Global Reconstituted Milk Market Size, Share, And Industry Analysis Report By Source (Skimmed Milk, Whole Milk), By Type (Lactose Free, Organic Milk, Flavored Milk), By Application (Dairy Products Manufacturing, Food and Beverage, Dietary and Nutritional Supplements, Cosmetics and Personal Care, Infant Formula), By Distribution Channel (Supermarkets and Hypermarkets, Online Sales, Wholesale Stores), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: March 2026

- Report ID: 182436

- Number of Pages: 218

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

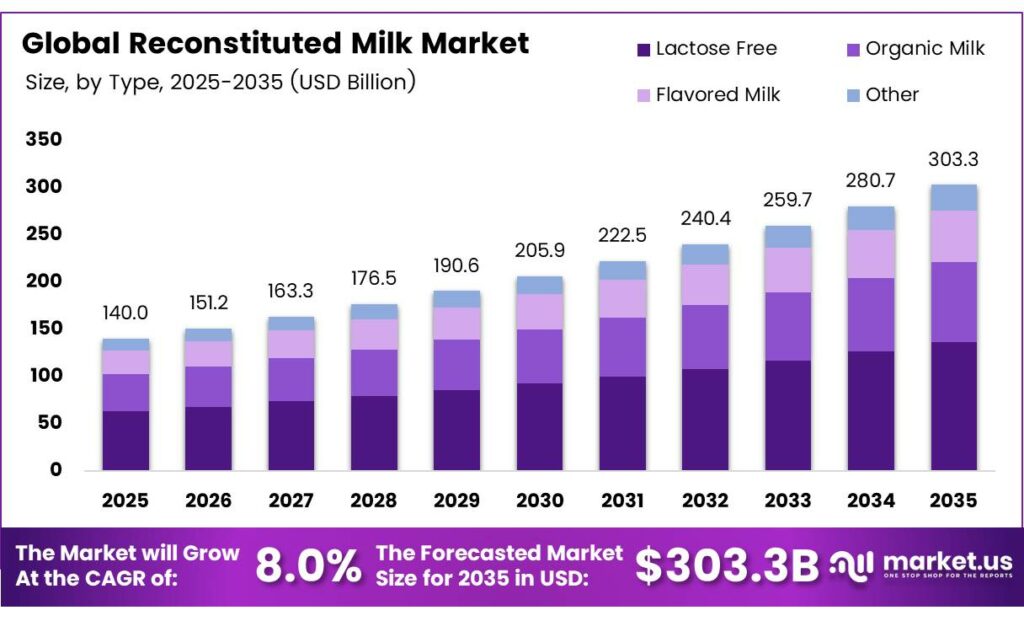

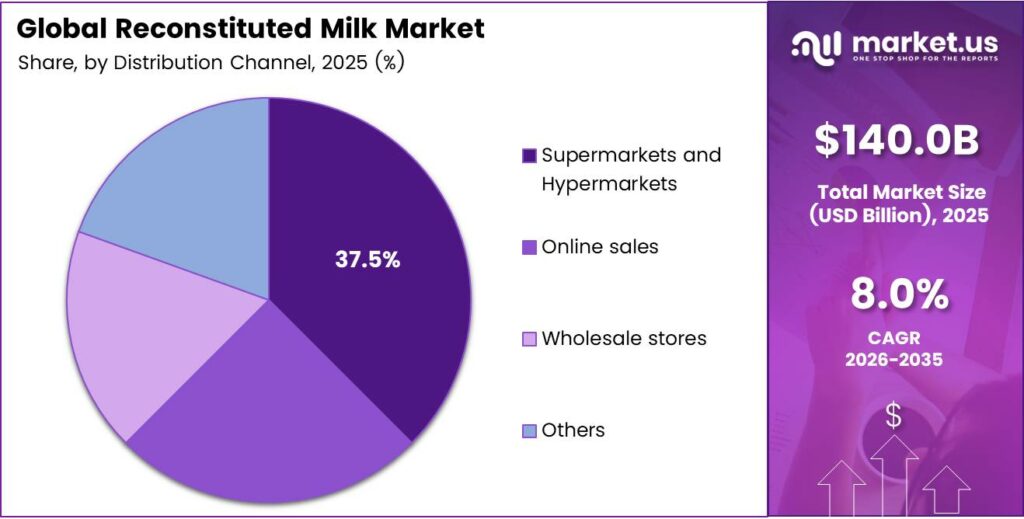

The Global Reconstituted Milk Market size is expected to be worth around USD 303.3 billion by 2035 from USD 140.0 billion in 2025, growing at a CAGR of 8.0% during the forecast period 2026 to 2035.

The reconstituted milk market involves the production and distribution of liquid milk derived by blending dried milk powders, primarily skim milk powder and whole milk powder, with water. This process allows dairy manufacturers to produce consistent, shelf-stable, and cost-effective milk products in regions where fresh milk supply is limited or seasonally constrained. The market serves a broad range of industries, including food processing, infant formula, and foodservice.

Regulatory frameworks across key dairy markets continue to shape reconstituted milk usage. Authorities in major consuming nations have introduced standards governing labeling, compositional requirements, and production protocols. These regulations ensure product quality while also defining the boundaries within which processors can use reconstituted milk in finished dairy goods.

Algeria’s annual milk consumption need was estimated at 4.5 MMT in 2024, with 55% supplied by domestic production and a 2 MMT shortfall filled by imported milk powder processed into reconstituted milk. This example illustrates the structural reliance many developing nations place on reconstituted dairy to fill domestic gaps.

Pasteurized reconstituted milk in Algeria was sold at a government-fixed price of DZD 25 per liter in 2024, compared to DZD 140 per liter for UHT milk. This pricing gap reflects the affordability advantage reconstituted milk offers to price-sensitive consumers and underscores its relevance in government-supported nutrition programs globally.

Taiwan imported 26,429 MT of frozen milk in 2024, and when reconstituted, this volume affected approximately 100,000 MT of the liquid milk market, pushing total milk demand above 600,000 MT. This data highlights how reconstituted dairy quietly underpins liquid milk availability even in moderately developed dairy markets.

Key Takeaways

- The Global Reconstituted Milk Market was valued at USD 140.0 billion in 2025 and is forecast to reach USD 303.3 billion by 2035, growing at a CAGR of 8.0%.

- Skimmed Milk held the largest share at 63.7% in 2025.

- Lactose-free was the dominant sub-segment with a 35.6% share in 2025.

- Dairy Products Manufacturing led the market with a 41.2% share in 2025.

- Supermarkets and Hypermarkets captured the highest share at 37.5% in 2025.

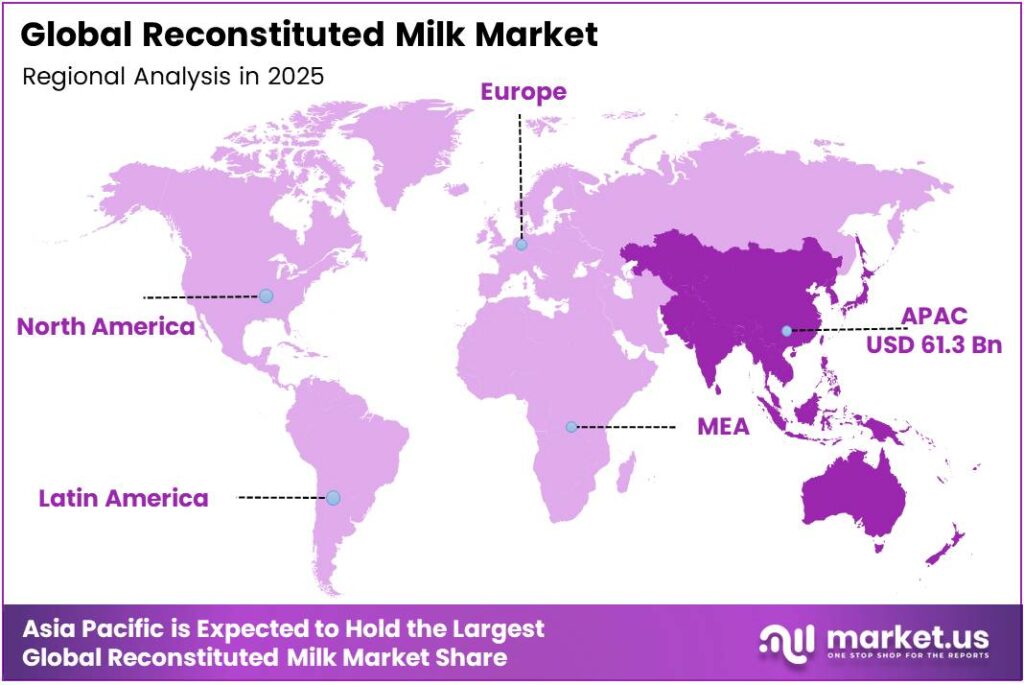

- Asia Pacific dominated the regional landscape with a 43.8% share, valued at USD 61.3 billion in 2025.

By Source Analysis

Skimmed Milk dominates with 63.7% due to its cost efficiency and widespread use in reconstitution-based dairy manufacturing.

In 2025, Skimmed Milk held a dominant market position in the By Source segment of the Reconstituted Milk Market, with a 63.7% share. Processors prefer skimmed milk powder for reconstitution because it offers a lower fat content, extended shelf life, and competitive procurement cost. Moreover, its widespread availability from major dairy-exporting nations makes it the default input material for large-scale reconstituted dairy operations.

Whole Milk powder serves as a complementary source in reconstitution, particularly in markets requiring full-fat dairy products such as infant formula and premium beverage applications. Consequently, whole milk powder demand remains steady across the Asia Pacific and Middle Eastern markets, where fat content and flavor profiles carry greater consumer importance in finished reconstituted products.

By Type Analysis

Lactose-free reconstituted milk dominates with 35.6% due to rising lactose intolerance awareness and health-driven consumer preferences.

In 2025, Lactose Free held a dominant market position in the By Type segment of the Reconstituted Milk Market, with a 35.6% share. Growing consumer awareness of digestive health and lactose intolerance has accelerated demand for lactose-free variants. Additionally, foodservice operators and institutional buyers increasingly specify lactose-free reconstituted milk to accommodate diverse dietary needs across their customer base.

Organic Milk reconstituted variants attract health-conscious buyers in premium retail and specialty food segments. Processors sourcing certified organic milk powders command higher margins, though supply constraints limit broad market penetration. Therefore, organic reconstituted milk remains a niche but fast-growing category within developed markets, particularly in North America and Western Europe.

By Application Analysis

Dairy Products Manufacturing dominates with 41.2% due to its extensive use of reconstituted milk as a core input across multiple processed dairy goods.

In 2025, Dairy Products Manufacturing held a dominant market position in the By Application segment of the Reconstituted Milk Market, with a 41.2% share. Large-scale dairy processors use reconstituted milk as a reliable, cost-controlled ingredient in cheese, yogurt, butter, and flavored dairy beverages. Moreover, reconstitution enables consistent product quality regardless of seasonal fluctuations in fresh milk availability.

Food and Beverage applications form the second-largest demand category, driven by bakery, confectionery, and beverage manufacturers that require stable milk solids inputs. Reconstituted milk delivers standardized protein and fat levels. Therefore, food producers across emerging markets prefer it as a scalable and affordable substitute for fresh liquid milk in continuous processing operations.

By Distribution Channel Analysis

Supermarkets and Hypermarkets dominate with 37.5% due to their extensive reach, product variety, and consumer trust in organized retail environments.

In 2025, Supermarkets and Hypermarkets held a dominant market position in the By Distribution Channel segment of the Reconstituted Milk Market, with a 37.5% share. These retail formats provide consumers with easy access to a wide range of reconstituted milk brands and packaging formats. Additionally, promotional activities and in-store visibility in hypermarkets drive significant impulse purchasing of packaged reconstituted dairy products.

Online Sales channels have grown rapidly as e-commerce platforms expand grocery delivery capabilities in urban markets. Consumers increasingly purchase reconstituted milk products through digital platforms for home delivery convenience. Consequently, dairy brands have invested in direct-to-consumer online channels and third-party marketplace listings to capture digitally active shoppers in the Asia Pacific and North America.

Wholesale Stores serve institutional buyers, catering companies, and small food businesses that purchase reconstituted milk in bulk quantities. This channel is particularly important in price-sensitive markets where cost efficiency drives procurement decisions. Therefore, wholesale distribution remains a significant channel for large-format packaging of milk powder and reconstituted dairy products destined for commercial end users.

Key Market Segments

By Source

- Skimmed Milk

- Whole Milk

By Type

- Lactose Free

- Organic Milk

- Flavored Milk

- Other

By Application

- Dairy Products Manufacturing

- Food and Beverage

- Dietary and Nutritional Supplements

- Cosmetics and Personal Care

- Infant Formula

- Other

By Distribution Channel

- Supermarkets and Hypermarkets

- Online Sales

- Wholesale Stores

- Others

Emerging Trends

Whole Milk Powder Export Share Declines as Dairy Producers Pivot to Higher-Margin Products

Whole milk powder’s share within total global dairy exports is declining as producers prioritize cheese and butter manufacturing, which deliver stronger profit margins. This shift compresses reconstituted milk powder availability in certain origin markets. The Philippines’ skim milk powder imports were forecast at 175,000 MT in 2026, with some consumers using imported SMP directly as reconstituted liquid milk, reflecting regional adaptation to changing powder trade flows.

Oxidative Stability and Supply Chain Integrity Shape Next-Generation Reconstituted Dairy Standards

Dairy processors are investing in oxidative stability technologies to preserve sensory quality during powder storage and reconstitution. Simultaneously, regulatory bodies intensify supply chain fraud prevention measures that directly affect reconstituted product labeling and consumer trust. Additionally, MENA accounted for 22% of global NFDM/SMP trade in 2025, underscoring this region’s continued dependence on powder-based reconstitution and its sensitivity to supply chain compliance requirements.

Drivers

Foodservice Sector Accelerates Reconstituted Milk Adoption for Cost Control and Formulation Flexibility

The global foodservice and hospitality sector is increasingly replacing fresh milk with reconstituted variants to manage input costs and ensure formulation consistency. Hotels, quick-service restaurants, and catering companies value reconstituted milk for its predictable cost structure and extended shelf life. Mexico’s skimmed milk powder consumption was forecast at 279,000 MT in 2025, up 11%, driven by processing demand and reconstituted milk use in a government-supported social program.

Expanding Milk Powder Trade Strengthens Reconstitution Supply Across Deficient Dairy Regions

Government subsidies stabilizing whole milk powder output in major dairy export economies directly support reconstitution supply chains. New Zealand produced 1,420 thousand MT of whole milk powder in 2024 and was forecast to produce 1,400 thousand MT in 2026, making it the largest listed WMP origin globally. This steady export volume underpins reliable powder access for reconstituted dairy manufacturers worldwide.

Restraints

Processor Preference for Fresh Milk Limits Reconstituted Dairy Use in Premium Product Categories

Premium beverage and ice cream manufacturers increasingly shift toward fresh liquid milk to achieve superior taste, texture, and consumer perception in high-value products. This preference directly reduces the addressable market for reconstituted milk in developed economies. Consequently, processors competing in premium dairy segments face commercial pressure to reformulate products away from reconstituted dairy inputs, constraining volume growth in these higher-margin applications.

Amended National Standards Restrict Reconstituted Milk in Sterilized Dairy Products

Regulatory changes in key markets have directly reduced reconstituted milk volumes in certain processed dairy categories. China’s amended sterilized milk standard took effect, and prohibited reconstituted milk in UHT “pure milk,” while 2026 whole milk powder imports were forecast to remain stable at 425,000 tons. This regulatory restriction illustrates how national dairy standards can materially alter demand for reconstituted milk within large and strategically important markets.

Growth Factors

Infant Formula and Specialized Nutrition Drive Premium Reconstituted Milk Demand

High-quality imported whole milk powder is gaining targeted use in infant formula and specialized nutritional products, where compositional precision and purity are paramount. Milk protein concentrates also deliver enhanced functional performance in reconstituted dairy formulations targeting health-conscious consumers. Indonesia imported 56,504 MT of whole milk powder in January–August 2025, up from 48,367 MT in the same period of 2024, linked partly to reconstituted milk production growth.

Bubble Tea, Coffee Channels, and Global Powder Trade Expand Reconstituted Dairy Applications

Reconstituted milk is gaining rapid integration into bubble tea chains, specialty coffee shops, and custom foodservice channels, creating new demand segments beyond traditional dairy processing. Global NFDM/SMP trade reached 2.227 million MT in 2025, up 1% from 2024, providing a direct indicator of expanding powder availability that supports reconstitution-based dairy manufacturing across multiple end-use channels globally.

Regional Analysis

Asia Pacific Dominates the Reconstituted Milk Market with a Market Share of 43.8%, Valued at USD 61.3 Billion

Asia Pacific leads the global reconstituted milk market, holding a 43.8% share valued at USD 61.3 billion in 2025. The region’s dominance reflects high population density, limited fresh milk infrastructure in developing economies, and strong government support for dairy trade. Countries including China, Indonesia, and the Philippines rely heavily on powder-based reconstitution to meet their large and growing liquid milk demand.

North America maintains a mature but steady reconstituted milk market, primarily driven by industrial dairy manufacturing and foodservice procurement. The United States plays a dual role as both a major milk powder producer and a consumer of reconstituted dairy ingredients. However, consumer preference for fresh milk in retail channels limits the broader adoption of reconstituted variants in the region’s premium beverage segment.

Europe represents a significant supplier of milk powder inputs that feed global reconstitution supply chains, with the EU producing substantial volumes of both nonfat dry milk and whole milk powder annually. Domestically, reconstituted milk usage in Europe remains limited, as regulatory frameworks and consumer expectations favor fresh dairy products. Nevertheless, European processors actively serve export markets where reconstituted dairy manufacturing thrives.

The Middle East and Africa region depends heavily on reconstituted milk to address chronic fresh milk deficits caused by arid climates and underdeveloped domestic dairy sectors. Countries across North Africa and the Gulf region import large volumes of milk powder and convert it into reconstituted dairy products for direct consumer use and food manufacturing. Consequently, this region presents significant long-term growth potential for global powder exporters and reconstitution technology providers.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Nestlé S.A. operates as one of the world’s most diversified dairy and nutrition companies, with a strong presence across reconstituted milk ingredient sourcing and finished product manufacturing. The company leverages its global procurement network to maintain consistent powder supply chains. Moreover, Nestlé’s investment in nutritional science and product innovation positions it as a leading formulator of reconstituted dairy-based beverages and infant nutrition products worldwide.

Lactalis holds a commanding position in global dairy markets as the world’s largest dairy group, with operations spanning fluid milk, cheese, and dairy ingredients across multiple continents. The company’s extensive manufacturing and distribution infrastructure enables it to supply reconstituted dairy products to foodservice, retail, and industrial buyers at scale. Additionally, Lactalis’s broad geographic footprint supports consistent powder sourcing from major dairy export regions to serve high-demand markets.

Fonterra serves as a cornerstone supplier of whole milk powder and skim milk powder that underpin global reconstituted milk production. The New Zealand-based cooperative operates one of the world’s largest dairy ingredient export networks, supplying processors across Asia, the Middle East, and Latin America. Consequently, Fonterra’s production scale and supply chain capabilities make it a critical upstream partner for reconstituted dairy manufacturers globally.

Dairy Farmers of America operates as one of the largest dairy cooperatives in the United States, supplying high-quality milk solids and dairy ingredients to processors engaged in reconstituted milk manufacturing. The cooperative’s robust farmer network ensures reliable raw material volumes across processing seasons. Furthermore, its investment in value-added dairy ingredient production strengthens its role as a strategic supplier to both domestic and international reconstituted dairy customers.

Top Key Players in the Market

- Nestle S.A.

- Lactalis

- Fonterra

- Dairy Farmers of America

- Arla Foods

- Saputo

- DMK Group

- Schreiber Foods

- Mengniu Dairy

- Meiji Holdings

Recent Developments

- In March 2025, Nestlé S.A. reconstituted the milk sector (primarily via milk powder products like NIDO, which is reconstituted by adding water) center on brand updates, capacity expansions, and supply-chain challenges with powdered dairy ingredients. Nestlé Ghana Ltd. launched redesigned packaging for its NIDO full-cream milk powder brand, using easier-to-recycle plastic while maintaining nutritional focus for families.

- In May 2025, Lactalis has been active in milk powder launches and major acquisitions that expand its footprint in consumer dairy (including powdered milk products used for reconstitution). Lactalis Malaysia launched PRIDE Family Milk Powder, a new, affordable, nutrient-fortified product (high in calcium, vitamin D, and magnesium) targeted at Malaysian families to address bone health gaps.

Report Scope

Report Features Description Market Value (2025) USD 140.0 Billion Forecast Revenue (2035) USD 303.3 Billion CAGR (2026-2035) 8.0% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Source (Skimmed Milk, Whole Milk), By Type (Lactose Free, Organic Milk, Flavored Milk, Other), By Application (Dairy Products Manufacturing, Food and Beverage, Dietary and Nutritional Supplements, Cosmetics and Personal Care, Infant Formula, Other), By Distribution Channel (Supermarkets and Hypermarkets, Online Sales, Wholesale Stores, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Nestle S.A., Lactalis, Fonterra, Dairy Farmers of America, Arla Foods, Saputo, DMK Group, Schreiber Foods, Mengniu Dairy, Meiji Holdings Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)  Reconstituted Milk MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample

Reconstituted Milk MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Nestle S.A.

- Lactalis

- Fonterra

- Dairy Farmers of America

- Arla Foods

- Saputo

- DMK Group

- Schreiber Foods

- Mengniu Dairy

- Meiji Holdings

Our Clients

- 182436

- March 2026