Quick Navigation

Overview

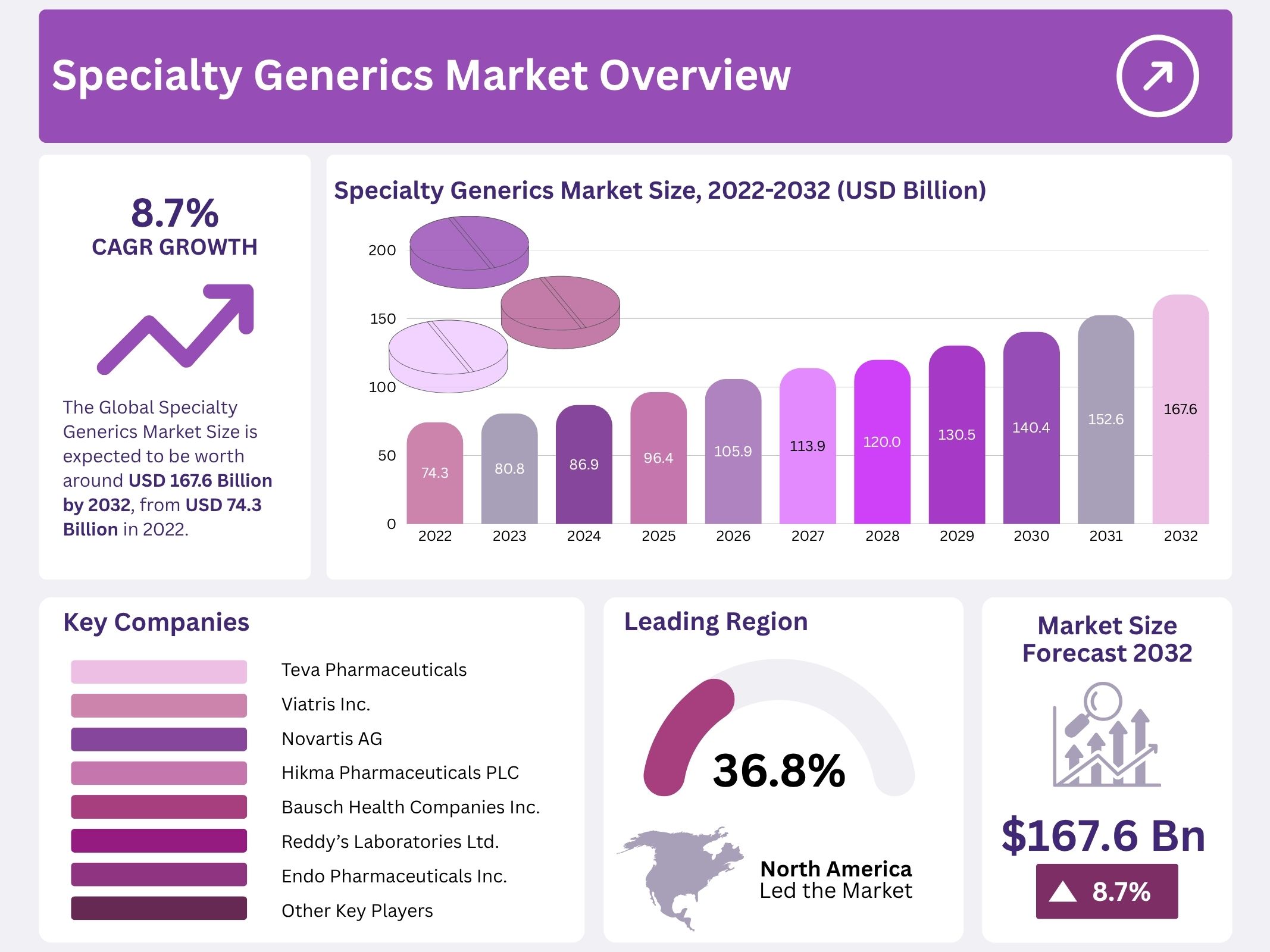

The global Specialty Generics Market was valued at USD 74.3 billion in 2022 and is projected to reach USD 167.6 billion by 2032, expanding at a CAGR of 8.7% from 2023 to 2032. Specialty generics refer to complex generic versions of advanced therapies, including injectables, inhalables, and drug–device combinations. Market expansion is driven by patent expirations, regulatory support, cost pressures, and technological progress. The rising prevalence of chronic diseases and healthcare cost containment policies continue to stimulate demand for affordable complex therapies. This shift positions specialty generics as an essential component of modern healthcare systems.

Patent expiries of branded specialty drugs remain a core growth catalyst. As exclusivity lapses, new opportunities arise for generic manufacturers to introduce cost-effective equivalents in high-value therapeutic areas. This trend ensures a consistent pipeline of market entrants, promoting competition and expanding patient access. Regulatory agencies such as the FDA and EMA have strengthened guidance for complex generic approvals, simplifying pathways and improving predictability. Streamlined review processes and harmonized global standards encourage more manufacturers to invest in developing high-quality specialty generics.

Technological advancements in formulation science, analytical characterization, and manufacturing automation have enabled precise replication of complex drugs. Modern bioequivalence modeling and delivery innovations have enhanced efficiency and therapeutic consistency. These developments lower production barriers and improve scalability, allowing manufacturers to meet global demand effectively. Moreover, strategic collaborations between pharmaceutical firms, contract manufacturers, and technology providers have become crucial in overcoming technical and regulatory complexities. Such partnerships enhance expertise sharing, accelerate market entry, and expand global reach.

Economic pressures on healthcare systems are also reshaping market priorities. Governments and payers are increasingly adopting value-based care frameworks that emphasize cost-effectiveness. Specialty generics meet this need by offering comparable efficacy at reduced cost, aligning with institutional goals for sustainable healthcare spending. Emerging markets, supported by healthcare infrastructure improvements and favorable regulatory reforms, present significant opportunities for expansion. The growing acceptance of complex generics in these regions further diversifies revenue streams for global players.

Manufacturers are now focusing on differentiated offerings to gain a competitive edge. Enhanced formulations, improved patient compliance, and longer shelf life help create product differentiation within a competitive market. Overall, the specialty generics sector is being strengthened by structural market shifts, regulatory evolution, and scientific innovation. Continued progress in technology, quality standards, and policy support is expected to sustain growth and establish specialty generics as a vital enabler of affordable, accessible, and effective healthcare globally.

Key Takeaways

- The Specialty Generics Market is projected to reach USD 167.6 billion by 2032, growing at a robust CAGR of 8.7% from 2023.

- Increasing prevalence of chronic diseases significantly drives demand for specialty generics, as patients seek cost-effective treatment alternatives for long-term conditions.

- The injectables segment dominates the market due to rapid absorption rates and enhanced therapeutic effectiveness, contributing the highest revenue share.

- Rising cases of inflammatory conditions have made this segment particularly lucrative, as demand for targeted and affordable treatments continues to grow.

- Specialty pharmacies lead distribution, offering reduced operational costs, improved accessibility, and efficient handling of complex specialty generic products.

- Emerging markets in Asia and Latin America exhibit substantial potential, supported by unmet healthcare needs and expanding pharmaceutical infrastructure.

- Manufacturers are increasingly focusing on innovation, developing novel drug delivery systems and administration methods to achieve market differentiation and enhance patient outcomes.

Regional Analysis

North America held a dominant market position in Specialty Generics Market, capturing more than a 36.8% share and holds US$ 27.4 Billion market value for the year. The region’s growth is driven by favorable regulatory frameworks supporting the approval of innovative and cost-effective products. The United States remains the key contributor due to strong healthcare infrastructure and the presence of leading pharmaceutical manufacturers. Continuous efforts by major producers to launch specialty generics for commercial use strengthen market penetration. Canada and Mexico also demonstrate steady growth, supported by increasing adoption of affordable alternatives to branded specialty medicines.

Western Europe represents another significant regional market for specialty generics. The presence of advanced healthcare systems in countries such as Germany, France, the United Kingdom, and Italy contributes to market expansion. Increasing healthcare expenditure and government initiatives promoting generic substitution strengthen growth prospects. Additionally, the demand for cost-effective treatment options in Benelux, Nordic nations, and Southern European countries further boosts market development. Regulatory harmonization within the European Union facilitates quicker approvals, creating favorable conditions for generic manufacturers across the region.

The Asia Pacific region is projected to experience the fastest growth during the forecast period. This expansion is mainly attributed to high unmet needs for affordable specialty drugs and the increasing introduction of new generic formulations. Countries such as China, India, and Japan are emerging as major contributors due to large patient populations and expanding manufacturing capabilities. The region’s growing healthcare investments and government efforts to enhance drug accessibility are accelerating adoption. Moreover, local pharmaceutical companies are increasingly targeting niche therapeutic areas with generic solutions.

Latin America and the Middle East & Africa (MEA) regions are anticipated to register moderate yet steady growth in the specialty generics market. In Latin America, Brazil, Argentina, and Colombia are key contributors, supported by economic reforms and improved healthcare infrastructure. In MEA, countries such as Saudi Arabia, South Africa, and the United Arab Emirates are witnessing rising generic drug penetration due to increasing healthcare awareness. Supportive government initiatives to reduce treatment costs are expected to strengthen regional demand over the forecast horizon.

Segmentation Analysis

The injectables segment accounted for the largest revenue share in the specialty generics market. This dominance was mainly attributed to benefits such as fast absorption and long-lasting effects, which improve patient compliance. The rising number of product approvals and strong market penetration further enhanced the segment’s performance. The approval of injectables for cancer and chronic conditions has also boosted prescription rates. This trend is expected to continue, as affordability and therapeutic efficiency support market expansion during the forecast period.

The inflammatory conditions segment held the leading share in the specialty generics market by application. The growing prevalence of diseases such as arthritis and psoriasis has fueled the demand for affordable specialty generics. This trend has encouraged major market players to strengthen their portfolios in this category. Meanwhile, the oncology segment is projected to show significant growth due to the increasing burden of cancer. Factors such as poor lifestyle habits and higher tobacco and alcohol consumption have contributed to this demand surge.

The pharmacy distribution channel segment dominated the specialty generics market with the largest market share. Specialty pharmacies were the preferred choice for manufacturers and insurers because of their cost-effective distribution model. These pharmacies ensure quick access, efficient inventory management, and timely delivery of drugs, which improves patient convenience. The affordability of specialty generic medicines results in better returns on investment compared to branded counterparts. The expanding role of specialty pharmacies in patient support and care management is expected to sustain market growth.

Key Players Analysis

The specialty generics market is characterized by the active participation of leading pharmaceutical companies expanding their presence globally. Key players such as Teva Pharmaceuticals Industries Ltd., Viatris Inc., and Novartis AG are investing in developing affordable yet effective specialty generic drugs. Their strategic focus lies in strengthening distribution networks and expanding therapeutic portfolios. The growth of these companies is driven by the increasing demand for cost-effective treatments and the expiration of branded drug patents, opening opportunities for competitive market entry.

Partnerships and licensing agreements are central to the competitive landscape. Hikma Pharmaceuticals PLC and Sun Pharmaceutical Industries Ltd. recently entered an exclusive agreement to distribute Ilumya in the MEA region. This collaboration enhances access to advanced therapies for moderate to severe plaque psoriasis. Through such alliances, companies aim to meet unmet medical needs while maintaining affordability and quality. The strategy highlights a growing emphasis on regional expansion and specialized treatment solutions within the specialty generics sector.

The market also benefits from contributions by companies such as Mallinckrodt, Akorn, Inc., Bausch Health Companies Inc., and Dr. Reddy’s Laboratories Ltd. These firms focus on research, development, and manufacturing efficiency to enhance product accessibility. Continuous innovation and strong regulatory compliance are essential for maintaining competitiveness. Their growing product pipelines, supported by robust global distribution networks, enable them to cater to complex therapeutic areas, including oncology, neurology, and dermatology, where affordability and patient access are critical growth factors.

Other significant players such as Endo Pharmaceuticals Inc., Apotex Corp., Fresenius Kabi Brasil Ltd., Stada Arzneimittel AG, and Pfizer Inc. are expanding their specialty generics portfolios through mergers and acquisitions. These companies focus on strengthening market presence in emerging economies. Their strategies include capacity expansion, technology integration, and the introduction of differentiated generic formulations. The collective efforts of these firms contribute to a dynamic and competitive global specialty generics landscape, driving innovation and affordability in specialty medicine.

Market Key Players

- Teva Pharmaceuticals Industries Ltd.

- Viatris Inc.

- Novartis AG

- Hikma Pharmaceuticals PLC

- Mallinckrodt; Akorn, Inc.

- Bausch Health Companies Inc.

- Reddy’s Laboratories Ltd.

- Endo Pharmaceuticals Inc.

- Apotex Corp.

- Sun Pharmaceutical Industries Ltd.

- Fresenius Kabi Brasil Ltd.

- Stada Arzeimittel AG

- Pfizer, Inc.

- Other Market Players

Conclusion

The specialty generics market is showing strong and sustainable growth due to rising healthcare needs and the demand for cost-effective treatments. Factors such as patent expirations, advanced manufacturing technologies, and supportive government policies are driving market expansion. Increasing cases of chronic and complex diseases are further boosting the adoption of specialty generics across key regions. Continuous innovation and partnerships among leading pharmaceutical companies are helping to enhance product quality and patient access. With expanding production capabilities and regulatory alignment, specialty generics are expected to play a vital role in delivering affordable, high-quality therapies and strengthening global healthcare accessibility in the years ahead.

Get in Touch with Us:

Market.us (Powered By Prudour Pvt. Ltd.)

Address: 420 Lexington Avenue, Suite 300, New York City, NY 10170, United States.

Contact No: +1 718 874 1545 (International), +91 78878 22626 (Asia).

Email: [email protected]

View More

Generic Pharmaceuticals Market | Generic Drugs Market | Generic Sterile Injectable Market | Generic Injectable Market