Global Vegetable Protein Market By Source (Soya, Pea, Wheat, Rice), By Form (Dry, Liquid), By Product (Protein Isolates, Concentrates, Textures), By Application (Food And Beverage, Animal Feed, Nutraceuticals And Pharmaceuticals, Others) , By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2025-2034

- Published date: Feb 2026

- Report ID: 177415

- Number of Pages: 204

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

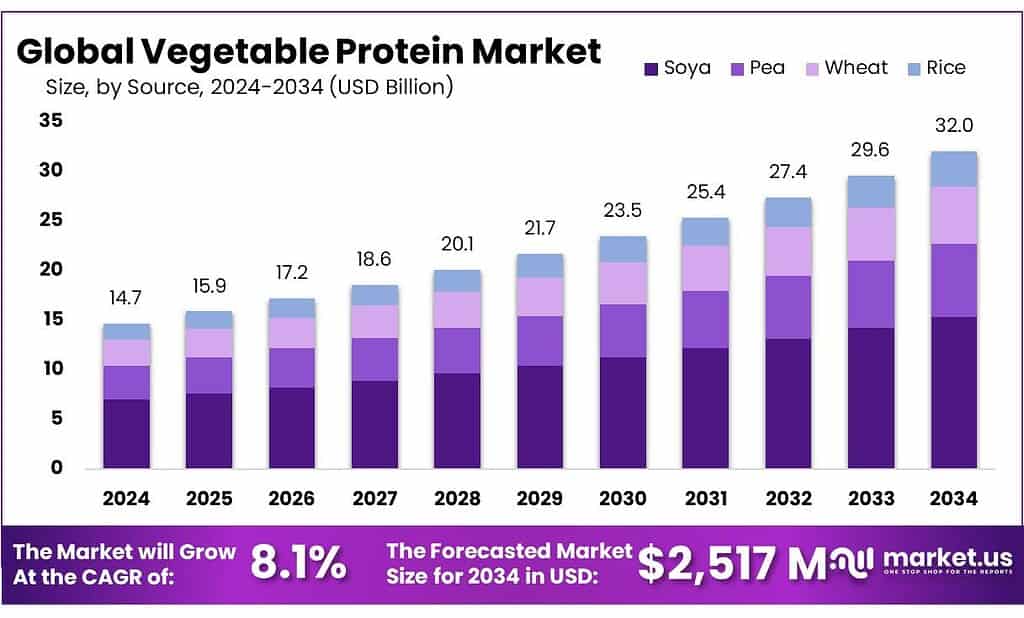

The Global Vegetable Protein Market is expected to be worth around USD 32.0 Billion by 2034, up from USD 14.7 Billion in 2024, and is projected to grow at a CAGR of 8.1% from 2025 to 2034. The North America segment maintained 37.3%, supporting a Shore Power value of USD 5.4 Bn.

Vegetable protein refers to protein ingredients extracted from crops such as soy, peas, wheat, chickpeas, and other pulses, then used in foods, beverages, nutrition powders. On the consumption side, plant-based categories continue to create visibility: global retail sales of plant-based meat/seafood, milk, yogurt, ice cream, and cheese increased 5% to $28.6 billion in 2024, reflecting steady consumer trial even amid pricing pressure.

- In the EU, the arable crop sector supplied 64 million tonnes of crude protein in 2023–24, but the bloc still imports plant-based products equal to 19 million tonnes of crude protein; dry pulses contribute only 1.1 million tonnes, highlighting the gap that processors and farmers are targeting. On the demand side, retail performance shows a “recalibration” rather than a collapse: in the U.S., plant-based meat and seafood dollar sales were $1.2 billion in 2024 and unit sales fell 11%, while certain plant-protein categories posted stronger growth.

Several forces are keeping the sector moving. First, agricultural fundamentals still support long-run protein-crop scaling: the OECD–FAO outlook projects soybean production growth of about 1.0% per year over the coming decade, which matters because soy remains a core industrial protein input.

Second, policy and public R&D are increasingly aligned with protein security and innovation: the European Commission notes it has invested €644 million since 2015 across 125 Horizon projects focused on legumes/protein and related food-chain innovation. In the U.S., the USDA National Institute of Food and Agriculture reports AFRI funding of $445.2 million under the Consolidated Appropriations Act of 2024, supporting the broader research pipeline that ingredient and food companies draw from.

Government initiatives are also pushing the “protein security” angle, particularly through pulses and domestic processing. In India, the Mission for Aatmanirbharta in Pulses launched with a budget of ₹11,440 crore and targets 350 lakh tonnes of pulse production plus 310 lakh hectares under pulses by 2030–31, supporting the upstream pipeline for vegetable protein ingredients. Internationally, policy discussions are explicit about reducing import dependence: the European Commission has maintained an agenda to reduce the EU’s “plant protein deficit,” linking protein crops to resilience and food security priorities.

Key Takeaways

- Vegetable Protein Market is expected to be worth around USD 32.0 Billion by 2034, up from USD 14.7 Billion in 2024, and is projected to grow at a CAGR of 8.1%.

- Soya held a dominant market position, capturing more than a 48.1% share.

- Dry held a dominant market position, capturing more than an 84.6% share.

- Concentrates held a dominant market position, capturing more than a 41.4% share.

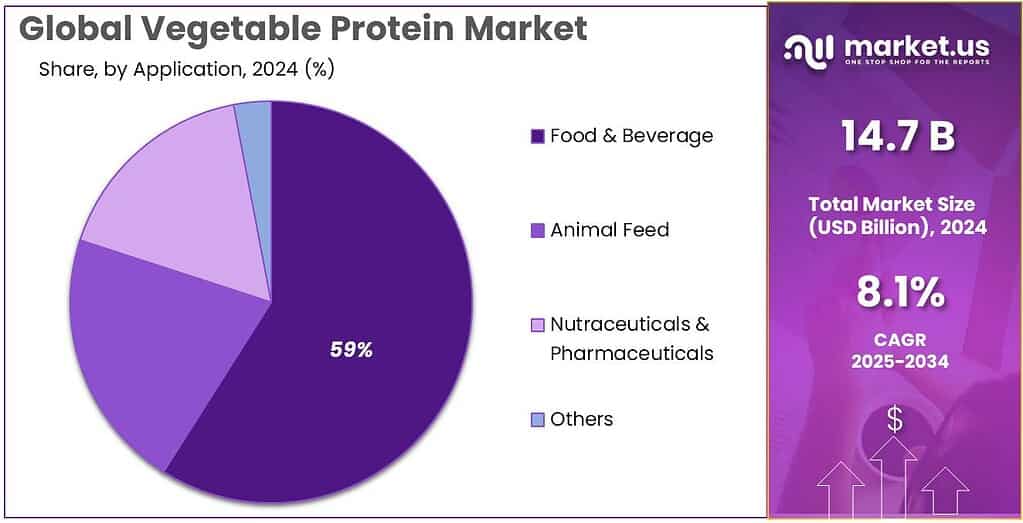

- Food & Beverage held a dominant market position, capturing more than a 59.9% share.

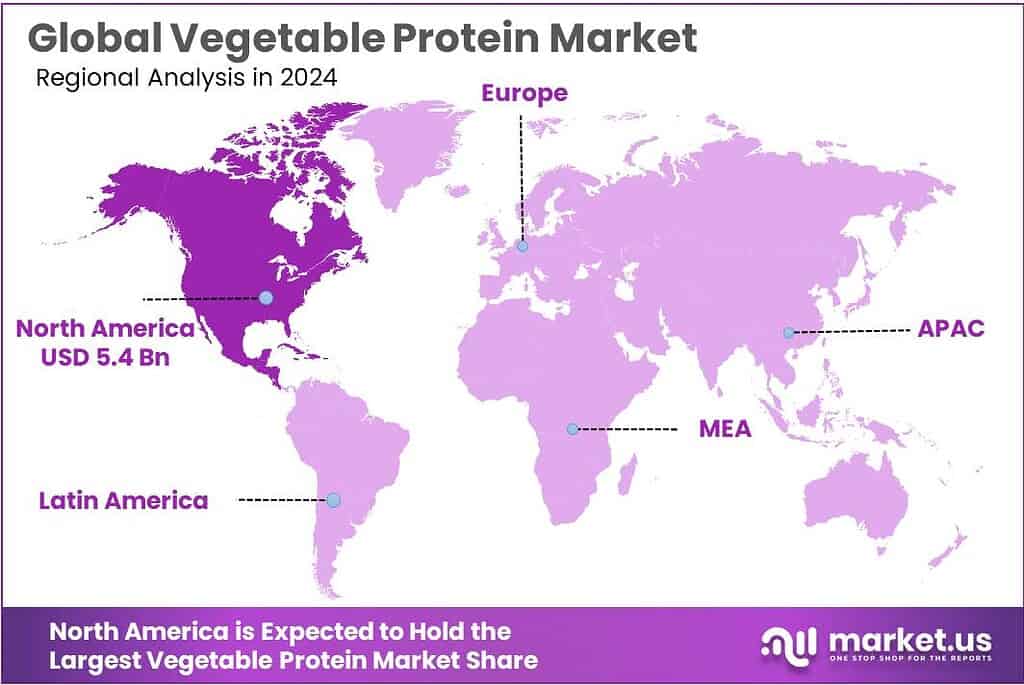

- North America held the dominant regional position in the vegetable protein market, accounting for 37.3% and reaching USD 5.4 Bn

By Source Analysis

Soya dominates with 48.1% owing to its strong global supply base and versatile protein functionality.

In 2024, Soya held a dominant market position, capturing more than a 48.1% share, supported by its large agricultural footprint, mature processing ecosystem, and high protein concentration. The segment benefitted from the consistent rise in global soybean harvests and wide industrial acceptance across food, beverage, and nutrition categories. Global demand for soy protein ingredients strengthened through 2024 as manufacturers focused on affordable, scalable protein sources that maintain texture, emulsification, and stability in everyday formulations.

By Form Analysis

Dry Form dominates with 84.6% because of its longer shelf life and easy industrial handling.

In 2024, Dry held a dominant market position, capturing more than an 84.6% share, mainly because food and beverage manufacturers prefer dry vegetable protein for its stability, convenience, and cost-effective transport. Dry forms—including powders, concentrates, and isolates—fit seamlessly into large-scale processing lines, allowing consistent blending, higher protein loading, and simpler storage without cold-chain requirements. This made dry protein the first choice for bakeries, nutrition brands, plant-based meat formulators, and sports drink manufacturers looking for reliable ingredients at scale.

By Product Analysis

Protein Concentrates dominate with 41.4% due to their balanced cost, nutrition, and formulation flexibility.

In 2024, Concentrates held a dominant market position, capturing more than a 41.4% share, driven by their ideal balance of protein content, affordability, and functional performance across multiple food categories. Manufacturers favored concentrates because they offer moderate protein levels while retaining natural fibers and micronutrients, making them suitable for everyday foods such as bakery items, snacks, cereals, and dairy alternatives. Their milder flavor profile and smooth texture also helped formulators achieve better product consistency without extensive masking or additional processing steps.

By Application Analysis

Food & Beverage dominates with 59.9% as daily nutrition demand and product fortification continue to rise.

In 2024, Food & Beverage held a dominant market position, capturing more than a 59.9% share, driven by strong consumer interest in high-protein foods, plant-based alternatives, and clean-label formulations. Vegetable proteins became essential in everyday categories such as bakery, snacks, cereals, dairy alternatives, and ready-to-drink nutrition beverages. Brands used these proteins to improve texture, enhance mouthfeel, boost protein levels, and meet consumer expectations for healthier, more natural ingredient lists. The segment also grew because vegetable proteins blend well with mainstream food processing systems, allowing manufacturers to scale production easily without major equipment changes.

Key Market Segments

By Source

- Soya

- Pea

- Wheat

- Rice

By Form

- Dry

- Liquid

By Product

- Protein Isolates

- Concentrates

- Textures

By Application

- Food & Beverage

- Animal Feed

- Nutraceuticals & Pharmaceuticals

- Others

Emerging Trends

Shift toward plant-based diets and mainstream acceptance is redefining vegetable protein use

One of the most noticeable trends shaping the vegetable protein landscape today is the mainstream shift toward plant-based eating. What started as a movement led by a relatively small group of health-focused or ethically driven consumers has now become a broader cultural and market force. More people are choosing plant-forward meals not just for health or ethical reasons, but because these foods fit better into everyday life, taste better than before, and align with growing concerns about sustainability. This trend is transforming how vegetable proteins are used — expanding them from niche vegan products into everyday categories that appeal to a wide consumer base.

The growing popularity of plant-based foods is reflected clearly in retail numbers. Global retail sales of plant-based meat, seafood, milk, yogurt, ice cream, and cheese reached $28.6 billion in 2024, marking a 5% increase over previous periods. Even as economic pressures affect consumer spending, this growth shows that people still value plant-based options and the vegetable proteins that make them possible. It signals that plant-based eating is no longer confined to specialty sections of the grocery store — it’s becoming part of everyday shopping habits.

In the United States, the trend is similarly visible. Plant-based retail food sales totaled $8.1 billion in 2024, demonstrating strong consumer interest in plant-led alternatives. These figures include a range of foods where vegetable proteins play a critical role, whether that’s soy protein in dairy-free drinks, pea protein in meat alternatives, or other plant extracts in high-protein snack bars. The broad scope of sales shows that consumers are not just trying these products once — they are buying them repeatedly, and this increases the volume of vegetable protein moving through supply chains.

Government support further reinforces the trend toward plant-led solutions. For instance, India’s Mission for Aatmanirbharta in Pulses has earmarked ₹11,440 crore from 2025–26 to 2030–31, with a goal to push domestic pulse production to 350 lakh tonnes and increase pulse cultivation area to 310 lakh hectares by 2030–31. This kind of support helps stabilize and expand the supply of raw materials used for pulse proteins — peas, chickpeas, lentils — making vegetable protein ingredients more accessible and affordable, especially in large, emerging markets. As production scales, brands can innovate more boldly without being limited by raw-material scarcity or cost spikes.

Drivers

Rising demand for affordable protein fortification in everyday foods is accelerating vegetable protein use

One major driver for vegetable protein is the steady push by food makers to add “more protein” to products people already buy every week. In practical terms, vegetable proteins help brands raise nutrition without completely changing a recipe. They also improve texture and stability in baked goods, snacks, beverages, and ready meals—so the ingredient is valued for performance, not only for health messaging. This is why vegetable protein demand is closely tied to large, daily-consumption categories like dairy alternatives, nutrition drinks, breakfast foods, and plant-forward convenience meals.

This driver is visible in the scale of plant-based retail activity that keeps ingredient pipelines busy. In 2024, global retail sales of plant-based meat, seafood, milk, yogurt, ice cream, and cheese rose 5% to $28.6 billion, showing that consumers continue to buy products where vegetable proteins are a core building block. The same reporting notes that the United States plant-based food retail market totaled $8.1 billion in 2024, reinforcing that this is not a niche shelf; it is a meaningful commercial channel that requires consistent ingredient volumes.

Government initiatives add another layer to this driving factor because they expand the availability of pulse-based proteins used in fortification. In India, the Mission for Aatmanirbharta in Pulses (covering 2025–26 to 2030–31) carries a budget allocation of ₹11,440 crore, with targets to scale domestic pulse production to 350 lakh tonnes and expand cultivation area to 310 lakh hectares by 2030–31. This kind of program supports higher, steadier pulse output over time, which helps ingredient companies offer more pea, lentil, and other pulse protein options for local and export markets.

Restraints

High production and processing costs continue to limit wider adoption of vegetable protein

One major restraint slowing the growth of vegetable protein is the cost burden attached to both crop production and ingredient processing. While demand keeps rising, many manufacturers still struggle to absorb the full cost of protein concentrates and isolates, especially when compared with conventional animal-based proteins or lower-priced carbohydrate ingredients. This cost gap often makes it difficult for food companies to scale high-protein products in mainstream markets, particularly where price sensitivity is high.

A large part of this constraint begins at the agricultural level. Crop prices fluctuate sharply due to weather, fertilizer costs, and global trade conditions, creating volatility in the raw materials used for vegetable proteins. For example, global soybean production remains heavily concentrated in a few regions. For 2024/25, USDA Foreign Agricultural Service projects Brazil to produce 171.5 million metric tons of soybeans and the United States 119.05 million metric tons, making the supply chain highly exposed to disruptions in just two countries.

Processing costs add another layer of pressure. Extracting protein—whether soy, pea, chickpea, or wheat—requires energy-intensive steps such as milling, fractionation, drying, and isolation. These steps become even more expensive when companies aim for high-purity isolates, which are essential for beverages and sports nutrition. While some plant proteins are affordable in concentrate form, isolates remain costly, partly because they require more water, more energy, and more filtration cycles. This is especially challenging for small and mid-sized food brands that cannot easily offset ingredient cost by scaling volume.

Policy efforts also illustrate the scale of investment required just to stabilize upstream supply. In India, the government launched the Mission for Aatmanirbharta in Pulses with a budget of ₹11,440 crore for 2025–26 to 2030–31, targeting 350 lakh tonnes of domestic pulse production. While this initiative aims to support self-reliance, it also highlights how much capital is needed to maintain stable yields for crops like peas and lentils—the very inputs used in vegetable protein processing. The need for such investment reinforces how fragile and cost-intensive the upstream supply chain can be without government intervention.

Opportunity

Growing clean-label and high-protein product demand opens huge opportunities for vegetable proteins

One of the biggest growth opportunities for vegetable protein lies in the accelerating global demand for clean-label and high-protein products. Today’s consumers are not just looking for food that fills them up, they want foods that make them feel better, support their health goals, and fit modern lifestyle values such as sustainability, plant-forward eating, and transparent ingredients. This shift is not just a passing fad; it is reshaping product development in both mainstream and niche categories, and vegetable proteins are right at the heart of this change.

People are increasingly educated about the role of protein in daily nutrition. Diets that prioritize adequate protein intake—whether for weight management, fitness goals, or healthy aging—are becoming more common. Vegetable proteins are especially attractive because they offer protein without cholesterol and with lower saturated fats compared to many animal-based sources. For instance, global plant-based meat and dairy alternatives continue to demonstrate real market scale: in 2024, retail sales of plant-based meat, seafood, milk, yogurt, ice cream, and cheese reached $28.6 billion, growing 5% over the previous period.

In the United States, the plant-based food category also holds strong consumer relevance, with total retail food sales hitting $8.1 billion in 2024. While this number includes both meat and dairy alternatives, it reflects a deeper consumer willingness to pay for foods where vegetable protein is a key ingredient. This kind of consumer engagement creates room for food manufacturers to innovate with new clean-label products that use vegetable protein not as a niche enrichment but as a core functional component.

Government-led initiatives also support this opportunity by nurturing the crop base that feeds the vegetable protein supply chain. For example, India’s Mission for Aatmanirbharta in Pulses allocates ₹11,440 crore for the 2025–26 to 2030–31 period, aiming to boost domestic pulse production to 350 lakh tonnes and cover 310 lakh hectares under pulses by 2030–31. Higher domestic pulse production means greater availability of raw materials for pea, chickpea, and other pulse protein ingredients. This not only supports local food manufacturers but also strengthens export opportunities, making vegetable protein more affordable and accessible globally.

Regional Insights

North America leads with 37.3% share, valued at USD 5.4 Bn, supported by strong retail demand and processing capacity

North America held the dominant regional position in the vegetable protein market, accounting for 37.3% and reaching USD 5.4 Bn, largely because the region combines large-scale crop supply, advanced ingredient processing, and consistent consumer demand for protein-enriched foods.

In the United States, vegetable protein use is closely linked with everyday packaged food innovation—especially dairy alternatives, ready-to-drink nutrition, and plant-based meals. The Good Food Institute reports that the U.S. plant-based food retail market totaled $8.1 billion in 2024, indicating that products relying heavily on plant proteins are firmly established in mainstream grocery.

Supply-side strength reinforces this leadership. The USDA National Agricultural Statistics Service reported U.S. soybean production of 4.37 billion bushels in 2024, which supports large and steady availability of key protein inputs for concentrates and isolates.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Cargill Incorporated – Cargill is a global food and agriculture firm with extensive operations in vegetable protein and textured vegetable protein production. In August 2024, it invested US$300 million in expanding its textured vegetable and soy protein facilities, responding to rising demand for plant-based alternatives and demonstrating long-term commitment to protein capacity growth.

Ingredion Incorporated – Ingredion is a U.S.-based ingredient solutions provider operating in 44 locations with over 12,000 employees worldwide. The company converts plant materials like corn, tapioca, and grains into functional ingredients, including plant proteins for beverages, snacks, and nutrition bars, with broad global reach in over 120 countries.

Archer Daniels Midland (ADM) – ADM is a major U.S. food and agricultural processing company with 44,043 employees and total assets of US$53.3 billion in 2024, making it one of the largest players in vegetable protein ingredients. ADM’s plant protein portfolio includes textured soy, pea, and wheat proteins used in meat substitutes, snacks, and nutrition products.

Top Key Players Outlook

- Archer Daniels Midland (ADM)

- Cargill Incorporated

- Roquette Frères

- Ingredion Incorporated

- Kerry Group plc

- Wilmar International

- DuPont Nutrition & Health

- International Flavors & Fragrances (IFF)

- Bunge Limited

- Glanbia plc

Recent Industry Developments

ADM reported $101.160 billion in revenue from external customers in 2024, with the Nutrition segment contributing $7.636 billion of that total, showing the size of the higher-value ingredient engine behind its plant-protein push.

Roquette’s global footprint includes more than 40 industrial sites and 20 R&D labs, supporting ingredient development and quality control worldwide.

Report Scope

Report Features Description Market Value (2024) USD 14.7 Bn Forecast Revenue (2034) USD 32.0 Bn CAGR (2025-2034) 8.1% Base Year for Estimation 2024 Historic Period 2020-2023 Forecast Period 2025-2034 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Source (Soya, Pea, Wheat, Rice), By Form (Dry, Liquid), By Product (Protein Isolates, Concentrates, Textures), By Application (Food And Beverage, Animal Feed, Nutraceuticals And Pharmaceuticals, Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA Competitive Landscape Archer Daniels Midland (ADM), Cargill Incorporated, Roquette Frères, Ingredion Incorporated, Kerry Group plc, Wilmar International, DuPont Nutrition & Health, International Flavors & Fragrances (IFF), Bunge Limited, Glanbia plc Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- Archer Daniels Midland (ADM)

- Cargill Incorporated

- Roquette Frères

- Ingredion Incorporated

- Kerry Group plc

- Wilmar International

- DuPont Nutrition & Health

- International Flavors & Fragrances (IFF)

- Bunge Limited

- Glanbia plc

Our Clients

- 177415

- Feb 2026