Global Surface to Air Missiles Market Size, Share, Growth Analysis By Range (Very Short Range, Short Range, Medium Range, Long Range, Extended Range), By Launch Platform (Man-Portable, Mobile/Land Vehicle-Mounted, Fixed-Site Ground Installations, Naval-based), By Propulsion Type (Solid, Liquid, Hybrid, Cryogenic, Ramjet/Scramjet), By Guidance (Command-guided, Semi-Active Radar Homing, Infrared (IR) Homing, Laser-guided), By Speed Class (Subsonic, Supersonic, Hypersonic), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Apr 2026

- Report ID: 183780

- Number of Pages: 210

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

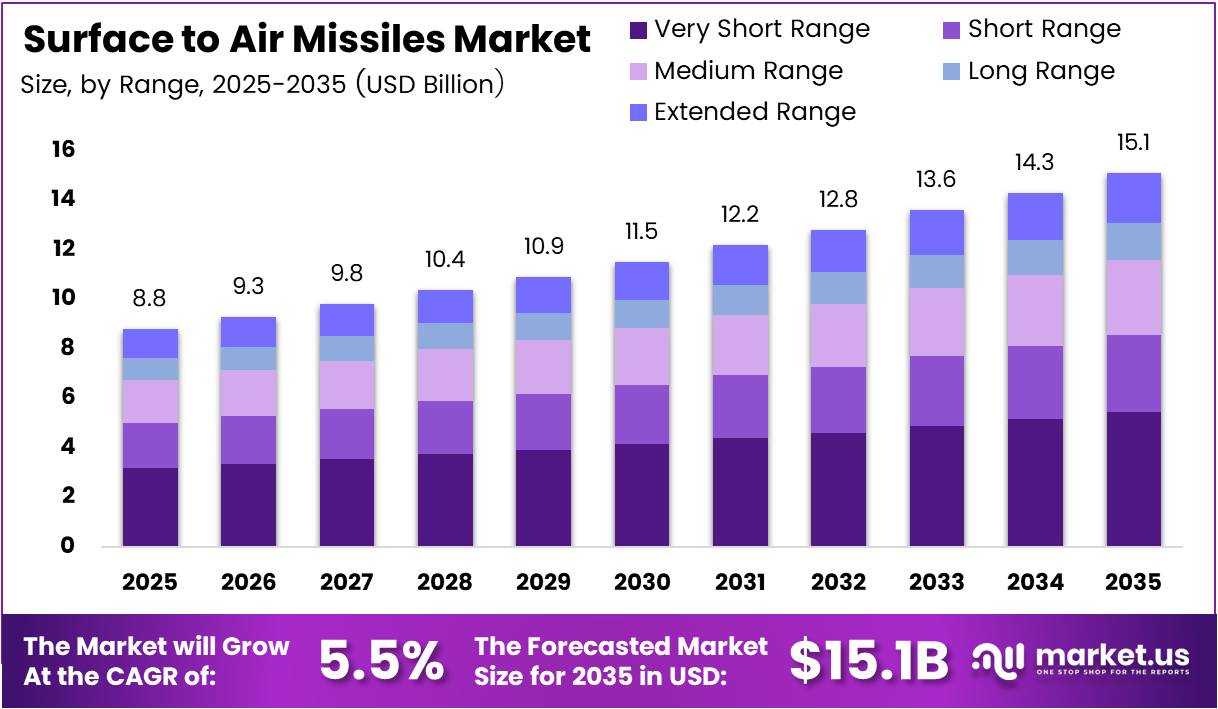

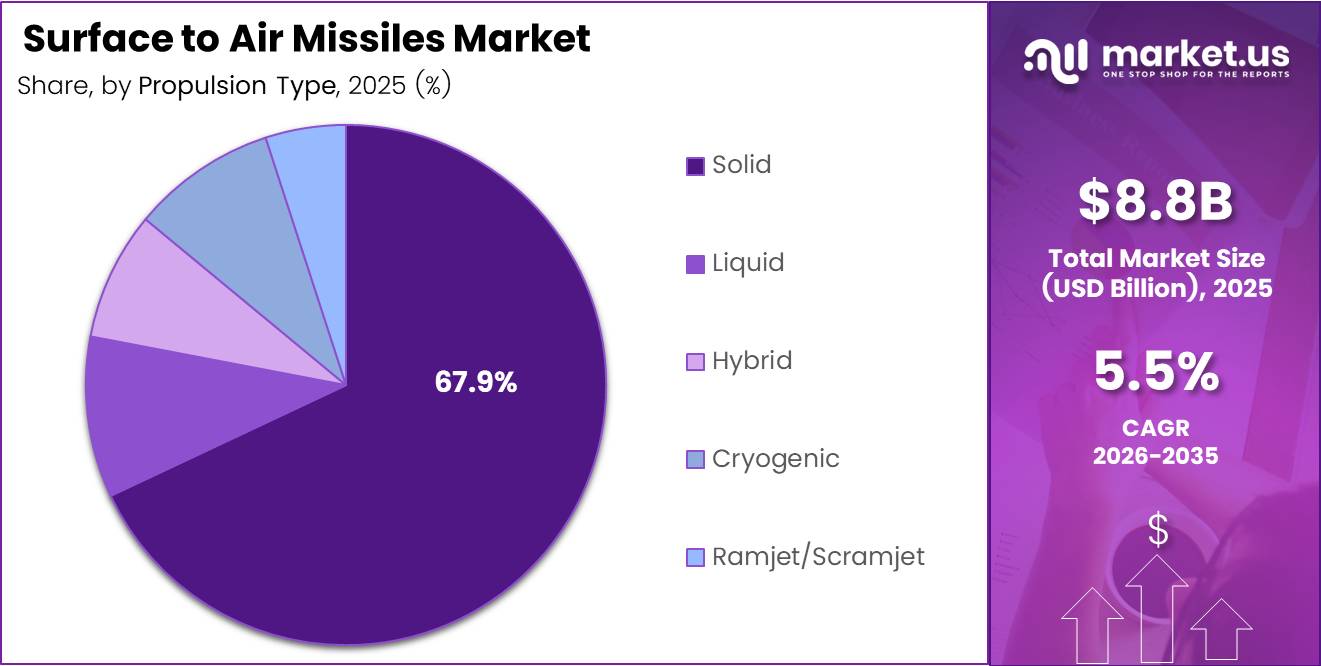

Global Surface to Air Missiles Market size is expected to be worth around USD 15.1 Billion by 2035 from USD 8.8 Billion in 2025, growing at a CAGR of 5.5% during the forecast period 2026 to 2035.

The surface-to-air missile (SAM) market covers ground and naval-launched defensive weapon systems designed to detect, track, and neutralize airborne threats including fighter aircraft, ballistic missiles, cruise missiles, and unmanned aerial vehicles. These systems range from man-portable units to complex integrated air defense networks. Modern SAM platforms combine radar, command-and-control software, and multi-role interceptors.

Defense procurement cycles now treat air defense as a top-tier budget priority. Nations across Europe, Asia-Pacific, and the Middle East are restructuring their air defense architectures in response to demonstrated battlefield threats. The Ukraine conflict and the Israel-Iran exchanges have turned SAM performance data into procurement arguments — giving vendors concrete evidence of system effectiveness to present to government buyers.

The 5.5% CAGR reflects a structural shift: air defense is no longer a supplementary capability but a core defense investment. Governments are replacing aging single-layer systems with multi-tiered architectures that require continuous interceptor replenishment, radar upgrades, and integration software — creating sustained multi-year revenue streams for prime contractors.

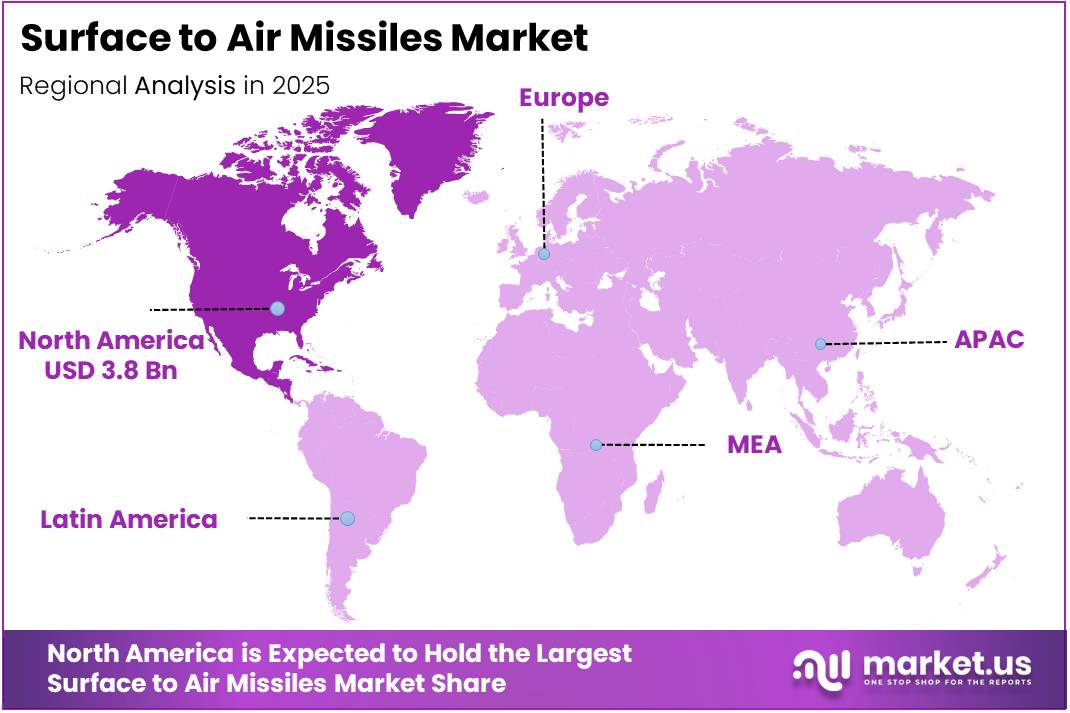

North America holds the largest regional share at 43.70%, valued at approximately USD 3.8 Billion. This position reflects decades of procurement infrastructure, NATO interoperability standards, and home-country advantage for major SAM system developers. The U.S. market also sets baseline performance requirements that cascade into allied procurement decisions globally.

Iron Dome maintains 85–90% sustained effectiveness across multiple conflicts and has intercepted over 4,000 projectiles since 2011, with overall combat success reported above 90%. This combat-proven track record directly drives allied procurement confidence — buyers now reference operational data rather than test results when approving defense budgets.

According to defence analysts, by March 2026, the IDF’s integrated air defense system achieved a reported 92% success rate intercepting incoming missile and drone threats operating with U.S. support. This figure signals that multi-nation system integration amplifies individual platform performance — a finding that accelerates joint procurement and interoperability investment among allied defense networks.

The IRIS-T SLM system in Ukraine reported approximately 99% interception rate with over 240 confirmed kills, including a single battery neutralizing 15 cruise missiles in one engagement. For procurement decision-makers, this operational data eliminates theoretical performance risk and shortens approval cycles — compressing what were multi-year budget debates into expedited acquisition decisions.

Key Takeaways

- The global Surface to Air Missiles Market was valued at USD 8.8 Billion in 2025 and is forecast to reach USD 15.1 Billion by 2035.

- The market grows at a CAGR of 5.5% during the forecast period 2026 to 2035.

- North America leads all regions with a 43.70% market share, valued at approximately USD 3.8 Billion.

- By Range, Very Short Range dominates with a 35.7% share of the SAM market.

- By Launch Platform, Mobile/Land Vehicle-Mounted systems hold 48.5% share, the largest platform segment.

- By Propulsion Type, Solid propulsion leads with 67.9% share, reflecting operational readiness requirements.

- By Guidance, Infrared (IR) Homing holds 41.4% share in the guidance segment.

- By Speed Class, Subsonic systems account for 61.2% of the market by speed classification.

Product Analysis

Very Short Range dominates with 35.7% due to widespread frontline tactical deployment demand.

In 2025, Very Short Range held a dominant market position in the By Range segment of the Surface to Air Missiles Market, with a 35.7% share. These systems serve as the last layer of point defense against low-altitude threats including drones, helicopters, and precision munitions. Their portability and rapid deployment capability make them the most procured category across both conventional and asymmetric conflict scenarios.

Short Range systems bridge the gap between man-portable units and medium-range batteries. They protect forward operating bases, critical infrastructure, and mobile military formations. Their integration with mobile platforms extends battlefield coverage without requiring fixed installations, making them attractive for armies conducting rapid-tempo operations.

Medium Range systems form the backbone of national air defense architecture. They provide area coverage against aircraft and cruise missiles and typically anchor multi-layered defense networks. The growing complexity of aerial threat environments pushes militaries toward medium-range platforms that can engage multiple threat classes simultaneously.

Long Range systems address ballistic missile defense and high-altitude aircraft threats. Their higher unit cost and longer procurement cycles mean purchase volumes are lower, but contract values are substantially larger. Nations investing in long-range SAM capability are typically building sovereign deterrence infrastructure rather than replacing existing assets.

Extended Range systems represent the most advanced tier, targeting hypersonic and exo-atmospheric threats. Development programs in this category carry the highest R&D investment. The SAMP/T NG achieved a confirmed Sukhoi aircraft kill at approximately 100 km range in Ukraine in March 2025, validating extended-range performance under combat conditions and strengthening the procurement case for this segment.

Launch Platform Analysis

Mobile/Land Vehicle-Mounted dominates with 48.5% due to operational flexibility in high-tempo warfare.

In 2025, Mobile/Land Vehicle-Mounted systems held a dominant market position in the By Launch Platform segment of the Surface to Air Missiles Market, with a 48.5% share. Their ability to reposition between engagements reduces vulnerability to counter-battery fire, a lesson reinforced by Ukraine combat experience. Militaries now treat mobility as a survival requirement, not a convenience feature.

Man-Portable systems deliver individual-soldier air defense capability against low-flying threats. Their low cost per unit and minimal logistical footprint make them the most distributed SAM format globally. However, their single-operator design limits engagement altitude and target complexity, positioning them as a complement to vehicle-mounted and fixed systems rather than a replacement.

Fixed-Site Ground Installations anchor permanent national air defense networks protecting capitals, nuclear sites, and strategic infrastructure. Their higher radar power, larger interceptor loads, and integrated command systems allow engagement of the widest threat spectrum. Fixed installations command the highest per-unit contract values, even though their share by volume is lower than mobile platforms.

Naval-based SAM platforms protect carrier strike groups, amphibious fleets, and littoral zones. Naval procurement cycles differ from land systems — driven by fleet modernization timelines and hull replacement schedules rather than conflict response. However, the growing threat of anti-ship missiles is accelerating naval SAM upgrade programs across multiple Pacific and Mediterranean navies.

Propulsion Type Analysis

Solid propulsion dominates with 67.9% due to readiness, storage stability, and field reliability.

In 2025, Solid propulsion held a dominant market position in the By Propulsion Type segment of the Surface to Air Missiles Market, with a 67.9% share. Solid-fuel motors require no cryogenic handling, no fueling time, and withstand harsh field conditions — qualities that directly map to military operational requirements. Patriot PAC-3 interceptors, which achieved 100% success against Russian Kinzhal hypersonic missiles in Ukraine, use solid propulsion, validating its real-world reliability at the highest performance levels.

Liquid propulsion systems offer higher specific impulse for long-range and high-altitude intercepts. However, their handling complexity and storage sensitivity limit their battlefield deployment. Liquid-fueled SAMs are predominantly found in legacy systems and fixed-site installations where infrastructure exists to support fueling operations.

Hybrid propulsion combines elements of solid and liquid systems to improve performance flexibility. Development programs targeting this category seek the energy density of liquid fuels with the handling simplicity of solid motors. Hybrid propulsion remains early-stage for SAM applications, with most programs still in testing rather than fielded deployment.

Cryogenic propulsion is limited to specialized high-performance intercept applications. Its operational complexity restricts use to research programs and select strategic missile defense platforms. The logistical burden of maintaining cryogenic propellants in field conditions makes broad military adoption structurally unlikely without major technology advancement.

Ramjet/Scramjet propulsion enables sustained high-speed flight across extended engagement ranges. Ramjet-powered missiles like METEOR achieve beyond-visual-range performance that conventional solid motors cannot match. This propulsion class is central to next-generation long-range SAM development programs focused on hypersonic threat interception — a segment receiving disproportionate R&D investment relative to its current market volume.

Guidance Analysis

Infrared (IR) Homing dominates with 41.4% due to passive targeting and electronic warfare resistance.

In 2025, Infrared (IR) Homing held a dominant market position in the By Guidance segment of the Surface to Air Missiles Market, with a 41.4% share. IR guidance requires no active radar emission from the launch platform, reducing the interceptor’s electronic signature. This passive engagement capability is particularly valued in contested electromagnetic environments where radar emissions invite counter-targeting responses.

Command-guided systems rely on ground-based radar to direct the interceptor throughout its flight path. This approach allows continuous trajectory adjustment but creates dependency on the radar’s continued operation. Command guidance remains prevalent in short-to-medium range applications where maintaining radar contact throughout engagement is operationally feasible.

Semi-Active Radar Homing uses ground radar to illuminate the target while the interceptor homes on reflected energy. This method offers precision at medium-to-long ranges and underpins several NATO-standard SAM platforms. However, radar illumination requirements constrain simultaneous engagement capacity — a limitation that drives investment in active radar homing alternatives.

Laser-guided SAM systems provide high terminal accuracy for point-defense applications. Their precision advantage is most relevant against slow, low-altitude targets including drones and helicopters. Laser guidance is primarily deployed in short-range configurations where atmospheric scattering does not significantly degrade beam coherence or tracking accuracy.

Speed Class Analysis

Subsonic dominates with 61.2% due to cost efficiency and broad threat coverage in existing inventories.

In 2025, Subsonic held a dominant market position in the By Speed Class segment of the Surface to Air Missiles Market, with a 61.2% share. Most fielded air defense systems worldwide use subsonic interceptors, reflecting decades of procurement and the continued relevance of subsonic threat categories. Cost per interceptor remains far lower than supersonic alternatives, enabling larger inventory stockpiles — a critical factor when engagement rates in active conflicts can exhaust reserves within days.

Supersonic interceptors extend engagement envelopes against fast-moving aircraft and cruise missiles. Their higher closing velocity improves intercept probability at distance, justifying their premium cost for medium-to-long range SAM platforms. Defense planners increasingly specify supersonic capability as the baseline for new procurement programs targeting multi-threat engagement scenarios.

Hypersonic interceptors represent the smallest current segment but carry the highest strategic priority. The S-500 Prometheus reportedly engages up to 10 hypersonic targets simultaneously at speeds around 7 km/s, with interceptor speeds up to Mach 20 and engagement ranges up to 600 km for ballistic targets. This performance specification sets the benchmark for the next generation of strategic missile defense investment.

Key Market Segments

By Range

- Very Short Range

- Short Range

- Medium Range

- Long Range

- Extended Range

By Launch Platform

- Man-Portable

- Mobile/Land Vehicle-Mounted

- Fixed-Site Ground Installations

- Naval-based

By Propulsion Type

- Solid

- Liquid

- Hybrid

- Cryogenic

- Ramjet/Scramjet

By Guidance

- Command-guided

- Semi-Active Radar Homing

- Infrared (IR) Homing

- Laser-guided

By Speed Class

- Subsonic

- Supersonic

- Hypersonic

Drivers

Documented Combat Performance and Expanding Defense Budgets Accelerate SAM Procurement Worldwide

Real-world interception data from Ukraine and the Middle East has removed the guesswork from SAM procurement decisions. In June 2025, Israel’s integrated air defense system achieved an 86% interception rate against Iranian ballistic missiles and a 99% rate against hundreds of Iranian drones, preventing an estimated USD 15 billion in potential property damage. These figures translate directly into budget justifications for allied governments reviewing their own air defense gaps.

Defense ministries are also responding to a broader threat environment where fighter jets, drones, and ballistic missiles operate simultaneously rather than sequentially. Multi-layered air defense architecture requires procurement across all range bands — from very short-range point defense to extended-range ballistic intercept. This architecture model multiplies procurement volume compared to single-system approaches used in prior decades.

In March 2026, India’s Defence Acquisition Council approved approximately USD 25 billion in defence procurement, including five additional S-400 surface-to-air missile systems for the Indian Air Force and approximately USD 258 million for Russian Shtil naval SAM systems. This single procurement decision illustrates how major military powers are committing to integrated, multi-platform air defense investments at a scale that sustains vendor production pipelines for years.

Restraints

Escalating Interceptor Costs and Arms Control Restrictions Create Structural Barriers to Market Expansion

The cost structure of advanced SAM systems creates a fundamental budget tension for most defense ministries. Arrow interceptors cost approximately USD 2–3 million each, THAAD interceptors approximately USD 13 million each, and around 200 ballistic missile interceptors were launched during the June 2025 Israel-Iran conflict alone — generating total interceptor expenditure exceeding USD 1 billion in a single engagement cycle. For most nations outside the wealthiest defense spenders, this burn rate is fiscally unsustainable at scale.

Cost asymmetry compounds the challenge. During 2024–2025 Iranian attack campaigns, Tamir interceptors costing USD 40,000–USD 50,000 each faced a 40–100:1 cost asymmetry against rockets costing only USD 500–USD 1,000. This arithmetic disadvantage raises legitimate questions about long-term sustainability for procurement planners and constrains how aggressively governments will stockpile interceptors.

Strict export regulations and international arms control agreements further limit market reach. Advanced SAM systems with ballistic missile defense capability are subject to Missile Technology Control Regime restrictions, limiting transfer to allied nations only under bilateral agreements. This regulatory layer extends qualification timelines, adds compliance costs, and eliminates potential buyer markets — particularly among emerging economies seeking modern air defense without pre-existing alliance frameworks.

Growth Factors

Mobile Platform Demand, Radar Integration, and Asia-Pacific Modernization Open Structural Growth Channels

Mobile SAM platform procurement is accelerating as militaries absorb Ukraine battlefield lessons. Fixed-site systems proved vulnerable to precision strikes, pushing defense planners to prioritize wheeled and tracked SAM configurations that can reposition after each engagement. This operational shift creates upgrade demand across existing inventories and new procurement cycles focused on vehicle-mounted systems across NATO and Indo-Pacific allies.

The Hensoldt TRML-4D radar integrated into IRIS-T fire units deployed in Ukraine delivers detection ranges of up to approximately 250 km, with each fire unit comprising three SLM and two SLS launchers. This radar-to-launcher integration architecture demonstrates that detection capability amplifies interceptor effectiveness — driving defense ministries to invest in radar upgrades alongside missile procurement rather than treating them as separate budget lines.

Asia-Pacific and Middle East modernization programs represent the clearest near-term revenue expansion channels. Both regions operate significant legacy air defense inventories requiring replacement, face documented aerial threat escalation, and hold defense budgets large enough to fund multi-system purchases. The convergence of replacement demand, threat urgency, and available funding in these two regions positions them as the primary growth markets through 2035.

Emerging Trends

AI-Driven Threat Assessment and Hypersonic Interception Investment Define the Next SAM Technology Cycle

Artificial intelligence integration into SAM command-and-control systems is shifting from experimental to operational. Iron Dome’s automated threat assessment system already prevents interceptors from engaging rockets headed toward unpopulated areas, achieving estimated ammunition savings of 40–60% versus unselective engagement protocols. This selective-intercept logic reduces cost per engagement and extends inventory life — two metrics that defense budget planners track directly.

By March 2026, the IDF’s air defense system operating with U.S. integration support achieved a reported 92% success rate against incoming threats. This performance improvement over earlier standalone figures demonstrates that AI-assisted multi-system coordination produces measurably better outcomes than individual platform operation. Allied defense planners now treat interoperability software as a procurement requirement rather than an optional upgrade.

Long-range hypersonic interception programs are attracting disproportionate R&D investment relative to their current deployment volumes. Development of multi-mission air defense platforms capable of engaging subsonic drones and hypersonic missiles from the same launch unit reduces the number of separate systems a military must procure and maintain. This platform consolidation trend reshapes vendor product roadmaps — rewarding developers who can deliver multi-threat coverage within a single integrated architecture.

Regional Analysis

North America Dominates the Surface to Air Missiles Market with a Market Share of 43.70%, Valued at USD 3.8 Billion

North America holds 43.70% of the global SAM market, valued at approximately USD 3.8 Billion. The United States drives this position through home-country advantage for leading SAM developers, sustained Pentagon procurement, and NATO-standard setting that shapes allied purchasing decisions globally. U.S. defense industrial capacity also enables faster production scaling than any other region when allied demand spikes.

Europe Surface to Air Missiles Market Trends

Europe’s SAM investment has accelerated sharply following Russia’s military operations in Ukraine. NATO members are actively procuring IRIS-T, Patriot, and SAMP/T systems to meet the alliance’s revised air defense density targets. European governments that previously deferred air defense modernization are now treating SAM procurement as politically non-negotiable, compressing procurement timelines significantly.

Asia Pacific Surface to Air Missiles Market Trends

Asia-Pacific represents the fastest-expanding regional procurement market. India’s Defence Acquisition Council approved approximately USD 25 billion in defence spending in March 2026, including S-400 additions and naval SAM systems. China, South Korea, Japan, and Australia are simultaneously upgrading air defense architectures in response to regional missile proliferation, creating parallel procurement cycles across multiple major buyers.

Middle East and Africa Surface to Air Missiles Market Trends

The Middle East’s SAM procurement is directly shaped by operational necessity. Israel’s multi-layered defense architecture — Iron Dome, David’s Sling, and Arrow — has demonstrated combat effectiveness against massed drone and ballistic missile attacks. Gulf states and regional powers are drawing the same architectural lessons, accelerating procurement of multi-tier SAM systems to address the drone and short-range missile threat environment.

Latin America Surface to Air Missiles Market Trends

Latin America represents a smaller but developing SAM market, primarily focused on modernizing legacy Soviet-era and early Western systems. Budget constraints limit large-platform procurement, positioning the region as a stronger market for short-to-medium range systems and technology transfer arrangements. Brazil and Mexico drive the bulk of regional defense procurement discussions.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Raytheon Technologies Corporation holds a commanding position in the global SAM market through the Patriot system — the most widely deployed advanced air defense platform in the Western alliance. The July 2024 USD 1.2 billion Patriot contract for Germany and the October 2024 USD 736 million AIM-9X award demonstrate active order flow across both platform and interceptor categories. Raytheon’s dual revenue stream from hardware and recurring interceptor replenishment provides structural earnings visibility.

Lockheed Martin Corporation anchors its SAM market position around the PAC-3 MSE interceptor, which the U.S. Army contracted in November 2024 to expand production capacity to approximately 650 interceptors per year. This production ramp positions Lockheed to capture the sustained replenishment demand generated by Patriot system deployments globally. The company’s integration of missile defense across land, sea, and space platforms creates cross-selling pathways that competitors with narrower portfolios cannot replicate.

MBDA leverages its multi-nation European ownership structure — spanning France, Germany, Italy, Spain, and the UK — to access procurement budgets across all major NATO-European defense ministries simultaneously. The IRIS-T SLM’s operational performance in Ukraine, including approximately 99% interception rates and over 240 confirmed kills, provides MBDA and its partners with live-combat validation that materially strengthens their competitive position in allied procurement competitions.

Northrop Grumman Corporation differentiates through advanced radar and battle management systems that integrate multiple SAM platforms into unified defense networks. NASAMS, co-developed with Kongsberg, achieves reaction times under 10 seconds with 72+ simultaneous tracks — performance metrics that address the high-volume simultaneous threat scenarios documented in recent conflicts. Northrop’s systems integration capability positions it as an architecture-layer player, not merely a missile manufacturer.

Key Players

- Raytheon Technologies Corporation

- Lockheed Martin Corporation

- MBDA

- Northrop Grumman Corporation

- BrahMos Aerospace

- Thales Group

- BAE Systems

- Rafael Advanced Defense Systems

- China Aerospace Science and Technology Corporation

- Kongsberg Defence Aerospace

- Bharat Dynamics Limited

- Rosoboronexport

Recent Developments

- July 2024 — RTX’s Raytheon business received a USD 1.2 billion contract from the U.S. government to supply additional Patriot air and missile defense systems to Germany, covering Configuration 3+ radars, launchers, and command-and-control stations. This award reflects Germany’s accelerated air defense investment following NATO’s revised capability targets post-Ukraine.

- October 2024 — RTX’s Raytheon business was awarded a USD 736 million contract to produce AIM-9X Sidewinder Block II missiles for the U.S. Navy and allied customers. The award included hardware upgrades to the fuze and ignition safety device, extending the missile’s operational relevance across multiple platform types.

- November 2024 — The U.S. Army awarded Lockheed Martin a contract to expand PAC-3 MSE missile production capacity, targeting output of approximately 650 interceptors per year. This production increase directly addresses global allied demand for Patriot-compatible interceptors generated by active conflict resupply requirements.

- 2024 — RTX reported an additional USD 1.2 billion order for Patriot fire units and associated missiles under allied air defense strengthening programs. This order added to an already substantial installed base, reinforcing Raytheon’s long-term servicing and replenishment revenue pipeline across multiple customer nations.

- 2024 — Lockheed Martin’s Missile and Fire Control business announced new orders and production ramp-up for PAC-3 and related air defense interceptors. The ramp reflected increased allied government commitments to expanding interceptor stockpiles beyond traditional peacetime inventory levels.

- March 2026 — India’s Defence Acquisition Council approved approximately ₹2.38 lakh crore (~USD 25 billion) in defence procurement, including five additional S-400 surface-to-air missile systems for the Indian Air Force and approximately ₹2,182 crore (~USD 258 million) for Russian Shtil naval SAM systems with a ~45 km range for the Indian Navy.

Report Scope

Report Features Description Market Value (2025) USD 8.8 Billion Forecast Revenue (2035) USD 15.1 Billion CAGR (2026-2035) 5.5% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Range (Very Short Range, Short Range, Medium Range, Long Range, Extended Range), By Launch Platform (Man-Portable, Mobile/Land Vehicle-Mounted, Fixed-Site Ground Installations, Naval-based), By Propulsion Type (Solid, Liquid, Hybrid, Cryogenic, Ramjet/Scramjet), By Guidance (Command-guided, Semi-Active Radar Homing, Infrared (IR) Homing, Laser-guided), By Speed Class (Subsonic, Supersonic, Hypersonic) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Raytheon Technologies Corporation, Lockheed Martin Corporation, MBDA, Northrop Grumman Corporation, BrahMos Aerospace, Thales Group, BAE Systems, Rafael Advanced Defense Systems, China Aerospace Science and Technology Corporation, Kongsberg Defence Aerospace, Bharat Dynamics Limited, Rosoboronexport Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Surface to Air Missiles MarketPublished date: Apr 2026add_shopping_cartBuy Now get_appDownload Sample

Surface to Air Missiles MarketPublished date: Apr 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Raytheon Technologies Corporation

- Lockheed Martin Corporation

- MBDA

- Northrop Grumman Corporation

- BrahMos Aerospace

- Thales Group

- BAE Systems

- Rafael Advanced Defense Systems

- China Aerospace Science and Technology Corporation

- Kongsberg Defence Aerospace

- Bharat Dynamics Limited

- Rosoboronexport

Our Clients

- 183780

- Apr 2026