Global Skin Tightening Products Market Size, Share, Growth Analysis By Product (Creams/Lotions, Serums, Face Oils, Others), By Application (Face Lifting, Anti-Ageing, Others), By Distribution Channel (Supermarkets/Hypermarkets, Specialty Stores, Pharmacies, Online), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Feb 2026

- Report ID: 179572

- Number of Pages: 342

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

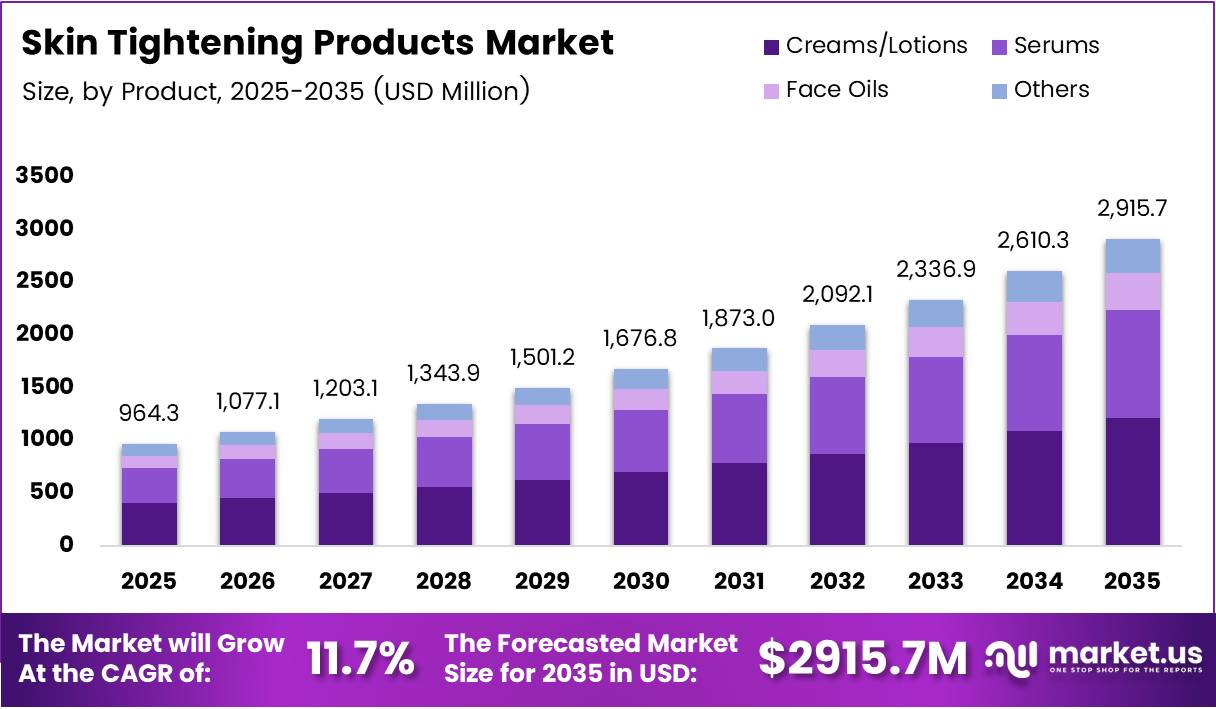

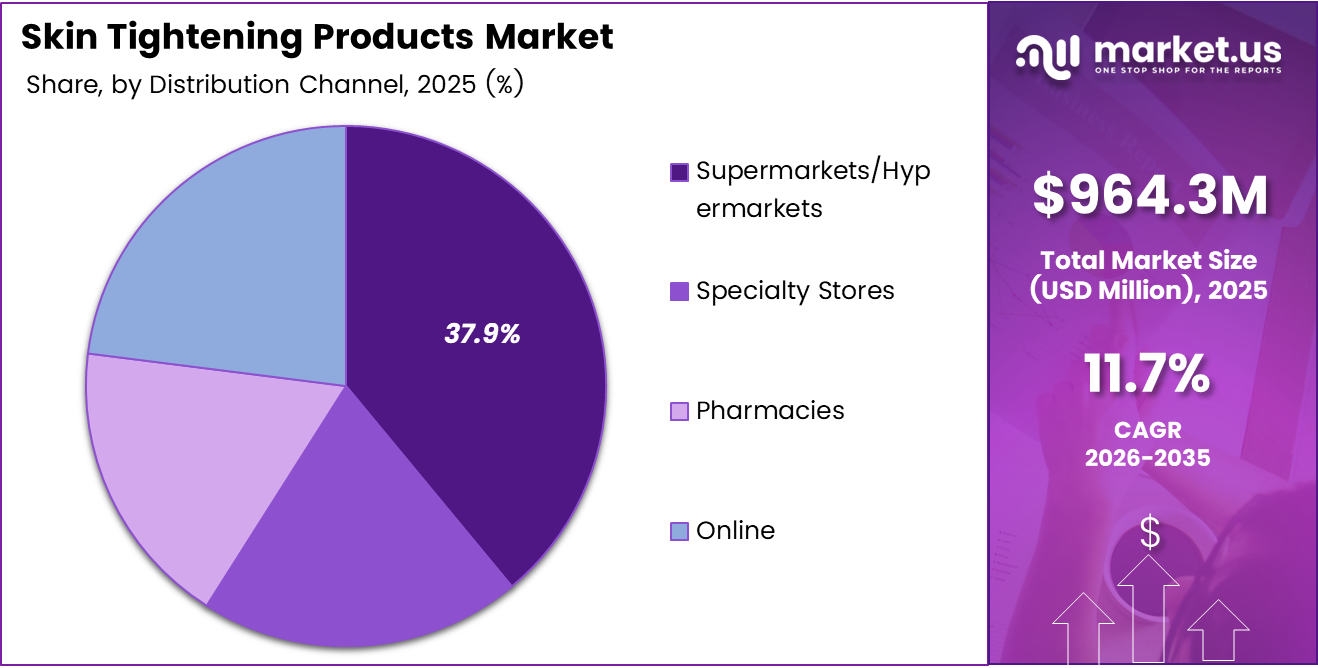

Global Skin Tightening Products Market size is expected to be worth around USD 2,915.7 Million by 2035 from USD 964.3 Million in 2025, growing at a CAGR of 11.7% during the forecast period 2026 to 2035.

The skin tightening products market covers topical formulations — including creams, serums, and face oils — designed to firm skin, stimulate collagen production, and reduce visible signs of aging. These products sit at the intersection of cosmetics and cosmeceuticals, where clinical efficacy increasingly defines purchase decisions rather than brand familiarity alone.

Urban aging populations across North America, Europe, and Asia Pacific now represent the primary buyer base. Consumers in these regions actively seek alternatives to surgical procedures, and topical skin firming solutions fill that gap. This preference shift toward non-invasive personal care directly sustains product volume across multiple price tiers.

Premium skincare spending continues to outpace mass-market growth, with consumers trading up toward serums and peptide-enriched formulations. Cosmeceutical products with dermatology-backed ingredients now command shelf space that previously belonged to general moisturizers, indicating a structural shift in how retailers and e-commerce platforms allocate category investment.

Digital beauty influencers accelerate ingredient-level education, shortening the path from clinical study to consumer purchase intent. When a specific active — such as retinol or a collagen-boosting peptide — gains traction on social platforms, product velocities respond within weeks. This shortens product innovation cycles and rewards brands with agile formulation pipelines.

Distribution expansion reinforces volume. Online channels now reach consumers in markets where specialty retail infrastructure remains underdeveloped, enabling brands to penetrate emerging middle-class demographics without physical store investment. This channel shift also improves margin profiles for direct-to-consumer brands competing against legacy retail incumbents.

According to pubmed.ncbi.nlm.nih.gov, 53.1% of patients reported over 50% overall improvement at 2 months post-treatment in a 2025 monopolar RF pilot study. This clinical validation matters for topical brands because it raises the consumer benchmark for what “effective” skin tightening means, pushing product developers to demonstrate measurable outcomes rather than rely on subjective claims.

According to gangnammedicalconcierge.com, most patients describe 20–30% improvement in skin firmness following non-invasive treatments. This expectation threshold now flows directly into topical product marketing, where brands must communicate clinically comparable or complementary results to retain buyers who compare devices and creams within the same purchase decision.

Key Takeaways

- The global Skin Tightening Products Market was valued at USD 964.3 Million in 2025 and is forecast to reach USD 2,915.7 Million by 2035.

- The market advances at a CAGR of 11.7% during the forecast period 2026 to 2035.

- By Product, Creams/Lotions dominate with a 51.3% share in 2025.

- By Application, Face Lifting leads with a 71.2% share in 2025.

- By Distribution Channel, Supermarkets/Hypermarkets hold the largest share at 37.9% in 2025.

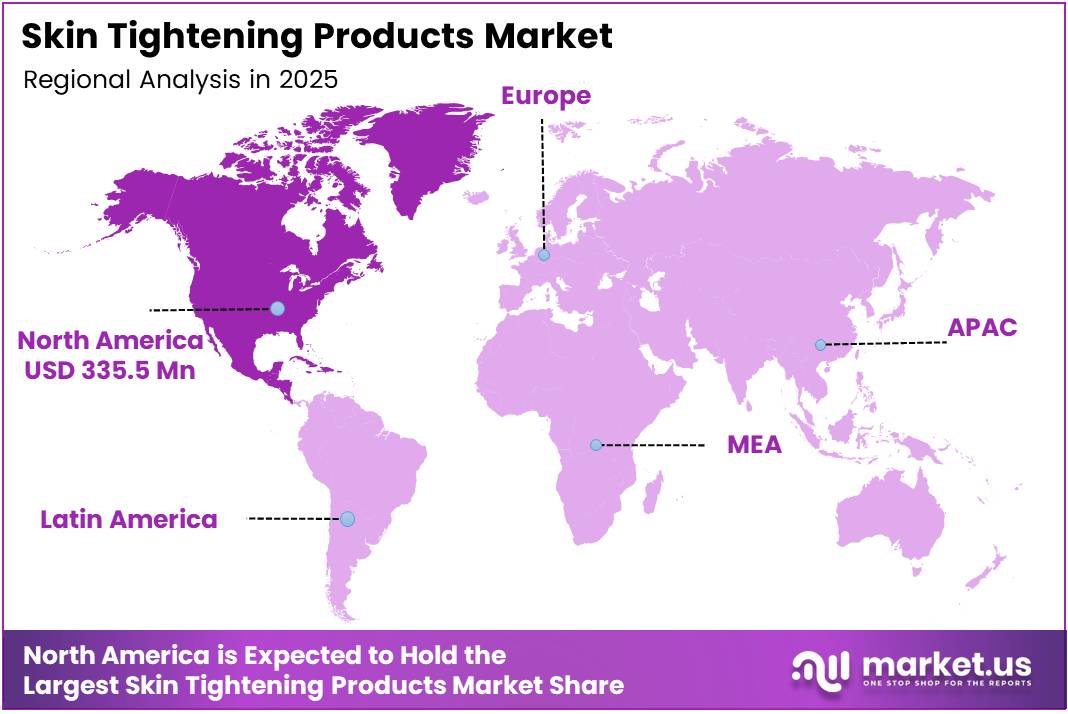

- North America leads all regions with a 34.80% share, valued at USD 335.5 Million in 2025.

Product Analysis

Creams/Lotions dominates with 51.3% due to broad consumer familiarity and accessibility.

In 2025, Creams/Lotions held a dominant market position in the By Product segment of the Skin Tightening Products Market, with a 51.3% share. Their dominance reflects consumer preference for familiar, easy-to-apply formats that integrate into daily skincare routines without requiring professional guidance or clinical settings.

Serums carry the highest active-ingredient concentration within the skin tightening category. Buyers seeking faster, more visible firming results gravitate toward serums, driving above-average unit pricing. Consequently, serum SKUs contribute disproportionately to revenue per transaction, making this sub-segment the primary margin driver for premium brands despite lower volume than creams.

Face Oils differentiate through a dual-benefit positioning — delivering both hydration and skin firming actives in a single step. Consumer interest in multi-functional, minimalist routines supports face oil adoption, particularly among buyers who prioritize ingredient transparency and clean-label formulations over traditional emulsion formats.

Others in the product segment include masks, patches, and mist-format tightening products. These formats serve occasion-based use cases, such as pre-event skin preparation. In October 2024, Classys completed its merger with Ilooda, integrating device and topical technologies — a move that signals complementary product formats will increasingly bundle devices with topical SKUs, widening the “Others” category over the forecast period.

Application Analysis

Face Lifting dominates with 71.2% due to concentrated consumer demand for visible facial contouring.

In 2025, Face Lifting held a dominant market position in the By Application segment of the Skin Tightening Products Market, with a 71.2% share. Consumers associate skin tightening primarily with facial definition — jawline contouring and cheek lifting — making facial applications the clearest purchase motivator and the segment with the strongest repeat-buy behavior.

Anti-Ageing applications extend the use case beyond lifting to broader skin quality improvement, including fine line reduction and elasticity restoration. This sub-segment attracts buyers at an earlier stage of the aging concern spectrum, effectively expanding the addressable consumer base and creating a longer purchase lifecycle per customer within the skin tightening category.

Others in the application segment cover neck tightening, body firming, and décolletage care. These areas represent an underpenetrated opportunity where consumer awareness lags facial applications. Brands that extend clinically validated facial formulations into neck and body formats can capture incremental revenue without rebuilding formulation infrastructure from scratch.

Distribution Channel Analysis

Supermarkets/Hypermarkets dominates with 37.9% due to mass-market reach and impulse purchase behavior.

In 2025, Supermarkets/Hypermarkets held a dominant market position in the By Distribution Channel segment of the Skin Tightening Products Market, with a 37.9% share. High foot traffic and visible shelf placement make this channel the most efficient route for mass-market skin firming products, particularly creams and lotions targeting first-time buyers.

Specialty Stores serve as the primary point of sale for premium and cosmeceutical skin tightening products. Trained beauty consultants in specialty retail convert higher-value transactions than mass channels, and the in-store testing environment allows consumers to experience product texture and absorption before purchase — a decisive factor for premium serums and oils.

Pharmacies reinforce the clinical credibility of dermatologist-recommended skin tightening formulations. Consumers who purchase through pharmacy channels signal higher trust in ingredient efficacy and are more likely to complete full treatment regimens, creating stronger repeat-purchase rates than impulse-driven mass retail formats.

Online channels remove geographic barriers and enable direct-to-consumer brands to compete on ingredient story and clinical evidence rather than shelf positioning. Subscription models and bundled product kits — common in online skin tightening retail — raise average order values and build customer lifetime value beyond what traditional retail formats can achieve.

Key Market Segments

By Product

- Creams/Lotions

- Serums

- Face Oils

- Others

By Application

- Face Lifting

- Anti-Ageing

- Others

By Distribution Channel

- Supermarkets/Hypermarkets

- Specialty Stores

- Pharmacies

- Online

Drivers

Aging Urban Consumers and Premium Skincare Spending Accelerate Topical Skin Firming Adoption

Urban aging populations now treat skin tightening products as a planned skincare investment rather than an occasional purchase. Consumers actively replace surgical consultations with topical collagen-boosting solutions, shifting volume from clinical settings to retail shelves. This behavioral change expands the addressable buyer pool well beyond traditional anti-aging demographics.

Premium cosmeceutical spending reinforces this shift. Buyers trade up to higher-priced serums and peptide-enriched formulations when they associate product efficacy with visible, measurable outcomes. According to jkslms.or.kr, collagen bundle diameter showed significant thickening at the 6.78 + 2 MHz dual-frequency mode one month post-treatment (p < 0.0001), confirming that device-validated collagen response now informs consumer expectations for topical products delivering similar biological pathways.

Digital beauty influencers accelerate ingredient-level education at scale. When specific actives — retinol, peptides, radiofrequency-complementary compounds — gain clinical credibility online, consumer purchase intent responds within weeks. In August 2025, Debut raised $20 million in funding to advance AI-driven biotech ingredients targeting in-office-comparable skin tightening results, signaling that the topical formulation pipeline is moving closer to device-level clinical benchmarks.

Restraints

High Regulatory Compliance Costs and Efficacy Skepticism Limit Market Accessibility for Smaller Brands

Developing skin tightening products that meet stringent cosmetic regulatory requirements across multiple geographies demands substantial investment. Formulation testing, stability studies, and claim substantiation add cost layers that smaller or emerging brands struggle to absorb. This creates a structural barrier that consolidates product development capacity among well-capitalized incumbents.

Consumer skepticism compounds the cost problem. Buyers who do not see visible tightening results within their expected timeline abandon repurchase, even when the product’s clinical mechanism requires consistent use over several months. This disconnect between marketing timelines and biological reality directly pressures brand credibility and forces higher investment in consumer education and clinical evidence communication.

Delayed visible results reduce repeat-purchase conversion rates in online channels where reviews drive discovery. A single wave of low-rating reviews citing slow efficacy can suppress organic search ranking and new buyer acquisition simultaneously. Therefore, brands without robust clinical trial data to set realistic consumer expectations face disproportionate attrition in the direct-to-consumer segment.

Growth Factors

Advanced Formulations, Emerging Market Penetration, and Clinic-Brand Partnerships Open New Revenue Channels

Peptide-based and retinol-infused formulations address the performance gap between topical products and device-based treatments. Brands that build clinical evidence for these advanced actives can reposition skin tightening from a cosmetic category into a cosmeceutical one — commanding premium pricing and attracting dermatology-driven distribution partnerships. According to pubmed.ncbi.nlm.nih.gov, skin radiance significantly increased at 4 weeks (p = 0.037) and 8 weeks (p < 0.001) following monopolar RF treatment, establishing the biological benchmark that topical brands must now reference in efficacy communications.

Emerging markets with rising middle-class beauty consumption represent the next geographic growth layer. Online distribution removes the need for physical retail infrastructure, allowing brands to enter markets in Southeast Asia, Latin America, and the Middle East without traditional channel investment. In February 2025, Crown Laboratories completed the acquisition of Revance Therapeutics, combining skincare and aesthetic offerings including SkinPen microneedling — a move that illustrates how brand consolidation accelerates cross-category penetration into new consumer segments.

Strategic collaborations between dermatology clinics and skincare brands create credibility bridges that pure retail cannot replicate. Clinic-endorsed formulations reach consumers already primed for skin tightening investment and willing to pay premium prices for dermatologist-validated products. AI-driven skin analysis tools that generate personalized product recommendations extend this clinical credibility into digital retail, converting data-led consultations into high-intent purchases.

Emerging Trends

Clean-Label Formulations, Multi-Functional Products, and Device Complementarity Redefine the Skin Tightening Category

Consumer preference for clean-label, dermatologically tested skin tightening products reflects a broader shift in purchase criteria — from fragrance and texture to ingredient transparency and safety documentation. Brands that publish clinical testing data and third-party dermatologist validation capture the trust premium that marketing spend alone cannot buy, particularly among buyers researching purchases through digital channels.

Multi-functional creams that combine hydration, lifting, and UV protection reduce the step-count in skincare routines while maintaining efficacy expectations. This format resonates with time-constrained urban consumers who previously required three separate products. According to findyourbeautiful.com, Ultherapy PRIME treatments are 20% faster than prior versions while delivering equivalent lifting results — a device-side efficiency benchmark that topical multi-functional formats are now competing against in consumer preference surveys.

Sustainable packaging adoption in premium skincare lines signals a shift in brand positioning strategy. Consumers purchasing premium skin tightening products increasingly factor environmental credentials into their choice. Additionally, home-use skin tightening devices now complement topical products rather than compete with them, creating bundle opportunities where a serum or cream becomes a prescribed companion to a personal RF or ultrasound device — expanding the total transaction value per skin tightening buyer.

Regional Analysis

North America Dominates the Skin Tightening Products Market with a Market Share of 34.80%, Valued at USD 335.5 Million

North America leads with a 34.80% share valued at USD 335.5 Million in 2025. The region’s dominance reflects mature consumer skincare spending habits, strong dermatologist-recommended product ecosystems, and early adoption of cosmeceutical ingredients. The US market, in particular, supports premium price points that sustain high revenue concentration relative to volume.

Europe Skin Tightening Products Market Trends

Europe represents the second-largest market, supported by stringent cosmetic ingredient regulations that paradoxically raise consumer trust. Buyers in Germany, France, and the UK associate regulatory compliance with product safety, making certified formulations a commercial advantage. Premium anti-aging brand heritage across Western Europe also supports above-average spending per unit.

Asia Pacific Skin Tightening Products Market Trends

Asia Pacific presents the fastest-expanding consumer base for skin tightening formulations. China, South Korea, and Japan lead regional consumption, driven by high beauty expenditure per capita and a cultural premium placed on youthful skin appearance. South Korea’s cosmeceutical innovation pipeline also positions APAC as a product development hub, not just a consumption market.

Latin America Skin Tightening Products Market Trends

Latin America’s market develops on the back of rising middle-class disposable income and increasing digital retail penetration. Brazil and Mexico anchor regional volume. In November 2025, Classys acquired JL Health (Brazil) for $13 million, securing exclusive HIFU device distribution rights across South America — signaling that global players now view the region as a strategic priority worth direct investment.

Middle East and Africa Skin Tightening Products Market Trends

The Middle East and Africa region records early-stage but consistent consumption growth in skin tightening products, concentrated within GCC countries where high per-capita income supports luxury cosmetics spending. Clinic-based aesthetic treatments remain the primary entry point for skin tightening awareness, creating downstream demand for topical maintenance products among post-treatment consumers.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Neutrogena positions itself at the convergence of dermatology credibility and mass-market distribution, a combination that few competitors replicate effectively. Its clinical heritage — reinforced through dermatologist endorsements — allows Neutrogena to sustain premium pricing within supermarket and pharmacy channels where competing brands rely primarily on packaging. This dual-channel advantage creates a defensible volume and margin position simultaneously.

Olay leverages decades of consumer trust data to target the anti-aging segment with science-backed formulations accessible at mass-market price points. Its Regenerist and Collagen Peptide lines directly address the skin firming category, competing on clinical ingredient credibility rather than luxury positioning. This strategy captures cost-sensitive buyers who demand visible results without premium pricing — a large and structurally stable segment.

SkinCeuticals concentrates its competitive advantage in the professional and clinic-based distribution channel, where dermatologist recommendations drive purchase decisions rather than advertising. Products supported by antioxidant and collagen-stimulation science command significantly higher unit prices. This clinic-first model creates high brand loyalty and insulates SkinCeuticals from price competition in mass retail channels where ingredient storytelling is harder to execute.

The Ordinary disrupted the premium skincare market by publishing ingredient concentrations transparently and pricing formulations at accessible levels, forcing legacy brands to justify their price premiums with comparable clinical evidence. Within skin tightening, its retinol and peptide products attract ingredient-educated consumers who would previously have purchased at two to five times the price point. This value-led positioning expands the category’s total consumer base.

Key Players

- Neutrogena

- Olay

- SkinCeuticals

- The Ordinary

- Kiehl’s

- Clarins

- Estée Lauder Inc

- Murad

- Dr. Dennis Gross Skincare

- StriVectin

Recent Developments

- September 2024 — Merz Aesthetics launched Ultherapy PRIME, a next-generation noninvasive microfocused ultrasound platform for personalized skin lifting and tightening. The system features real-time visualization, treatments that are 20% faster than prior versions, and zero downtime for patients.

- March 2025 — ENDYMED completed its full merger with majority shareholder and China distributor Shanghai Haohai Biological Technology. The merger strengthens ENDYMED’s global supply chain and accelerates innovation in its 3DEEP RF skin tightening systems across key international markets.

- August 2025 — Cynosure Lutronic received U.S. FDA clearance on August 11 for the XERF dual-frequency (6.78 MHz + 2 MHz) monopolar RF system. The device delivers noninvasive structural skin tightening with no needles, no numbing agent required, and zero recovery downtime.

- November 2025 — Classys acquired JL Health (Brazil) for $13 million, securing exclusive distribution rights for its flagship HIFU skin tightening devices across South America. The acquisition directly strengthens Classys’s position in the Latin American aesthetics market ahead of forecast period growth.

Report Scope

Report Features Description Market Value (2025) USD 964.3 Million Forecast Revenue (2035) USD 2,915.7 Million CAGR (2026-2035) 11.7% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product (Creams/Lotions, Serums, Face Oils, Others), By Application (Face Lifting, Anti-Ageing, Others), By Distribution Channel (Supermarkets/Hypermarkets, Specialty Stores, Pharmacies, Online) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Neutrogena, Olay, SkinCeuticals, The Ordinary, Kiehl’s, Clarins, Estée Lauder Inc, Murad, Dr. Dennis Gross Skincare, StriVectin Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Skin Tightening Products MarketPublished date: Feb 2026add_shopping_cartBuy Now get_appDownload Sample

Skin Tightening Products MarketPublished date: Feb 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Neutrogena

- Olay

- SkinCeuticals

- The Ordinary

- Kiehl's

- Clarins

- Estée Lauder Inc

- Murad

- Dr. Dennis Gross Skincare

- StriVectin

Our Clients

- 179572

- Feb 2026