Quick Navigation

Report Overview

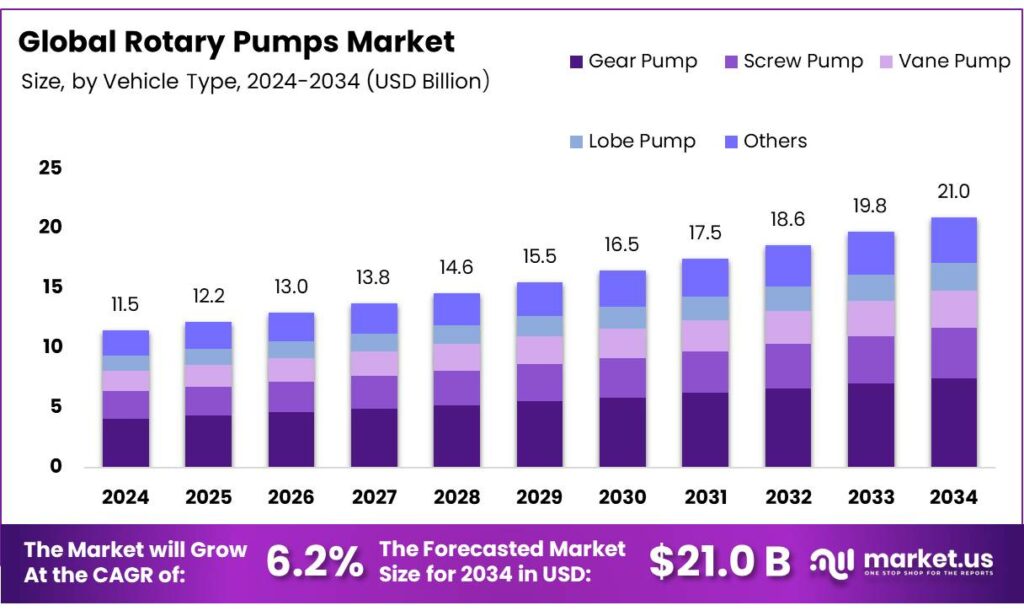

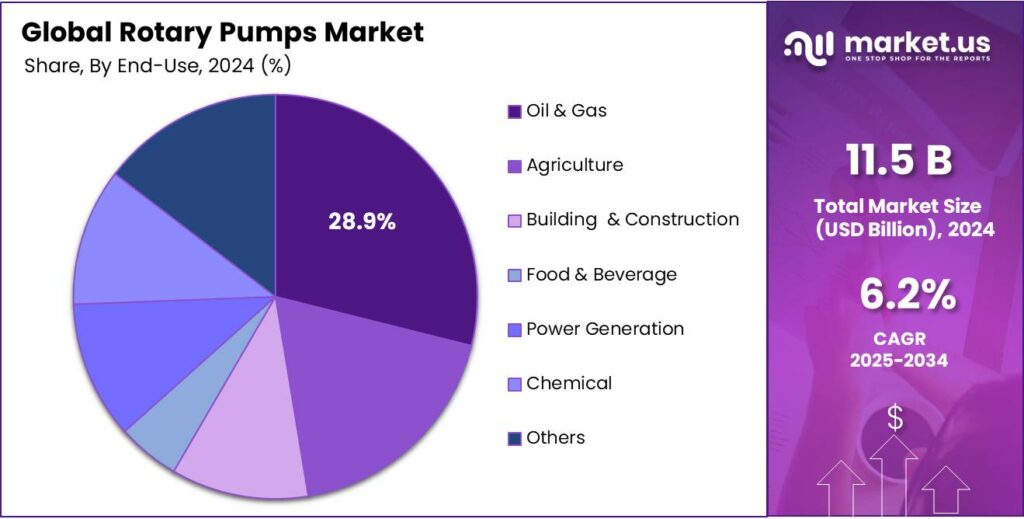

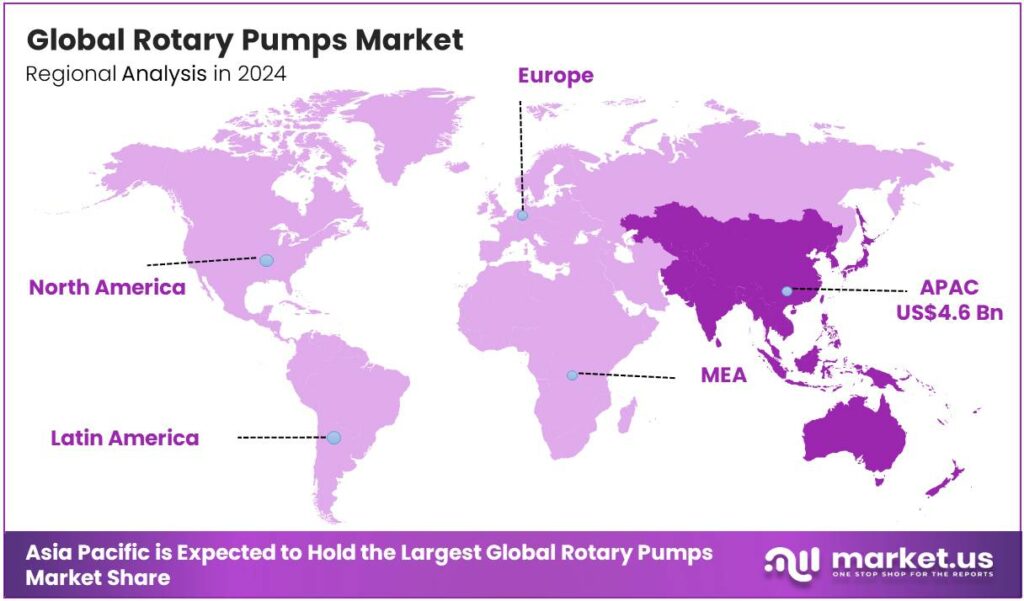

The Global Rotary Pumps Market is expected to be worth around USD 21.0 Billion by 2034, up from USD 11.5 Billion in 2024, and is projected to grow at a CAGR of 6.2% from 2025 to 2034. The Asia Pacific segment maintained 40.2%, supporting a Rotary Pumps value of USD 4.6 Bn.

Rotary pumps are a type of positive displacement (PD) pump that move fluid by trapping a fixed volume within a rotating mechanism and forcing it through a discharge port. Unlike centrifugal pumps, which use kinetic energy to create flow, rotary pumps rely on mechanical action to provide a consistent, nearly constant flow rate regardless of changes in system pressure.

- The U.S. Department of Energy (DOE) notes that industrial manufacturing processes utilize over 2.4 million pumps, consuming approximately 142 billion kWh annually.

Its market is driven by diverse industrial needs, with applications spanning sectors such as oil and gas, chemicals, water treatment, and food processing. These pumps are particularly valued for their ability to handle a wide range of fluids, including high-viscosity, abrasive, or solid-laden materials. The oil and gas industry remains the largest market for rotary pumps, as their ability to manage high-pressure and high-volume flows is essential in extraction, transportation, and refining processes.

- A study commissioned by the U.S. Department of Energy (DOE) found that a gear pump’s efficiency can degrade by 10% to 25% before replacement, with standard industrial efficiencies commonly ranging between 50% and 60%.

Pumps with discharge pressures of 25-100 bar and capacities between 151-500 m³/h are commonly used due to their versatility and cost-efficiency. While other industries use rotary pumps, such as pharmaceuticals and chemicals, the oil and gas sector’s demand for specialized, robust equipment pushes its prominence. Innovations in design, such as seal-less pumps and energy-efficient models, are further enhancing pump performance and addressing growing environmental and operational challenges across sectors.

Key Takeaways:

- The global rotary pumps market was valued at USD 11.5 billion in 2024.

- The global rotary pumps market is projected to grow at a CAGR of 6.2% and is estimated to reach USD 21.0 billion by 2034.

- On the basis of types of pumps, gear rotary pumps dominated the market, constituting 35.6% of the total market share.

- Based on the discharge pressure, rotary pumps with 25-100 bar dominated the market, with a market share of around 33.2%.

- Based on the pump capacity, rotary pumps with 151-500 m³/h capacity led the market, comprising 30.1% of the total market.

- Among the end-uses, the oil & gas sector held a major share in the rotary pumps market, 28.9% of the market share.

- In 2024, the Asia-Pacific was the most dominant region in the rotary pumps market, accounting for 40.2% of the total global consumption.

Pump Type Analysis

Gear Rotary Pumps are a Prominent Segment in the Market.

The rotary pumps market is segmented based on pump type into gear pump, screw pump, vane pump, lobe pump, and others. The gear rotary pumps led the market, comprising 35.6% of the market share, due to their simplicity, cost-effectiveness, and versatility. Their design features two interlocking gears that efficiently move fluid with minimal pulsation, making them ideal for a wide range of applications, including low to medium-viscosity fluids.

Gear pumps can handle clean and slightly contaminated liquids, making them adaptable for industries such as chemicals, food processing, and pharmaceuticals. Additionally, their compact design and ease of maintenance contribute to their popularity. Similarly, they provide reliable performance in high-pressure applications, making them a preferred choice where consistent, smooth flow is crucial.

Discharge Pressure Analysis

Rotary Pumps with 25-100 bar Discharge Pressure Dominated the Market.

On the basis of the discharge pressure, the rotary pumps market is segmented into up to 10 bar, 10-25 bar, 25-100 bar, and above 100 bar. The rotary pumps with 25-100 bar discharge pressure dominated the market, comprising 33.2% of the market share. Rotary pumps with discharge pressures between 25 and 100 bar offer a versatile range that meets the demands of many industries without requiring excessive design complexity or high costs.

The pressure range is ideal for handling fluids in medium-to-heavy-duty applications, such as chemical processing, food and beverage, and water treatment, where moderate pressures are necessary for efficient operation. Pumps in this range are well-suited for maintaining steady flow rates and are generally more energy-efficient than those designed for either low or very high pressures.

In contrast, pumps with discharge pressures below 25 bar may not provide sufficient performance for these industries, while pumps exceeding 100 bar are typically used for niche, high-pressure applications that require specialized equipment and incur higher operational costs.

Pump Capacity Analysis

Rotary Pumps with a Capacity of 151-500 m³/h Accounted for Most Shares in the Market.

Based on the pump capacity, the rotary pumps market is divided into up to 50 m³/h, 51-150 m³/h, 151-500 m³/h, and above 500 m³/h. Rotary pumps with a capacity of 151-500 m³/h dominated the market, with a notable market share of 30.1%. They meet the demands of a broad range of medium to large-scale industrial applications, such as chemical processing, water treatment, and oil and gas. This capacity range offers a good balance between flow rate and operational efficiency, making it suitable for industries that require consistent, moderate flow over extended periods.

In contrast, pumps with smaller capacities, up to 50 m³/h or 51-150 m³/h, may not provide enough throughput for larger facilities, while those with capacities above 500 m³/h are typically designed for specialized, high-flow applications that require more complex systems and incur higher costs. The 151-500 m³/h range strikes a cost-effective balance for industries requiring steady, high-volume fluid movement without excessive energy consumption or maintenance issues.

End-Use Analysis

The Oil & Gas Industry Held a Major Share of the Rotary Pumps Market.

Among the end-uses, 28.9% of the total global consumption of rotary pumps is for the oil & gas industry. These pumps are highly suited to handle the specific demands of the oil and gas industry, such as pumping viscous, abrasive, or volatile fluids under high pressure. Rotary pumps offer reliable, continuous flow with minimal pulsation, making them ideal for oil extraction, transportation, and refining processes. Additionally, they are effective in managing heavy-duty fluids, including crude oil and drilling muds, which require robust, efficient handling systems.

While other industries, such as agriculture, food and beverage, or power generation, use rotary pumps, the oil and gas sector’s need for high-pressure, high-volume fluid handling makes rotary pumps indispensable. Additionally, oil and gas applications often demand specialized equipment that ensures safety and compliance with regulatory standards, further driving the preference for rotary pumps in this industry.

Key Market Segments:

By Pump Type

- Gear Pump

- Screw Pump

- Vane Pump

- Lobe Pump

- Others

By Discharge Pressure

- Up to 10 bar

- 10-25 bar

- 25-100 bar

- Above 100 bar

By Pump Capacity

- Up to 50 m³/h

- 51-150 m³/h

- 151-500 m³/h

- Above 500 m³/h

By End-Use

- Oil & Gas

- Agriculture

- Building & Construction

- Food & Beverage

- Power Generation

- Chemical

- Others

Drivers

Industrial Expansion Drives the Rotary Pumps Market.

Industrial expansion and the systemic modernization of production facilities serve as primary drivers for the rotary pump market, shifting demand from basic fluid transport to high-precision, energy-efficient applications. This transition is rooted in regulatory compliance and the need for operational optimization. As manufacturing sectors adopt advanced technologies to improve productivity, the demand for reliable and efficient pumping solutions has surged.

- For instance, in the energy sector, the International Energy Agency (IEA) forecasted that the total supply of oil capacity would rise by 6 mb/d to nearly 113.8 mb/d by 2030, driving the need for more robust pumping equipment in oil and gas extraction. Similarly, the expansion of water treatment facilities, particularly in developing regions, has led to heightened demand for rotary pumps used in desalination and wastewater management.

- According to the U.S. Bureau of Labor Statistics, between 2010 and 2020, the number of industrial machinery manufacturing jobs in the U.S. grew by 4.5%, underlining the sector’s expansion.

Furthermore, advancements in automation and precision engineering have bolstered the capabilities of rotary pumps, making them integral to industries such as food and beverage, chemicals, and pharmaceuticals, where stringent operational standards are essential.

Restraints

Operational Limitations Pose Significant Challenges to the Rotary Pumps Market.

The operational limitations of rotary pumps present a significant challenge in the market. One key issue is their sensitivity to the viscosity and temperature of the fluids being pumped. The rotary pumps face performance degradation when handling highly viscous fluids, as the increased resistance leads to reduced efficiency and higher energy consumption.

- After China and the USA, Europe has the third-largest electricity consumption in the world, of around 3,300 terawatt hours (TWh) per year. Additionally, more than 300 TWh of this is accounted for by electric pumps.

Furthermore, rotary pumps can experience cavitation in low-pressure conditions, causing damage to components and leading to frequent maintenance. In water treatment plants, rotary pumps must often be replaced or repaired due to cavitation or wear from abrasive fluids, particularly in wastewater management applications.

Additionally, rotary pumps may struggle with variable flow rates, making them less suitable for operations requiring precise flow control. These limitations are evident in various industries, where the need for highly accurate and reliable pumps often requires the use of alternative pump types.

Opportunity

Management of Complex Media and Sanitary Applications Creates Opportunities in the Rotary Pumps Market.

The capability of rotary lobe and gear pumps to manage complex media under stringent regulatory frameworks represents a critical growth opportunity in the fluid handling market. These positive displacement pumps maintain consistent volumetric efficiency across varying viscosities and pressures.

Rotary lobe pumps are specifically engineered to transport media with viscosities ranging from 1 cSt to over 1,000,000 SSU, approximately 200,000 to 1,000,000 cP. Their non-contacting, counter-rotating lobes create large cavities capable of passing significant suspended solids, such as fruit pieces, curd, or meat cubes, without product degradation or mechanical clogging.

Similarly, the market for sanitary rotary pumps is underpinned by institutional compliance, particularly in the food, pharmaceutical, and biotechnology sectors. Modern lobe pumps utilize Clean-in-Place (CIP) and Steam-in-Place (SIP) capabilities, reducing downtime by allowing sterilization without disassembly.

They accommodate solid-laden fluids without compromising their integrity, a feature critical in sectors such as wastewater treatment and chemicals. For sensitive pharmaceutical media, these pumps offer low-shear operation to preserve biological cultures or delicate suspensions. In the pharmaceutical industry, sanitary standards are paramount, and lobe and gear pumps’ ability to meet stringent hygiene requirements is underscored by their compliance with FDA and European Hygienic Engineering & Design Group (EHEDG) standards for hygienic design.

Trends

Shift Towards Seal-Less Rotary Pumps.

The transition toward seal-less rotary pumps, primarily magnetic drive and canned motor designs, represents a strategic shift in industrial fluid handling aimed at eliminating mechanical seals, which are frequently identified as the primary point of failure in conventional pumps. The seal-less pumps replace dynamic mechanical seals with a static containment shell or isolation shroud, creating a hermetically sealed environment.

This is particularly advantageous in industries handling hazardous chemicals or volatile substances. The environmental benefits of seal-less pumps in preventing fluid leakage are crucial for compliance with spill prevention and control regulations.

Seal-less technology is increasingly integrated into various rotary designs, including sliding vane, hollow disc, and screw pumps. These are essential for high-purity sectors like semiconductor fabrication and pharmaceutical manufacturing, where maintaining a contamination-free environment is a regulatory mandate.

In the chemical industry, seal-less pumps are increasingly used in applications involving aggressive fluids or high pressures, where the risk of seal failure can result in costly shutdowns or safety hazards. Additionally, the U.S. Food and Drug Administration (FDA) supports the use of seal-less pumps in pharmaceutical manufacturing, as they reduce contamination risks associated with seal leakage.

Geopolitical Impact Analysis

Geopolitical Uncertainties Have Affected Global Rotary Pumps Supply Chains.

The geopolitical tensions, particularly the ongoing conflicts and trade disputes, have significantly impacted the rotary pumps market, primarily through supply chain disruptions and material shortages. The sanctions and trade restrictions on key industrial suppliers, especially in Europe and Asia, have led to delays in the procurement of raw materials such as stainless steel, which is critical for manufacturing pumps.

For instance, the EU’s imposition of tariffs on certain Chinese and Russian industrial products has caused fluctuations in material costs and availability for pump manufacturers. Additionally, the U.S. Bureau of Industry and Security (BIS) has restricted exports of advanced manufacturing technology to countries such as China, affecting the production capabilities of certain pump models.

Furthermore, geopolitical instability in energy-producing regions, such as the Middle East, has disrupted the supply of petroleum-based fluids, directly impacting the demand for rotary pumps in the oil and gas sector. The International Energy Agency (IEA) highlighted that fluctuations in energy prices due to these tensions could affect operational budgets for industries reliant on fluid handling systems. Consequently, manufacturers face increasing costs, which are often passed on to end-users, impacting the overall market dynamics.

Regional Analysis

Asia Pacific Held the Largest Share of the Global Rotary Pumps Market.

In 2024, the Asia Pacific dominated the global rotary pumps market, holding about 40.2% of the total global consumption, driven by rapid industrialization, infrastructure development, and growing demand across various sectors such as chemicals, water treatment, and food processing. According to the International Energy Agency (IEA), the region’s energy demand has grown significantly, with countries such as China and India investing heavily in oil and gas infrastructure, increasing the need for robust pumping solutions in exploration and extraction processes.

In the water treatment sector, over 60% of the global demand for water treatment systems originates from the region, further bolstering the demand for rotary pumps. Additionally, the region’s rapid urbanization has led to greater investment in sanitation and wastewater management. These factors position Asia Pacific as the dominant market for rotary pumps, catering to diverse and growing industrial needs.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Manufacturers of rotary pumps focus on several strategic activities, including innovation in pump design to improve efficiency, reduce energy consumption, and enhance durability under challenging operating conditions, such as handling high-viscosity or abrasive fluids. Companies invest in enhancing after-sales services, including offering maintenance contracts, technical support, and repair services, to build long-term customer relationships.

Additionally, manufacturers are increasingly prioritizing sustainability by developing eco-friendly solutions, such as seal-less and energy-efficient pumps, to meet growing environmental regulations. Similarly, expanding production facilities and strategic partnerships for a more robust supply chain help manufacturers reduce lead times and ensure consistent product availability across regions.

The Major Players in The Industry

- Atlas Copco AB

- Dover Corporation

- Xylem Inc.

- Colfax Corporation

- IDEX Corporation

- Flowserve Corporation

- KSB SE & Co. KGaA

- HMS Group

- Pentair Ltd.

- SPX Flow

- Alfa Laval

- Ingersoll Rand

- ITT INC.

- Roper Technologies Inc.

- Schlumberger Ltd.

- Other Key Players

Key Development

- In January 2024, Atlas Copco introduced its DVS vacuum pump series. The outcome is the DVS models, which are oil-free, dry rotary vane pumps that ensure emission-free, quiet operation while maintaining process purity by preventing contamination.

- In June 2025, PSG, a subsidiary of Dover Corporation, announced the acquisition of ipp Pump Products GmbH, a company specializing in the manufacture of sanitary pump technologies, including hygienic lobe pumps, progressive cavity pumps, and other processing equipment.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | US$11.5 Bn |

| Forecast Revenue (2034) | US$21.0 Bn |

| CAGR (2025-2034) | 6.2% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Pump Type (Gear Pump, Screw Pump, Vane Pump, Lobe Pump, and Others), By Discharge Pressure (Up to 10 bar, 10-25 bar, 25-100 bar, and Above 100 bar), By Pump Capacity (Up to 50 m³/h, 51-150 m³/h, 151-500 m³/h, and Above 500 m³/h), By End-Use (Agriculture, Building & Construction, Food & Beverage, Power Generation, Oil & Gas, Chemical, and Others) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Atlas Copco AB, Dover Corporation, Xylem Inc., Colfax Corporation, IDEX Corporation, Flowserve Corporation, KSB SE & Co. KGaA, HMS Group, Pentair Ltd., SPX Flow, Alfa Laval, Ingersoll Rand, ITT INC., Roper Technologies Inc., Schlumberger Ltd., and Other Players. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |