Global Turf And Ornamental Inputs Market Size, Share Analysis Report By Turf Grass Type (Bermuda Grass, Zoysia Grass, Kentucky Bluegrass, Ryegrass, Tall Fescue, Others), By Ornamental Grass Type (Feather Reed Grass, Fountain Grass, Purple Millet, Ravenna Grass, Fiber Optic Grass, Others), By Input Type (Pesticides, Fertilizers, Plant Growth Regulators, Wetting Agents and Surfactants, Bio-stimulants) , By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2026-2035

- Published date: April 2026

- Report ID: 183804

- Number of Pages: 230

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

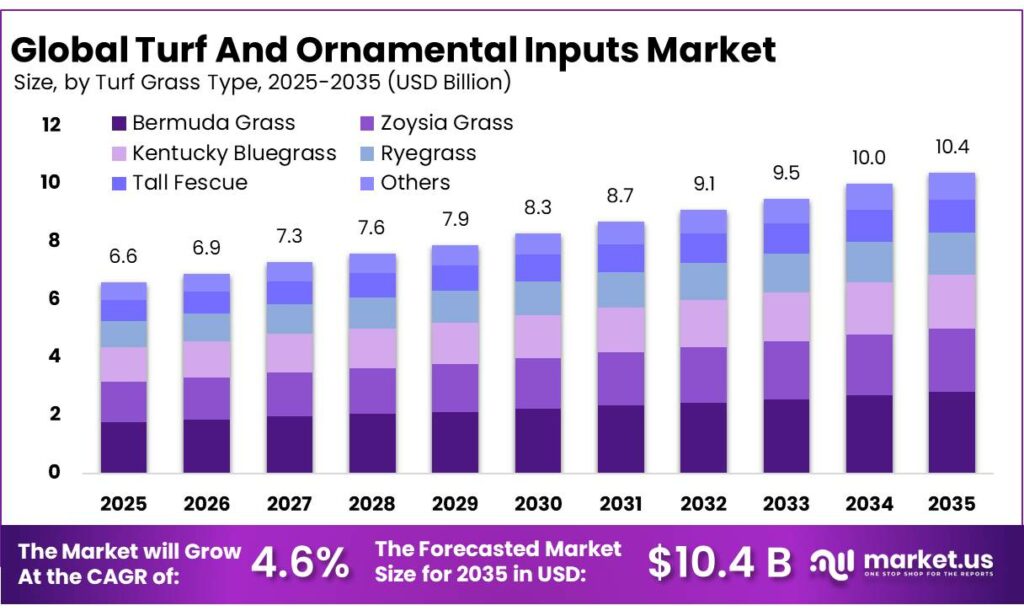

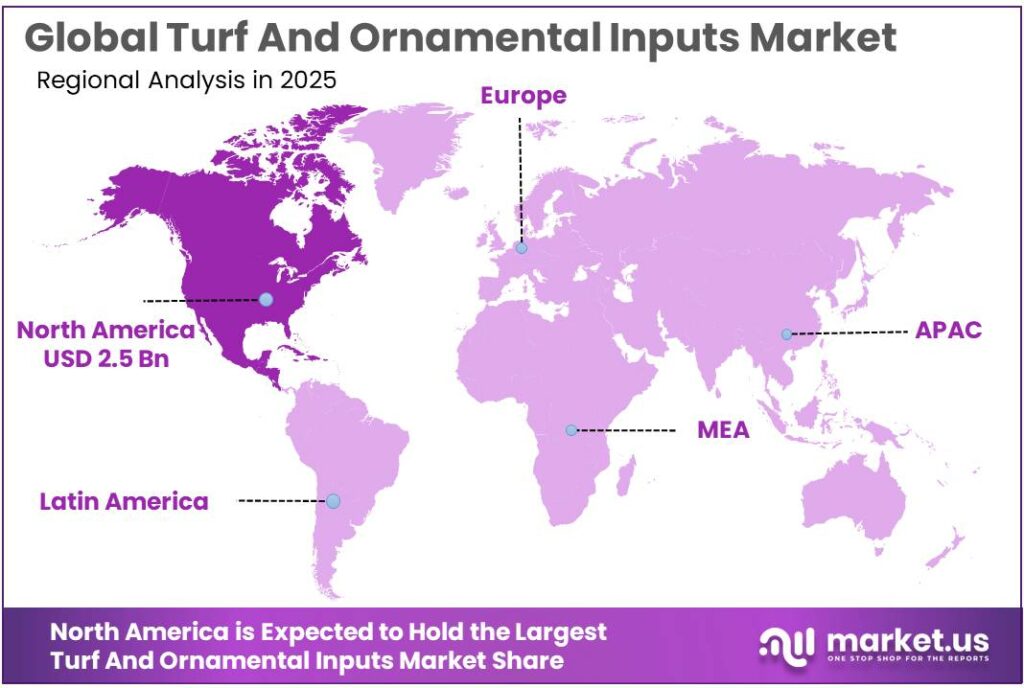

The Global Turf And Ornamental Inputs Market size is expected to be worth around USD 10.4 Billion by 2035, from USD 6.6 Billion in 2025, growing at a CAGR of 4.6% during the forecast period from 2026 to 2035. In 2025, North America held a dominant market position, capturing more than a 38.2% share, holding USD 2.5 Billion revenue.

The turf and ornamental inputs industry sits at the intersection of landscape management, golf-course agronomy, nursery production, floriculture, and urban green infrastructure. Its commercial logic is supported by the broader ornamental horticulture economy, which AIPH valued at $70 billion in 2024, while USDA reported $18.3 billion in U.S. horticultural sales in 2024, including $5.34 billion in nursery stock, $2.67 billion in annual bedding plants, and $1.70 billion in sod.

In parallel, USDA’s floriculture summary showed $6.69 billion in total floriculture crop sales in 2023 and 10,216 producers, indicating a large and diversified downstream base for fertilizers, crop protection, biostimulants, wetting agents, seed, and plant-health products.

From an industrial scenario perspective, demand is being reinforced by the expansion and professionalization of managed turf surfaces and ornamental plant systems. The R&A reported that in its affiliated markets there were 108 million golfers in 2024, with 43.3 million people playing on 9- and 18-hole courses, up from 42.7 million in 2023. That matters because golf, sports turf, municipal landscapes, and premium residential landscapes require intensive input programs for disease control, insect management, nutrition, color, water retention, and stress tolerance.

The main growth drivers are increasingly agronomic rather than purely aesthetic. Water efficiency is becoming central: the U.S. EPA states that outdoor water use accounts for more than 30% of household water use on average and can reach 60% in arid regions. This is increasing demand for wetting agents, soil conditioners, stress-mitigation chemistries, and precision irrigation-compatible inputs. Regulation is also reshaping product mix. The European Commission states that the Sustainable Use Directive remains in force, while the earlier proposal linked to Farm to Fork had aimed at 50% reduction in the use and risk of chemical pesticides by 2030.

Government-backed support remains relevant: USDA states that the Specialty Crop Research Initiative provides up to $80 million per year, while USDA also added $650 million in January 2025 to the Marketing Assistance for Specialty Crops program. Because U.S. law explicitly includes horticulture, nursery crops, and floriculture within specialty crops, these initiatives indirectly strengthen the innovation pipeline and commercial resilience of ornamental input demand.

BASF, meanwhile, reported €9.798 billion in 2024 Agricultural Solutions sales and €1.938 billion EBITDA before special items in its 2024 report published in 2025, while its 2025 Factbook said the company would complete the legal separation of Agricultural Solutions and BASF’s Professional & Specialty Solutions unit continues to target reduced nitrogen emissions and improved tree, shrub, flower, turf, and soil health.

Key Takeaways

- Turf And Ornamental Inputs Market size is expected to be worth around USD 10.4 Billion by 2035, from USD 6.6 Billion in 2025, growing at a CAGR of 4.6%.

- Bermuda Grass held a dominant market position, capturing more than a 27.9% share.

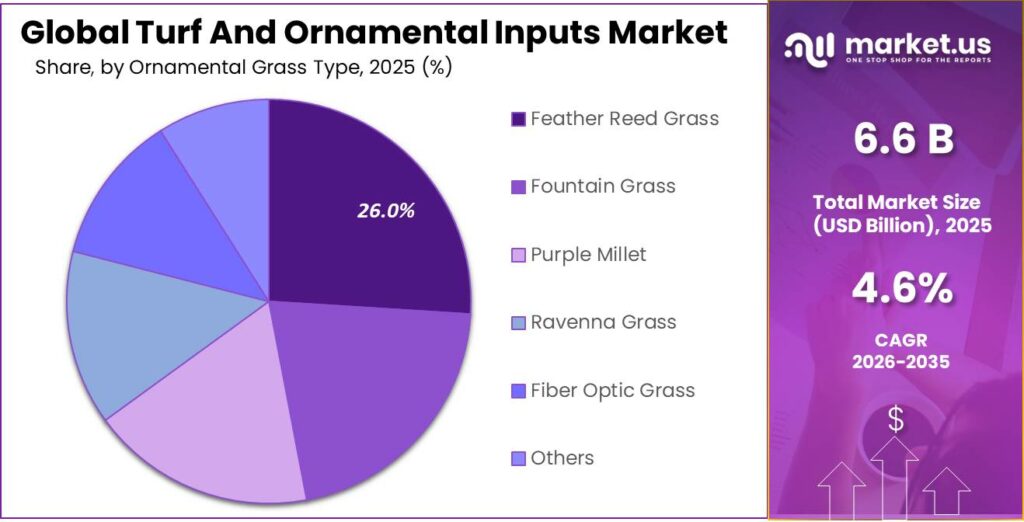

- Feather Reed Grass held a dominant market position, capturing more than a 26.5% share.

- Fertilizers held a dominant market position, capturing more than a 36.3% share.

- North America emerged as the dominant regional market in the turf and ornamental inputs industry, accounting for 38.2% of the global market and valued at USD 2.5 Bn.

By Turf Grass Type Analysis

Bermuda Grass dominates with 27.9% share, supported by strong use across sports fields and premium landscaped turf areas.

In 2025, Bermuda Grass held a dominant market position, capturing more than a 27.9% share in the turf and ornamental inputs market by turf grass type. Its leading position was mainly supported by its strong acceptance across golf courses, sports grounds, commercial landscapes, and high-traffic recreational lawns, where durability and fast recovery remain critical purchase factors. The segment continued to benefit from Bermuda grass’s natural tolerance to heat, drought, and repeated foot movement, making it one of the most preferred warm-season turf choices in professionally managed green spaces.

By Ornamental Grass Type Analysis

Feather Reed Grass leads with 26.5% share, driven by strong landscaping demand and low-maintenance ornamental appeal.

In 2025, Feather Reed Grass held a dominant market position, capturing more than a 26.5% share in the turf and ornamental inputs market by ornamental grass type. This segment’s leadership was mainly supported by its growing use in commercial landscapes, public gardens, urban beautification projects, and premium residential spaces where structured visual appeal and year-round texture are highly valued. Feather reed grass remained a preferred choice among landscape planners because of its upright growth habit, neat appearance, and ability to perform well across seasonal transitions with relatively low upkeep.

By Input Type Analysis

Fertilizers lead with 36.3% share, backed by their essential role in year-round turf strength and ornamental plant quality.

In 2025, Fertilizers held a dominant market position, capturing more than a 36.3% share in the turf and ornamental inputs market by input type. This leading position was mainly supported by the constant need to maintain healthy turf density, uniform green color, strong root systems, and consistent ornamental plant growth across managed landscapes. Fertilizers remained the most widely used input category because both turfgrass surfaces and ornamental plants require regular nutrient replenishment to sustain visual quality and performance under varying climate conditions.

Key Market Segments

By Turf Grass Type

- Bermuda Grass

- Zoysia Grass

- Kentucky Bluegrass

- Ryegrass

- Tall Fescue

- Others

By Ornamental Grass Type

- Feather Reed Grass

- Fountain Grass

- Purple Millet

- Ravenna Grass

- Fiber Optic Grass

- Others

By Input Type

- Pesticides

- Fertilizers

- Plant Growth Regulators

- Wetting Agents and Surfactants

- Bio-stimulants

Emerging Trends

Smart irrigation and water-saving inputs are the latest defining trend

One of the most important latest trends in the turf and ornamental inputs industry is the fast shift toward smart irrigation-linked input programs. In 2025 and moving into 2026, turf managers are no longer using fertilizers, wetting agents, and soil conditioners as standalone products. Instead, these inputs are increasingly being selected based on how well they work with sensor-based irrigation, moisture mapping, and water-saving landscape systems.

The U.S. EPA notes that outdoor water use accounts for more than 30% of total household water use on average, and can reach 60% in arid regions, while as much as 50% of outdoor water can be lost through evaporation, wind, and runoff from inefficient irrigation.

Soil biology and sustainable nutrition blends are becoming mainstream

A second strong trend is the rising use of soil biology-based and sustainable nutrition blends across turfgrass and ornamental landscapes. In 2025, more golf facilities, municipalities, and landscape contractors are shifting toward microbial enhancers, biofertilizers, and carbon-based soil health products that improve root performance naturally.

A strong support point comes from the USDA’s Specialty Crop Research Initiative, which continues to provide up to $80 million per year for research into productivity, pest management, climate resilience, and technology innovation across specialty crop systems.

Drivers

Water-efficient landscape management is a major growth driver for turf and ornamental inputs

One of the strongest driving factors for the turf and ornamental inputs industry is the rising need for water-efficient landscape management. In 2025, this has become a major priority for golf courses, sports fields, commercial lawns, and decorative landscapes, especially in regions facing tighter water-use regulations and higher irrigation costs. The U.S. EPA states that outdoor water use typically accounts for nearly 30% of household water use, and in dry regions it can reach almost 60%, which directly pushes demand for specialty fertilizers, wetting agents, soil conditioners, and moisture-retention inputs used in turf systems.

Government support and conservation programs are strengthening long-term demand

A second major factor supporting this driver is the role of government-backed conservation and specialty crop support programs, which continue to strengthen the broader innovation ecosystem around turf and ornamental care. USDA’s FY 2025 performance and budget documents continue to emphasize water conservation, climate resilience, and protection of specialty crops and ornamental trees through federal agricultural and land stewardship programs. USDA also highlighted progress in pest-risk mapping, with 24 cumulative climate suitability maps completed for high-risk pests, helping protect ornamental trees and managed green spaces from destructive outbreaks.

Restraints

Stringent pesticide and fertilizer regulations are a major restraint for turf and ornamental inputs

One of the biggest restraining factors for the turf and ornamental inputs market is the tightening regulation around pesticide and fertilizer use, especially in professional turf, golf, municipal landscapes, and ornamental plant maintenance. In 2025, compliance pressure has become a real operational challenge for input manufacturers as well as end users.

The U.S. EPA continues to require extensive scientific data before any pesticide can remain in the market, covering effects on humans, wildlife, plants, and water systems. These requirements are governed under 40 CFR Part 158, and the agency updated its pesticide data submission framework again in January 2026, making registration pathways more documentation-heavy and time-consuming.

Use restrictions and buffer rules are reducing flexibility in field applications

Another major pressure point is the increasing number of site-level use restrictions and application limits, which make routine turf and ornamental maintenance more difficult. A strong 2025 example comes from EPA’s updated herbicide mitigation measures, which include a 240-foot downwind buffer, a single-use cap of 0.5 lb acid equivalent per acre, and no more than two applications annually for certain products. While these rules are designed to protect ecosystems and surrounding vegetation, they reduce operational flexibility for golf courses, sports fields, parks, and ornamental landscape contractors that depend on precise weed and disease control windows.

Opportunity

Biological and sustainable inputs are creating the biggest growth opportunity

One of the strongest growth opportunities in the turf and ornamental inputs industry is the rapid shift toward biological and sustainable plant nutrition solutions. In 2025 and moving into 2026, turf managers, golf facilities, nurseries, and ornamental landscape operators are increasingly looking for products that improve plant health while reducing chemical load and nutrient losses.

This is creating strong room for biofertilizers, microbial soil enhancers, biostimulants, and natural stress-management inputs. A major support point comes from the USDA’s Specialty Crop Research Initiative, which provides up to $80 million per year for integrated research and extension projects focused on critical specialty crop challenges, including productivity, pest management, and technology innovation.

Smart nutrition and climate-resilient turf programs will open long-term expansion

A second major opportunity lies in climate-resilient nutrition and soil health programs, especially for sports turf, golf courses, and high-value landscape assets exposed to heat and water stress. USDA’s SCRI legislative priorities specifically include improving production efficiency, long-term profitability, pest control, and new innovations in mechanization and technologies, which strongly supports advanced nutrient delivery systems and precision input programs for turf and ornamental use.

This creates a favorable path for controlled-release fertilizers, microbial root-zone products, wetting agents, and carbon-based soil conditioners that help maintain turf quality under limited water and rising temperatures. From a practical industry view, buyers are no longer focused only on greener appearance; they are investing in products that extend turf life, reduce renovation frequency, and improve recovery from environmental stress.

Regional Insights

North America dominates with 38.2% share, reaching USD 2.5 Bn, supported by mature turf care infrastructure and large-scale ornamental landscaping demand.

North America emerged as the dominant regional market in the turf and ornamental inputs industry, accounting for 38.2% of the global market and valued at USD 2.5 Bn. The region’s leadership is strongly supported by its highly developed turf management ecosystem across golf courses, sports stadiums, public parks, institutional campuses, and premium residential landscapes.

The United States remains the key revenue contributor, where demand for fertilizers, plant protection chemicals, wetting agents, seed treatments, and soil health products stays consistently high due to intensive maintenance standards. A strong support base comes from the USDA, which reported that U.S. horticulture operations generated USD 18.3 billion in floriculture, nursery, and specialty crop sales in 2024, highlighting the size of the downstream ornamental and managed green-space economy that directly consumes these inputs.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Bayer AG remains a leading player in turf and ornamental inputs through its strong Crop Science portfolio, widely used in turf fungicides, herbicides, insecticides, and ornamental plant health solutions. In 2025, Bayer’s Crop Science sales reached €21.622 billion, supported by continued demand for seed and crop protection technologies. The company’s strength in disease control for golf courses, sports turf, and landscape maintenance supports its premium market position. Its broad innovation pipeline and digital agronomy tools also improve nutrient efficiency and pest management performance across professional turf systems.

Syngenta Group holds a strong position in turf and ornamental inputs through advanced crop protection chemistry, biologicals, and specialty seed technologies used in managed landscapes. In 2024, the company reported $28.8 billion in sales, and it indicated that the crop protection market is expected to stabilize through 2025. Syngenta’s turf portfolio is widely used across golf greens, sports fields, and ornamental nurseries, particularly for fungicide-led disease prevention and stress management. The company’s continued investments in R&D, biological nitrogen solutions, and precision application systems strengthen its long-term influence in premium turf care programs.

BASF SE is one of the most established suppliers in the turf and ornamental inputs market, especially in fungicides, herbicides, soil health solutions, and professional landscape care products. In the 2025 business year, BASF’s Agricultural Solutions sales stood at €9,587 million, highlighting its strong scale in crop and specialty plant protection. BASF’s products are widely adopted in golf course management, sports turf renovation, and ornamental shrub protection. Its continued focus on sustainable chemistry, stress-tolerance solutions, and biological research supports stable demand in high-value landscape maintenance applications.

Top Key Players Outlook

- Bayer AG

- Syngenta Group

- BASF SE

- FMC Corporation

- Nufarm Ltd

- American Vanguard Corporation

- Koch Agronomic Services

- Gowan International

- Precision Laboratories

- UPL Limited

- Valent USA

- SiteOne Landscape Supply Inc

- LebanonTurf

Recent Industry Developments

In 2025, Bayer’s Crop Science division reported sales of €21.622 billion, showing a 1.1% increase, which reflects the company’s stable performance in professional plant health and landscape care solutions.

In 2025, Syngenta Crop Protection sales reached USD 9.8 billion for the first nine months, showing 3% growth, while the overall group reported USD 20.9 billion in sales and USD 3.4 billion EBITDA, reflecting stable commercial momentum.

Report Scope

Report Features Description Market Value (2025) USD 6.6 Bn Forecast Revenue (2035) USD 10.4 Bn CAGR (2026-2035) 4.6% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Turf Grass Type (Bermuda Grass, Zoysia Grass, Kentucky Bluegrass, Ryegrass, Tall Fescue, Others), By Ornamental Grass Type (Feather Reed Grass, Fountain Grass, Purple Millet, Ravenna Grass, Fiber Optic Grass, Others), By Input Type (Pesticides, Fertilizers, Plant Growth Regulators, Wetting Agents and Surfactants, Bio-stimulants) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA Competitive Landscape Bayer AG, Syngenta Group, BASF SE, FMC Corporation, Nufarm Ltd, American Vanguard Corporation, Koch Agronomic Services, Gowan International, Precision Laboratories, UPL Limited, Valent USA, SiteOne Landscape Supply Inc, LebanonTurf Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Turf And Ornamental Inputs MarketPublished date: April 2026add_shopping_cartBuy Now get_appDownload Sample

Turf And Ornamental Inputs MarketPublished date: April 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Bayer AG

- Syngenta Group

- BASF SE

- FMC Corporation

- Nufarm Ltd

- American Vanguard Corporation

- Koch Agronomic Services

- Gowan International

- Precision Laboratories

- UPL Limited

- Valent USA

- SiteOne Landscape Supply Inc

- LebanonTurf

Our Clients

- 183804

- April 2026