Quick Navigation

Introduction

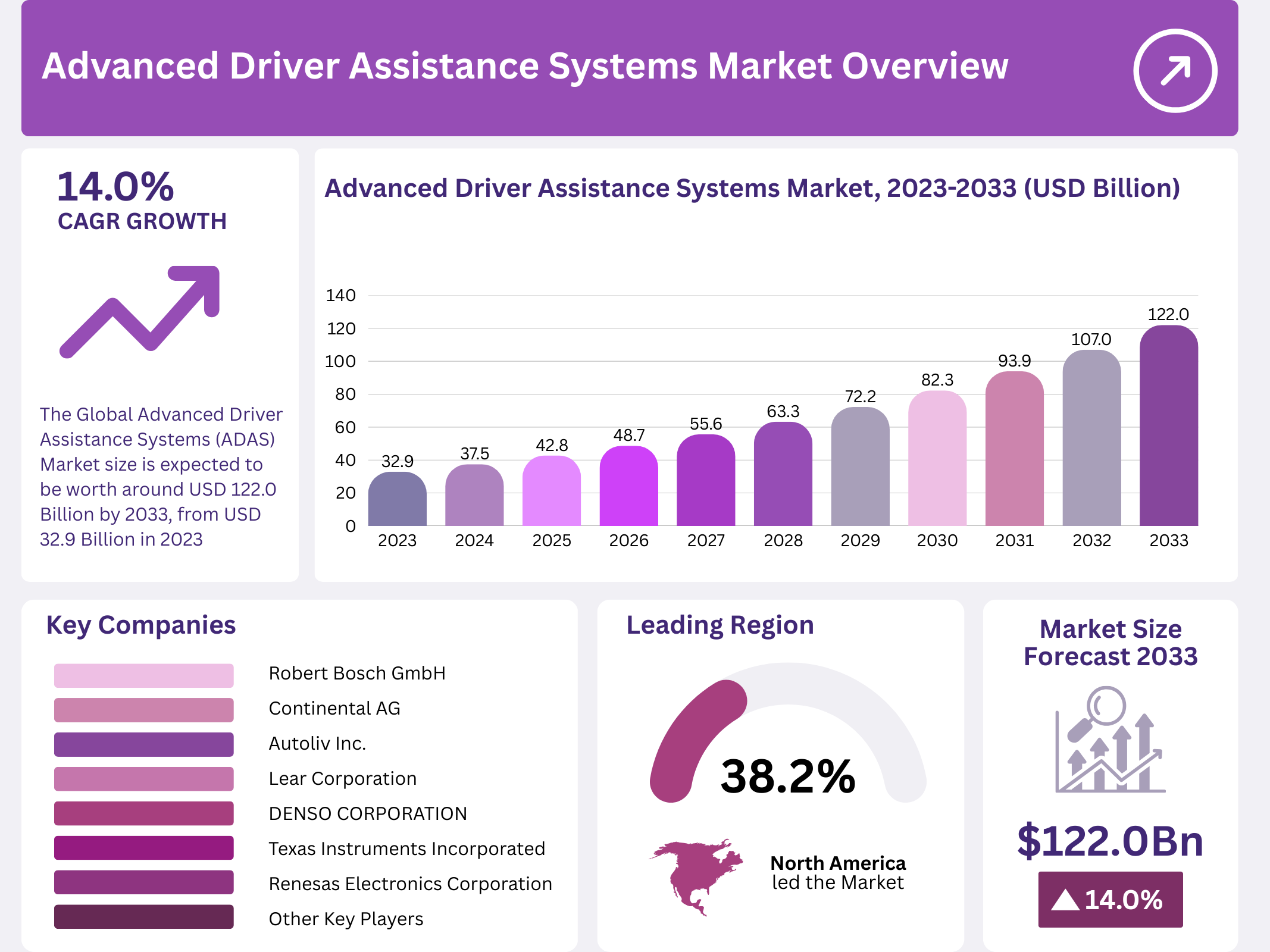

The global Advanced Driver Assistance Systems (ADAS) market is entering a transformative era. Valued at USD 32.9 Billion in 2023, the market is projected to surge to USD 122.0 Billion by 2033, reflecting a compound annual growth rate of 14.0%. This remarkable trajectory signals a fundamental shift in how the automotive industry approaches vehicle safety.

Consequently, ADAS technologies are no longer a luxury — they are fast becoming standard. Systems such as automatic emergency braking, lane departure warnings, and adaptive cruise control are now embedded in millions of new vehicles globally. Consumer expectations around safety have never been higher, accelerating industry-wide adoption.

Furthermore, regulatory bodies across North America, Europe, and Asia Pacific are mandating the inclusion of ADAS features in new vehicles. Government pressure, combined with growing public awareness of road safety risks, is creating a powerful convergence of demand that automakers cannot afford to ignore.

In addition, the rise of electric vehicles is amplifying market growth. As automakers pivot toward electrification, ADAS integration has become a defining feature of next-generation EV models. Together, these forces are reshaping the global automotive landscape at an unprecedented pace.

According to the AAA Foundation for Traffic Safety, widespread ADAS adoption could reduce overall crashes by up to 40%, injuries by 37%, and fatalities by 29%. As a result, the technology is gaining recognition not only as a commercial asset but also as a critical public safety infrastructure.

Ultimately, the ADAS market represents one of the most significant growth stories in the automotive sector today. With technology, regulation, and consumer demand aligning, the outlook for the next decade is exceptionally promising for stakeholders across the value chain.

Key Takeaways

- The Advanced Driver Assistance Systems Market was valued at USD 32.9 Billion in 2023 and is expected to reach USD 122.0 Billion by 2033, with a CAGR of 14.0%.

- In 2023, Tire Pressure Monitoring Systems (TPMS) dominate the solution segment with 29% due to enhanced vehicle safety.

- In 2023, Sensors lead the component segment with 49%, reflecting their essential role in system performance.

- In 2023, Passenger Cars are the dominant vehicle type with 59%, indicating their primary use of ADAS technologies.

- In 2023, North America is the dominant region with 35%, underscoring its advanced automotive sector.

Market Segmentation Overview

In the solutions segment, Tire Pressure Monitoring Systems (TPMS) lead with a 29% share. Their prominence stems from critical roles in vehicle safety, fuel efficiency, and compliance with mandatory regulations across several countries. Notably, other solutions including Adaptive Cruise Control and Autonomous Emergency Braking are also expanding rapidly as driver expectations evolve.

Turning to components, Sensors dominate with a 49% share, functioning as the backbone of all ADAS operations. Radar, LiDAR, and ultrasonic sensors each serve distinct purposes — from distance monitoring to high-resolution 3D mapping. Meanwhile, advancements in processors and software are enabling faster, more accurate real-time decision-making across all ADAS platforms.

Regarding vehicle types, Passenger Cars account for 59% of ADAS adoption, driven by strong consumer demand for safety and convenience. Automakers are increasingly standardizing these features across model ranges. Additionally, Commercial Vehicles represent a growing segment, with fleet operators investing in Lane Departure Warning and Adaptive Cruise Control to reduce accidents and lower operational costs.

Drivers

The primary driver of ADAS market growth is the increasing global focus on road safety. Governments across North America, Europe, and Asia Pacific are enacting stricter safety regulations that mandate ADAS inclusion in new vehicles. Simultaneously, consumer awareness of accident prevention technologies is rising, prompting automakers to prioritize these systems as standard features rather than optional upgrades.

Equally important, rapid advancements in sensor and radar technologies are enhancing the precision and reliability of ADAS. Improved sensors now perform more accurately across varied weather and road conditions. Furthermore, the ongoing development of autonomous driving technologies is positioning ADAS as a critical stepping stone toward fully self-driving vehicles, attracting substantial investment from both automakers and technology companies.

Use Cases

One of the most impactful use cases of ADAS is in preventing rear-end collisions. Forward Collision Warning (FCW) and Automatic Emergency Braking (AEB) systems have achieved a penetration rate of 91–94% in 2023 in the U.S., according to the NHTSA. These systems detect imminent crashes and automatically engage braking, significantly reducing collision frequency and severity on highways and urban roads.

Another prominent use case is lane management. Lane Departure Warning (LDW) and Lane Keeping Assist (LKA) systems actively monitor road markings and alert drivers drifting out of their lanes. In the commercial vehicle sector, these technologies are proving especially valuable for long-haul trucking fleets, where driver fatigue increases lane departure risks and the consequences of accidents are significantly more severe.

Major Challenges

One of the most pressing challenges facing the ADAS market is the high cost of integration. Sophisticated sensors, processors, and software significantly raise vehicle production costs, making ADAS-equipped models less affordable for consumers in emerging markets. Moreover, the lack of standardization across different regional regulatory frameworks complicates manufacturing processes for automakers seeking to develop globally compatible systems.

Cybersecurity presents another serious challenge as vehicles become increasingly connected. ADAS systems are potential targets for hacking and data breaches, which could compromise vehicle safety and erode consumer trust. Additionally, the performance of sensors in adverse weather conditions — such as heavy rain, fog, or snow — remains technically inconsistent, limiting the reliability and effectiveness of ADAS features in real-world scenarios.

Business Opportunities

The rapid expansion of the electric vehicle market creates a compelling business opportunity for ADAS providers. As global EV sales reached approximately 14 million units in 2023 — a 35% increase year-over-year — automakers are actively seeking to integrate advanced safety systems into their EV platforms. Companies that offer scalable, energy-efficient ADAS solutions are positioned to capture significant share in this fast-growing segment.

Furthermore, the advancement of next-generation LiDAR technology opens new commercial avenues. LiDAR’s high-resolution, 3D mapping capabilities are essential for the development of Level 3 and Level 4 autonomous driving systems. Additionally, the growth of smart city infrastructure — including intelligent traffic management and vehicle-to-infrastructure communication — is generating fresh demand for ADAS solutions tailored to connected urban mobility ecosystems.

Regional Analysis

North America leads the global ADAS market with a 35% share, valued at USD 11.52 Billion. The region benefits from a mature automotive industry, high consumer safety expectations, and strong government mandates. Notably, Mercedes-Benz received regulatory approval for Level 3 autonomous driving systems in California and Nevada, signaling continued regulatory support for progressive vehicle automation technologies.

Asia Pacific, meanwhile, is emerging as the fastest-growing ADAS region. Rising vehicle production in China, Japan, and South Korea — combined with evolving safety regulations — is driving rapid market expansion. Europe also maintains a strong position, underpinned by stringent EU safety directives and a robust automotive manufacturing base. Together, these regions underscore the truly global momentum behind ADAS adoption.

Recent Developments

- In August 2024, Jaguar Land Rover (JLR) intensified efforts to raise driver awareness of ADAS after a survey found that 41% of UK drivers were unclear on how these systems operate — including the impact of dirty or obstructed sensors on emergency braking performance.

- In August 2024, Samsung announced a collaboration with Qualcomm to integrate its LPDDR4X automotive memory into Qualcomm’s Snapdragon Digital Chassis, enhancing in-vehicle infotainment and ADAS capabilities while ensuring automotive supply chain stability.

- In September 2024, Gauzy unveiled its AI-powered ADAS for commercial trucks at IAA Transportation 2024, integrating Smart-Vision camera monitor technology to eliminate blind spots, improve visibility, and deliver real-time safety notifications.

Conclusion

The Advanced Driver Assistance Systems market stands at the intersection of safety, technology, and regulatory momentum. With a projected value of USD 122.0 Billion by 2033, the sector offers exceptional growth prospects for automakers, technology developers, and investors alike. As electric vehicles proliferate, AI integration deepens, and governments tighten safety mandates, ADAS is no longer a differentiator — it is an industry imperative. Stakeholders who invest early and innovate continuously will be best positioned to lead in this rapidly evolving landscape.