Global Sugarcane Harvesters Market Size, Share Analysis Report By Type (Whole-Stalk Harvesters, Chopper/Billet Harvesters), By Drive Mode (Self-Propelled, Tractor-Mounted/Towed), By Row-Capacity (Single-Row, Multi-Row) , By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2026-2035

- Published date: April 2026

- Report ID: 183699

- Number of Pages: 345

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

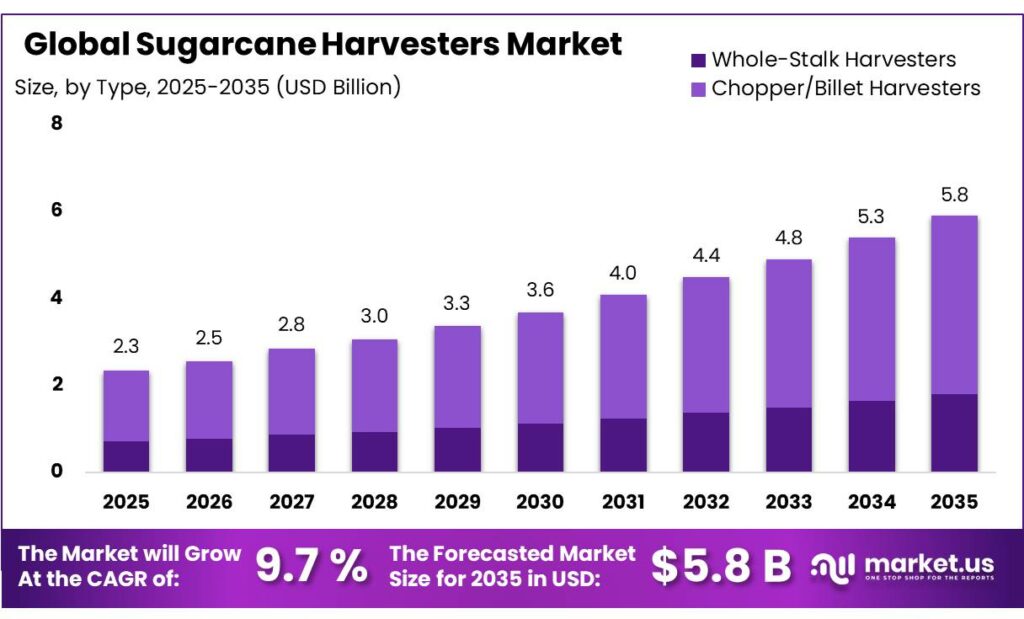

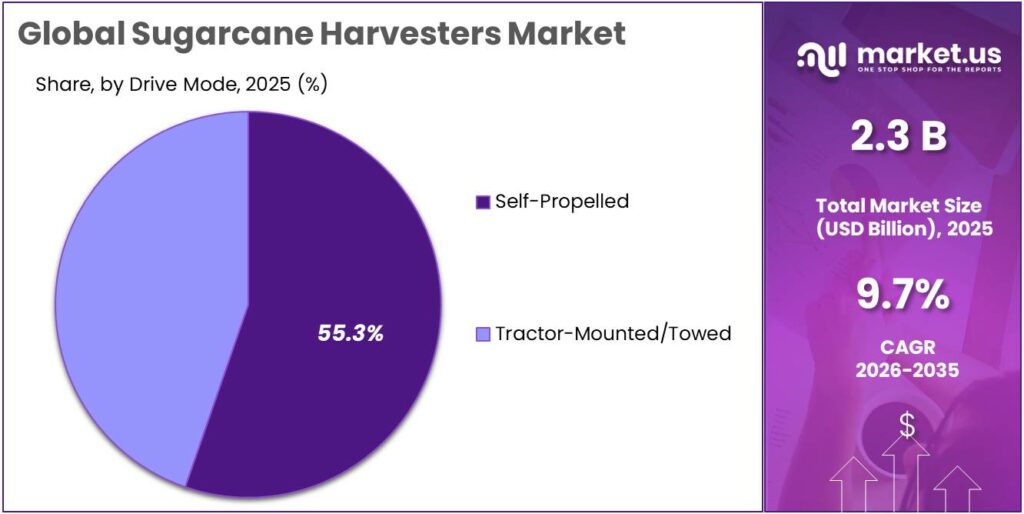

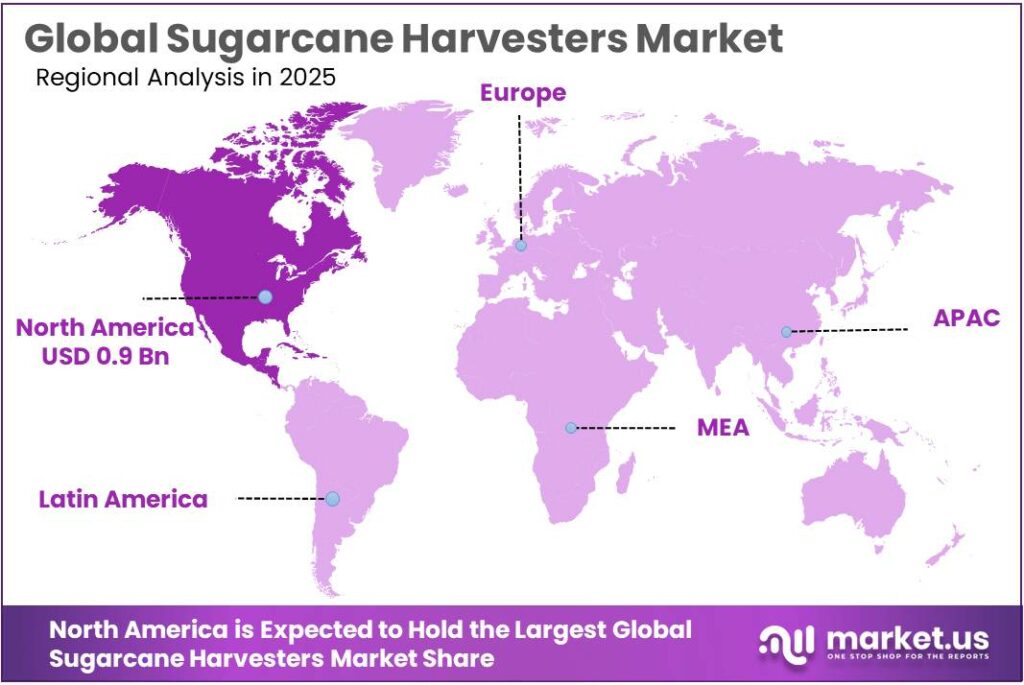

The Global Sugarcane Harvesters Market size is expected to be worth around USD 5.8 Billion by 2035, from USD 2.3 Billion in 2025, growing at a CAGR of 9.7% during the forecast period from 2026 to 2035. In 2025, Latin America held a dominant market position, capturing more than a 41.9% share, holding USD 0.9 Billion revenue.

The sugarcane harvester industry is positioned within a large and strategically important global cane economy, where harvesting efficiency directly influences sugar recovery, logistics cost, and mill throughput. FAO reported that global sugar-crop output reached 2.2 billion tonnes in 2024, while FAO’s forecast for world sugar production in 2024/25 stood at 175.6 million tonnes. This scale keeps mechanized harvesting relevant in major cane-producing regions because harvest windows are tight and mills require predictable raw-material flow.

From an industrial scenario perspective, demand is strongest in large plantation systems and mill-linked cane belts where throughput, field cleanliness, and labor productivity matter more than simple machine ownership. Brazil remains the most influential operating environment. USDA FAS projected Brazil’s 2025/26 sugarcane harvest at 660 million metric tons, with agricultural yield at 79.2 tons per hectare, while the sugar-ethanol mix was expected to favor sugar at 51% versus 49% for ethanol. Such volumes support continued replacement demand for high-capacity harvesters, precision cleaning systems, and fleet-management tools.

USDA forecast Thailand’s sugarcane production at 96 million metric tonnes in MY 2025/26, up about 1% from MY 2024/25, while sugar output was projected at 10.3 million metric tonnes, up 2%. In Australia, USDA forecast raw sugar exports to rise to 3.1 million metric tonnes in MY 2025/26 from 2.7 million metric tonnes a year earlier. Meanwhile, the Australian government notes that about 95% of the country’s sugar is grown in Queensland and around 85% of Queensland raw sugar is exported, which supports continued investment in harvesting timeliness, contractor productivity, and field-to-mill coordination.

The main demand drivers are therefore clear: large crop volumes, export orientation, tighter labor availability, pressure to lower cost per tonne, and the need for cleaner cane and lower field losses. Government and quasi-government initiatives strengthen this case. In Brazil, RenovaBio’s 2025 target was set at 49.4 million CBIOs, and 331 plants were under certification to issue CBIOs, representing 75% of Brazilian biofuel producers; this supports the broader sugarcane bioenergy ecosystem that indirectly sustains mechanized harvesting investment.

AGCO, meanwhile, announced in February 2025 an expansion in Jundiaí, São Paulo, with remanufactured mechanical transmission production starting in April 2025 and reman CVT production beginning by the end of 2025; AGCO said reman transmissions can come at an average 30% lower cost to farmers. Together, these developments suggest that the industry’s next phase will be defined by localized engineering, lower lifecycle cost, and more service-led value capture.

Key Takeaways

- Sugarcane Harvesters Market size is expected to be worth around USD 5.8 Billion by 2035, from USD 2.3 Billion in 2025, growing at a CAGR of 9.7%.

- Chopper/Billet Harvesters held a dominant market position, capturing more than a 71.7% share.

- Self-Propelled held a dominant market position, capturing more than a 76.3% share.

- Multi-Row held a dominant market position, capturing more than a 68.2% share.

- Latin America held the dominant position in the Sugarcane Harvesters market, accounting for 41.9% share, valued at USD 0.9 Bn.

By Type Analysis

Chopper/Billet Harvesters dominate with 71.7% share due to faster harvesting and better cane quality handling

In 2025, Chopper/Billet Harvesters held a dominant market position, capturing more than a 71.7% share. This leading position reflects their strong adoption across large sugarcane-producing regions where speed, consistency, and lower field losses are major priorities. These machines are widely preferred because they cut sugarcane into small billets during harvesting, making transport and mill feeding easier and more efficient. Their ability to deliver cleaner cane with less extraneous matter also supports better sugar recovery, which is an important factor for mill operators and commercial growers.

By Drive Mode Analysis

Self-Propelled harvesters lead with 76.3% share thanks to high efficiency and better field mobility

In 2025, Self-Propelled held a dominant market position, capturing more than a 76.3% share. This segment remained the preferred choice in commercial sugarcane harvesting because it offers strong operational efficiency, faster field coverage, and better movement across large plantation areas. Self-propelled machines are designed as complete harvesting units, allowing operators to cut, clean, and process cane in a single pass, which helps save time during peak harvest seasons. Their independent movement and built-in power systems also make them suitable for continuous harvesting across long working hours.

By Row-Capacity Analysis

Multi-Row harvesters dominate with 68.2% share as growers focus on covering more acreage in less time

In 2025, Multi-Row held a dominant market position, capturing more than a 68.2% share. This segment led the market because it is highly effective for large sugarcane farms that need faster harvesting across wide field areas. Multi-row machines are built to harvest more than one row in a single pass, which significantly improves field productivity and helps reduce the total time required during the harvesting season. This makes them especially valuable in regions where crop maturity windows are short and mills require a steady supply of cane.

Key Market Segments

By Type

- Whole-Stalk Harvesters

- Chopper/Billet Harvesters

By Drive Mode

- Self-Propelled

- Tractor-Mounted/Towed

By Row-Capacity

- Single-Row

- Multi-Row

Emerging Trends

Precision farming and telematics integration is the latest major trend in sugarcane harvesters

One of the most important latest trends in sugarcane harvesters is the shift toward precision farming, telematics, and real-time machine monitoring. In 2025, growers are no longer looking at harvesters as only cutting machines; they increasingly want connected systems that can improve route planning, reduce downtime, and track field productivity in real time.

This trend is becoming highly relevant in large sugarcane plantations where every hour of harvesting affects cane freshness and mill recovery. A trusted 2025 industry update highlights that digital harvesting platforms helped improve field efficiency by 8 hectares per day while reducing unscheduled maintenance events by 4 times per month in large fleet operations.

OEMs are expanding autonomous and mixed-fleet smart farming platforms in 2025

A second major trend is the growing move toward autonomous upgrades and mixed-fleet digital platforms from leading machinery manufacturers. In 2025, AGCO expanded this trend through its PTx precision agriculture ecosystem, introducing smarter retrofit and autonomy-ready solutions that can work across different machine brands, not just new factory equipment.

The company’s 2025 technology showcase highlighted autonomous field solutions and digital fleet tools designed to improve machine productivity and labor efficiency.

Drivers

Labor shortage is a major growth driver for sugarcane harvesters, pushing faster farm mechanization

In 2025, one of the strongest driving factors for sugarcane harvesters is the growing shortage of farm labor during the peak cutting season. Sugarcane is a time-sensitive crop, and delayed harvesting directly affects sugar recovery and cane quality. Because of this, growers are steadily shifting toward mechanized harvesting systems that can work longer hours with consistent output.

The need is becoming more urgent as global sugar output continues to expand. FAO estimated global sugar production at 185.3 million tonnes in 2025/26, up 5.5% from the previous season, which means more cane needs to be harvested within fixed seasonal windows.

Government mechanization support and rising sugar output are strengthening future demand

A second major growth factor is the support coming from government-led mechanization and sugar diversification programs. Public initiatives linked to farm modernization, biofuel expansion, and higher cane productivity are indirectly increasing the use of sugarcane harvesters.

For example, official sugar policy support for the broader sugar sector continues to focus on operational efficiency and cane supply stability, while long-term production outlooks remain strong. OECD-FAO projects that global sugar production will rise further to nearly 205 million tonnes by 2034, showing sustained demand for efficient harvesting systems over the next decade.

Restraints

High machine cost remains the biggest restraint for wider sugarcane harvester adoption

One of the biggest restraining factors in the sugarcane harvesters market is the high upfront cost of machines, which makes adoption difficult for many growers and harvesting contractors. Sugarcane harvesters require a major capital investment, and this becomes a real challenge in regions where farm holdings are fragmented or seasonal harvesting volumes are limited. A trusted 2025-26 government sugarcane policy report clearly states that the “major obstacles to mechanization in sugarcane are high cost of machinery and implements, particularly sugarcane planter and harvester.”

Small farm structure and cost recovery concerns limit return on investment

A second layer of this restraint comes from the difficulty of recovering machine costs in smaller farming setups. Government-backed assessments for the 2025-26 sugar season highlight that along with machinery cost, small farm size is another major obstacle to mechanized harvesting adoption. When harvested acreage is limited, the machine cannot be utilized enough days in a season to justify ownership, which pushes up the cost per tonne harvested. At the same time, the all-India A2+FL cost of production for sugarcane is projected at 189 per quintal in 2025-26, showing that growers are already operating under rising input and labor expenses.

Opportunity

Biofuel expansion is creating the biggest growth opportunity for sugarcane harvesters

One of the strongest growth opportunities for sugarcane harvesters is the rapid expansion of sugarcane-based biofuel production, especially ethanol. As governments continue to raise blending targets and support cleaner transport fuels, sugarcane growers are under increasing pressure to supply larger volumes of cane within shorter harvest windows. This directly improves the long-term demand outlook for harvesting machinery.

- According to the OECD-FAO Agricultural Outlook 2025–2034, global biofuel demand is projected to grow by 0.9% per year, mainly supported by rising transport fuel demand and favorable domestic policies.

The same outlook notes that Brazil and other middle-income countries will remain key growth engines for ethanol consumption, which keeps sugarcane harvesting capacity strategically important. For harvester manufacturers and fleet contractors, this creates a clear opportunity in larger machine fleets, faster replacement cycles, and higher-capacity field systems. In simple terms, as more cane moves toward fuel use, the need for timely and cleaner harvesting becomes even more valuable, opening a long runway for mechanized harvesting growth.

Government blending targets and long-term ethanol capacity support future equipment demand

A second major opportunity comes from government-backed ethanol blending initiatives, which are encouraging long-term investment across the sugarcane value chain. The OECD-FAO biofuels outlook highlights that ethanol production is expected to reach 15 billion liters by 2034, supported by policies aimed at higher fuel blending levels.

Such policy-driven growth strengthens sugar mill economics, encourages higher cane acreage in efficient regions, and increases the need for harvesters that can operate with speed and precision. In Brazil, the government’s move in 2025 to raise the mandatory gasoline ethanol blend from 27% to 30% is expected to require well over 1 billion additional liters of ethanol per year, according to Reuters coverage of the official measure.

Regional Insights

Latin America dominates with 41.9% share, valued at USD 0.9 Bn, driven by Brazil’s large-scale mechanized cane ecosystem

Latin America held the dominant position in the Sugarcane Harvesters market, accounting for 41.9% share, valued at USD 0.9 Bn, supported by the region’s deep integration of large-scale sugarcane farming, ethanol production, and highly mechanized harvesting practices.

The region’s leadership is primarily anchored in Brazil, which remains the world’s largest sugarcane producer and one of the most advanced markets for mechanized cane harvesting. The industrial structure across Latin America favors high-capacity harvesting fleets because plantations are large, mill-linked, and focused on reducing field losses while maintaining cane quality during transport and crushing cycles.

The regional advantage is strongly supported by trusted food and agriculture data. According to the OECD-FAO Agricultural Outlook 2025–2034, global sugarcane production is expected to reach 2,100 million tonnes by 2034, with Brazil alone contributing an additional 112 million tonnes over the outlook period, the highest increase globally.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Deere & Company remains one of the most established names in sugarcane harvesting, supported by its strong presence in Latin American commercial cane operations. Its CH-series machines are widely used in large plantations because of high daily throughput and strong precision farming compatibility. The company’s harvester platforms are known for 13.6 L engine capacity, support for 1.7–1.9 meter row spacing, and enhanced drivetrain durability, which improves machine life in heavy harvesting cycles. Its scale, technology integration, and strong dealer support continue to make it a benchmark player in high-capacity harvesting systems.

Samart Kasetyon Co., Ltd. has built a strong niche in Southeast Asia with field-friendly harvesters designed for small and medium sugarcane farms. Its SM-200C model delivers 80–100 tons per day with a 200 horsepower 6-piston engine, while the newer SM-200 Predator raises capacity to 80–180 tons per day. The company’s strength comes from transport-friendly designs, easy maintenance, and better suitability for uneven terrain, making it highly practical in regional cane markets where field conditions vary significantly.

TAGRM Co. Ltd. focuses on compact and mid-sized sugarcane harvesting solutions, particularly for diverse field conditions. Its SH15 sugarcane harvester uses 52 kW power, offers 0.12–0.20 hectares per hour productivity, and maintains fuel consumption at ≤12 L/h, making it cost-efficient for medium acreage farms. The machine’s 4-wheel drive, 350 mm ground clearance, and 4,140 kg operating weight improve mobility in plains and hilly terrain, helping the company gain traction in Asia and export-led developing markets.

Top Key Players Outlook

- Deere & Company

- AGCO Corporation

- Samart Kasetyon Co., Ltd.

- Zoomlion Heavy Industry Science and Technology Co., Ltd.

- Tirth Agro Technology Private Limited (Shaktiman Agro)

- TAGRM Co. Ltd.

- Grupo Jacto

- Jiangsu World Agriculture Machinery Co., Ltd (World Group)

- Kartar Agro Industries Private Limited

- Yanmar Holdings Co., Ltd.

- Guangxi LiuGong Group

- Wuhan Wubota Machinery Co., Ltd.

Recent Industry Developments

In 2026, AGCO has guided net sales of $10.4 billion to $10.7 billion, adjusted operating margin of 7.5% to 8.0%, and earnings per share of $5.50 to $6.00, with production volumes expected to stay relatively flat.

In 2026, Deere reported net sales and revenues of $9,611 million, net income of $656 million, diluted EPS of $2.42, and Production & Precision Agriculture net sales of $3,163 million; management also raised its FY2026 net income outlook to $4.5 billion-$5.0 billion.

Report Scope

Report Features Description Market Value (2025) USD 2.3 Bn Forecast Revenue (2035) USD 5.8 Bn CAGR (2026-2035) 9.7% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Type (Whole-Stalk Harvesters, Chopper/Billet Harvesters), By Drive Mode (Self-Propelled, Tractor-Mounted/Towed), By Row-Capacity (Single-Row, Multi-Row) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA Competitive Landscape Deere & Company, AGCO Corporation, Samart Kasetyon Co., Ltd., Zoomlion Heavy Industry Science and Technology Co., Ltd., Tirth Agro Technology Private Limited (Shaktiman Agro), TAGRM Co. Ltd., Grupo Jacto, Jiangsu World Agriculture Machinery Co., Ltd (World Group), Kartar Agro Industries Private Limited, Yanmar Holdings Co., Ltd., Guangxi LiuGong Group, Wuhan Wubota Machinery Co., Ltd. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Sugarcane Harvesters MarketPublished date: April 2026add_shopping_cartBuy Now get_appDownload Sample

Sugarcane Harvesters MarketPublished date: April 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Deere & Company

- AGCO Corporation

- Samart Kasetyon Co., Ltd.

- Zoomlion Heavy Industry Science and Technology Co., Ltd.

- Tirth Agro Technology Private Limited (Shaktiman Agro)

- TAGRM Co. Ltd.

- Grupo Jacto

- Jiangsu World Agriculture Machinery Co., Ltd (World Group)

- Kartar Agro Industries Private Limited

- Yanmar Holdings Co., Ltd.

- Guangxi LiuGong Group

- Wuhan Wubota Machinery Co., Ltd.

Our Clients

- 183699

- April 2026