Quick Navigation

- Report Overview

- Key Takeaways

- Type Analysis

- Radar Architecture Analysis

- Component Analysis

- Deployment Mode Analysis

- Frequency Band Analysis

- Application Analysis

- Key Market Segments

- Drivers

- Restraints

- Growth Factors

- Emerging Trends

- Regional Analysis

- Key Regions and Countries

- Key Company Insights

- Recent Developments

- Report Scope

Report Overview

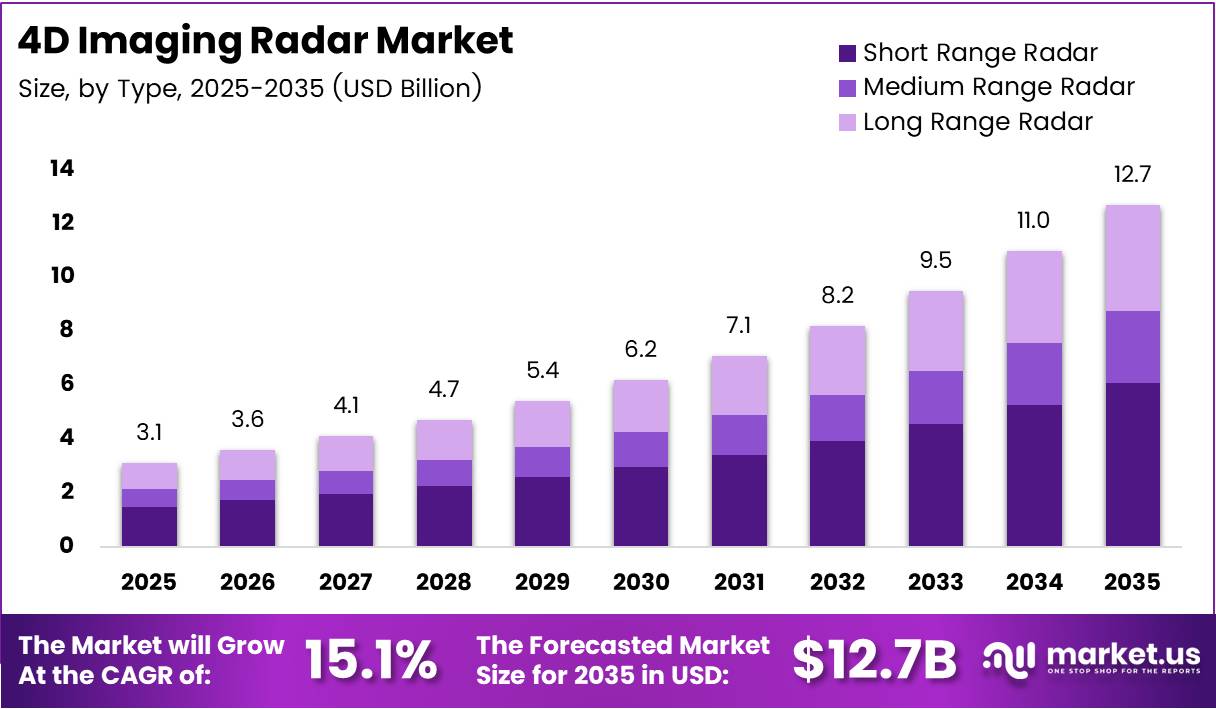

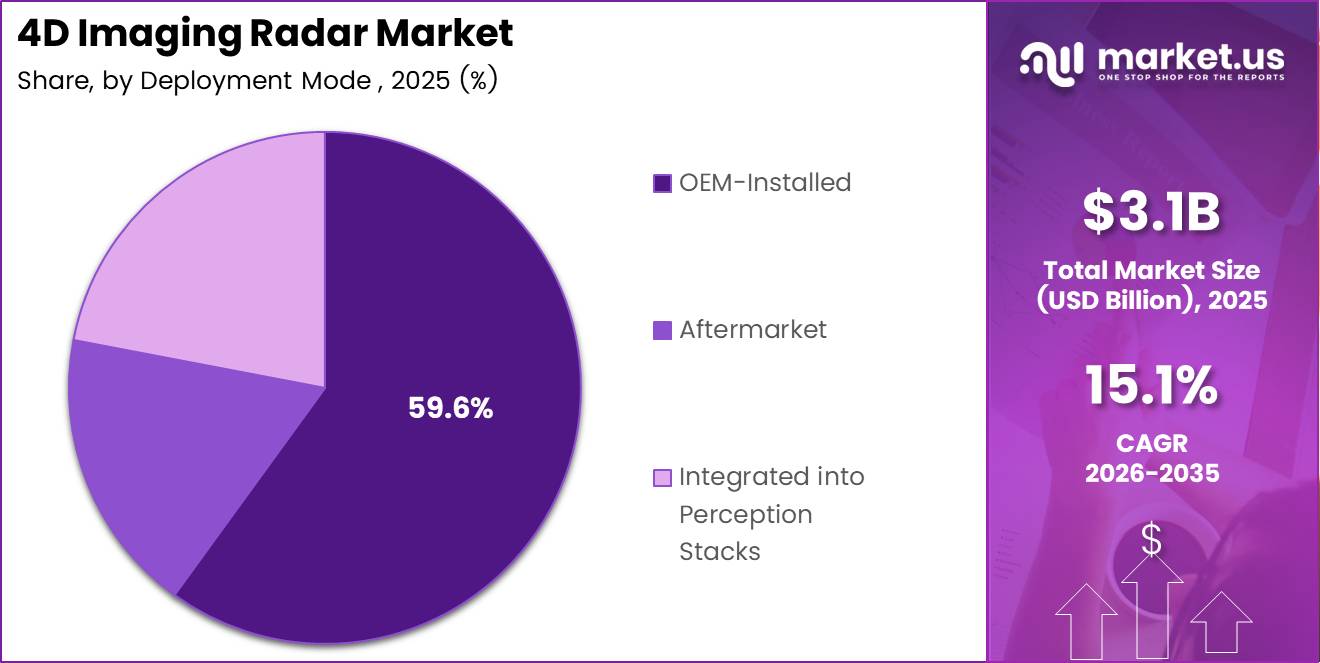

Global 4D Imaging Radar Market size is expected to be worth around USD 12.7 Billion by 2035 from USD 3.1 Billion in 2025, growing at a CAGR of 15.1% during the forecast period 2026 to 2035.

4D imaging radar technology delivers simultaneous measurement of range, velocity, azimuth, and elevation in a single sensor pass. This capability separates it from conventional radar, which captures only two or three of these dimensions. Automotive OEMs, defense contractors, and smart infrastructure operators now treat 4D radar as a core perception layer rather than a supplementary sensor.

The automotive sector is the primary commercial driver of this market. Advanced driver assistance systems require precise object classification at highway speeds, and camera-LiDAR combinations still struggle in rain, fog, and dust. 4D radar addresses this gap directly. Automakers are embedding these sensors at the design stage, not retrofitting them, which signals a structural shift in vehicle architecture.

Regulatory pressure is accelerating hardware adoption across major markets. The US National Highway Traffic Safety Administration and Euro NCAP have both tightened mandatory collision avoidance requirements. Manufacturers unable to meet these standards face market access restrictions. Radar hardware suppliers with production-ready solutions hold a clear commercial advantage as these deadlines approach.

Defense and aerospace agencies are allocating capital toward high-resolution imaging radar for unmanned systems, border surveillance, and low-altitude threat detection. These programs require sensors that perform reliably under electronic countermeasures and adverse weather. The defense segment represents a less price-sensitive demand base, which supports higher-margin contracts for specialized radar manufacturers.

Smart city and traffic monitoring deployments are expanding the non-automotive revenue base. Urban mobility planners use 4D radar to measure pedestrian flow, vehicle speed, and intersection occupancy in real time. This application does not require automotive-grade certifications, which shortens deployment cycles and opens procurement to a wider set of vendors.

According to research published via arxiv.org, the 2025 R2LDM framework increased 4D radar point-cloud density by 6-fold to 10-fold using latent diffusion modeling. This means sensor hardware with limited physical resolution can now produce data quality previously achievable only by physically larger, more expensive arrays, effectively lowering the cost floor for high-performance radar deployment.

According to research published via link.springer.com, RadarNeXt achieved more than 67 FPS on an NVIDIA RTX A4000 GPU for real-time 4D imaging radar perception in 2025. This processing throughput confirms that real-time 4D radar inference is now commercially viable on hardware already embedded in production vehicle platforms, removing a major technical barrier to mass-market deployment.

Key Takeaways

- The global 4D Imaging Radar Market was valued at USD 3.1 Billion in 2025 and is forecast to reach USD 12.7 Billion by 2035.

- The market advances at a CAGR of 15.1% during the 2026 to 2035 forecast period.

- North America leads all regions with a 43.60% market share, valued at USD 1.3 Billion in 2025.

- By Type, Short Range Radar holds the dominant position with a 43.7% share in 2025.

- By Radar Architecture, Frequency Modulated Continuous Wave (FMCW) accounts for 37.2% of the market.

- By Component, Radar SoC / RFIC leads with a 32.8% share in 2025.

- By Deployment Mode, OEM-Installed accounts for 59.6% of all deployments.

- By Frequency Band, the 77-81 GHz band holds a 38.3% share.

- By Application, Automotive leads with a 63.7% share of total market revenue.

Type Analysis

Short Range Radar dominates with 43.7% due to high ADAS integration volumes.

In 2025, Short Range Radar held a dominant market position in the By Type segment of the 4D Imaging Radar Market, with a 43.7% share. Near-field detection requirements in automated parking, blind-spot monitoring, and low-speed collision avoidance systems generate consistent volume demand. This segment benefits directly from OEM mandates requiring sensor coverage at close proximity ranges.

Medium Range Radar serves the mid-field detection zone critical for lane-change assistance and cross-traffic alerts. Automakers deploying full-coverage sensor rings use medium range units to bridge the gap between short and long range arrays. Demand in this segment tracks closely with the rollout of SAE Level 2+ vehicles across North America, Europe, and China.

Long Range Radar addresses highway-speed following distance control and forward collision warning at ranges exceeding 200 meters. This sub-segment carries higher per-unit value and aligns with premium vehicle platforms. In April 2025, HiRain Technologies launched the LRR615 long-range 4D imaging radar system based on Arbe’s chipset, marking China’s first radar system using a high-density waveguide antenna for OEM evaluation.

Radar Architecture Analysis

Frequency Modulated Continuous Wave (FMCW) dominates with 37.2% due to mature production infrastructure.

In 2025, Frequency Modulated Continuous Wave (FMCW) held a dominant market position in the By Radar Architecture segment of the 4D Imaging Radar Market, with a 37.2% share. FMCW architecture offers simultaneous range and velocity measurement with lower power consumption than pulsed alternatives. Automotive Tier 1 suppliers have standardized on FMCW-based designs, creating a deep supply chain and predictable cost structure.

Multiple-Input Multiple-Output (MIMO) architecture expands the effective aperture of radar arrays without requiring physically larger antennas. This makes MIMO particularly valuable in constrained packaging environments such as automotive bumpers and rooflines. Sensor vendors combining MIMO with 4D imaging achieve angular resolution improvements that shift radar performance closer to LiDAR-grade outputs.

Digital Beamforming (DBF) enables real-time electronic steering of radar beams across wide fields of view. Defense and traffic monitoring programs favor DBF architectures because they eliminate mechanical scanning components. According to research published via link.springer.com, RadarNeXt achieved 28.40 FPS on Jetson AGX Orin embedded hardware in 2025, confirming that DBF-based perception models can meet real-time requirements on compact embedded platforms.

Doppler Radar specializes in velocity-first detection scenarios, including pedestrian speed profiling and cyclist tracking in urban environments. Traffic management operators deploy Doppler units at intersections where instantaneous velocity data takes priority over full 3D mapping. This architecture holds a defensible niche in smart city infrastructure contracts.

Synthetic Aperture Radar (SAR) delivers the highest spatial resolution of any radar modality by synthesizing a large virtual antenna aperture from a moving platform. Aerospace and defense agencies apply SAR in reconnaissance drones and surveillance satellites. This sub-segment commands premium pricing and operates largely outside automotive cost pressures.

Component Analysis

Radar SoC / RFIC dominates with 32.8% due to tight integration of processing and RF functions.

In 2025, Radar SoC / RFIC held a dominant market position in the By Component segment of the 4D Imaging Radar Market, with a 32.8% share. Monolithic integration of RF front-end and signal processing on a single chip reduces bill-of-materials cost and improves power efficiency. This consolidation trend gives SoC suppliers strong design-win leverage with automotive OEMs specifying next-generation radar platforms.

Antenna-in-Package (AiP) technology embeds antenna arrays directly within the chip package, enabling millimeter-wave radar modules with a significantly smaller footprint. AiP adoption accelerates as OEMs demand sensors that fit within tight body panel tolerances. This component category is central to the miniaturization roadmaps of most automotive radar programs.

Transceivers handle the signal conversion between digital processing cores and physical antenna elements. High-channel-count radar architectures require transceivers with low phase noise and tight synchronization across multiple transmit-receive pairs. Transceiver performance directly limits the angular resolution ceiling of any 4D radar system.

Software components encompass the signal processing algorithms, object classification models, and sensor abstraction layers that transform raw radar data into actionable perception outputs. Software differentiation is increasingly where radar vendors compete, as hardware specifications across competing platforms converge. Vendors with proprietary AI-based classification pipelines command higher licensing margins.

Embedded Systems provide the compute fabric that runs radar processing workloads at the edge, inside the vehicle or infrastructure node. Low-latency embedded processing is a hard requirement for safety-critical ADAS functions. This component segment benefits as radar channel counts increase and raw data volumes outpace what can be offloaded to central compute modules.

Deployment Mode Analysis

OEM-Installed dominates with 59.6% due to factory-stage integration mandates.

In 2025, OEM-Installed held a dominant market position in the By Deployment Mode segment of the 4D Imaging Radar Market, with a 59.6% share. Automakers embedding radar at the assembly stage control sensor placement, calibration, and software integration from the outset. This approach reduces post-sale warranty exposure and enables tighter coupling between radar outputs and vehicle control systems.

Aftermarket deployment addresses retrofit demand for commercial fleet operators, logistics companies, and older vehicle cohorts that lack factory-installed radar. Aftermarket units face tighter constraints on installation accuracy and recalibration, which limits performance relative to OEM-integrated systems. However, the large global installed base of pre-radar commercial vehicles sustains a durable aftermarket revenue stream.

Integrated into Perception Stacks represents the most software-intensive deployment model, where radar data feeds directly into a centralized AI perception platform alongside camera, LiDAR, and ultrasonic inputs. Autonomous vehicle developers and robotaxi operators favor this model because it allows continuous over-the-air updates to radar processing logic without hardware changes.

Frequency Band Analysis

77-81 GHz dominates with 38.3% due to superior resolution and regulatory allocation.

In 2025, the 77-81 GHz band held a dominant market position in the By Frequency Band segment of the 4D Imaging Radar Market, with a 38.3% share. Regulators in the US, EU, and China have all allocated this band specifically for automotive radar use. The wider bandwidth available at 77-81 GHz directly enables the finer range resolution that 4D imaging radar requires to separate closely spaced objects.

The 76-77 GHz sub-band supports legacy long-range automotive radar installations and continues in production for platforms requiring backward compatibility with existing vehicle architectures. This band remains relevant for commercial vehicle applications where total cost of ownership takes priority over peak resolution performance.

The 60 GHz band serves short-range indoor and vehicular proximity detection applications. Parking assistance systems and in-cabin gesture recognition modules use 60 GHz sensors because the higher atmospheric absorption at this frequency naturally limits interference range. This band is less relevant for highway-speed detection but holds a defensible niche in low-range applications.

The 24 GHz band represents the oldest commercially deployed automotive radar frequency. Regulatory phase-out programs in Europe and North America are progressively retiring 24 GHz narrow-band radar allocations. New design wins at 24 GHz are limited, and suppliers are actively migrating existing customers to 77 GHz platforms.

Application Analysis

Automotive dominates with 63.7% due to ADAS mandates and autonomous vehicle programs.

In 2025, Automotive held a dominant market position in the By Application segment of the 4D Imaging Radar Market, with a 63.7% share. Collision avoidance regulations and consumer safety ratings directly link vehicle sales performance to radar capability. Every new vehicle platform designed for the US, European, or Chinese market now includes radar as a non-negotiable sensor requirement at the platform engineering stage.

Aerospace and Defense applications use 4D imaging radar for drone detection, low-altitude surveillance, and targeting systems where camera and infrared sensors are compromised by environmental conditions. Defense procurement cycles are longer than automotive, but contract values per unit are substantially higher. This segment provides revenue stability that offsets automotive volume fluctuations.

Security and Surveillance deployments cover perimeter monitoring, border security, and critical infrastructure protection. 4D radar outperforms traditional video surveillance in low-visibility conditions, which makes it the preferred sensor for outdoor security installations. Government procurement programs in this segment show multi-year contract structures, reducing customer churn risk for vendors.

Traffic Monitoring and Management applications deploy 4D radar at intersections, highway gantries, and toll plazas to count vehicles, measure speeds, and classify traffic by type. Municipal and highway authorities prefer radar over cameras for all-weather reliability. This segment generates recurring infrastructure upgrade contracts across North America, Europe, and the Middle East.

Others encompasses industrial automation, agricultural vehicle guidance, and maritime navigation applications. These verticals are early-stage relative to automotive but benefit from the cost reductions that high-volume automotive production drives into the radar component supply chain.

Key Market Segments

By Type

- Short Range Radar

- Medium Range Radar

- Long Range Radar

By Radar Architecture

- Multiple-Input Multiple-Output (MIMO)

- Digital Beamforming (DBF)

- Frequency Modulated Continuous Wave (FMCW)

- Doppler Radar

- Synthetic Aperture Radar

By Component

- Radar SoC / RFIC

- Antenna-in-Package (AiP)

- Transceivers

- Software

- Embedded Systems

By Deployment Mode

- OEM-Installed

- Aftermarket

- Integrated into Perception Stacks

By Frequency Band

- 24 GHz

- 60 GHz

- 76-77 GHz

- 77-81 GHz

By Application

- Automotive

- Aerospace and Defense

- Security and Surveillance

- Traffic Monitoring and Management

- Others

Drivers

Mandatory Collision Avoidance Regulations and ADAS Adoption Are Directly Expanding Radar Hardware Procurement

Automotive safety regulators across the US, EU, and China now mandate collision warning and avoidance systems as standard equipment on new vehicles. These requirements are not voluntary targets. They carry market access consequences for OEMs that miss compliance deadlines, which turns regulatory timelines directly into hardware purchase orders for radar suppliers.

The push toward SAE Level 2 and Level 3 automation creates a parallel procurement channel alongside regulatory compliance. Automakers building highway pilot and urban autopilot features require radar capable of distinguishing pedestrians, cyclists, and stationary objects simultaneously. Conventional two-dimensional radar cannot meet this classification requirement, which forces a hardware upgrade cycle across active vehicle programs.

According to research published via link.springer.com, RadarNeXt achieved more than 50 mAP on the View-of-Delft dataset using 4D radar point clouds in 2025 evaluations. This detection accuracy benchmark demonstrates that 4D radar now delivers object classification performance previously associated with LiDAR, validating the technology for safety-critical ADAS functions. In July 2025, Sensrad began delivering its first radar series powered by Arbe’s chipset for autonomous off-road defense vehicles and intelligent road infrastructure, confirming that production-grade hardware is reaching end customers.

Restraints

High Development Costs and Signal Processing Complexity Limit Adoption Speed Among Smaller Tier 2 Suppliers

Developing a production-ready 4D imaging radar system requires investment across RF chip design, antenna engineering, signal processing algorithms, and automotive-grade validation testing. Each layer carries significant capital requirements. Smaller Tier 2 suppliers cannot self-fund this development cycle, which concentrates supply capability among a narrow group of well-capitalized vendors and slows overall market velocity.

Sensor calibration accuracy presents a persistent technical barrier at scale. 4D radar systems require precise alignment between transmit and receive antenna arrays, and any manufacturing variation degrades elevation accuracy. High-volume production lines that maintain tight calibration tolerances require specialized equipment and process controls, adding cost at exactly the point where automotive customers apply the most price pressure.

According to research published via arxiv.org, the 2025 R2LDM framework improved point-cloud registration recall rates by up to 31.7%. The fact that a dedicated research program was necessary to achieve this improvement confirms that signal processing complexity in 4D radar remains an active engineering problem, not a solved one. Vendors without the resources to pursue this level of algorithmic development will find their hardware performance ceiling lower than market requirements.

Growth Factors

Autonomous Commercial Vehicles, Defense Programs, and AI-Enhanced Radar Classification Are Creating New Revenue Streams Beyond Passenger Cars

Autonomous trucking, robotaxi, and last-mile delivery programs demand sensor arrays that operate continuously under all weather conditions. These commercial autonomy platforms purchase radar in higher channel configurations than passenger vehicles and replace hardware on shorter technology refresh cycles. This procurement pattern generates higher per-platform revenue and sustains supplier margins above passenger vehicle averages.

Defense and aerospace agencies fund 4D radar programs that require imaging performance beyond automotive specifications. Drone counter-measures, perimeter surveillance, and airborne reconnaissance applications all specify sensors that can resolve small, slow-moving targets in cluttered environments. These contracts carry multi-year terms and performance-based renewal clauses, providing revenue visibility that automotive spot pricing does not.

According to research published via arxiv.org, the 2025 R2LDM framework improved downstream object-detection accuracy by up to 24.9% through AI-driven point-cloud enhancement. This accuracy gain means radar hardware already deployed in vehicles can deliver meaningfully better classification outputs through a software update alone. In October 2025, Aptiv unveiled its Gen-8 radar lineup, doubling channel count from the previous generation, confirming that hardware improvements are compounding alongside software-driven gains to create a widening performance gap over older sensor generations.

Emerging Trends

Semiconductor Advances and Strategic OEM-Supplier Partnerships Are Consolidating the 4D Radar Technology Stack Around a Smaller Set of Platform Providers

The 77-79 GHz frequency band is becoming the de facto standard for high-performance automotive radar platforms. Semiconductor manufacturers are concentrating 4D radar chip development in this band because it offers the best available combination of range resolution, regulatory clearance, and antenna packaging density. Vendors outside this band face growing headwinds as OEM platform architectures standardize around 77-81 GHz designs.

Strategic partnerships between radar chip suppliers and automotive OEMs are shifting from component transactions to co-development agreements. This changes the competitive dynamic. Suppliers embedded in an OEM’s design process gain influence over platform specifications, which creates durable switching barriers for competitors. Vendors without a co-development relationship at a major OEM face a growing risk of being locked out of future platform generations.

According to research published via arxiv.org, the 2025 4DR P2T study achieved an average PSNR of 30.39 dB for 4D radar tensor synthesis. This image reconstruction quality metric indicates that AI-generated radar data now reaches fidelity levels sufficient for sensor simulation and training data generation. Early movers who integrate synthetic radar data pipelines into their AI development workflows will compress test cycles significantly, reaching production validation faster than competitors relying solely on physical test drives.

Regional Analysis

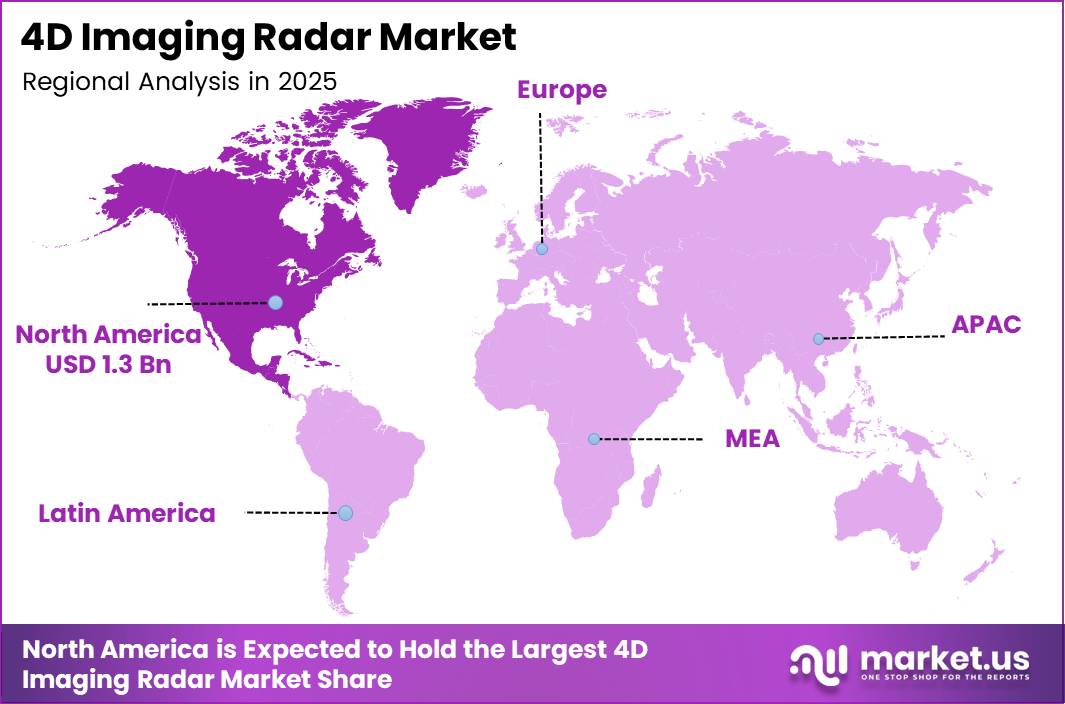

North America Dominates the 4D Imaging Radar Market with a Market Share of 43.60%, Valued at USD 1.3 Billion

North America holds the largest share of the global 4D imaging radar market at 43.60%, anchored by a USD 1.3 Billion valuation in 2025. The region benefits from concentrated autonomous vehicle development programs, stringent NHTSA collision avoidance mandates, and active defense radar procurement through DARPA and DoD agencies. US-based automotive OEMs and Tier 1 suppliers drive consistent hardware demand across both passenger and commercial vehicle programs.

Europe 4D Imaging Radar Market Trends

Europe maintains a strong position in 4D radar development, driven by Euro NCAP’s progressive radar requirement upgrades and the region’s established automotive engineering base in Germany. European OEMs and Tier 1 suppliers have embedded radar into vehicle safety architectures ahead of many global peers. Regulatory timelines for automated lane-keeping and emergency braking systems continue to pull forward hardware procurement decisions.

Asia Pacific 4D Imaging Radar Market Trends

Asia Pacific represents the fastest-expanding production and consumption base for 4D imaging radar. China’s domestic OEM programs, supported by government industrial policy favoring electric and autonomous vehicles, generate large-volume radar procurement. Japan and South Korea contribute through established automotive supplier networks. China’s radar supply chain localization efforts are creating competitive domestic alternatives to Western suppliers across multiple segments.

Latin America 4D Imaging Radar Market Trends

Latin America is an early-stage market for 4D imaging radar, with adoption concentrating in premium vehicle imports and commercial fleet safety upgrades. Brazil and Mexico host the region’s largest automotive assembly operations, which import radar-equipped platforms from global OEM programs. Local radar development and manufacturing activity remains limited, keeping the region primarily an end-market rather than a production contributor.

Middle East and Africa 4D Imaging Radar Market Trends

Middle East and Africa radar adoption centers on smart city infrastructure and security applications rather than automotive volumes. GCC governments are funding intelligent transportation systems across Saudi Arabia and UAE, creating demand for traffic monitoring and perimeter surveillance radar. In November 2025, Zadar Labs announced the Zadar Saudi Solutions joint venture with Bidaya Holding and SmartChips to expand 4D imaging radar perception systems across Saudi Arabia and GCC smart mobility markets.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Robert Bosch GmbH holds a structural advantage in 4D radar through its fully integrated automotive supply chain, which spans semiconductor procurement, sensor manufacturing, and ADAS software integration. Bosch’s position as a Tier 1 supplier to virtually every major global OEM gives it unmatched platform reach. The risk is that this breadth makes Bosch a follower rather than a pioneer, as specialised radar-only vendors move faster on algorithm development.

ZF Friedrichshafen AG competes in 4D radar as part of a broader vehicle safety systems portfolio that includes braking, steering, and chassis control. This systems-level positioning allows ZF to offer integrated safety packages rather than standalone sensor units. OEMs simplifying their supplier relationships find this bundled approach attractive, giving ZF a cross-selling advantage that pure-play radar vendors cannot replicate.

Arbe has built its competitive position on chipset licensing rather than finished sensor manufacturing. This asset-light model allows Arbe’s radar technology to reach market through OEM-relationship partners such as HiRain Technologies and Sensrad, multiplying distribution reach without proportional capital expenditure. The strategic risk is dependency on partner execution, but the January 2025 collaboration with NVIDIA at CES 2025 on AI-driven free-space mapping signals Arbe’s intent to anchor its platform in the software-defined vehicle architecture.

Aptiv approaches 4D radar as a component of its broader software-defined vehicle strategy, embedding radar capability within centralized compute architectures rather than selling discrete sensor units. The October 2025 launch of its Gen-8 radar lineup, which doubled channel count from the prior generation, demonstrates that Aptiv is competing on hardware performance while simultaneously integrating sensors into system-level solutions that raise switching costs for OEM customers.

Key Players

- Robert Bosch GmbH

- ZF Friedrichshafen AG

- Arbe

- Aptiv

- Renesas Electronics Corporation

- Zadar Labs, Inc.

- Huawei Technologies Co., Ltd.

- Continental AG

- RADSee Technologies Ltd.

- smart microwave sensors GmbH

Recent Developments

- January 2024 – Arbe Robotics announced that HiRain Technologies would begin mass production of its LRR610 4D imaging radar systems powered by Arbe’s chipset by end of 2024, including a 1 million-kilometer vehicle data collection program to support system validation.

- April 2024 – Uhnder launched the S81 4D digital imaging radar chip for mass-market ADAS vehicles, featuring support for up to 96 MIMO channels and high-contrast resolution technology designed to meet mid-segment OEM cost targets.

- January 2025 – Arbe Robotics announced collaboration with NVIDIA at CES 2025 to advance radar-based free-space mapping and AI-driven autonomous driving capabilities using ultra-high-definition 4D imaging radar technology integrated with NVIDIA’s autonomous vehicle compute platform.

- November 2025 – Zadar Labs announced the launch of Zadar Saudi Solutions (ZSS), a joint venture with Bidaya Holding and SmartChips to deploy 4D imaging radar perception systems across Saudi Arabia and GCC smart mobility infrastructure programs.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 3.1 Billion |

| Forecast Revenue (2035) | USD 12.7 Billion |

| CAGR (2026-2035) | 15.1% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Short Range Radar, Medium Range Radar, Long Range Radar), By Radar Architecture (MIMO, DBF, FMCW, Doppler Radar, Synthetic Aperture Radar), By Component (Radar SoC/RFIC, AiP, Transceivers, Software, Embedded Systems), By Deployment Mode (OEM-Installed, Aftermarket, Integrated into Perception Stacks), By Frequency Band (24 GHz, 60 GHz, 76-77 GHz, 77-81 GHz), By Application (Automotive, Aerospace and Defense, Security and Surveillance, Traffic Monitoring and Management, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Robert Bosch GmbH, ZF Friedrichshafen AG, Arbe, Aptiv, Renesas Electronics Corporation, Zadar Labs Inc., Huawei Technologies Co. Ltd., Continental AG, RADSee Technologies Ltd., smart microwave sensors GmbH |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |