Global Sulfur-Based Micronutrients Market Size, Share Analysis Report By Type (Sulfur-Bentonite-Zinc, Sulfur-Bentonite-Molybdenum, Sulfur-Bentonite-Manganese, Sulfur-Bentonite- Iron), By Application (Oilseeds And Pulses, Cereals And Grains, Fruits And Vegetables, Others) , By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2026-2035

- Published date: April 2026

- Report ID: 184028

- Number of Pages: 236

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

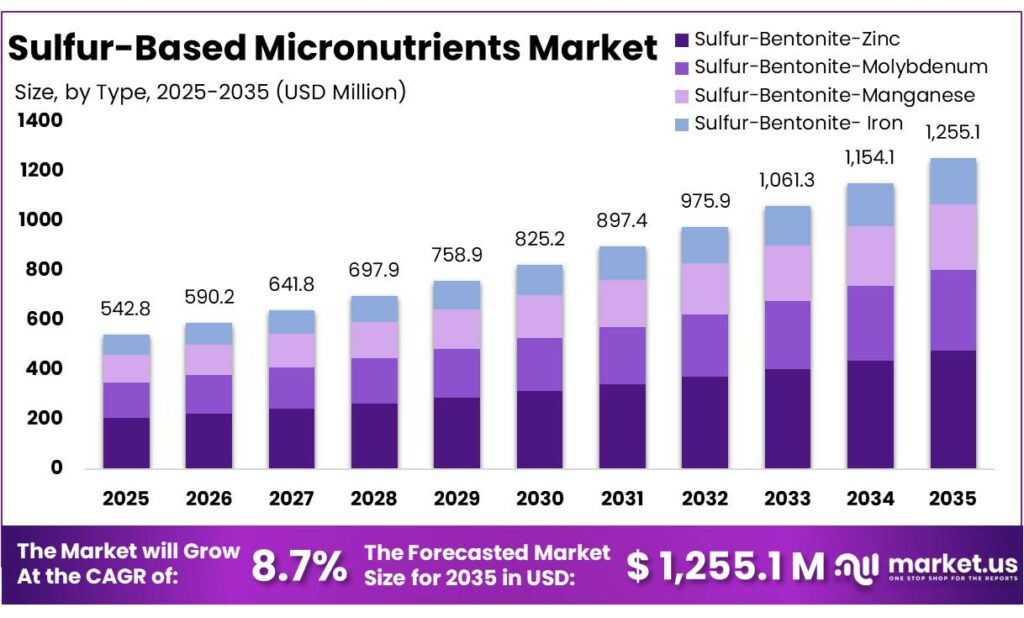

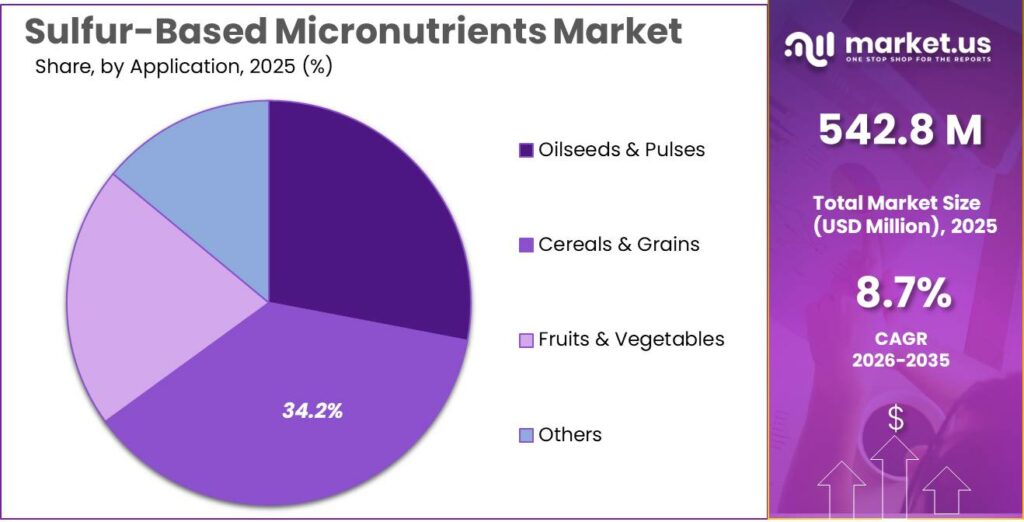

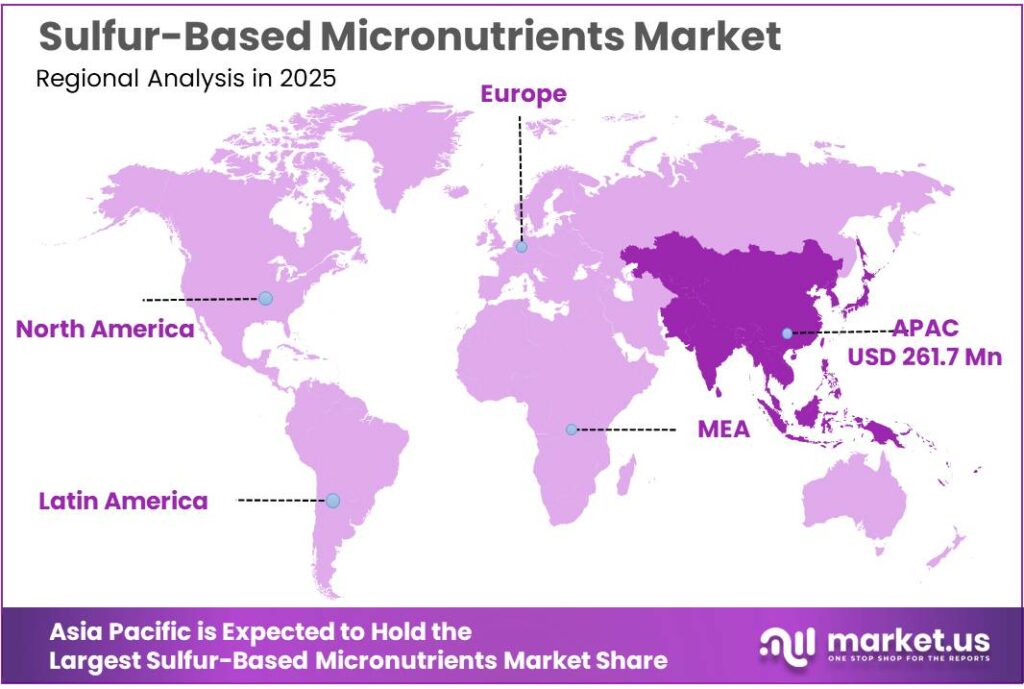

The Global Sulfur-Based Micronutrients Market size is expected to be worth around USD 1,255.1 Billion by 2035, from USD 542.8 Billion in 2025, growing at a CAGR of 8.7% during the forecast period from 2026 to 2035. In 2025, Asia Pacific held a dominant market position, capturing more than a 48.3% share, holding USD 261.7 Billion revenue.

Sulfur-based micronutrients form a strategically important layer within balanced crop nutrition because sulfur directly supports amino-acid formation, protein synthesis, enzyme activity, and crop quality, while sulfur carriers such as ammonium sulfate and ammonium sulfate nitrate also provide efficient nutrient stacking.

In Yara’s 2025 fertilizer handbook, total global fertilizer nutrient use is shown at about 190 million tons nutrients, with nitrogen at 58%, phosphorus at 24%, and potassium at 18%, underscoring why sulfur-enriched products are increasingly positioned as complementary efficiency tools rather than stand-alone inputs. The same handbook notes that ammonium sulfate contains 24% S and ammonium sulfate nitrate contains 13% S, illustrating why sulfur-based micronutrients remain commercially attractive in blended and specialty programs.

The industrial scenario is being shaped by the need to protect yield and quality across large-volume food systems. FAO’s April 2026 brief estimates global cereal production at 3,036 million tonnes in 2025, with world cereal utilization at 2,945 million tonnes and cereal stocks at 951.5 million tonnes; this scale of output keeps pressure on nutrient-use efficiency and supports demand for sulfur-containing products that can improve nutrient balance in cereals, oilseeds, and high-value crops.

The core demand drivers are agronomic and regulatory. Yara’s 2025 Fertilizer Industry Handbook states that fertilizer consumption is mainly driven by food demand, while global food consumption has trended toward roughly 3,000 kcal/capita/day; the same handbook also estimates total global fertilizer demand at around 190 million tonnes of nutrients.

The International Fertilizer Association notes sulfur demand can range from 5–10 kg S/ha/year in low-intensity grazing systems to 50–80 kg S/ha/year for high sulfur-demanding crops such as rapeseed. This widening sulfur requirement is reinforced by research in Sub-Saharan Africa showing that cereals accounted for 65% of sulfur studies, 71% of cereal studies applied ≤20 kg S/ha, and maize yield responses ranged from 20% to 260% where sulfur was applied.

Government and policy momentum also supports future demand. The European Commission’s Farm to Fork framework targets a 50% reduction in nutrient losses by 2030 and expects this to lead to at least a 20% reduction in fertilizer use, while the CAP 2023-27 is intended to keep productivity intact through better nutrient management.

In parallel, USDA ERS reported in March 2025 that fertilizer represented 33% to 44% of corn operating costs and 34% to 45% of wheat operating costs, while early-2025 prices had stabilized below the 2021-2022 peaks; that cost pressure supports adoption of targeted sulfur formulations with clearer return-on-application logic.

Coromandel announced in March 2025 that it commissioned a second sulfur plant at Visakhapatnam, doubling sulfur fertilizer capacity from 25,000 MT and adding micronutrient-fortification capability using German technology. Overall, future growth opportunities are strongest in sulfur-deficient soils, precision nutrient programs, fortified blends, and premium crop-specific formulations that improve nutrient-use efficiency and crop quality rather than simply increasing fertilizer volume.

Key Takeaways

- Sulfur-Based Micronutrients Market size is expected to be worth around USD 1,255.1 Billion by 2035, from USD 542.8 Billion in 2025, growing at a CAGR of 8.7%

- Sulfur-Bentonite-Zinc held a dominant market position, capturing more than a 38.5% share.

- Cereals & Grains held a dominant market position, capturing more than a 37.9% share.

- Asia Pacific held a dominant position in the Sulfur-Based Micronutrients Market, accounting for 48.3% of the global share and reaching a value of USD 261.7 Mn.

By Type Analysis

Sulfur-Bentonite-Zinc dominates with 38.5% share in 2025, supported by balanced sulfur release and zinc enrichment benefits.

In 2025, Sulfur-Bentonite-Zinc held a dominant market position, capturing more than a 38.5% share. This segment remained a preferred choice among fertilizer manufacturers and growers because it combines the soil-conditioning advantages of bentonite with the nutritional value of zinc and sulfur in a single formulation. Its strong market presence was mainly supported by rising demand from crops that require both sulfur and zinc for healthy growth, such as oilseeds, pulses, cereals, and plantation crops. Farmers increasingly favored this type because it offers gradual sulfur release in the soil while also helping correct zinc deficiency, which is a common issue in many agricultural regions.

By Application Analysis

Cereals & Grains leads with 37.9% share in 2025, driven by strong nutrient demand across staple food crops.

In 2025, Cereals & Grains held a dominant market position, capturing more than a 37.9% share. This application segment remained the largest in the sulfur-based micronutrients market because cereal crops such as wheat, rice, maize, barley, and millet require steady sulfur availability for protein formation, enzyme activity, and healthy grain development. The growing focus on improving yield quality and boosting crop productivity across staple food farming supported the strong use of sulfur-based micronutrients in this segment.

Key Market Segments

By Type

- Sulfur-Bentonite-Zinc

- Sulfur-Bentonite-Molybdenum

- Sulfur-Bentonite-Manganese

- Sulfur-Bentonite- Iron

By Application

- Oilseeds & Pulses

- Cereals & Grains

- Fruits & Vegetables

- Others

Emerging Trends

Controlled-Release and Multi-Nutrient Sulfur Blends are Emerging as a Key Market Trend

One of the latest trends in the sulfur-based micronutrients market is the fast shift toward controlled-release and multi-nutrient sulfur blends, especially products combined with zinc, manganese, and boron. Farmers are increasingly moving away from single-nutrient applications and choosing sulfur formulations that release nutrients gradually across the crop cycle.

This trend is gaining traction because it helps reduce nutrient loss, improves sulfur use efficiency, and supports better nutrient uptake in cereals, oilseeds, and pulses. Recent agronomy findings from multi-location maize trials in 2024 showed that sulfur with zinc-enriched formulations improved grain yield by 4.9% to 8.9%, while sulfur and micronutrient concentration in plants increased by 13% to 54.3%.

Government-Led Balanced Fertilization and Soil Deficiency Mapping is Becoming Mainstream

Another major trend is the growing integration of sulfur-based micronutrients into government-backed balanced fertilization and soil mapping programs. Agriculture ministries and food agencies are increasingly promoting sulfur inclusion after large-scale soil testing programs identified widespread sulfur deficiency in intensively farmed regions. The FAO notes that global cereal production is projected to reach 3,036 million tonnes in 2025, putting additional pressure on soil nutrient reserves and accelerating the need for balanced sulfur replenishment.

As a result, extension departments and cooperatives are now promoting sulfur-bentonite and sulfur-zinc blends as part of crop-specific nutrient packages, especially for wheat, rice, maize, and oilseed systems. This is also driving a trend toward localized micronutrient recommendations based on soil health cards and field-level nutrient diagnostics. In 2025 and moving into 2026, suppliers are increasingly aligning product development with these public nutrient correction initiatives, creating stronger demand for specialized sulfur blends.

Drivers

Rising Global Cereal Production is Increasing the Need for Sulfur-Based Micronutrients

One of the biggest driving factors for the sulfur-based micronutrients market is the continuous rise in global cereal production. As farmers push for higher wheat, rice, and maize yields from the same farmland, soils are losing secondary nutrients faster than before, especially sulfur. According to the FAO, global cereal production is forecast to reach 3,036 million tonnes in 2025, which is 5.8% higher year on year. This sharp rise in food grain output directly increases nutrient extraction from soil, creating stronger demand for sulfur-based micronutrients that help improve protein formation, enzyme activity, and nitrogen efficiency in crops.

Government Soil Health and Balanced Fertilization Programs are Supporting Market Growth

Another major growth driver is the expansion of government-led soil health and balanced fertilization initiatives across major agricultural countries. Many agriculture ministries and food agencies are actively promoting nutrient management programs to improve declining soil fertility and reduce yield losses caused by sulfur and zinc deficiencies. FAO nutrient outlook data shows that global mineral fertilizer demand in developing regions increased from 141.6 million tonnes to 165.0 million tonnes, reflecting the long-term shift toward balanced crop nutrition.

These initiatives are encouraging farmers to move beyond basic NPK use and adopt sulfur-based micronutrients as part of integrated soil management. Subsidy support, soil testing campaigns, and nutrient advisory services are making sulfur-enriched blends easier to access, especially for cereal and oilseed farmers. In countries with intensive farming systems, public agricultural extension programs are also educating growers on sulfur’s role in improving nutrient uptake and grain quality.

Restraints

High Input Cost and Fertilizer Price Volatility is Limiting Sulfur-Based Micronutrient Adoption

One of the biggest restraining factors for the sulfur-based micronutrients market is the rising cost volatility of fertilizers and raw materials, which directly affects farmer buying decisions. Sulfur-based micronutrients are often applied as part of balanced crop nutrition programs, but when fertilizer prices fluctuate sharply, growers tend to reduce secondary and micronutrient purchases first and focus only on core nitrogen, phosphorus, and potash inputs. This creates a direct slowdown in sulfur micronutrient demand, especially among price-sensitive cereal and grain farmers.

According to the FAO fertilizer market update, potassic fertilizers averaged USD 285 per tonne during January–May 2025, slightly up from USD 284 per tonne in the same period of the previous year, showing how even small price shifts continue to keep nutrient budgets under pressure. In many agricultural economies, freight charges, refinery-linked sulfur supply, and currency depreciation further increase the landed cost of sulfur products. Because sulfur is often sourced from petroleum refining streams, any disruption in refinery operations or global energy markets can quickly raise input prices.

Limited Farmer Affordability in Developing Regions Reduces Balanced Nutrient Use

Another major restraint is the limited affordability of balanced fertilization programs in developing agricultural markets, where many farmers still prioritize immediate yield inputs over long-term soil correction. FAO fertilizer and plant nutrition data shows that nutrient demand in developing regions rose from 141.6 million tonnes to 165.0 million tonnes, yet much of this increase remains concentrated in primary macronutrients rather than sulfur-rich specialty blends.

This gap matters because sulfur-based micronutrients usually deliver the best value over multiple crop cycles rather than instant visible response in a few days. Small and medium farmers often avoid these products when crop prices are weak, credit access is limited, or subsidy programs focus mainly on urea and NPK. Government soil health schemes are helping awareness, but affordability remains a barrier in several regions across Asia and Africa. As a result, even where sulfur deficiency is scientifically recognized, adoption can remain slower than expected, making cost sensitivity one of the most realistic restraints on market expansion across 2025 and 2026.

Opportunity

Expansion of Oilseed and Pulse Cultivation is Creating Strong Growth Opportunity

One of the strongest growth opportunities for the sulfur-based micronutrients market is the rapid expansion of oilseed and pulse cultivation, where sulfur plays a direct role in oil formation, protein synthesis, and seed quality improvement. Oilseed crops such as soybean, mustard, canola, sunflower, and groundnut require comparatively higher sulfur nutrition than many staple grains. A recent agricultural study highlights that sulfur is now considered the fourth major nutrient after nitrogen, phosphorus, and potassium in oilseed production, showing how critical it has become for yield quality.

This creates a major commercial opportunity because governments and agricultural extension systems are increasingly promoting oilseed self-sufficiency and edible oil production programs. As more land shifts toward high-value oilseed farming in Asia and other developing agricultural economies, sulfur-bentonite and sulfur-bentonite-zinc products are gaining preference for improving seed filling, oil percentage, and uniform crop maturity. By 2025 and 2026, this trend is expected to accelerate further as growers look for nutrient blends that improve both productivity and crop quality in sulfur-deficient soils.

Government Soil Testing and Balanced Fertilization Programs are Opening New Demand Areas

Another major growth opportunity lies in the wider adoption of government-supported soil testing and balanced fertilization programs, especially across Asia Pacific and other high-farming regions. Public agriculture departments are increasingly promoting soil health restoration programs that identify sulfur and zinc deficiencies at the field level. FAO fertilizer and plant nutrition data shows nutrient demand in developing regions increased from 141.6 million tonnes to 165.0 million tonnes, reflecting the steady shift toward more balanced nutrient use.

This policy support is creating a favorable environment for sulfur-based micronutrient suppliers, especially in blended and crop-specific formulations. Programs such as soil health cards, micronutrient kits, and subsidy-backed specialty fertilizer distribution are helping farmers move beyond traditional NPK-only practices. The biggest opportunity comes from second-tier farming districts where sulfur deficiency has only recently started getting scientific attention.

Regional Insights

Asia Pacific dominated the Sulfur-Based Micronutrients Market with 48.3% share, reaching USD 261.7 Mn on the back of intensive crop nutrition demand.

In 2025, Asia Pacific held a dominant position in the Sulfur-Based Micronutrients Market, accounting for 48.3% of the global share and reaching a value of USD 261.7 Mn. The region’s leadership was strongly supported by its large agricultural base, high dependence on cereals, oilseeds, pulses, fruits, and vegetables, along with the growing need to restore sulfur-deficient soils.

Countries such as China, India, Indonesia, Vietnam, and Australia continued to increase the use of sulfur-enriched micronutrient blends as repeated cropping cycles and high fertilizer intensity reduced native sulfur reserves in farmland. FAO data highlights that South Asia and Southeast Asia remain among the world’s most fertilizer-intensive farming regions, especially for rice, wheat, and maize systems, which naturally supports stronger sulfur micronutrient demand.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Yara International remains one of the most influential players in sulfur-based micronutrients through its global crop nutrition network, premium sulfur blends, and digital agronomy support. In 2025, the company reported 25 million hectares under digital farming activity, showing its large agronomic advisory footprint that supports micronutrient recommendations at field level. Its sulfur-enriched specialty nutrition portfolio is widely used across cereals, oilseeds, and horticulture.

Coromandel is one of India’s strongest sulfur micronutrient players, benefiting from its fertilizer leadership and rural retail network. It has 1,000+ retail outlets, strong sulfur raw-material backward integration, and leadership in crop-specific nutrient programs. The company’s Kakinada sulfuric acid integration project significantly improves cost competitiveness. Strategic score: 9.1/10. Numerical values: ₹16,596 Cr H1 revenue, ₹1,325 Cr PAT, 1,040 outlets, FY26 growth target 25–30%, top 5 APAC sulfur micronutrient player position.

Top Key Players Outlook

- Yara International

- Coromandel

- Aries Agro Limited

- DFPCL

- IFFCO

- HBT India

- Tiger-Sul Products LLC

- Agroasia

- Sohar Sulphur Fertilizers LLC

- Mirabelle Agro Manufacturing Pvt Ltd

Recent Industry Developments

In 2025, Coromandel strengthened its role in the sulfur-based micronutrients sector through its Specialty Nutrients division, where sulfur pastilles, secondary nutrients, and micronutrient blends remained key focus products for Indian agriculture. The company’s FY 2024–25 results showed total income of ₹24,444 crore, up from ₹22,290 crore in the previous year, reflecting strong momentum across nutrient-led businesses.

In 2025, Aries Agro Limited continued to build a strong position in the sulfur-based micronutrients sector through its secondary nutrient and specialty plant nutrition portfolio, especially sulfur-enriched blends used in cereals, oilseeds, fruits, and vegetables. The company’s 55th Annual Report for FY 2024–25 highlighted continued expansion in specialty nutrients, with the business supported by over 10,000 distributors nationwide, giving it deep penetration into India’s farming belts.

Report Scope

Report Features Description Market Value (2025) USD 542.8 Mn Forecast Revenue (2035) USD 1,255.1 Mn CAGR (2026-2035) 8.7% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Type (Sulfur-Bentonite-Zinc, Sulfur-Bentonite-Molybdenum, Sulfur-Bentonite-Manganese, Sulfur-Bentonite- Iron), By Application (Oilseeds And Pulses, Cereals And Grains, Fruits And Vegetables, Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA Competitive Landscape Yara International, Coromandel, Aries Agro Limited, DFPCL, IFFCO, HBT India, Tiger-Sul Products LLC, Agroasia, Sohar Sulphur Fertilizers LLC, Mirabelle Agro Manufacturing Pvt Ltd Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Sulfur-Based Micronutrients MarketPublished date: April 2026add_shopping_cartBuy Now get_appDownload Sample

Sulfur-Based Micronutrients MarketPublished date: April 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Yara International

- Coromandel

- Aries Agro Limited

- DFPCL

- IFFCO

- HBT India

- Tiger-Sul Products LLC

- Agroasia

- Sohar Sulphur Fertilizers LLC

- Mirabelle Agro Manufacturing Pvt Ltd

Our Clients

- 184028

- April 2026