Quick Navigation

Introduction

The Global Smart TV Market is experiencing steady expansion as consumers increasingly shift toward digital and connected entertainment solutions. Smart TVs integrate internet connectivity, interactive apps, and advanced display technologies, making them central to modern home entertainment systems.

Driven by rising streaming adoption and enhanced display innovations, the market continues accelerating. Manufacturers are introducing models that balance affordability with sophisticated features, meeting consumer demand for on-demand content access and seamless smart home integration.

As a result, Smart TVs are evolving beyond traditional viewing devices, becoming central hubs for communication, gaming, content streaming, and connected living. This growth trend is expected to strengthen throughout the forecast period.

Key Takeaways

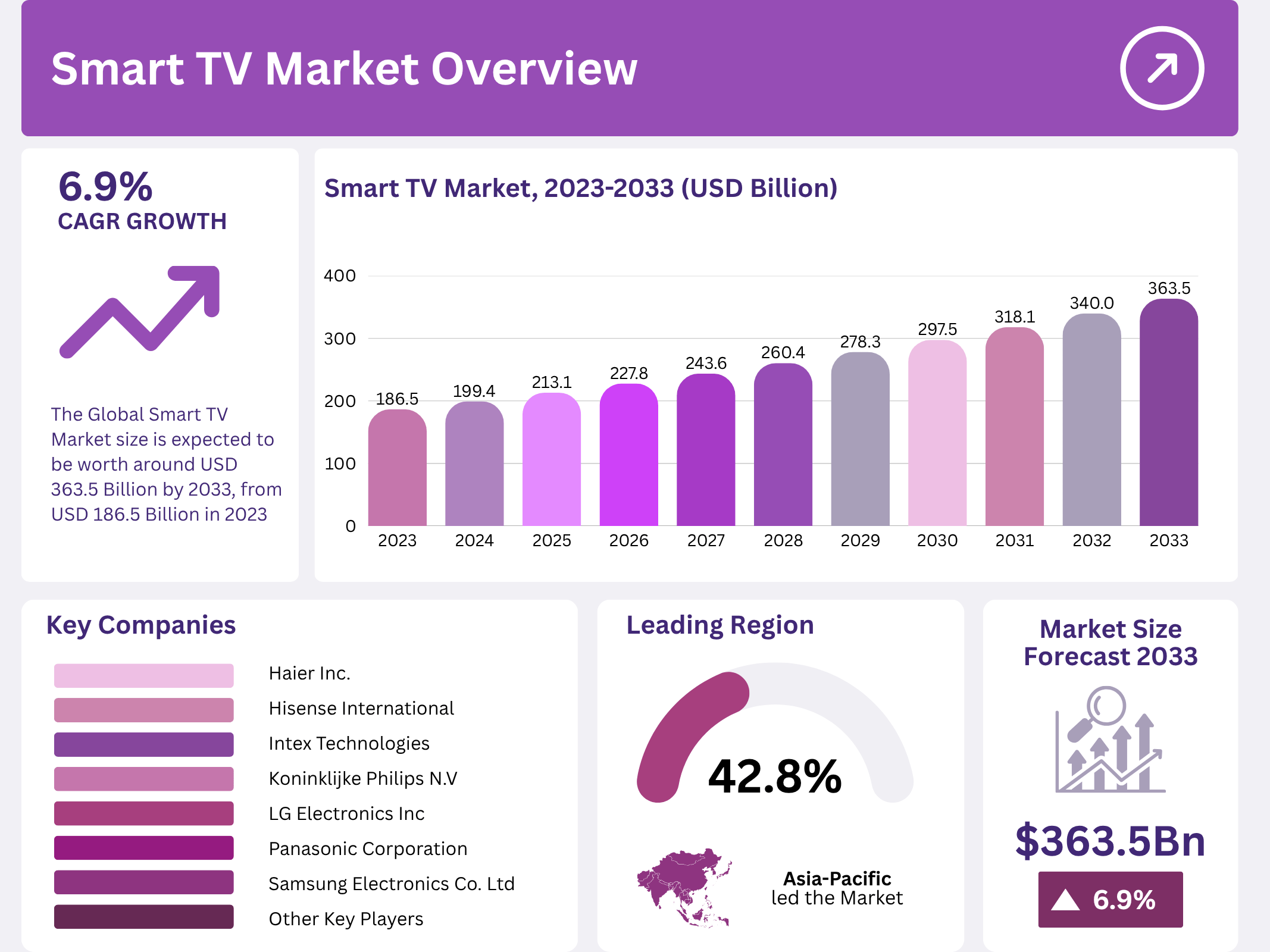

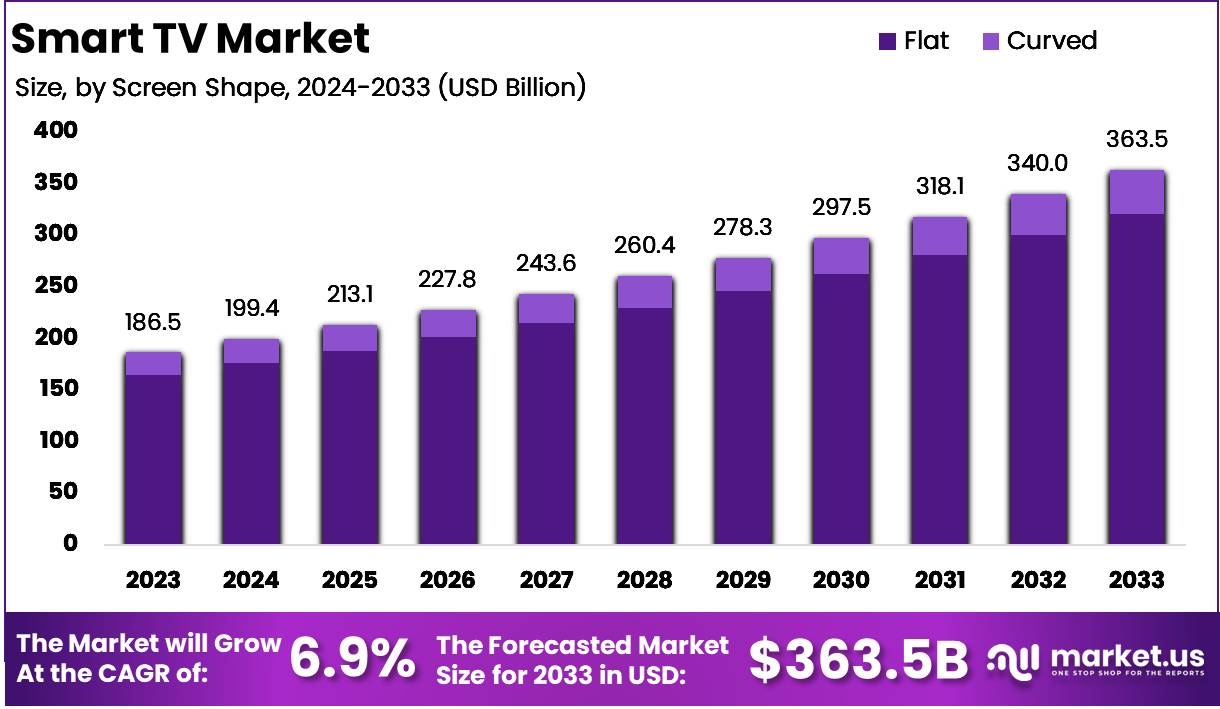

- The global Smart TV market is projected to grow from USD 186.5 billion in 2023 to USD 363.5 billion by 2033, driven by a robust 6.9% CAGR during the forecast period.

- Android OS dominates the Smart TV operating system segment, capturing over 43.2% of the global market share in 2023.

- 4K UHD TV leads the Smart TV resolution market with a commanding 48.3% market share in 2023.

- The 46 to 55 inches screen size segment dominates, holding more than 35.6% of the Smart TV market share in 2023.

- LED technology remains the market leader, accounting for more than 54.3% of the Smart TV market share in 2023.

- Asia Pacific holds the largest market share in the Smart TV market, with 42.8% of the global market share in 2023.

Market Segmentation Overview

By operating system, Android OS leads due to its flexible ecosystem and compatibility across multiple brands. Its robust app availability and seamless integration with voice assistants enhance user convenience, sustaining its strong adoption among consumers across both premium and budget TV segments.

By resolution, 4K UHD TVs dominate as consumers increasingly prefer higher clarity and realistic visuals. With broader content availability from streaming platforms and gaming consoles, 4K TVs continue to replace lower-resolution models in mainstream households.

In terms of screen size, the 46 to 55 inches category remains most preferred, balancing affordability, space efficiency, and high-impact viewing. This segment appeals widely to home users upgrading their entertainment setups.

By screen shape, flat screens prevail with over 88% share, favored for their practicality, affordability, and wide availability. Curved screens retain niche appeal among users seeking immersive cinematic viewing experiences.

By technology, LED TVs hold the largest share due to cost efficiency and reliable performance. Meanwhile, OLED and QLED continue expanding in the premium segment, driven by superior color accuracy and contrast enhancements.

In application, the residential segment dominates with more than 78.5% share, reflecting growing home entertainment investments. Commercial adoption is rising in hospitality, retail, and corporate environments.

By distribution channel, online platforms lead with over 58.4% share due to rising preference for comparison shopping, discounts, and home delivery convenience.

Drivers

Increasing Smart Home Integration: Smart TVs are now core to connected living environments as they integrate with smart speakers, IoT sensors, and voice assistants. This seamless control functionality is driving household adoption globally.

Growth of Streaming Services: The rapid shift from traditional cable TV to OTT platforms has accelerated Smart TV demand. Consumers prefer TVs with built-in access to platforms such as Netflix, Prime Video, and Disney+, driving continuous upgrades.

Use Cases

Home Entertainment & Streaming: Smart TVs enable personalized streaming, gaming, and content browsing experiences. They serve as centralized entertainment hubs, catering to multi-user households with tailored recommendations.

Commercial Digital Display & Engagement: Businesses use Smart TVs for digital signage, presentations, and video conferencing. Hospitality and retail sectors leverage Smart TVs for interactive customer engagement and promotional content display.

Major Challenges

High Cost of Advanced Models: While basic LED Smart TVs are affordable, premium technologies like OLED, QLED, and 8K panels remain expensive. This limits adoption, particularly in price-sensitive markets.

Limited High-Speed Internet Access: In regions lacking stable broadband infrastructure, Smart TV functionalities are underutilized. Poor connectivity reduces streaming quality and discourages users from upgrading.

Business Opportunities

Emerging Market Expansion: With growing internet penetration in Asia, Africa, and Latin America, manufacturers can target first-time Smart TV buyers with affordable models optimized for varied bandwidth conditions.

Content & Service Partnerships: Collaboration between Smart TV manufacturers and OTT platforms enables bundled subscriptions, exclusive content access, and enhanced user engagement, creating additional revenue streams.

Regional Analysis

Asia Pacific: The region leads with 42.8% market share driven by rising disposable incomes, rapid urbanization, and strong manufacturing presence in China, South Korea, and Japan. Consumers in this region actively adopt advanced home entertainment technologies.

North America and Europe: These mature markets maintain steady demand due to high streaming service penetration and preference for premium display technologies. Saturation challenges exist, but upgrades to larger and higher-resolution screens continue supporting market stability.

Recent Developments

- Walmart announced acquisition of VIZIO for USD 2.3 billion in February 2024 to enhance smart home entertainment offerings.

- Xiaomi reported 10.9% YoY revenue growth and a 126.3% increase in adjusted net profit in 2023, supported by smart ecosystem expansion.

Conclusion

The Global Smart TV Market is poised for continued growth driven by rising digital content consumption, technological advancements, and expanding smart home ecosystems. While affordability and connectivity challenges persist, increasing innovation and market expansion opportunities are expected to support strong long-term development.