Global Slideway Oil Market By Base Oil (Mineral Oil-based Slideway Lubricants, Synthetic Oil-based Slideway Lubricants, and Bio-based Slideway Lubricants), By Viscosity (ISO VG 68, ISO VG 220, and Others), By Application (Lathes, Milling Machines, Grinding Machines, Machining Centers (CNC), and Others), By End-Use (Metalworking, Automotive And Auto Components, Aerospace And Defense, Marine And Rail, and Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2025-2034

- Published date: Feb 2026

- Report ID: 177370

- Number of Pages: 324

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

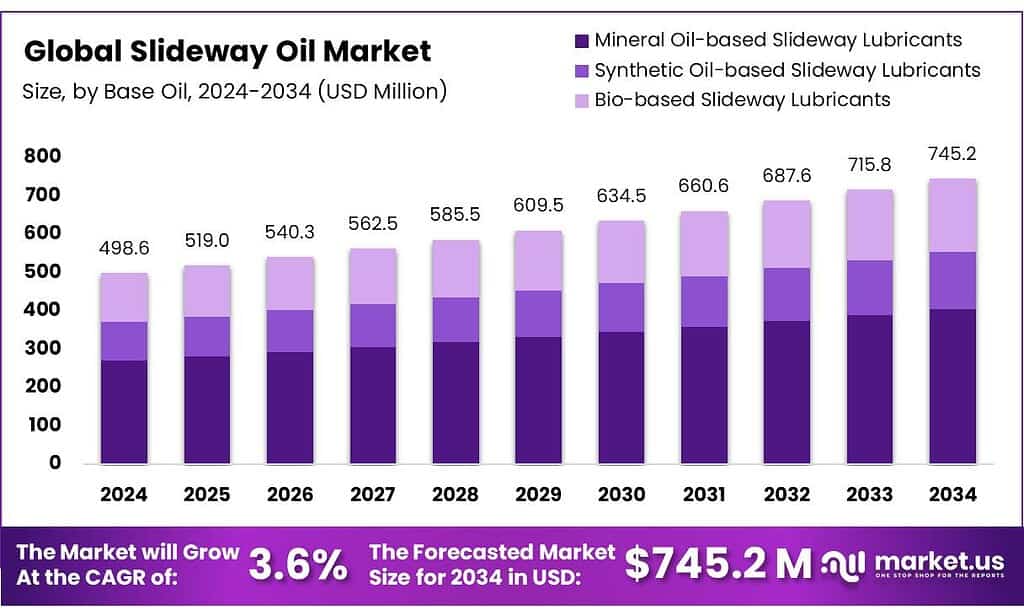

The Global Slideway Oil Market is expected to be worth around USD 745.2 Million by 2034, up from USD 498.6 Million in 2024, and is projected to grow at a CAGR of 4.1% from 2025 to 2034. The North America segment maintained 36.1%, supporting a Slideway Oil value of USD 192.0 Mn.

Slideway oil, also commonly called way oil or way lube, is a specialized industrial lubricant designed for the sliding surfaces of machine tools like lathes, milling machines, and grinders. Unlike standard oils, it is formulated to ensure precision and smooth movement at low speeds under high loads.

The market is driven primarily by industrial applications, especially in metalworking, where precision machinery, such as CNC machines, requires effective lubrication to ensure smooth operation, reduce wear, and maintain accuracy. In addition, the mineral oil-based slideway oils dominate the market due to their cost-effectiveness, availability, and proven performance across various temperature ranges.

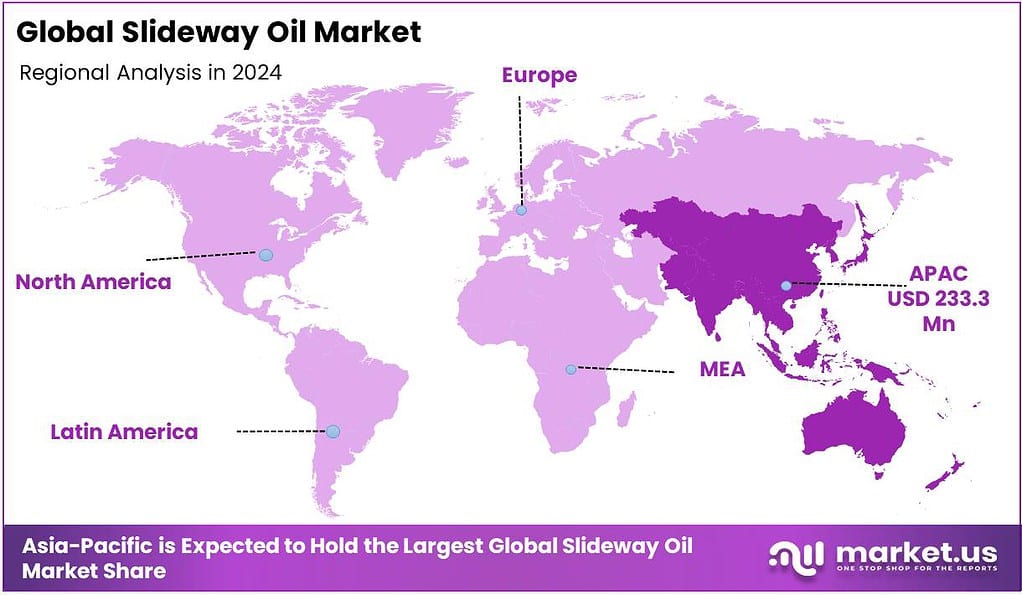

Asia Pacific is the largest market for slideway oils, driven by extensive manufacturing activities in countries like China, Japan, and South Korea, where high-precision equipment is in constant demand. However, the geopolitical tensions, such as trade disruptions and supply chain uncertainties, can impact the availability of raw materials, adding complexity to the market.

- The Chinese Ministry of Industry and Information Technology (MIIT) reported that alone China’s industrial output in 2024 rose by 5.8%, reaching US$5.7 trillion, with significant contributions from the machinery and automotive sectors, both of which are major consumers of slideway oils.

Furthermore, environmental regulations are pushing for more biodegradable options, while the ongoing adoption of automation in sectors such as automotive and electronics creates a growing need for lubricants that ensure efficient operation of advanced machinery.

- According to the U.S. Bureau of Labor Statistics, industrial automation in sectors such as automotive manufacturing and electronics has seen an uptick, with robotics usage increasing by 12% annually.

Key Takeaways

- The global slideway oil market was valued at USD 498.6 million in 2024.

- The global slideway oil market is projected to grow at a CAGR of 4.1% and is estimated to reach USD 745.2 million by 2034.

- On the basis of types of base oil, mineral oil-based slideway lubricants dominated the market, constituting 54.4% of the total market share.

- Based on the viscosity, ISO VG 68 dominated the slideway oil market, with a substantial market share of around 48.7%.

- Based on the applications, machining centers (CNC) led the slideway oil market, comprising 31.7% of the total market.

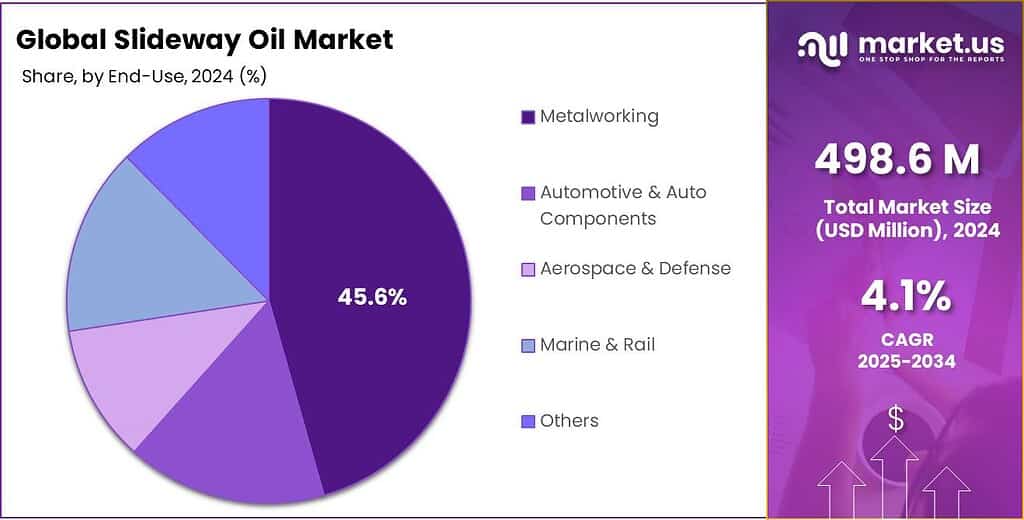

- Among the end-uses, metalworking held a major share in the slideway oil market, 45.6% of the market share.

- In 2024, the Asia Pacific was the most dominant region in the slideway oil market, accounting for 46.8% of the total global consumption.

Base Oil Analysis

Mineral Oil-based Slideway Lubricants are a Prominent Segment in the Market.

The slideway oil market is segmented based on base oil into mineral oil-based slideway lubricants, synthetic oil-based slideway lubricants, and bio-based slideway lubricants. The mineral oil-based slideway lubricants led the market, comprising 54.4% of the market share, due to their cost-effectiveness, availability, and established performance in a variety of industrial applications. Mineral oils, derived from crude oil, are relatively inexpensive to produce and are readily available, making them a practical choice for industries with large-scale lubricant needs.

Additionally, they have a well-observed performance history in reducing friction, wear, and corrosion on the slideway, providing reliability in long-term operations. While synthetic oils offer superior high-temperature stability and bio-based oils promote environmental sustainability, mineral oils remain the preferred choice due to their balance of performance, cost, and the established infrastructure for their use.

Viscosity Analysis

ISO VG 68 Slideway Oils Dominated the Market.

On the basis of the viscosity, the slideway oil market is segmented into ISO VG 68, ISO VG 220, and Others. The ISO VG 68 slideway oils dominated the market, comprising 48.7% of the market share, primarily due to their optimal viscosity for general industrial applications. ISO VG 68 provides a balanced performance in a wide range of temperatures, offering sufficient fluidity for ease of pumpability while maintaining effective film strength to prevent wear on machinery components. This makes it versatile for various types of machinery, particularly in moderate-temperature environments.

In contrast, ISO VG 220, with its higher viscosity, is more suitable for high-load, high-temperature applications but can lead to issues such as poor pumpability or excessive drag in machines operating under less demanding conditions. The broad compatibility and ease of use make ISO VG 68 the preferred choice for most industries.

Application Analysis

Slideway Oil Products Are Mostly Utilized in Machining Centers (CNC).

Based on the applications, the slideway oil market is divided into lathes, milling machines, grinding machines, machining centers (CNC), and others. The machining centers (CNC) dominated the slideway oil market, with a notable market share of 31.7%, as CNC machines require higher precision and smoother operation. CNC machining centers are equipped with complex, automated systems that rely on precise movements of axes and components, which makes high-quality lubrication essential to reduce friction, maintain accuracy, and prevent wear.

Slideway oils in CNCs ensure consistent performance of linear guides and ball screws under variable loads and speeds. In contrast, lathes, milling machines, and grinding machines, while still requiring lubrication, often involve simpler, less complex movements and less stringent demands for precision in the lubrication process. The CNC machining centers, with their need for high performance and reliability, consume the majority of slideway oils.

End-Use Analysis

Metalworking Held a Major Share of the Slideway Oil Market.

Among the end-uses, 45.6% of the total global consumption of slideway oil products is for metalworking, as it directly supports the critical operations in machining processes, where smooth movement and precision are essential. In metalworking, slideway oils are crucial for lubricating the slideways and linear guides in machines such as CNC mills, lathes, and grinders. These oils help reduce friction, maintain accuracy, and prolong the lifespan of equipment, ensuring efficient operation under constant mechanical stress.

While automotive, aerospace, marine, and rail industries require lubricants, their applications typically focus on engine oils, greases, and hydraulic fluids, which differ in function from slideway oils. Additionally, metalworking machines often run continuously, creating a higher demand for slideway oils in maintaining performance over extended periods, making this sector the largest consumer.

Key Market Segments

By Base Oil

- Mineral Oil-based Slideway Lubricants

- Synthetic Oil-based Slideway Lubricants

- Bio-based Slideway Lubricants

By Viscosity

- ISO VG 68

- ISO VG 220

- Others

By Application

- Lathes

- Milling Machines

- Grinding Machines

- Machining Centers (CNC)

- Others

By End-Use

- Metalworking

- Automotive & Auto Components

- Aerospace & Defense

- Marine & Rail

- Others

Drivers

Rapid Adoption of Automation in Various Sectors is a Key Driver of the Slideway Oil Market.

The rapid adoption of automation in various sectors has emerged as a critical driver in the demand for slideway oils, essential for machinery operating in automated environments. In manufacturing, the increased use of robotic systems and automated machinery, spanning from assembly lines to packaging, has necessitated the use of high-performance lubricants such as slideway oils to ensure smooth operations and minimize friction.

- According to the IEA, European companies have over half of the market share for industrial automation solutions, which marks the European countries as the major consumers of the slideway oil.

Similarly, in the energy sector, automation is driving greater demand for slideway oils in turbine and engine components. The automation technologies are being incorporated into oil extraction and refining operations to boost efficiency and safety, requiring advanced lubricants that can withstand higher operational stresses. These developments underscore that the shift toward automation, particularly in high-demand sectors such as manufacturing and energy, is directly influencing the growth of the slideway oil market.

Restraints

Environmental Regulations Along with Alternatives Might Dampen the Demand for the Slideway Oil.

Environmental regulations and the growing adoption of alternative lubricants are significant challenges for the slideway oil market. Stringent global regulations, such as the European Union’s REACH (Registration, Evaluation, Authorization, and Restriction of Chemicals) and the U.S. Environmental Protection Agency’s (EPA) requirements on toxic substances, have increasingly targeted the chemical composition of industrial lubricants.

The EU has specifically placed restrictions on hazardous substances commonly found in conventional slideway oils, such as heavy metals and certain chlorinated compounds, pushing manufacturers to reformulate products to comply with these standards. Simultaneously, the rise of multi-functional lubricants, products designed to serve multiple purposes, including lubrication, cooling, and corrosion protection, has emerged as an alternative to traditional slideway oils.

Moreover, the reduction in VOC (volatile organic compounds) emissions in line with the Clean Air Act in the U.S. and similar regulations in other regions has prompted oil producers to develop low-VOC alternatives, further impacting the traditional slideway oil market. These regulatory pressures may limit the growth of conventional slideway oil formulations.

Opportunity

Precision Manufacturing Creates Opportunities in the Slideway Oil Market.

The adoption of precision manufacturing technologies presents a notable opportunity for the slideway oil market. As industries increasingly adopt advanced techniques such as Computer Numerical Control (CNC) machining, additive manufacturing, and ultra-precise machining, there is a growing demand for high-performance lubricants, including slideway oils, to meet the stringent operational standards. Precision manufacturing often involves complex machinery that requires optimal lubrication to maintain accuracy, reduce wear, and ensure smooth movement.

The U.S. Department of Commerce’s National Institute of Standards and Technology (NIST) reported that the adoption of precision manufacturing technologies in sectors such as aerospace and electronics has risen. This growth has driven the demand for specialized lubricants that can withstand higher pressures and provide greater stability under extreme conditions.

Additionally, the European Commission’s Industry 4.0 initiative has underscored the importance of precision manufacturing in maintaining competitiveness in global markets, particularly in automotive and high-tech industries. The demand for lubricants capable of supporting high-precision systems, such as slideway oils, is expected to continue increasing as these industries push for enhanced efficiency and precision in manufacturing processes.

Trends

Shift Towards Biodegradable Slideway Oils.

The shift towards biodegradable slideway oils is gaining momentum as environmental concerns and regulatory pressures increase across industries. Governments worldwide are introducing stricter environmental regulations regarding the use and disposal of industrial lubricants. For instance, the European Union’s REACH regulation and the U.S. Environmental Protection Agency’s Clean Water Act have led to an increased focus on reducing the environmental impact of lubricants, prompting a move toward more sustainable alternatives, such as biodegradable slideway oils.

The biodegradable lubricants are essential in industries such as forestry, mining, and agriculture, where spillages are more frequent and can significantly harm ecosystems. The U.S. Forest Service has implemented the use of biodegradable lubricants in forestry equipment to mitigate environmental risks, with a focus on preventing contamination of soil and water.

Similarly, the International Maritime Organization (IMO) has emphasized the adoption of biodegradable lubricants for equipment used in marine environments, where non-biodegradable oils pose a significant ecological threat. Consequently, manufacturers are developing biodegradable alternatives that meet stringent performance standards. This shift represents a growing trend within the slideway oil market towards more environmentally responsible products.

Geopolitical Impact Analysis

Affected Demand Dynamics of Slideway Oil Amid Geopolitical Tensions.

The geopolitical tensions are having a notable impact on the slideway oil market, influencing supply chains and demand dynamics. The conflicts, such as the Russia-Ukraine war, have led to disruptions in the global supply of base oils and raw materials, which are essential for lubricant manufacturing. The sanctions on Russian oil exports have caused supply shortages, particularly affecting regions dependent on these imports, such as parts of Europe. This has led to higher production costs for lubricants, including slideway oils, as companies source alternatives from more distant suppliers. Additionally, trade restrictions and political instability are intensifying volatility in the supply of critical additives for slideway oils.

The geopolitical situation has influenced manufacturing and industrial production. In Asia, particularly China, trade uncertainty has caused fluctuations in industrial activity, directly impacting the consumption of slideway oils. The Chinese Ministry of Industry and Information Technology reported a decline in industrial output growth in 2022 due to geopolitical uncertainties, which likely contributed to slower lubricant demand in key sectors such as automotive and machinery.

Regional Analysis

Asia Pacific Held the Largest Share of the Global Slideway Oil Market.

In 2024, the Asia Pacific dominated the global slideway oil market, holding about 46.8% of the total global consumption, driven by its dominant manufacturing base and industrial activities. The region’s extensive industrial sector, which includes automotive, machinery, and electronics production, significantly drives the demand for high-performance lubricants such as slideway oils, which are essential for the smooth operation of automated machinery.

- According to the United Nations Industrial Development Organization (UNIDO), the Asia Pacific accounts for over 50% of global manufacturing output, particularly in countries such as China, Japan, and South Korea.

Additionally, Japan’s advanced manufacturing technologies, including robotics and precision machinery, require specialized lubricants, contributing to the steady demand for slideway oils. Furthermore, the region’s increasing emphasis on automation and precision manufacturing further amplifies the need for lubricants that ensure the smooth operation of high-precision equipment. As the demand for automated systems grows, the reliance on slideway oils to maintain operational efficiency and component longevity rises.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Manufacturers of slideway oils invest in research and development (R&D) to innovate and formulate lubricants with superior performance characteristics, such as enhanced stability, reduced friction, and better temperature tolerance. Additionally, manufacturers prioritize product customization to cater to specific needs in different industries, offering oils with varied viscosities and special additives.

Furthermore, they focus on expanding their distribution networks to reach new geographic markets, particularly in the Asia Pacific, where industrial activity is booming. Similarly, responding to environmental concerns, manufacturers are increasingly developing biodegradable and eco-friendly slideway oils, aligning with global sustainability initiatives.

The Major Players in The Industry

- BP plc

- Chem Arrow Corporation

- Chevron Corporation

- ENEOS Corporation

- ExxonMobil Corporation

- FUCHS

- LUKOIL

- MotulTech

- Petro-Canada Lubricants Inc.

- PETRONAS Lubricants International

- PT Idemitsu Lube Techno Indonesia

- Quaker Houghton

- Saudi Arabian Oil Co. (Valvoline)

- Shell plc

- Sinopec Lubricants Company

- TotalEnergies SE

- Other Key Players

Key Development

- In December 2024, Fuchs Group, a prominent global leader in the lubricant industry, completed its acquisition of STRUB & Co. AG., which aligned with Fuchs’ strategic initiative to expand its operations in Switzerland.

- In September 2025, TotalEnergies Marketing Canada unveiled a three-year strategic partnership with W.O. Stinson & Son Ltd., a leading independent distributor of petroleum products and lubricants in Canada, based in Ottawa, Ontario.

Report Scope

Report Features Description Market Value (2024) US$498.6 Mn Forecast Revenue (2034) US$745.2 Mn CAGR (2025-2034) 4.1% Base Year for Estimation 2024 Historic Period 2020-2023 Forecast Period 2025-2034 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Base Oil (Mineral Oil-based Slideway Lubricants, Synthetic Oil-based Slideway Lubricants, and Bio-based Slideway Lubricants), By Viscosity (ISO VG 68, ISO VG 220, and Others), By Application (Lathes, Milling Machines, Grinding Machines, Machining Centers (CNC), and Others), By End-Use (Metalworking, Automotive & Auto Components, Aerospace & Defense, Marine & Rail, and Others) Regional Analysis North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA Competitive Landscape BP p.l.c., Chem Arrow Corporation, Chevron Corporation, ENEOS Corporation, ExxonMobil Corporation, FUCHS, LUKOIL, MotulTech, Petro-Canada Lubricants Inc., PETRONAS Lubricants International, PT Idemitsu Lube Techno Indonesia, Quaker Houghton, Saudi Arabian Oil Co. (Valvoline), Shell plc, Sinopec Lubricants Company, TotalEnergies SE, and Other Players. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)

-

-

- BP plc

- Chem Arrow Corporation

- Chevron Corporation

- ENEOS Corporation

- ExxonMobil Corporation

- FUCHS

- LUKOIL

- MotulTech

- Petro-Canada Lubricants Inc.

- PETRONAS Lubricants International

- PT Idemitsu Lube Techno Indonesia

- Quaker Houghton

- Saudi Arabian Oil Co. (Valvoline)

- Shell plc

- Sinopec Lubricants Company

- TotalEnergies SE

- Other Key Players

Our Clients

- 177370

- Feb 2026