Global Propane Market Size, Share and Report Analysis By Grade (HD-5, HD-10, Commercial), By Source (Refinery, Associated Gas, Non-Associated Gas, Bio-Propane), By End-user ( Residential, Commercial, Industrial, Transportation, Others), By Distribution Channel (Bulk Delivery, Cylinder Distribution, Autogas Refueling Network, Retail Packaged) , By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2025-2035

- Published date: Mar 2026

- Report ID: 179970

- Number of Pages: 332

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

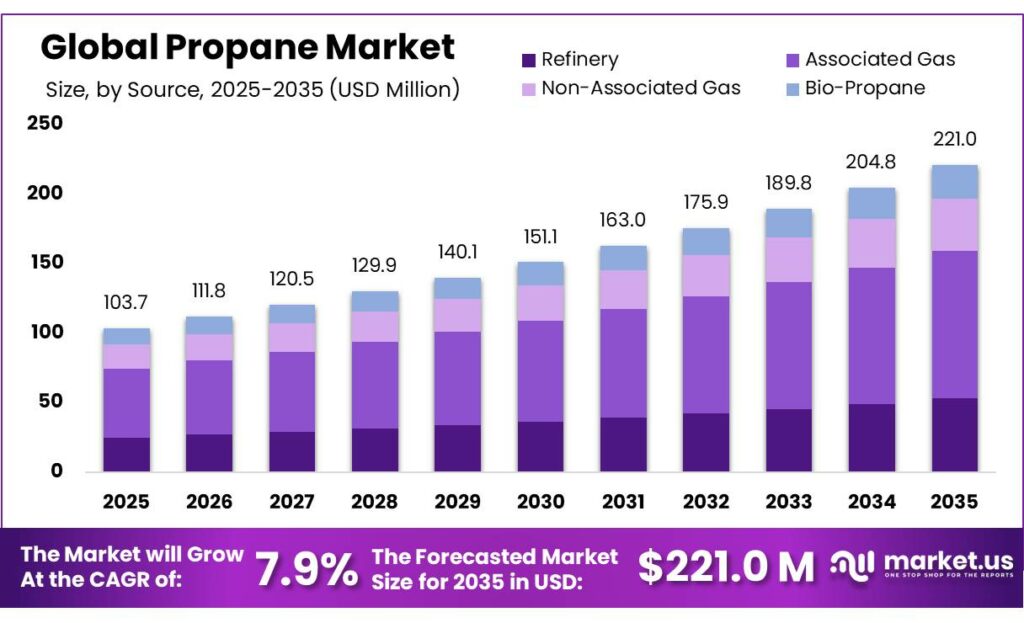

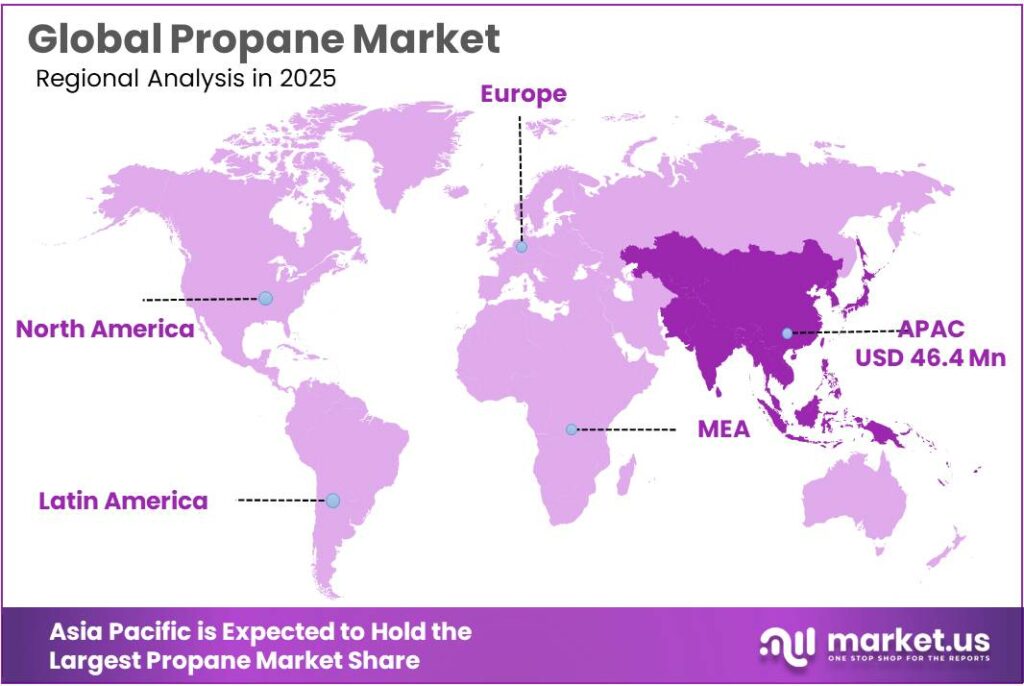

The Global Propane Market is expected to be worth around USD 221.0 Billion by 2035, up from USD 103.7 Billion in 2025, at a CAGR of 7.9% from 2026 to 2035. The Asia Pacific segment maintained 44.8%, supporting a Propane value of USD 46.4 Mn.

Propane, typically traded and consumed as part of liquefied petroleum gas (LPG), is a key link between upstream hydrocarbons and final energy use in homes, farms and industry. Its appeal comes from a high useful energy value of about 20.7 MJ per kilogram of LPG, compared with roughly 16 MJ/kg for air-dried firewood, meaning less fuel is needed for the same heat output.

The industrial scenario is shaped by strong production growth and export capacity, especially from the United States. The U.S. Energy Information Administration reported that U.S. propane production from October 2022 to March 2023 averaged 2.4 million barrels per day, about 14% higher than the previous five-winter average.

- Exports are increasingly central: U.S. propane exports reached a record 1.7 million barrels per day in March 2023, the highest since data collection began in 1973. In 2023, annual U.S. propane exports to Asia increased by 25%, or 190,000 barrels per day, with exports to China alone up 49%, while exports to Europe rose 20% as EU countries reduced reliance on Russian supply.

Several structural drivers support continued industrial use of propane. First, global LPG demand is increasingly shaped by petrochemicals: propane dehydrogenation (PDH) units alone required around 21 million tonnes of propane feedstock in 2022, more than double the level five years earlier, and current investment plans could see PDH propane demand double again by 2025.

In Europe, Liquid Gas Europe notes that nearly 50 million rural households remain off the gas grid, many still dependent on coal or oil for heat, which opens space for propane and renewable LPG as lower-carbon heating options.

- Government and development-finance initiatives further shape propane’s outlook. The IEA notes that delivering universal clean cooking could save up to 1.5 gigatonnes of CO₂-equivalent emissions by 2030, much of it in sub-Saharan Africa, if modern fuels such as LPG replace traditional biomass.

A study for the World LPG Association, drawing on World Bank and IEA data, estimates that if half of all people using solid fuels switched to LPG for cooking, the total economic benefits—from health gains, time savings and productivity—would be around USD 90 billion per year, compared with intervention costs of about USD 13 billion, a benefit-cost ratio close.

Key Takeaways

- Propane Market is expected to be worth around USD 221.0 Billion by 2035, up from USD 103.7 Billion in 2025, at a CAGR of 7.9%.

- Commercial held a dominant market position, capturing more than a 58.3% share.

- Associated Gas held a dominant market position, capturing more than a 48.2% share.

- Residential held a dominant market position, capturing more than a 45.5% share.

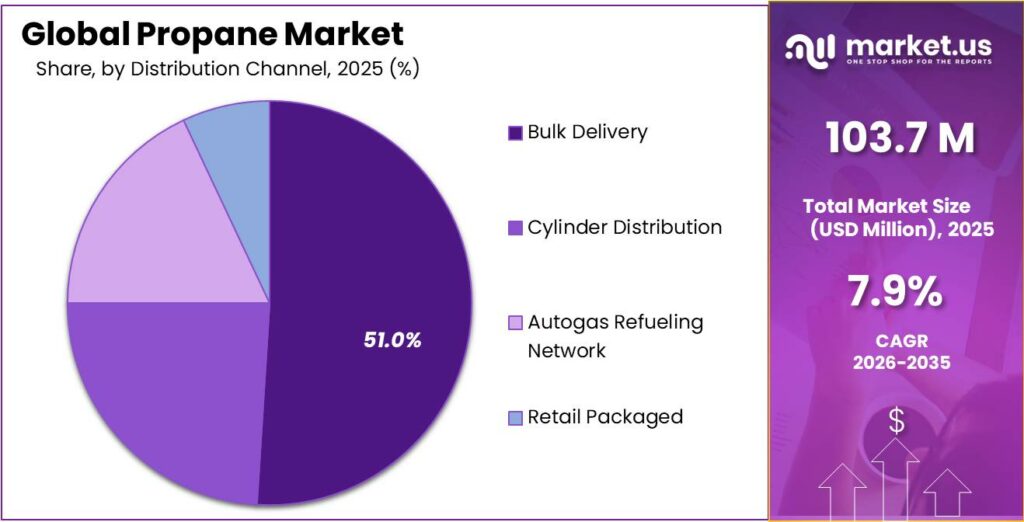

- Bulk Delivery held a dominant market position, capturing more than a 51.7% share.

- Asia Pacific emerged as the dominant regional segment, accounting for 44.8% of total market share, representing around 46.4 Mn.

By Grade Analysis

Commercial Grade Propane leads the market with a strong 58.3% share in 2024

In 2024, Commercial held a dominant market position, capturing more than a 58.3% share, supported by its wide use across restaurants, small industries, food services, hotels, commercial heating systems, and bulk fuel applications. This segment continued to grow steadily through 2025 as more commercial facilities shifted from diesel-based systems to cleaner propane solutions, especially for space heating, hot water generation, backup power, and mid-scale cooking needs.

Many commercial users preferred propane because it delivers consistent heat, works well in off-grid areas, and helps lower operational costs during peak demand seasons. The segment’s strong footprint in 2024 also carried forward into 2025, with rising demand from warehouses, logistics centers, and institutional kitchens. These sectors increasingly turned to propane cylinders and bulk tanks for dependable energy, supporting the commercial grade’s continued leadership.

By Source Analysis

Associated Gas dominates with 48.2% as a reliable propane source

In 2024, Associated Gas held a dominant market position, capturing more than a 48.2% share, driven by its steady recovery from crude oil production and the increasing efficiency of gas-processing units. This source remained the preferred channel for propane extraction because producers could tap into existing oil fields and generate propane without the need for large new installations.

Throughout 2024, stronger upstream activity and improved flare-reduction programs helped raise the availability of associated gas, keeping supply stable for downstream users. By 2025, its role grew even more important as refineries and gas-treating facilities upgraded separation systems to improve yield and reduce losses. Many energy companies continued to rely on associated gas due to its predictable flow, cost advantage, and ability to support both domestic consumption and export demand, ensuring the segment maintained its leadership in the propane market.

By End-user Analysis

Residential propane usage leads the market with a strong 45.5% share

In 2024, Residential held a dominant market position, capturing more than a 45.5% share, mainly because households continue to rely on propane for heating, cooking, hot water systems, and backup power solutions. The segment benefited from colder weather patterns in several regions and the growing number of homes located outside natural gas pipeline networks.

Throughout 2024, many families chose propane as a dependable and safe energy option, especially in rural and semi-urban areas where electricity shortages or grid fluctuations are common. Moving into 2025, the demand stayed firm as more residential users adopted propane-powered heaters, kitchen appliances, and small generators for daily use and emergency preparedness. The ease of delivery, cylinder availability, and consistent performance kept residential consumers strongly engaged in the propane supply chain, securing this segment’s continued leadership.

By Distribution Channel Analysis

Bulk Delivery leads the distribution landscape with a solid 51.7% share

In 2024, Bulk Delivery held a dominant market position, capturing more than a 51.7% share, supported by strong adoption among commercial sites, residential communities, farms, and industrial facilities needing steady and uninterrupted propane supply. This channel remained the preferred choice because it enables large-volume storage, fewer refill cycles, and better cost control for end-users who consume propane regularly.

Throughout 2024, bulk delivery gained further traction as businesses opted for on-site tanks to manage seasonal peaks and reduce dependence on frequent cylinder replacements. By 2025, this model continued to strengthen as more users upgraded to automated tank monitoring and scheduled refills, making propane availability smoother and more predictable. The convenience, scalability, and reliable service network kept bulk delivery at the center of the propane distribution system, supporting its sustained leadership across markets.

Key Market Segments

By Grade

- HD-5

- HD-10

- Commercial

By Source

- Refinery

- Associated Gas

- Non-Associated Gas

- Bio-Propane

By End-user

- Residential

- Commercial

- Industrial

- Transportation

- Others

By Distribution Channel

- Bulk Delivery

- Cylinder Distribution

- Autogas Refueling Network

- Retail Packaged

Emerging Trends

Rising Integration of Propane in Food Cold-Chain Systems Marks a Key Market Trend

A major recent trend in the propane market is its growing integration into cold-chain systems across food production, storage and transport networks. As global food demand rises and countries work to reduce waste and improve food security, reliable energy for refrigeration has become essential. Propane is increasingly chosen because it can support temperature control in areas where electricity access is limited, intermittent, or costly.

- The Food and Agriculture Organization (FAO) estimates that 526 million tonnes of food are lost or wasted each year due to inadequate cold-chain infrastructure and insufficient energy resources for cooling and storage. This staggering figure shows the scale of the challenge, particularly in developing countries where infrastructure gaps are most acute. In the same context, FAO highlights that improving cold-chain systems — including better refrigeration and thermal energy support — could prevent 144 million tonnes of food waste in developing regions alone if modern practices were more broadly applied.

Governments and multilateral agencies are increasingly supporting these propane-linked cold-chain initiatives. As part of Sustainable Development Goal 7 (SDG7) — which aims to ensure universal access to affordable, reliable and modern energy services — many national energy plans now explicitly include support for distributed energy systems that can bridge gaps in rural and peri-urban areas. The United Nations and FAO both promote cleaner energy solutions that help reduce dependence on biomass and diesel while improving food storage outcomes, which opens policy space for propane as a transitional energy source.

The efficiency gains are meaningful. FAO notes that roughly 70% of energy used in agrifood systems is consumed after harvest — in transport, storage, processing and packaging — underscoring the importance of dependable energy sources in these stages.

Drivers

Growing Energy Demand in Food & Agriculture Strongly Lifts Global Propane Consumption

One of the strongest driving forces behind the propane market today is the rapid rise in energy needs across the global food and agriculture chain. This driver has become even more important because the world’s agrifood system relies heavily on dependable heating, drying, and refrigeration—areas where propane offers a clean, stable and easily deployable energy source. Data from Food and Agriculture Organization (FAO) shows that agrifood systems already consume about 30% of the world’s total energy, highlighting just how significant the sector’s fuel requirements have become.

Propane’s role in agriculture becomes especially clear when looking at food loss caused by weak cold-chain infrastructure. According to FAO and UNEP analyses, the world loses 526 million tonnes of food every year, and a major portion of this loss occurs because farmers and food suppliers lack reliable cooling and processing energy.

Government programs are further amplifying this trend. Many countries are prioritizing cold-chain expansion and clean cooking transitions as part of food-security and rural-development policies. For example, the UN’s clean-energy development frameworks emphasize LPG and propane as transitional fuels for rural food systems because they improve health, reduce biomass burning, and support local food production.

The connection between propane and food security becomes even clearer when looking at post-farm energy use. FAO reports that post-farm activities—such as transport, storage, processing and retail—consume around 70% of total energy used in agrifood chains, a level of demand that cannot always be met by the electric grid in developing regions.

Restraints

High Supply-Chain Vulnerability Limits Stable Propane Availability

One of the most significant restraining factors for the propane market today is the growing vulnerability of global supply chains, especially in sectors that depend heavily on stable energy access for food storage, processing, and distribution. Even though propane is widely used across agriculture and food logistics, the fuel’s availability is still closely linked to crude-oil operations, gas-processing facilities, and long-distance transport routes. Disruptions in any of these stages—weather-related, geopolitical, or logistical—can cause sharp fluctuations in supply.

This becomes particularly concerning when viewed through the lens of global food systems, which already operate with narrow margins of energy security. According to the Food and Agriculture Organization (FAO), the world loses 526 million tonnes of food every year, and a major cause of this loss is unreliable energy access, which prevents proper refrigeration and storage.

When propane supply turns unstable, cold-chain operators, grain-drying facilities, rural food processors, and distribution centers face immediate risks. FAO further highlights that post-farm activities account for about 70% of the total energy used in agrifood systems, making these stages extremely sensitive to disruptions.

Governments acknowledge these vulnerabilities and have introduced several initiatives to strengthen domestic energy reliability, yet gaps still remain. Many countries promote renewable energy transitions, rural electrification, or distributed solar-cooling programs to reduce reliance on fuels like propane. While these policies are aimed at long-term resilience, they can unintentionally slow investment in conventional propane infrastructure, adding pressure on the existing distribution network.

Opportunity

Expanding Cold-Chain Energy Needs Open Major Growth Avenues for Propane

A major growth opportunity for the propane market lies in its role supporting expanding cold-chain and food-system energy demands globally. In recent years, governments, international organisations and industry stakeholders have come to recognise that sustainable cold-chain infrastructure is critical not just for reducing food loss and waste but also for improving food security, rural livelihoods and climate resilience. This opens a significant opportunity for propane, especially in regions where electricity access remains limited or grids are unreliable and where dependable thermal energy solutions are urgently needed.

Data from the Food and Agriculture Organization (FAO) shows that 526 million tonnes of food are lost or wasted each year as a direct result of inadequate refrigeration and cold-chain capacity, equivalent to a large fraction of global food production. This loss occurs largely at post-harvest storage and processing stages where consistent cooling and heat management are required to preserve quality. FAO also notes that enhancing cold-chain infrastructure in developing countries could prevent up to 144 million tonnes of food waste annually if these nations could reach similar cold-chain levels as advanced economies.

Governments and multilateral development agencies are increasingly prioritising modernisation of food energy systems. Many national policies now emphasise improved cold-chain logistics, agricultural value addition, and rural energy access as means to support food security and economic development. The UN’s Sustainable Development Goal 7 (SDG7) framework explicitly calls for affordable, reliable and modern energy access for all, recognising that energy is fundamental to every stage of agrifood systems—from irrigation and machinery to processing and storage.

At the same time, expanding cold-chains is not just about reducing food loss. Reliable cooling infrastructure enables farmers to diversify production into higher-value, perishable crops such as fruits, vegetables and dairy that can fetch better prices in distant markets. This expansion supports rural employment, stabilises food prices, and enhances local nutrition outcomes.

Regional Insights

Asia Pacific leads the propane landscape with a 44.8% share and 46.4 Mn volume

In the global Propane Market, Asia Pacific emerged as the dominant regional segment, accounting for 44.8% of total market share, representing around 46.4 Mn of the market volume in the latest assessment period. This leadership is underpinned by a powerful mix of demographic and policy factors: rapid urbanisation, strong petrochemical demand, and large residential dependence on LPG/propane for cooking and heating.

The region is already the world’s LPG powerhouse, with Asia-Pacific consuming over 180 million tonnes of LPG each year and representing about 55% of global LPG demand, which includes propane as a key component.

In parallel, clean-cooking policies have deepened household reliance on LPG and propane. The International Energy Agency (IEA) notes that developing Asia still has around 1.1 billion people without access to clean cooking, yet recent progress has pushed access rates to about 70% in India and around 90% in China and Indonesia, supported largely by LPG expansion.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

BP reported $52.6 billion revenue in 2023 and produced around 1.3 million barrels of oil equivalent per day across global operations. Its propane output comes mainly through NGL processing and refinery streams. The company manages over 70 trading hubs worldwide and supplies propane to industrial, residential and commercial customers. BP invested $4 billion in upstream development and maintains operations in 65+ countries, ensuring stable propane supply through integrated refining and logistics networks.

Chevron generated $194.7 billion revenue in 2023 and produced about 3.1 million barrels of oil equivalent per day. The company refines significant volumes of propane through its downstream assets and manages 13 major refineries globally. Chevron operates in 180 countries and invested $15 billion in capital projects focused on refining and petrochemicals. Its propane distribution network supports residential, agricultural and industrial clients, strengthened by strong NGL production from U.S. shale fields.

ExxonMobil recorded $344.6 billion revenue in 2023 and produced about 3.7 million barrels of oil equivalent per day. It is a top global supplier of propane through NGL extraction and refining operations. ExxonMobil operates 23 refineries in 14 countries, with NGL output exceeding 400,000 barrels per day. The company also invested $25 billion in upstream and chemical projects and serves large propane demand centers across North America, Europe and Asia.

Top Key Players Outlook

- BP Pic

- Chevron Corporation

- Royal Dutch Shell Pic

- Exxon Mobil Corporation

- ConocoPhillips

- Reliance Industries Ltd.

- PetroChina Company Limited

- Sinopec

- Total SA

- Ferrellgas Partners L.P.

Recent Industry Developments

In 2024–2025, Chevron’s operations included producing ~280,000 barrels per day of NGLs in key U.S. basins like the Permian, alongside ~435,000 barrels of crude oil as part of its broader output strategy.

For 2024, ExxonMobil reported $33.7 billion in earnings and invested $27.6 billion in capital and exploration expenditures, reinforcing the company’s ability to support core energy supply chains including propane, butane and ethane components of NGLs.

Report Scope

Report Features Description Market Value (2025) USD 103.7 Mn Forecast Revenue (2035) USD 221.0 Mn CAGR (2026-2035) 7.9% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Grade (HD-5, HD-10, Commercial), By Source (Refinery, Associated Gas, Non-Associated Gas, Bio-Propane), By End-user ( Residential, Commercial, Industrial, Transportation, Others), By Distribution Channel (Bulk Delivery, Cylinder Distribution, Autogas Refueling Network, Retail Packaged) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA Competitive Landscape BP Pic, Chevron Corporation, Royal Dutch Shell Pic, Exxon Mobil Corporation, ConocoPhillips, Reliance Industries Ltd., PetroChina Company Limited, Sinopec, Total SA, Ferrellgas Partners L.P. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- BP Pic

- Chevron Corporation

- Royal Dutch Shell Pic

- Exxon Mobil Corporation

- ConocoPhillips

- Reliance Industries Ltd.

- PetroChina Company Limited

- Sinopec

- Total SA

- Ferrellgas Partners L.P.

Our Clients

- 179970

- Mar 2026