Quick Navigation

Overview

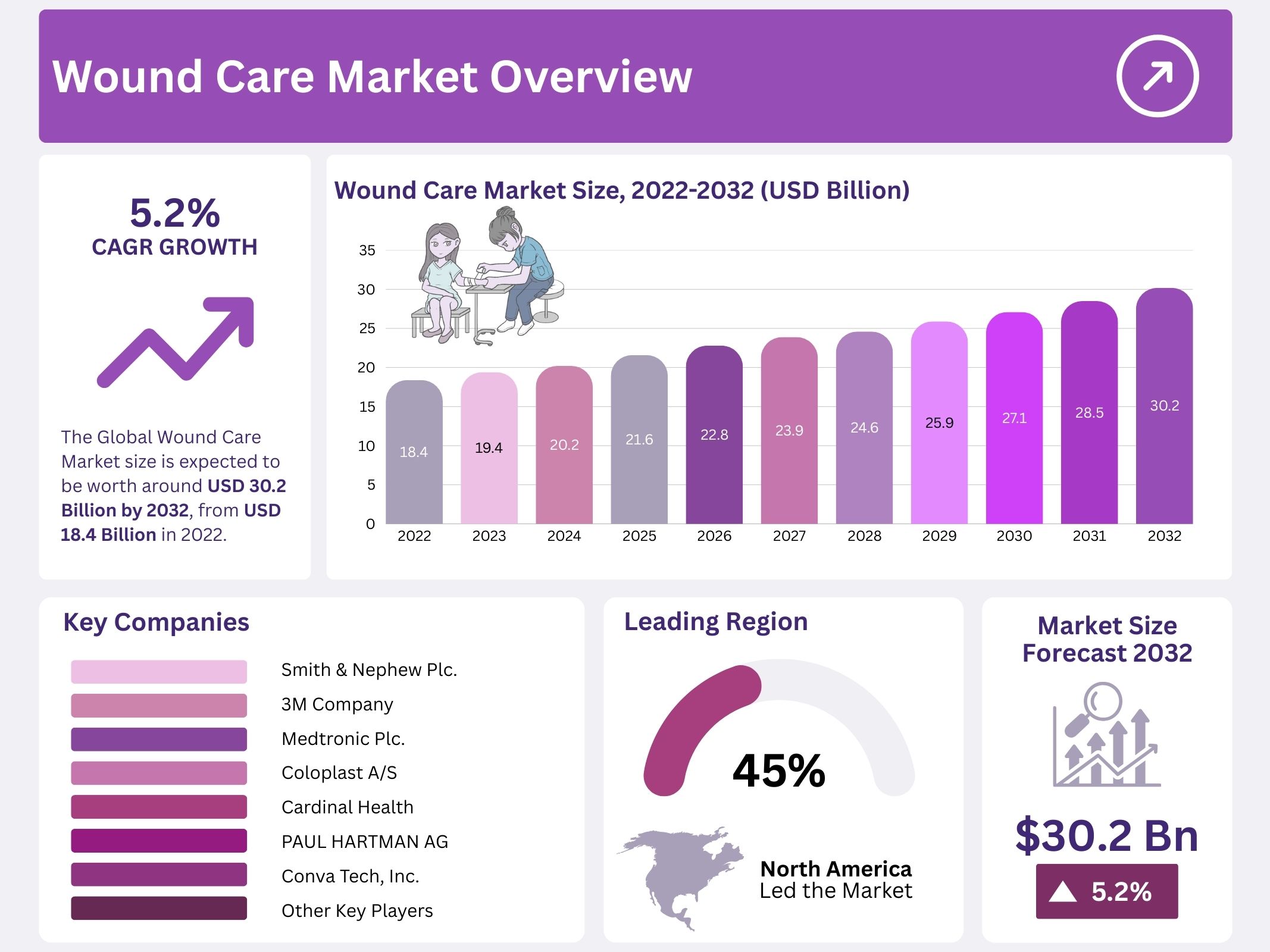

The Global Wound Care Market is projected to reach USD 30.2 billion by 2032, growing from USD 18.4 billion in 2022 at a CAGR of 5.2%. Wounds are disruptions in the normal structure and function of skin and soft tissue. Acute wounds follow normal healing stages, while chronic wounds show impaired healing. Wound care focuses on promoting proper healing, treating injuries, and repairing damaged skin and underlying tissues. The market excludes burns but includes injuries caused by therapeutics, radiation, and minor trauma.

Wound care products, particularly advanced dressings, play a vital role in treatment. They remove dead space, prevent bacterial growth, and maintain proper fluid balance. Dressings also improve convenience for patients and nursing staff. Technological advancements, including hydrogels, hydrocolloids, and negative pressure wound therapy (NPWT), have enhanced the healing process. These innovations provide protection, maintain optimal moisture, and accelerate recovery, especially in complex wounds. The adoption of these solutions is growing globally, driven by demand for improved patient outcomes.

The market is fueled by demographic and health trends. An aging global population increases the prevalence of chronic conditions such as diabetes and vascular diseases, leading to more chronic wounds. Rising incidence of obesity and diabetes contributes to diabetic foot ulcers and pressure ulcers, which require specialized care. As awareness grows, healthcare professionals and patients are better trained in wound assessment and management. This knowledge improves treatment efficiency and increases demand for advanced wound care products and services worldwide.

Healthcare infrastructure development and supportive policies further drive market growth. Expansion of healthcare facilities in emerging economies improves access to specialized wound care. Government initiatives strengthen healthcare systems, ensuring availability of trained professionals and advanced products. Additionally, regulatory support and reimbursement policies make wound care more affordable and accessible. These factors encourage investment and innovation in the sector, positioning the wound care market for sustained growth as healthcare providers focus on improving patient outcomes and reducing complications.

Key Takeaways

- The global wound care market is expanding steadily, growing at a CAGR of 5.2%, reflecting increasing demand for effective wound management solutions worldwide.

- Wounds are typically classified as acute or chronic, with wound care emphasizing proper healing, tissue repair, and overall patient recovery outcomes.

- Advanced wound dressings remain the most profitable segment, driven by rising burn cases and an aging population seeking improved treatment options.

- Chronic wounds, including diabetic foot ulcers and pressure ulcers, dominate the market due to higher patient numbers and escalating healthcare expenditure globally.

- Acute wounds, such as traumatic injuries and surgical wounds, are expected to grow rapidly, aided by infection prevention and enhanced patient satisfaction efforts.

- Hospitals serve as the primary end-users of wound care products, while home healthcare is projected to expand due to aging populations and shifting patient preferences.

- Technological advancements, along with product launches by companies like Conva Tech Group Plc. and Braun Melsungen AG, continue to drive significant market growth.

- The rising prevalence of diabetes adversely impacts wound healing, creating an increased demand for specialized wound care products to manage complications.

- Market growth faces restraints from rising product costs and occasional product recalls, which affect accessibility and overall confidence in wound care solutions.

- Developing economies with enhanced healthcare infrastructure present lucrative opportunities for market expansion, particularly in regions seeking modern wound care treatments.

Regional Analysis

North America dominates the wound care market, holding the largest revenue share of 45%. The region benefits from a well-established healthcare sector and growing demand for wound care products. Major drivers include a large population and a rising patient pool, particularly in the United States. As the elderly population is more prone to chronic wounds, demand for advanced wound care solutions is expected to increase. For example, the Administration for Community Living reports millions of people aged 65 and above, boosting market opportunities.

The aging population in North America is a key growth factor for the wound care market. Older adults are more vulnerable to injuries and chronic wounds, driving the need for specialized wound healing products. Additionally, skilled healthcare professionals in the region ensure better wound management and treatment. Factors such as the rising number of road accidents further increase the demand for wound care solutions. Overall, North America is poised for significant market growth over the forecast period due to these combined factors.

The Asia-Pacific region is projected to experience the fastest wound care market growth during the forecast period. This expansion is largely driven by a rise in chronic diseases caused by changing lifestyles. For instance, the Down to Earth organization estimates that millions of Indians between 20 and 79 years old will have diabetes. The growing prevalence of such conditions creates substantial demand for effective wound management solutions. Increased healthcare awareness and adoption of modern wound care products also contribute to regional growth.

Medical tourism is another major factor driving wound care demand in Asia-Pacific. More patients travel to the region for surgeries, leading to a higher need for post-operative wound care products. The rising number of hospitals and clinics offering advanced treatment further supports market expansion. Combined with chronic disease prevalence, these factors make Asia-Pacific a high-growth region. Over the forecast period, the wound care market in this region is expected to expand rapidly, presenting significant opportunities for manufacturers and healthcare providers.

Segmentation Analysis

Type Analysis

The wound care market is segmented into advanced, traditional, and surgical wound dressings. Among these, advanced wound dressings hold the largest revenue share during the forecast period. The growth is driven by the rising number of burn cases. According to the American Burn Association, burn patients have higher infection rates. Advanced wound care products are designed for conditions like diabetes and ulcers. Additionally, the growing geriatric population further drives demand, as elderly individuals are more prone to chronic and non-healing wounds, requiring innovative wound management solutions.

Application Analysis

Based on application, the market is classified into chronic and acute wounds. Chronic wounds dominate the market due to an increasing number of diabetic foot ulcers, pressure ulcers, leg ulcers, and vascular ulcers. Rising healthcare expenditure also supports this growth. Acute wounds, including burns and traumatic injuries, are expected to show the fastest revenue growth. Acute wound care products stimulate tissue regeneration and improve patient outcomes. These products are particularly effective in complex burn injuries and diabetic wounds, supporting faster healing and reducing hospital stays.

End-User Analysis

The market is segmented by end users into hospitals, home healthcare, trauma centers, and clinics. Hospitals hold the largest share due to the rise in multispecialty centers dedicated to wound care, especially in emerging regions. Home healthcare is projected to grow at a higher CAGR, driven by the aging population and increased prevalence of chronic conditions. Patients increasingly prefer treatment at home, supported by home-care services. Obesity and chronic illnesses also boost the demand for at-home wound management solutions, further expanding the market potential.

Key Players Analysis

The wound care market is highly fragmented, with numerous large and small manufacturers operating globally. This fragmentation increases competitive rivalry and encourages companies to adopt innovative strategies. Key players focus on expanding product lines, launching new treatments, and engaging in mergers and acquisitions. These strategies are essential for maintaining market share. Collaboration between major companies and smaller enterprises also helps accelerate technological advancements, improve product offerings, and enhance overall market growth, benefiting both patients and healthcare providers worldwide.

Smith & Nephew recently launched the PICO 14 NPWT system, which provides therapy for up to 14 days. This innovative product expanded the company’s existing portfolio and strengthened its position in advanced wound care. Introducing new treatments is a primary strategy for leading players to maintain dominance. Companies continuously focus on research and development to meet growing demand. Innovation not only enhances patient outcomes but also allows businesses to remain competitive, addressing evolving market requirements and staying ahead of regional and global competitors.

In addition to product innovation, mergers and acquisitions are a key growth strategy. For instance, Smith & Nephew acquired Southlake Medical Supplies, securing a stronger presence in the American market. Such strategic moves allow companies to expand geographically, improve distribution channels, and increase brand visibility. By combining resources, expertise, and market reach, these collaborations drive revenue growth and ensure sustained market presence. Consequently, these activities are expected to contribute significantly to the overall expansion of the wound care market during the forecast period.

The major players in the wound care market include Smith & Nephew Plc, 3M Company, B Braun Melsungen AG, Johnson & Johnson, Coloplast A/S, Medtronic Plc, Baxter International Inc., Investor AB, Derma Science Inc., Cardinal Health, BSN Medical GmbH, MiMedx Group, Inc., and Paul Hartman AG. These companies leverage innovation, acquisitions, and collaborations to remain competitive. Their strategic initiatives, combined with a focus on patient-centered solutions, are expected to drive market growth, improve product accessibility, and maintain leadership positions in the global wound care sector.

Top Leading Key Players In Wound Care Market Are:

- Smith & Nephew Plc.

- 3M Company

- Medtronic Plc.

- Coloplast A/S

- Cardinal Health

- PAUL HARTMAN AG

- Molnlycke Health Care AB

- Johnson & Johnson Services

- Conva Tech Inc.

- B Braun Melsungen AG

- Bactiguard AB

- Paul Heartman AG

- MiMedx Group Inc.

- Investor AB

- Baxter International Inc.

- Derma Science Inc.

- BSN Medical GmbH

- Other Key Players

Conclusion

In conclusion, the global wound care market is set for steady growth, driven by increasing awareness of proper wound management, technological advancements, and rising prevalence of chronic conditions. Advanced wound care products, such as specialized dressings and negative pressure therapy, are becoming essential for improving patient outcomes and speeding up recovery. Hospitals remain the primary users, while home healthcare is gaining importance due to aging populations and lifestyle-related chronic diseases. Key players continue to innovate through product launches, collaborations, and acquisitions, ensuring competitive advantages. Overall, the market offers significant opportunities for expansion, with emerging regions showing strong potential for modern wound care solutions and improved patient care.

Get in Touch with Us:

Market.us (Powered By Prudour Pvt. Ltd.)

Address: 420 Lexington Avenue, Suite 300, New York City, NY 10170, United States.

Contact No: +1 718 874 1545 (International), +91 78878 22626 (Asia).

Email: [email protected]