Global Rosemary Hair Care Products Market Size, Share, Growth Analysis By Product (Shampoo & Conditioner, Hair Oil, Hair Serum, Hair Masks, Others), By End-use (Women, Men), By Distribution Channel (Supermarkets & Hypermarkets, Specialty Beauty Stores, Pharmacies & Drugstores, E-commerce, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Mar 2026

- Report ID: 182639

- Number of Pages: 302

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

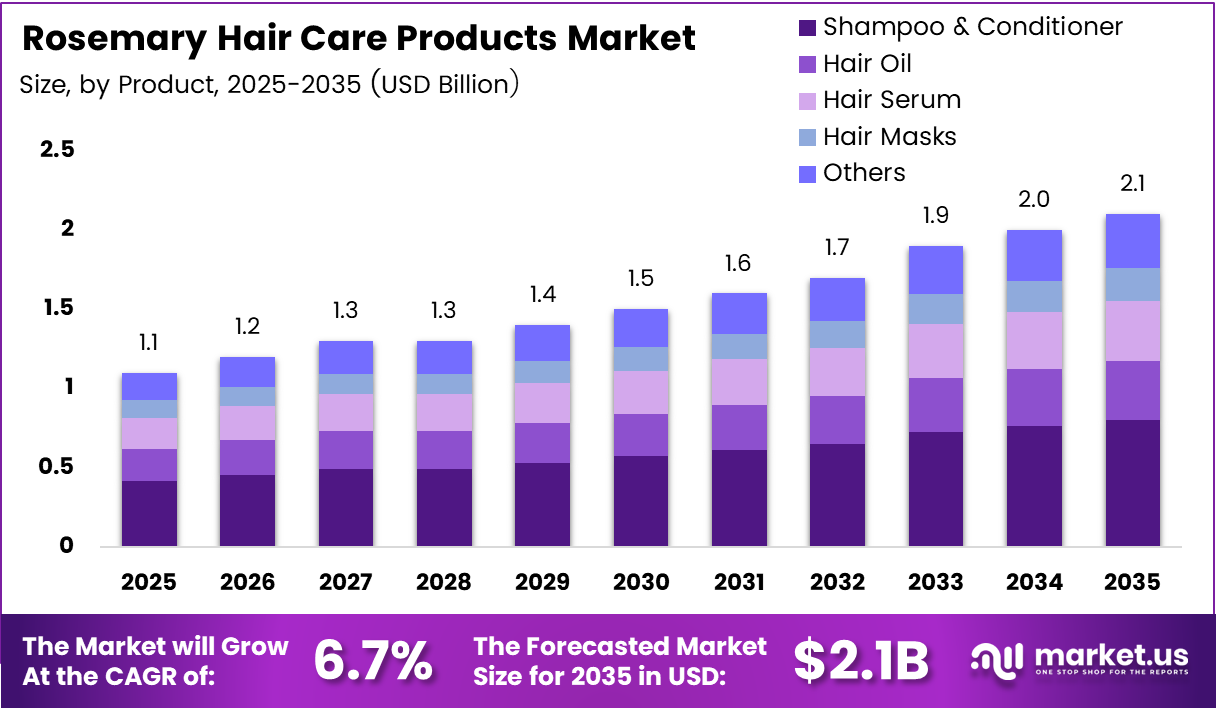

Global Rosemary Hair Care Products Market size is expected to be worth around USD 2.1 Billion by 2035 from USD 1.1 Billion in 2025, growing at a CAGR of 6.7% during the forecast period 2026 to 2035.

Rosemary hair care products include shampoos, conditioners, hair oils, serums, and masks formulated with rosemary extract as a primary botanical ingredient. Consumers choose these products for scalp stimulation, hair loss reduction, and natural alternatives to synthetic formulations. The category sits at the intersection of personal care and wellness, where buyer intent shifts from cosmetic to therapeutic.

The 6.7% CAGR reflects a structural shift in consumer behavior — buyers actively replace synthetic hair treatments with botanical alternatives backed by clinical evidence. This pace of adoption signals that rosemary-based hair care has moved beyond a niche segment into mainstream retail consideration, compressing the window for late-market entrants.

Women represent the dominant buyer group at 67.2% of end-use share, reflecting their higher engagement with scalp health and preventive hair care routines. However, the men’s segment presents an underpenetrated opportunity, particularly as hair loss awareness campaigns target male consumers through digital channels and dermatology-adjacent marketing.

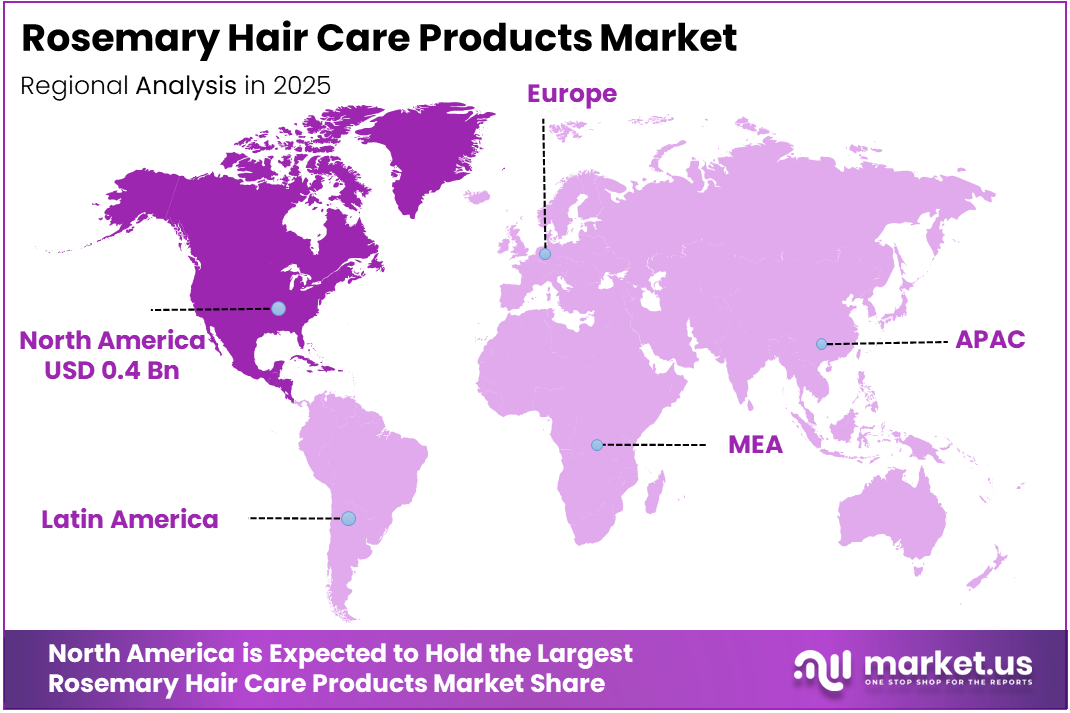

North America leads the market with a 43.7% share, valued at USD 0.4 Billion. Mature retail infrastructure, high consumer willingness to pay for premium botanical products, and established e-commerce penetration position the region as the primary revenue generator. Conditions forming in Western Europe and Asia Pacific suggest a geographic expansion sequence already underway.

Shampoo and conditioner products capture 36.7% of the product segment, confirming that daily-use formats drive the highest volume. This dominance signals that product developers prioritizing mass-market rinse-off formats will capture faster adoption than those entering with premium leave-in or treatment-specific SKUs.

According to a 2025 double-blind, randomized, placebo-controlled clinical trial published in PMC, rosemary-lavender oil increased hair growth rate by 57.73% from baseline after 90 days. This figure matters because clinical validation at this level removes the primary buyer objection — efficacy skepticism — and directly supports premium pricing strategies across the product portfolio.

According to the same PMC study, rosemary-lavender oil improved hair thickness by 68.70% from baseline after 90 days, with a 2.57-fold improvement versus coconut oil placebo. For brands, this quantified outcome converts consumer interest into purchase confidence, reducing reliance on influencer marketing alone and enabling evidence-led product positioning in both retail and clinical channels.

Key Takeaways

- The global Rosemary Hair Care Products Market is valued at USD 1.1 Billion in 2025 and forecast to reach USD 2.1 Billion by 2035.

- The market advances at a CAGR of 6.7% during the forecast period 2026 to 2035.

- By product, Shampoo and Conditioner leads with a 36.7% market share in 2025.

- By end-use, Women holds the dominant position with a 67.2% share of the market.

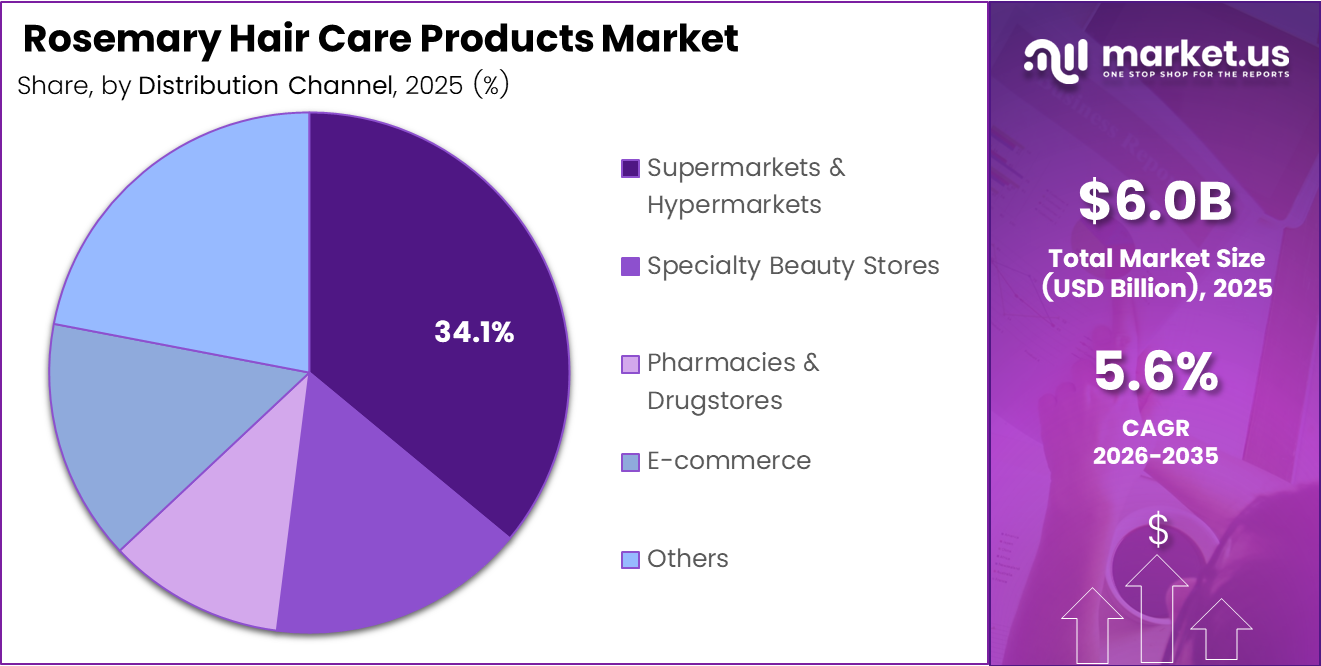

- By distribution channel, Supermarkets and Hypermarkets account for 34.1% of total distribution.

- North America dominates the regional landscape with a 43.7% share, valued at USD 0.4 Billion.

Product Analysis

Shampoo and Conditioner dominates with 36.7% due to daily-use format and mass retail availability.

In 2025, Shampoo and Conditioner held a dominant market position in the By Product segment of the Rosemary Hair Care Products Market, with a 36.7% share. Daily usage frequency makes this format the highest-volume entry point for rosemary-based formulations. Brands securing shelf space in this category capture repeat purchase cycles unavailable to treatment-specific formats like serums or masks.

Hair Oil serves as the therapeutic anchor of the rosemary hair care portfolio. Consumers apply it for targeted scalp treatment, positioning it as a higher-engagement product with stronger brand loyalty potential. However, its usage frequency is lower than rinse-off formats, limiting volume velocity despite strong unit economics and premium pricing acceptance.

Hair Serum carries the highest margin potential within the rosemary product lineup. Buyers purchase serums for concentrated, fast-absorbing delivery of active ingredients, making them the natural format for clinical-grade rosemary extract formulations. Additionally, serums attract urban, ingredient-conscious consumers who already read formulation labels and compare rosmarinic acid concentrations.

Hair Masks differentiate through deep-conditioning and scalp-detox positioning. Consumers use them less frequently than shampoos but invest more per session, supporting premium SKU development. Consequently, hair masks offer brands a pathway to higher average order values, particularly in e-commerce bundles combining weekly treatment routines with daily-use products.

Others in the product category encompass leave-in treatments, scalp scrubs, and tonic sprays containing rosemary extract. These formats serve niche buyer needs — post-wash care and targeted regrowth support — and attract early adopters. Therefore, they function as innovation incubators where new delivery mechanisms can be tested before wider retail rollout.

End-use Analysis

Women dominates with 67.2% due to higher engagement in preventive scalp health routines.

In 2025, Women held a dominant market position in the By End-use segment of the Rosemary Hair Care Products Market, with a 67.2% share. Female consumers drive purchase decisions across all product formats — from daily shampoos to intensive hair masks. Their preference for botanical ingredients with clinical backing makes them the primary audience for rosemary-specific product claims around scalp health and hair density.

Men represent the structurally underpenetrated end-use segment in this market. Male hair loss concerns — particularly androgenetic alopecia — create a high-intent buyer base that rosemary extract directly addresses through follicle stimulation. Moreover, as dermatology-adjacent marketing normalizes hair wellness for men, this segment offers one of the clearest volume expansion opportunities for brands willing to reformulate and reposition existing SKUs.

Distribution Channel Analysis

Supermarkets and Hypermarkets dominate with 34.1% due to high foot traffic and established personal care shelf space.

In 2025, Supermarkets and Hypermarkets held a dominant market position in the By Distribution Channel segment of the Rosemary Hair Care Products Market, with a 34.1% share. Physical retail visibility drives impulse discovery for rosemary hair care brands without established name recognition. In February 2024, HASK Beauty launched its Tea Tree Oil and Rosemary Scalp Relief Serum as part of the Soothe+ collection, reflecting how brands use mass retail channels to introduce new scalp-focused formulations to broad consumer audiences.

Specialty Beauty Stores serve as the primary channel for premium and ingredient-led rosemary formulations. Buyers visiting specialty retail demonstrate higher purchase intent and category knowledge, making this channel the optimal environment for hero SKUs with clinical claims and premium price points. Consequently, brands entering through specialty channels build brand equity faster than through mass-market distribution.

Pharmacies and Drugstores position rosemary hair care products within the therapeutic and dermatological aisle, lending clinical credibility to botanical formulations. This channel attracts buyers actively managing hair loss or scalp conditions — a high-value, repeat-purchase cohort. Additionally, pharmacist recommendations function as informal endorsements that accelerate trial among skeptical first-time users.

E-commerce enables brands to reach ingredient-conscious buyers beyond geographic retail constraints. Online platforms support detailed product education, clinical data sharing, and subscription models — all of which extend customer lifetime value. Therefore, e-commerce functions not just as a distribution channel but as a brand-building environment where rosmarinic acid percentages and trial data convert browsers into loyal buyers.

Others in distribution include direct-to-consumer brand websites, salon professional channels, and subscription beauty box services. These formats allow brands to control pricing, narrative, and formulation messaging without retail margin compression. Moreover, salon channels provide professional endorsement that transfers authority to consumer-facing product lines.

Key Market Segments

By Product

- Shampoo & Conditioner

- Hair Oil

- Hair Serum

- Hair Masks

- Others

By End-use

- Women

- Men

By Distribution Channel

- Supermarkets & Hypermarkets

- Specialty Beauty Stores

- Pharmacies & Drugstores

- E-commerce

- Others

Drivers

Clinical Evidence Behind Rosemary Extract Accelerates Consumer Shift Toward Botanical Hair Care

Consumer preference for botanical and natural hair care ingredients now rests on published clinical outcomes rather than marketing claims alone. According to a 2025 study published in the journal IPHR, 5% standardized rosemary extract produced a 2.7-fold increase in hair follicle length versus a testosterone-induced alopecia control group. This level of clinical documentation converts skeptical buyers into active purchasers and supports premium price positioning across the rosemary product range.

Scalp health awareness fuels a secondary but equally important driver. Buyers no longer treat dandruff and scalp sensitivity as separate concerns from hair growth — they seek formulations that address both simultaneously. In February 2024, HASK Beauty launched its Tea Tree Oil and Rosemary Scalp Relief Serum designed to balance scalp hydration and reduce irritation, reflecting how brands now engineer multi-benefit products around this converging buyer demand.

Herbal and organic personal care products now occupy dedicated sections in mainstream retail channels, creating physical shelf space that did not exist for botanical hair care five years ago. Additionally, e-commerce platforms enable niche rosemary brands to reach ingredient-literate consumers directly, bypassing traditional distribution gatekeepers. Therefore, distribution access and retail legitimacy now reinforce each other, compressing the time between product launch and mass-market penetration.

Restraints

Formulation Costs and Labeling Inconsistencies Limit Market Scalability for Rosemary Hair Care Brands

Premium rosemary-infused hair care products carry significantly higher formulation costs than synthetic alternatives. According to a 2025 alopecia study published in IPHR, effective rosemary extract formulations require standardized concentrations — with the study testing 1%, 3%, and 5% concentrations containing 0.605 g% rosmarinic acid. Maintaining this level of ingredient standardization at commercial scale raises production costs, which brands either absorb or transfer to consumers through higher retail prices.

Higher price points narrow the addressable buyer base. In markets where disposable income limits willingness to pay for premium botanical formulations, mass-market adoption stalls. Moreover, price-sensitive buyers default to synthetic hair care alternatives that deliver acceptable results at a fraction of the cost, preventing rosemary hair care brands from achieving the volume scale needed to reduce per-unit manufacturing costs.

Limited standardization in natural ingredient labeling creates a separate but compounding challenge. Without universally recognized certification frameworks for rosemary extract purity and concentration, buyers cannot reliably compare products across brands. Consequently, brand trust becomes the primary purchase driver rather than ingredient efficacy — a condition that protects established players but restricts smaller, formulation-led brands from gaining retail credibility based on product quality alone.

Growth Factors

Customized Serums, Professional Partnerships, and Sustainable Packaging Open New Revenue Streams

Customized rosemary hair serums for targeted concerns — including alopecia, postpartum hair loss, and thinning — represent a high-margin growth pathway. According to a 2025 clinical trial published on novobliss.in, rosemary-castor oil increased the anagen-to-telogen ratio by 246.12% from baseline after 90 days. This shift in hair growth phase duration signals that condition-specific formulations can deliver measurable, communicable outcomes — precisely what direct-to-consumer brands need to justify premium pricing and subscription models.

Strategic partnerships with salons and professional hair treatment chains offer rosemary brands a distribution and endorsement channel simultaneously. Salon professionals carry formulation authority with consumers, and their recommendation accelerates trial among buyers who would otherwise spend months researching before purchasing. Additionally, professional-grade rosemary product lines create a premium tier that sustains margins even as mass-market competition intensifies.

Eco-friendly and sustainable packaging solutions address an emerging purchase criterion among the core buyer demographic — health-conscious, environmentally aware consumers already selecting botanical over synthetic formulations. Furthermore, rosemary hair care brands that localize products for emerging markets — adjusting fragrance profiles, pricing, and application formats — can capture first-mover advantages in regions where botanical hair care penetration remains below developed market levels.

Emerging Trends

Influencer Campaigns, Multi-Functional Formats, and Subscription Models Reshape Rosemary Hair Care Distribution

Influencer-led hair wellness campaigns have become the primary discovery channel for rosemary hair care products among younger consumers. According to a 2025 clinical trial published by PMC, rosemary-lavender oil increased hair density by 32.21% from baseline after 90 days — a figure that translates directly into shareable, before-and-after content formats. Brands that equip influencers with clinical data alongside product samples convert organic reach into purchase intent more effectively than those relying on aesthetic content alone.

Multi-functional hair care solutions combining rosemary extract with complementary actives — niacinamide, ginger, perilla — are displacing single-ingredient products across both mass and premium tiers. In July 2025, Dancoly launched its Rosemary Activating Regrowth Essence combining rosemary, ginger, and perilla extracts to target scalp microcirculation and follicle nutrient absorption simultaneously. Consequently, buyers now expect rosemary products to address multiple hair concerns within a single application step.

Subscription beauty boxes have emerged as a structured trial channel for rosemary hair care brands. These boxes give emerging brands access to ingredient-curious consumers without requiring full retail distribution commitments. Moreover, small-batch and DIY rosemary hair care brands are gaining buyer trust through transparency in sourcing and formulation — a direct response to the certification gaps identified as a market restraint — positioning authenticity as a competitive differentiator.

Regional Analysis

North America Dominates the Rosemary Hair Care Products Market with a Market Share of 43.7%, Valued at USD 0.4 Billion

North America leads the global Rosemary Hair Care Products Market with a 43.7% share, valued at USD 0.4 Billion. The region benefits from a mature specialty beauty retail network, high consumer willingness to pay for clinically backed botanical products, and established e-commerce infrastructure that supports direct-to-consumer rosemary brands. Early adoption of ingredient-transparency labeling standards further reinforces buyer confidence in premium formulations.

Europe Rosemary Hair Care Products Market Trends

Europe represents the second-most-developed market for rosemary hair care, supported by the region’s longstanding regulatory emphasis on cosmetic ingredient safety and natural formulation standards. Germany, France, and the UK drive premium botanical hair care adoption through specialty retail and pharmacy channels. Additionally, European consumers show strong affinity for provenance-led marketing — a structural advantage for rosemary brands with Mediterranean sourcing credentials.

Asia Pacific Rosemary Hair Care Products Market Trends

Asia Pacific presents the highest volume expansion opportunity, driven by a large and rapidly urbanizing middle-class consumer base with growing interest in scalp health and hair wellness. China, Japan, South Korea, and India represent distinct buyer profiles — from K-beauty-influenced ingredient literates to Ayurvedic-adjacent herbal care adopters. Therefore, brands entering Asia Pacific with localized formulations and regional distribution partnerships stand to capture disproportionate share.

Latin America Rosemary Hair Care Products Market Trends

Latin America offers a structurally underpenetrated market for rosemary hair care, with Brazil and Mexico as the primary revenue contributors. Consumer preference for herbal and botanical personal care products aligns naturally with rosemary-based formulations, but price sensitivity limits mass penetration of premium-priced SKUs. Consequently, brands that introduce accessible entry-level rosemary products through supermarket channels can build category awareness before scaling premium offerings.

Middle East and Africa Rosemary Hair Care Products Market Trends

The Middle East and Africa market for rosemary hair care operates at an early adoption stage, with GCC countries showing the strongest purchase power for premium botanical personal care. Consumers across the GCC prioritize hair health and scalp conditioning — categories where rosemary extract’s therapeutic positioning aligns well. Moreover, the growth of organized retail and cross-border e-commerce in the region creates new access points for international rosemary hair care brands.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

L’Oréal S.A. holds a structural advantage in the rosemary hair care market through its dual capability in formulation R&D and global retail distribution. The company’s access to dermatological research infrastructure allows it to substantiate botanical ingredient claims at a scale that independent brands cannot replicate. This positions L’Oréal to capture premium buyers who require clinical evidence without sacrificing mass-market retail presence.

Unilever PLC leverages its established consumer trust in personal care and its multi-brand architecture to introduce rosemary-based formulations across different price tiers simultaneously. Its manufacturing scale reduces per-unit ingredient costs, enabling it to bring standardized rosemary extract products to mass retail at price points that challenge premium-only competitors. Additionally, Unilever’s sustainability commitments align with the eco-conscious buyer profile most likely to adopt botanical hair care.

The Estée Lauder Companies Inc. approaches the rosemary hair care market from a prestige positioning standpoint, targeting high-income buyers who expect clinical-grade ingredient sourcing and efficacy documentation. Their distribution model — centered on department stores, specialty beauty, and direct-to-consumer channels — insulates them from mass-market price competition. Consequently, Estée Lauder captures the highest-margin buyer segment while reinforcing premium brand equity across their hair care portfolio.

Moroccanoil built its brand identity around oil-based hair care — a format that directly aligns with rosemary oil formulations gaining clinical validation. This pre-existing consumer association with botanical oil treatments gives Moroccanoil a credibility advantage when introducing or expanding rosemary-specific SKUs. Moreover, its strong presence in professional salon channels provides a differentiated distribution pathway that amplifies both brand trust and product trial rates among high-engagement buyers.

Key Players

- L’Oréal S.A.

- Unilever PLC

- The Estée Lauder Companies Inc.

- Moroccanoil

- Avalon Organics

- As I Am

- John Masters Organics Inc.

- Renpure Ltd

Recent Developments

- January 2024 — Nykaa Naturals expanded its product portfolio by launching a sulphate-free haircare range featuring rosemary and naturally derived niacinamide. The collection included a shampoo priced at Rs 399 and a hair mask at Rs 599, targeting ingredient-conscious consumers in the affordable premium segment.

- May 2024 — Sky Organics launched five new organic hair care innovations at Walmart and Walmart.com, including the Organic Amla and Rosemary Oil priced at USD 10.48. The scalp oil targets dry and brittle hair by nourishing from the root while supporting shine and scalp balance, expanding accessible rosemary hair care through mass retail distribution.

Report Scope

Report Features Description Market Value (2025) USD 1.1 Billion Forecast Revenue (2035) USD 2.1 Billion CAGR (2026-2035) 6.7% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product (Shampoo & Conditioner, Hair Oil, Hair Serum, Hair Masks, Others), By End-use (Women, Men), By Distribution Channel (Supermarkets & Hypermarkets, Specialty Beauty Stores, Pharmacies & Drugstores, E-commerce, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape L’Oréal S.A., Unilever PLC, The Estée Lauder Companies Inc., Moroccanoil, Avalon Organics, As I Am, John Masters Organics Inc., Renpure Ltd Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Rosemary Hair Care Products MarketPublished date: Mar 2026add_shopping_cartBuy Now get_appDownload Sample

Rosemary Hair Care Products MarketPublished date: Mar 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- L'Oréal S.A.

- Unilever PLC

- The Estée Lauder Companies Inc.

- Moroccanoil

- Avalon Organics

- As I Am

- John Masters Organics Inc.

- Renpure Ltd

Our Clients

- 182639

- Mar 2026