcomes and direct commercial value. This difference can slow planning, communication, and decision-making in collaborative efforts.

Institutional processes can also create friction when approvals, funding rules, and internal structures are not designed for flexible partnerships. In many cases, collaboration becomes difficult not because interest is missing, but because both sides operate with different timelines, expectations, and measures of success.

For instance, in November 2025, Springer Nature extended its partnership with Research4Life to include access to protocols.io for researchers in many lower-income countries. The move addresses inequities in access to methods and tools, yet also highlights persistent structural gaps in funding, infrastructure, and policy that still limit how evenly collaboration benefits are shared worldwide.

Opportunities - Expansion of Digital Collaboration

Digital collaboration creates a strong opportunity for this market by making it easier for institutions to work across locations and disciplines. Online platforms support virtual meetings, shared research spaces, document exchange, and joint project tracking. This helps academic partnerships continue smoothly without being limited by physical distance.

The growing use of digital tools also supports wider participation from students, faculty, and external organisations. Institutions can build stronger research networks, improve access to knowledge, and manage collaborative work more efficiently. This makes digital systems an important enabler for future academic partnership growth and broader engagement.

For instance, in January 2025, Taylor & Francis renewed an open research agreement with Jisc in the United Kingdom, expanding open access publishing routes across thousands of journals. The deal helps universities coordinate digital publishing, promotes open research practices, and offers humanities and social science scholars more opportunities to collaborate and share results globally.

Challenges - Managing Complexity

Managing complexity remains a major challenge because academic collaboration often involves multiple institutions, departments, and outside partners. Each group may have different processes, goals, and responsibilities. This makes coordination more difficult and increases the effort needed to keep projects aligned, timely, and productive throughout the partnership cycle.

Complexity also affects communication, governance, and decision-making. When roles are not clearly defined, delays and confusion can emerge during project execution. Institutions must balance academic standards, partner expectations, and administrative requirements at the same time. Without strong coordination, collaboration can become slower and less effective.

For instance, in March 2026, Digital Science announced a partnership with HERSA in the United Kingdom to strengthen research security and integrity for universities. The collaboration responds to growing complexity around compliance, risk, and responsible data use, helping institutions manage multi-stakeholder projects while balancing openness with stricter demands on security and trust.

Key Players Analysis

One of the leading players, in July 2025, Wiley entered a strategic partnership with Anthropic to connect Wiley’s peer‑reviewed content directly into AI tools via the Model Context Protocol. The pilot will give universities more seamless access to trusted articles inside AI assistants, aiming to keep high‑quality literature at the core of AI‑driven research workflows.

Top Key Players in the Market

- Elsevier, Ltd.

- Digital Science & Research Solutions, Ltd.

- Springer Nature

- Clarivate plc

- John Wiley & Sons, Inc.

- Taylor & Francis Group

- Slack Technologies, LLC

- Microsoft Corporation

- Google LLC

- Dropbox, Inc.

- Open Science Framework

- Zotero

- F1000 Research, Ltd.

- Morressier

- AcademicPub (an Ingenta company)

- Others

Recent Developments

- In March 2025, Digital Science launched its Dimensions Industry Partnerships dashboard to help universities map and grow collaboration with companies, using rich data on funding, IP, and researcher networks. The tool gives tech‑transfer and research offices a clearer view of where to invest and whom to partner with, tightening the link between academia and industry.

- In January 2025, Dutch universities and research institutes renewed and expanded their national agreement with Elsevier, combining reading rights on ScienceDirect with 100% open‑access publishing in eligible journals. The deal also covers Scopus access and clearer rules for text‑and‑data mining, giving Dutch researchers a more open, interoperable collaboration environment.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 1.45 Billion |

| Forecast Revenue (2035) | USD 5.82 Billion |

| CAGR (2026-2035) | 14.9% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Component (Software, Services), By Deployment Mode (Cloud-based, On-premises), By Application (Research Project Management, Academic Writing & Co-authoring, Data Sharing & Management, Virtual Conferences & Networking, Grant & Funding Collaboration, Others), By End-User (Universities & Research Institutions, Individual Researchers & Faculty, Academic Societies & Associations, Government & Public Research Bodies, Others), By Discipline (STEM (Science, Technology, Engineering, Mathematics), Humanities & Social Sciences, Interdisciplinary Research, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Elsevier, Ltd., Digital Science & Research Solutions, Ltd., Springer Nature, Clarivate plc, John Wiley & Sons, Inc., Taylor & Francis Group, Slack Technologies, LLC, Microsoft Corporation, Google LLC, Dropbox, Inc., Open Science Framework, Zotero, F1000 Research, Ltd., Morressier, AcademicPub (an Ingenta company), Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |