Global Water-soluble Films Market By Type (Cold Water-soluble Films and Hot Water-soluble Films), By Thickness (Up to 30 μm, 30-60 μm, and Above 60 μm), By Dissolution Rate (Fast-soluble Films, Medium-soluble Films, and Slow-soluble Films), By Application (Detergent Packaging, Agrochemical Packaging, Laundry Bags, Embroidery, Dye Packaging, Medical And Pharmaceutical, Food Packaging, and Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2025-2035

- Published date: Mar 2026

- Report ID: 180641

- Number of Pages: 331

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

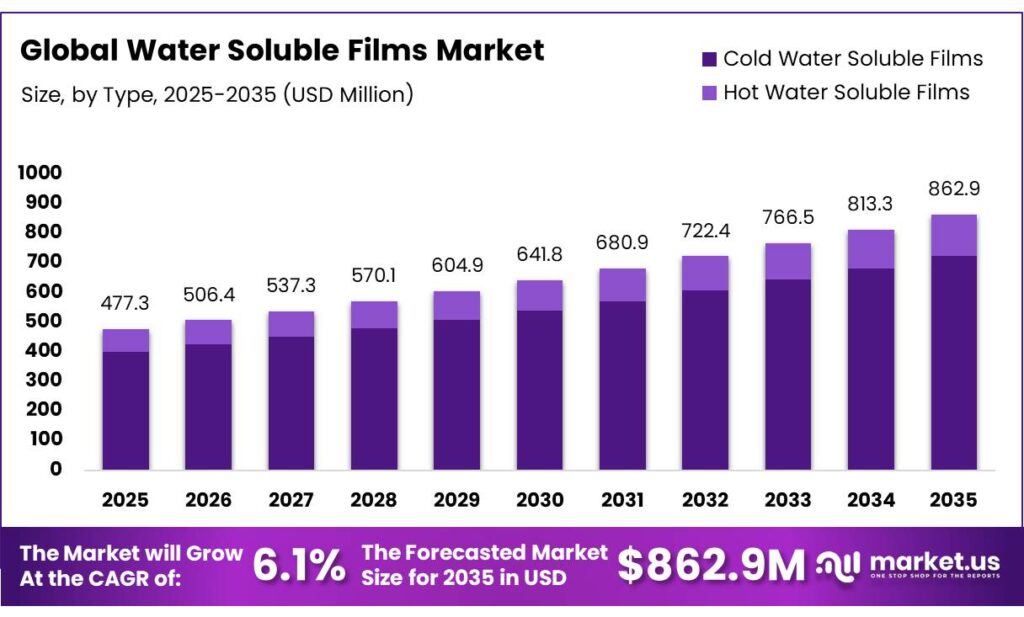

Global Water-soluble Films Market is expected to be worth around USD 862.9 Million by 2035, up from USD 477.3 Million in 2025, at a CAGR of 6.1% from 2026 to 2035. The Asia Pacific segment maintained 39.4%, supporting a Water-soluble Films value of USD 1.9 Bn.

Water-soluble films are specialized polymeric materials, most commonly made from polyvinyl alcohol (PVA or PVOH), that are designed to dissolve completely and safely when they come into contact with water. These films are widely used as an eco-friendly and convenient alternative to traditional plastics as they are biodegradable, non-toxic, and leave no harmful residues or microplastics after dissolution. The market is driven by increasing demand for sustainable packaging solutions, particularly in sectors such as household detergents, personal care, and agriculture.

Regulatory pressures on plastic waste, along with consumer preferences for eco-friendly products, have accelerated the adoption of water-soluble films, especially in single-dose applications such as detergent pods. Cold water-soluble films in the 30-60 μm thickness range are preferred due to their balance of durability and dissolution efficiency. Fast-soluble films dominate the market as they ensure quick and complete dissolution, making them ideal for time-sensitive applications.

While water-soluble films have seen significant uptake in detergent packaging, their use in other sectors such as agrochemicals, pharmaceuticals, and food packaging is limited. Manufacturers focus on product innovation, supply chain optimization, and regional expansion to enhance competitiveness. Despite challenges such as high production costs and raw material volatility, the market continues to grow as technology and sustainability trends evolve.

Key Takeaways:

- The global water-soluble films market was valued at USD 477.3 million in 2025.

- The global water-soluble films market is projected to grow at a CAGR of 6.1% and is estimated to reach USD 862.9 million by 2035.

- On the basis of types, cold water-soluble films dominated the market, constituting 83.9% of the total market share.

- Based on the thickness, 30-60 μm water-soluble films dominated the market, with a market share of around 48.1%.

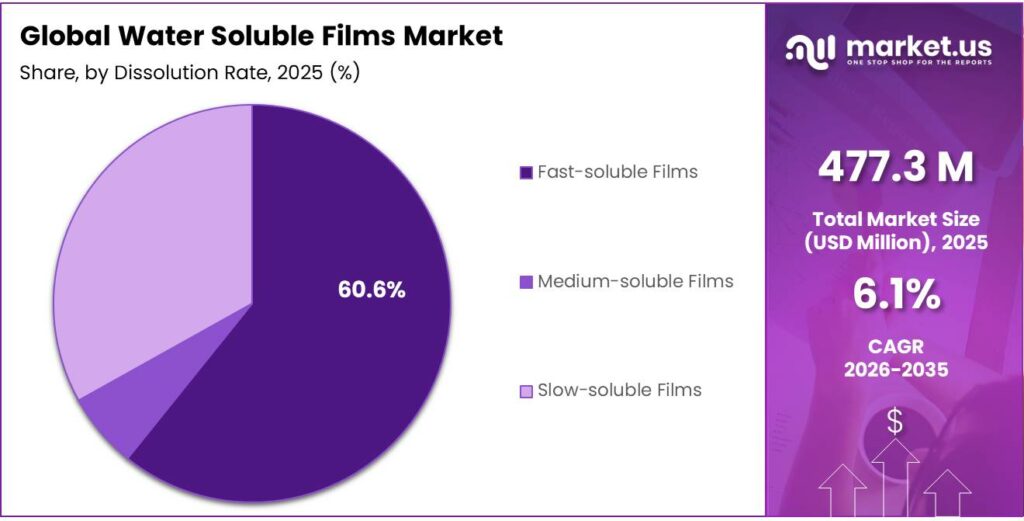

- Based on the dissolution rate, fast-soluble films led the market, comprising 60.6% of the total market.

- Among the applications, detergent packaging held a major share in the water-soluble films market, 37.2% of the market share.

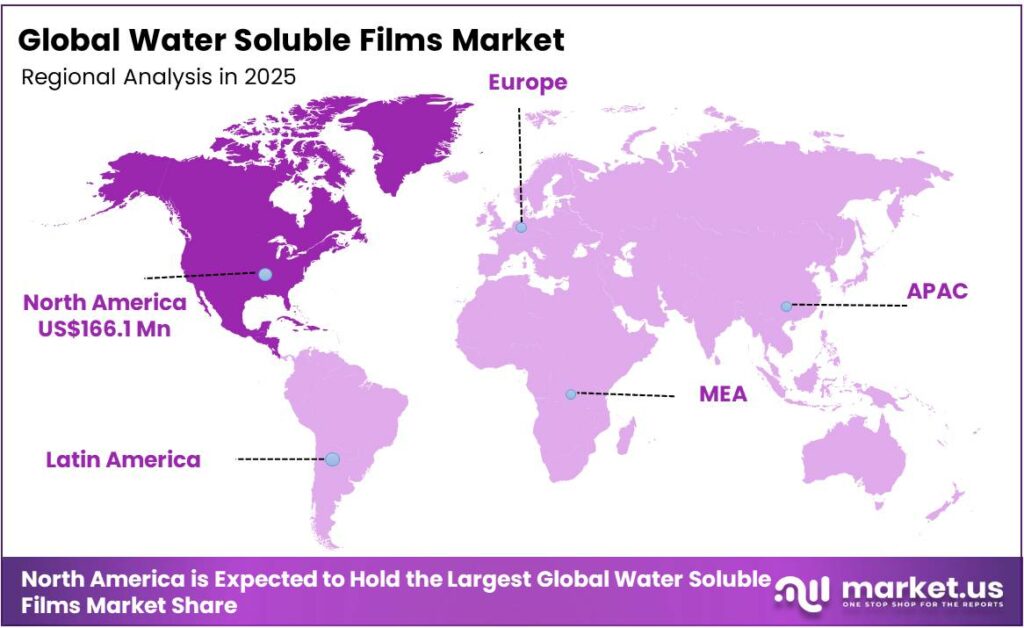

- In 2025, North America was the most dominant region in the water-soluble films market, accounting for 34.8% of the total global consumption.

Type Analysis

Cold Water-soluble Films are a Prominent Segment in the Market.

The water-soluble films market is segmented based on product type into cold water-soluble films and hot water-soluble films. The cold water-soluble films led the market, comprising 83.9% of the market share, primarily due to their broader applicability and ease of use. Cold water-soluble films dissolve at lower temperatures, making them suitable for a wider range of applications, including packaging for household detergents, laundry pods, and personal care products. These films can be used in everyday household environments, where water temperatures are generally not high.

In contrast, hot water-soluble films require elevated temperatures for dissolution, which limits their practical use in consumer-facing products, as it requires specific conditions or equipment. Cold water solubility ensures better consumer convenience and compatibility with a variety of household and industrial processes, contributing to their preference over hot water-soluble alternatives. Additionally, cold water films can dissolve quickly and efficiently at typical washing or cleaning temperatures, enhancing their overall utility.

Thickness Analysis

30-60 μm Water-Soluble Films Dominated the Market.

On the basis of the thickness, the water-soluble films market is segmented into up to 30 μm, 30-60 μm, and above 60 μm. The 30-60 μm water-soluble films dominated the market, comprising 48.1% of the market share, as they strike a balance between durability and solubility, making them ideal for a variety of applications. Films in this thickness range are strong enough to withstand handling during manufacturing, packaging, and transport, while still dissolving efficiently.

Films thinner than 30 μm may be too fragile, making them prone to tearing or breakage during production or application. In contrast, films thicker than 60 μm can be more resistant to dissolution, requiring higher temperatures or longer periods to fully dissolve, which can reduce their effectiveness in consumer products such as laundry pods or single-dose detergents.

Dissolution Rate Analysis

Water-soluble Films That are Most Utilized are Fast-soluble Films.

Based on the dissolution rate, the water-soluble films market is divided into fast-soluble films, medium-soluble films, and slow-soluble films. Fast-soluble films dominated the market, with a notable market share of 60.6%, due to their convenience and efficiency in dissolving under typical usage conditions. These films are ideal for applications such as single-dose detergent pods, where quick dissolution is crucial for immediate product release.

Additionally, fast solubility ensures that the active ingredients, such as detergents or cleaning agents, are quickly activated without delay, improving performance and user satisfaction. In contrast, medium- or slow-soluble films may take longer to dissolve, which can be less desirable for consumer-facing products that prioritize convenience and speed, such as instant beverage packets. Similarly, fast-soluble films enhance consumer experience by reducing residue or film presence.

Application Analysis

Detergent Packaging Held a Major Share of the Water-soluble Films Market.

Among the applications, 37.2% of the total global consumption of water-soluble films is for detergent packaging, due to their ideal characteristics for single-dose, easy-to-use applications. Detergents, particularly in the form of pods, require a material that dissolves rapidly and completely in water, which is a primary strength of water-soluble films. These films offer convenience for consumers, ensuring precise dosing and reducing waste.

In contrast, applications such as agrochemicals, medical, and food packaging often involve more complex regulatory, stability, or safety requirements that water-soluble films may not fully meet. For instance, agrochemicals and pharmaceuticals may require additional barriers to protect sensitive contents from environmental factors. Similarly, food packaging demands stringent safety and durability standards that may not be compatible with the dissolution properties of water-soluble films.

Key Market Segments:

By Type

- Cold Water-soluble Films

- Hot Water-soluble Films

By Thickness

- Up to 30 μm

- 30-60 μm

- Above 60 μm

By Dissolution Rate

- Fast-soluble Films

- Medium-soluble Films

- Slow-soluble Films

By Application

- Detergent Packaging

- Agrochemical Packaging

- Laundry Bags

- Embroidery

- Dye Packaging

- Medical & Pharmaceutical

- Food Packaging

- Others

Drivers

Regulatory Pressures and Environmental Concerns Create the Demand for the Water-soluble Films.

Regulatory pressures and environmental concerns are significant drivers of the water-soluble films market. Environmental concerns about plastic pollution have prompted several countries to focus on reducing plastic consumption. Governments globally are increasingly enforcing stricter regulations on plastic waste and encouraging the adoption of biodegradable materials.

For instance, the European Union’s Single-Use Plastics Directive (2019/904) mandates reductions in single-use plastics, targeting a 50% reduction in specific plastics by 2025, driving demand for alternative materials. Similarly, in the U.S., the Environmental Protection Agency (EPA) has taken steps to regulate plastic waste management, indirectly supporting the development of water-soluble films.

Concurrently, the need to mitigate microplastic pollution accelerates adoption, with PVA-based films meeting OECD 301B standards for biodegradability and demonstrating no relevant aquatic toxicity. Industrial and consumer-focused, applications are further driven by sustainability goals, evidenced by the adoption of water-soluble cement bags to eliminate on-site packaging waste.

Furthermore, the U.S. Department of Agriculture (USDA) has funded studies on water-soluble films for agricultural applications, underlining their environmental benefits. These developments highlight a clear shift toward sustainable practices, with policies increasingly favoring water-soluble films over conventional plastics to curb ecological impact.

Restraints

High Production Costs Pose a Significant Challenge to the Water-soluble Films Market.

The high production costs of water-soluble films present a key challenge to market adoption. A significant cost driver is the raw material expense, particularly for polyvinyl alcohol (PVA), which constitutes the primary polymer used in water-soluble films. PVA is synthesized through the hydrolysis of polyvinyl acetate, which relies on vinyl acetate monomer (VAM) feedstocks, and its price is subject to fluctuations in oil prices.

In addition, the manufacturing process, including polymerization and film-casting, requires specialized equipment to maintain precise control over film thickness. These stages are highly energy-intensive, further escalating operational expenses when industrial energy tariffs rise. This factor increases manufacturing costs compared to conventional plastic film production. The scaling up of biodegradable film production requires capital investment in technology to improve cost efficiency and scalability, which remains a significant barrier for widespread adoption in industries sensitive to material costs, such as packaging and agriculture.

Furthermore, unlike traditional plastics, water-soluble films are highly sensitive to humidity and temperature. This necessitates climate-controlled storage and specialized packaging for transit, which increases total landed costs and complicates global supply chain management.

Opportunity

Application in Household and Consumer Goods Creates Opportunities in the Water-soluble Films Market.

The application of water-soluble films in household and consumer goods serves as a critical expansion opportunity, primarily driven by the transition toward unit-dose concentration and plastic reduction mandates. In the laundry and dishwashing segment, water-soluble polyvinyl alcohol (PVA) films facilitate concentrated liquid and powder delivery. According to the Environmental Protection Agency (EPA), concentrated formulations reduce water content by up to 80%, significantly lowering related carbon emissions.

The water-soluble films are particularly well-suited for single-dose detergent pods, where consumer demand for convenient and eco-friendly products is increasing. Similarly, unlike traditional microplastics, these films used in consumer pods are engineered to be fully biodegradable in wastewater treatment conditions. According to a study published in the National Institutes of Health (NIH), PVA films achieve over 90% biodegradation within 28 days.

Furthermore, pre-measured pouches ensure precise chemical ratios, which prevent the environmental over-saturation of surfactants. This trend aligns with shifting consumer preferences towards environmentally conscious products, creating significant opportunities for water-soluble films in the consumer goods sector.

Trends

Adoption of Edible Water-soluble Films.

The adoption of edible water-soluble films in the food and beverage industry represents a significant shift toward zero-waste, functional packaging solutions. This trend is anchored in the utilization of bio-based polymers to replace synthetic barriers while maintaining food safety and quality. The development of sustainable biodegradable packaging materials is essential for enhancing food quality and shelf life while reducing plastic waste.

Edible films are primarily derived from polysaccharides (e.g., starch, pullulan, alginate), proteins (e.g., whey, soy, gelatin), and lipids. According to a study by the Department of Food Science, University of Massachusetts, advanced bilayer formulations, such as those combining polyvinyl alcohol (PVA) with sodium alginate (SA), have demonstrated ultra-low oil permeability and rapid solubility in hot water, making them suitable for single-serving seasoning oil pouches.

In the U.S., under the Food and Drug Administration (FDA) Title 21 CFR Part 184, standalone edible films are classified as direct food contact materials, further enabling their use in the sector. Similarly, EU Regulation 1935/2004 governs their use in Europe, where the European Food Safety Authority (EFSA) assesses the safety of natural-origin mixtures for food contact. These products must utilize Generally Recognized as Safe (GRAS) substances. This shift reflects demand for sustainable, zero-waste packaging solutions.

Geopolitical Impact Analysis

Geopolitical Uncertainties Have Affected Global Energy Supply Chains.

The geopolitical tensions are influencing the water-soluble films market through disruptions in global supply chains, changes in trade policies, and shifts in raw material availability. For instance, the ongoing conflict between Russia and Ukraine has disrupted the supply of petrochemical derivatives such as polyvinyl alcohol (PVA), a key material used in water-soluble films. The European Union’s sanctions on Russian exports and the instability in Eastern Europe have led to volatility in raw material and energy prices, affecting production costs for film manufacturers.

PVA production is highly energy-intensive and reliant on natural gas-derived feedstocks. According to the European Commission, energy import bills peaked at EUR604 billion in 2022 due to the Russia-Ukraine conflict, and while they receded to EUR427 billion in 2024, industrial electricity rates in the U.K. and Germany remain among the highest globally.

Additionally, trade tensions between the U.S. and China have led to tariffs and restrictions on chemicals and polymers, further complicating the procurement of raw materials for water-soluble films production. The manufacturers have been exploring alternative sourcing strategies, including regional suppliers and alternative biodegradable polymers.

Regional Analysis

North America Held the Largest Share of the Global Water-soluble Films Market.

In 2025, North America dominated the global water-soluble films market, led by the United States, holding about 34.8% of the total global consumption, driven by regulatory support, consumer demand for sustainable packaging, and innovations in biodegradable materials. The U.S. Environmental Protection Agency (EPA) has increasingly supported the adoption of biodegradable alternatives to conventional plastics, encouraging the use of water-soluble films in sectors such as agriculture and household products.

Additionally, the U.S. Food and Drug Administration (FDA) has approved specific water-soluble polymers for direct food contact applications, particularly in packaging. Similarly, initiatives such as the U.S. Zero Waste Program align with consumer and industrial demand for eco-friendly packaging solutions, further promoting the adoption of water-soluble films. The increasing regulatory pressure on single-use plastics in North America, as exemplified by local bans and restrictions, has accelerated the transition to sustainable alternatives such as water-soluble films.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Manufacturers of water-soluble films focus on product innovation, where companies prioritize developing more sustainable and efficient formulations, such as improving the biodegradability or functional properties of their films. R&D investments into new raw materials, including plant-based and renewable polymers, are a key focus to reduce dependence on petrochemicals.

Partnerships and collaborations with industries such as agriculture, packaging, and consumer goods are emphasized by the players. Additionally, manufacturers focus on regional expansion, leveraging local production facilities to reduce lead times and address specific market demands.

The Major Players in The Industry

- Kuraray Co., Ltd.

- Mitsubishi Chemical Group Corporation

- Aicello Corporation

- Sekisui Chemical Co., Ltd.

- Chang Chun Group

- Jiangmen Proudly Water-soluble Plastic Co., Ltd.

- Foshan Polyva Materials Co., Ltd.

- Amtrex Nature Care Pvt. Ltd.

- Arrow GreenTech Ltd.

- Cortec Corporation

- Ecopol SpA

- Noble Industries

- ElephChem Holding Limited

- Medanos Claros HK Limited

- Other Key Players

Key Development

- In October 2025, Novacel launched watersoluble, the first water-soluble adhesive and protective film. This eco-friendly solution combines a biodegradable backing with a soluble adhesive, protecting materials during production and dissolving in water without the use of chemicals.

- In July 2025, DM Group, a leading recycled cartonboard producer, partnered with Ecopol, an expert in biodegradable film technologies, to create a recyclable barrier board. This collaboration combines RDM’s recycled cartonboard with Ecopol’s PVOH film, offering sustainable packaging for various applications.

Report Scope:

Report Features Description Market Value (2025) US$477.3 Mn Forecast Revenue (2035) US$862.9 Mn CAGR (2026-2035) 6.1% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Type (Cold Water-soluble Films and Hot Water-soluble Films), By Thickness (Up to 30 μm, 30-60 μm, and Above 60 μm), By Dissolution Rate (Fast-soluble Films, Medium-soluble Films, and Slow-soluble Films), By Application (Detergent Packaging, Agrochemical Packaging, Laundry Bags, Embroidery, Dye Packaging, Medical & Pharmaceutical, Food Packaging, and Others) Regional Analysis North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA Competitive Landscape Kuraray Co., Ltd., Mitsubishi Chemical Group Corporation, Aicello Corporation, Sekisui Chemical Co., Ltd., Chang Chun Group, Jiangmen Proudly Water-soluble Plastic Co., Ltd., Foshan Polyva Materials Co., Ltd., Amtrex Nature Care Pvt. Ltd., Arrow GreenTech Ltd., Cortec Corporation, Ecopol SpA, Noble Industries, ElephChem Holding Limited, Medanos Claros HK Limited, and Other Players. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)

-

-

- Kuraray Co., Ltd.

- Mitsubishi Chemical Group Corporation

- Aicello Corporation

- Sekisui Chemical Co., Ltd.

- Chang Chun Group

- Jiangmen Proudly Water-soluble Plastic Co., Ltd.

- Foshan Polyva Materials Co., Ltd.

- Amtrex Nature Care Pvt. Ltd.

- Arrow GreenTech Ltd.

- Cortec Corporation

- Ecopol SpA

- Noble Industries

- ElephChem Holding Limited

- Medanos Claros HK Limited

- Other Key Players

Our Clients

- 180641

- Mar 2026