Global Pesticide Inert Ingredients Market Size, Share and Report Analysis By Source (Synthetic, Bio-based), By Ingredient Function (Surfactants, Oil-based Oils and Methylated Seed Oils, Emulsifiers, Suspension and Drift Control Agents, Buffers and Water Conditioners), By Form (Liquid, Solid), By Pesticide Type (Herbicides, Insecticides, Fungicides, Others), By Crop Type (Cereals and Grains, Fruits and Vegetables, Oilseeds and Pulses, Others) , By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2025-2035

- Published date: Mar 2026

- Report ID: 180543

- Number of Pages: 348

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

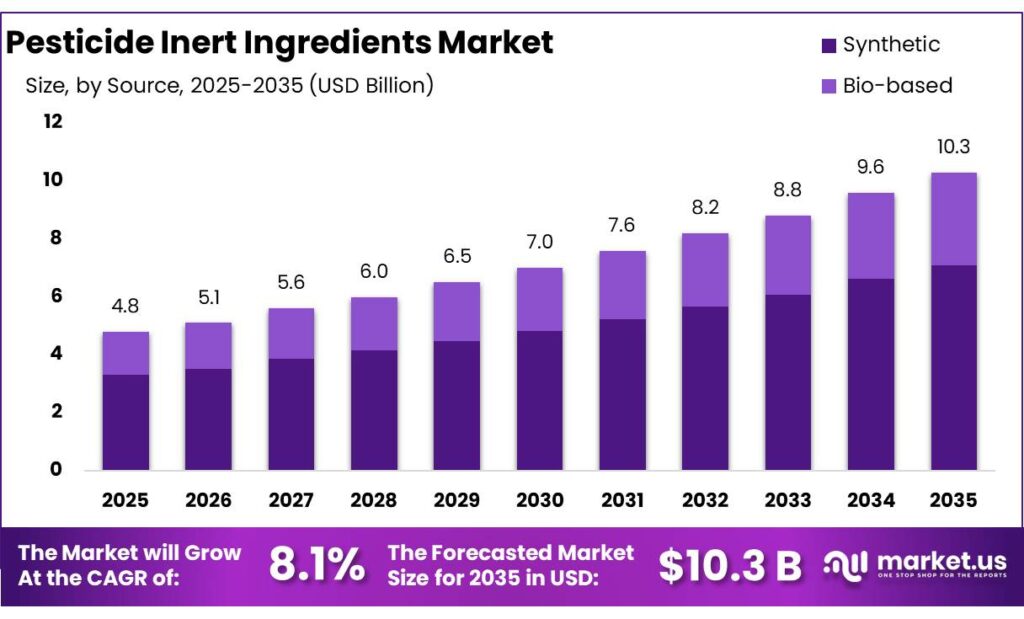

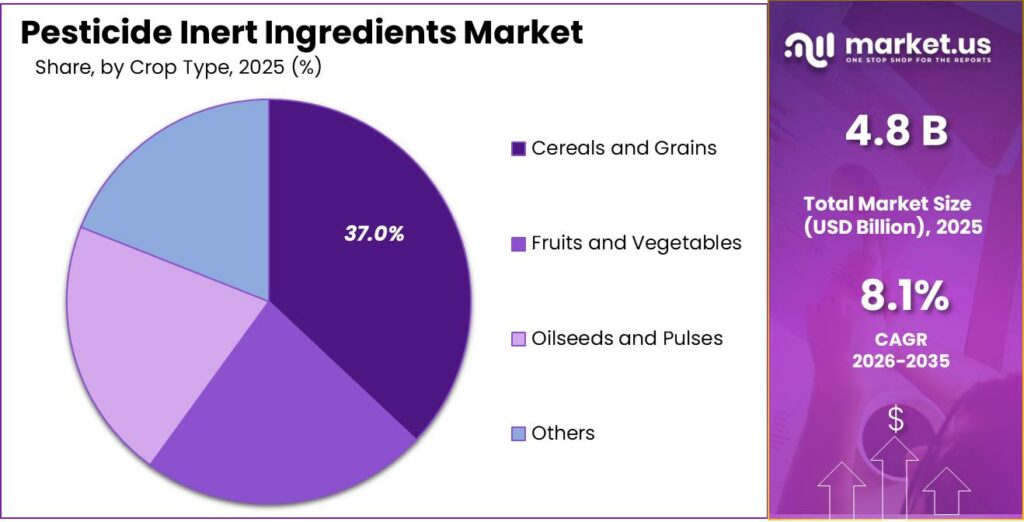

Global Pesticide Inert Ingredients Market is expected to be worth around USD 10.3 Billion by 2035, up from USD 4.8 Billion in 2025, at a CAGR of 8.1% from 2026 to 2035. The North America segment maintained 45.70%, supporting a Pesticide Inert Ingredients value of USD 2.1 Bn.

Pesticide inert ingredients form the performance backbone of modern crop protection products, even though they are not the pesticidally active molecules. The U.S. Environmental Protection Agency (EPA) defines an inert ingredient as any substance intentionally included in a pesticide product other than the active ingredient, with typical functions including emulsification, solvency, carrying, fragrance, anti-foaming, aerosol delivery and formulation stability.

EPA also classifies approvals by food and nonfood use, and notes that many food-use inert ingredients are regulated through tolerance or tolerance-exemption provisions under 40 CFR Part 180, while the agency completed the reassessment of inert ingredient tolerances required under the Food Quality Protection Act in 2006. This gives the segment a highly regulated, formulation-driven industrial identity in which compliance, residue acceptability and application performance are as important as chemistry itself.

FAO reported that total pesticide use in agriculture reached 3.73 million tonnes of active ingredients in 2023, while average application intensity stood at 2.40 kg per hectare. In the same year, global pesticide exports were 6.7 million tonnes of formulated products, valued at USD 42.8 billion, showing how formulation trade remains materially larger than active-ingredient movement alone and underscoring the commercial importance of solvents, surfactants, dispersants, carriers and stabilizers embedded in finished products.

FAO also reported that Asia exported 2.4 million tonnes of pesticides worth USD 11.4 billion in 2023, indicating that Asian formulation and co-formulant supply chains remain central to the global industrial landscape for both active and inert components.

The main demand drivers for inert ingredients are rising food-system pressure, crop-intensity growth, formulation specialization and tightening residue-safety expectations. FAO’s long-term outlook indicates that feeding a world population of 9.1 billion by 2050 would require roughly 70 percent higher food production than 2005/07 levels, with cereal demand projected to reach about 3 billion tonnes versus nearly 2.1 billion tonnes at the time of the FAO assessment.

The same FAO outlook states that 90 percent of crop production growth is expected to come from higher yields and increased cropping intensity rather than land expansion, which directly supports demand for better adjuvant systems, spreaders, wetting agents and compatibility enhancers that improve spray efficiency and reduce field losses. In practice, this means inert ingredients are increasingly being selected not merely as “inactive” carriers, but as productivity enablers that influence droplet behavior, tank-mix stability, shelf life and performance consistency across climatic conditions.

In Europe, the Farm to Fork framework set a 50 percent reduction target by 2030 for the use and risk of chemical pesticides, while the Common Agricultural Policy provides at least €48.5 billion for environmental and climate practices and at least €21.14 billion for rural-development management commitments, including pesticide reduction and organic farming measures.

In the United States, USDA announced up to USD 7.7 billion for FY2025 conservation practices, and NRCS received more than 156,485 applications in FY2024, indicating strong producer interest in climate-smart inputs and application systems. Collectively, these signals suggest that the inert ingredient industry’s next phase will be shaped by lower-toxicity surfactants, renewable feedstocks, multifunctional co-formulants and reformulation services aligned with food safety, environmental risk reduction and field-level efficiency.

Key Takeaways

- Pesticide Inert Ingredients Market is expected to be worth around USD 10.3 Billion by 2035, up from USD 4.8 Billion in 2025, at a CAGR of 8.1%.

- Synthetic held a dominant market position, capturing more than a 69.2% share of the pesticide inert ingredients market.

- Surfactants held a dominant market position, capturing more than a 29.1% share of the pesticide inert ingredients market.

- Liquid held a dominant market position, capturing more than a 67.4% share of the pesticide inert ingredients market.

- Herbicides held a dominant market position, capturing more than a 44.9% share.

- Cereals and Grains held a dominant market position, capturing more than a 37.3% share.

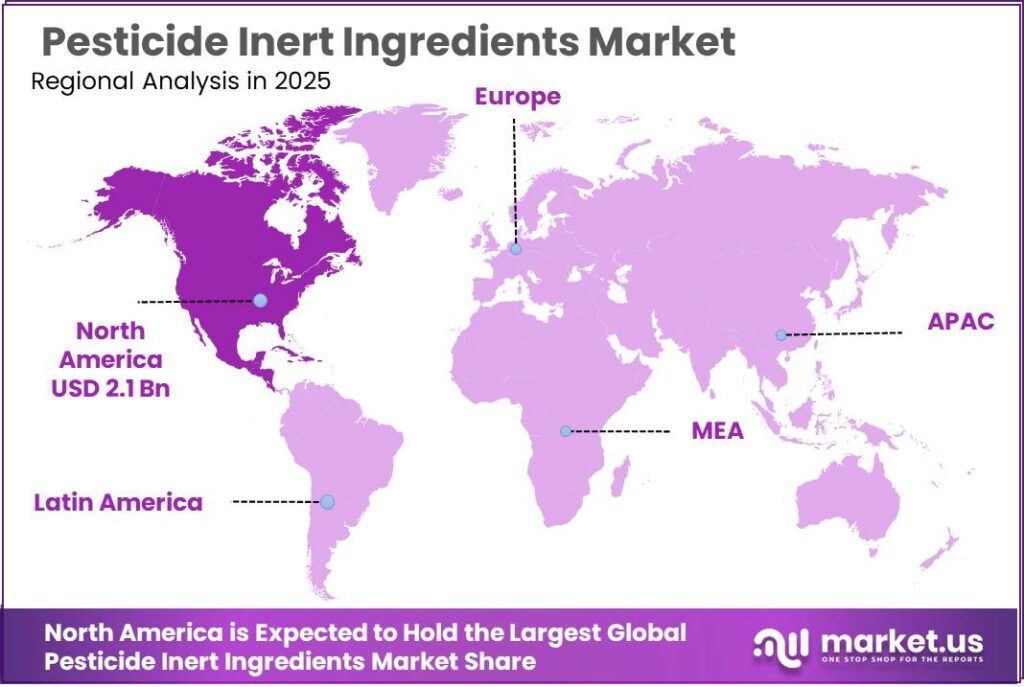

- North America emerged as the dominating region in the pesticide inert ingredients market, accounting for nearly 45.70% of the global share with an estimated value of about USD 2.1 billion.

By Source Analysis

Synthetic Source dominates with 69.2% due to its strong role in improving pesticide formulation stability

In 2024, Synthetic held a dominant market position, capturing more than a 69.2% share of the pesticide inert ingredients market. This dominance is largely attributed to the widespread use of synthetic solvents, surfactants, emulsifiers, and stabilizers in pesticide formulations. These ingredients help improve the dispersion, adhesion, and stability of active ingredients, making pesticides more effective when applied in agricultural fields. Synthetic inert ingredients are commonly used because they are chemically consistent, easier to manufacture at scale, and capable of performing reliably across a wide range of crop protection products such as herbicides, insecticides, and fungicides. Their strong compatibility with different active ingredients allows pesticide manufacturers to maintain uniform product performance under varying environmental conditions.

By Ingredient Function Analysis

Surfactants lead with 29.1% as they improve pesticide spreading and spray efficiency

In 2024, Surfactants held a dominant market position, capturing more than a 29.1% share of the pesticide inert ingredients market by ingredient function. Their strong position is mainly due to their important role in improving how pesticides perform once they are applied to crops. Surfactants help reduce surface tension, allowing pesticide droplets to spread more evenly across plant leaves and stems. This improves the contact between the pesticide and the target pest, which increases the overall effectiveness of the product. Because of this function, surfactants are commonly included in herbicides, insecticides, and fungicides to ensure better coverage and absorption.

By Form Analysis

Liquid form dominates with 67.4% as it supports easy mixing and efficient field application

In 2024, Liquid held a dominant market position, capturing more than a 67.4% share of the pesticide inert ingredients market by form. The strong presence of liquid formulations is mainly due to their ease of use in agricultural spraying systems. Liquid inert ingredients such as solvents, emulsifiers, and dispersing agents mix easily with active pesticide compounds and water, making them suitable for large-scale crop protection operations. Farmers and pesticide manufacturers prefer liquid formulations because they can be blended smoothly in spray tanks and applied uniformly across fields using standard spraying equipment.

By Pesticide Type Analysis

Herbicides dominate with 44.9% as farmers rely on them heavily for weed control

In 2024, Herbicides held a dominant market position, capturing more than a 44.9% share of the pesticide inert ingredients market by pesticide type. This strong share reflects the extensive use of herbicides in modern agriculture to manage weeds that compete with crops for nutrients, water, and sunlight. Weed pressure is one of the most common challenges faced by farmers, and herbicides are widely used to maintain crop productivity across large agricultural areas. In herbicide formulations, inert ingredients such as surfactants, solvents, carriers, and stabilizers play an important role in ensuring that the active ingredient spreads effectively on plant surfaces and penetrates the leaf tissue of weeds.

By Crop Type Analysis

Cereals and Grains lead with 37.3% as they remain the most widely cultivated crops worldwide

In 2024, Cereals and Grains held a dominant market position, capturing more than a 37.3% share of the pesticide inert ingredients market by crop type. The strong presence of this segment is mainly linked to the massive global cultivation of crops such as wheat, rice, maize, barley, and sorghum. These crops form the foundation of food systems in many countries and require consistent protection from weeds, pests, and diseases. Because pesticides are commonly used in cereal and grain farming, inert ingredients play an important role in improving pesticide formulation performance. These substances help active ingredients spread evenly, remain stable during storage, and perform effectively during field application.

Key Market Segments

By Source

- Synthetic

- Bio-based

By Ingredient Function

- Surfactants

- Oil-based Oils and Methylated Seed Oils

- Emulsifiers

- Suspension and Drift Control Agents

- Buffers and Water Conditioners

By Form

- Liquid

- Solid

By Pesticide Type

- Herbicides

- Insecticides

- Fungicides

- Others

By Crop Type

- Cereals and Grains

- Fruits and Vegetables

- Oilseeds and Pulses

- Others

Emerging Trends

Shift Toward Safer and More Environment-Friendly Inert Ingredients

One of the most noticeable recent trends in the pesticide inert ingredients industry is the growing shift toward safer, environmentally responsible formulation components. Governments, agricultural organizations, and consumers are increasingly concerned about the environmental and health effects of chemical pesticides and their formulation additives.

According to the Food and Agriculture Organization (FAO), total pesticide use in agriculture reached 3.73 million tonnes of active ingredients in 2023, demonstrating the heavy reliance on chemical crop protection worldwide. At the same time, the global average pesticide application intensity was about 2.40 kilograms per hectare of cropland in 2023, showing how frequently these products are used to maintain agricultural productivity.

Governments and regulatory agencies have already started introducing measures that influence the selection of inert ingredients in pesticide products. A clear example comes from the U.S. Environmental Protection Agency (EPA), which in 2022 removed 12 PFAS chemicals from the list of approved inert ingredients used in pesticide formulations. PFAS substances are often called “forever chemicals” because they can persist in the environment for a long time.

Along with regulatory pressure, the global push for sustainable agriculture is also influencing formulation trends. Agricultural organizations such as FAO promote practices like Integrated Pest Management (IPM), which encourage the careful and efficient use of pesticides while minimizing environmental risks. In these systems, pesticide formulations must work more precisely and efficiently, often requiring advanced inert ingredients that improve droplet spreading, adhesion to plant surfaces, and stability under different environmental conditions.

Drivers

Rising Global Food Demand and Crop Protection Needs

One of the most important driving factors for the pesticide inert ingredients market is the rapidly growing global demand for food production, which increases the need for effective crop protection solutions. As the global population continues to expand, agricultural systems are under pressure to produce more food from limited land and resources. This situation has pushed farmers and agricultural industries to rely more heavily on pesticides to protect crops from pests, weeds, and plant diseases. In pesticide formulations, inert ingredients play a crucial role because they help improve the stability, spreading ability, and effectiveness of the active ingredients. Without these supporting components, many pesticides would not work efficiently in real farming conditions.

The pressure on food production is clearly reflected in projections from global food organizations. The Food and Agriculture Organization (FAO) estimates that the world population could reach around 9.1 billion people by 2050, and feeding this population would require global food production to increase by nearly 70% compared with earlier levels. This expected growth in food demand means that agricultural productivity must improve significantly over the coming decades. Crop protection products will therefore remain essential tools for farmers trying to maintain high yields and reduce losses caused by pests and diseases.

At the same time, the actual use of pesticides worldwide has already grown substantially as farmers try to protect crops from increasing pest pressure. FAO data shows that global pesticide use reached about 3.73 million tonnes of active ingredients in 2023, reflecting the massive scale of crop protection practices in modern agriculture. This level of usage highlights the importance of pesticide formulations, where inert ingredients are used to improve spray coverage, stability, and compatibility with different application systems. These components help pesticides mix properly with water, stick to plant surfaces, and remain stable during storage and transport.

Another indicator of growing crop protection demand is the increase in pesticide application intensity across agricultural land. FAO reports that the average pesticide use intensity reached around 2.40 kilograms per hectare of cropland in 2023. This means farmers are applying pesticides more carefully and frequently to ensure crops are protected during different growth stages. Inert ingredients support this process by enhancing how pesticide droplets spread across leaves, how well they adhere to plant surfaces, and how effectively the active ingredients penetrate pests or weeds.

Restraints

Increasing Regulatory Restrictions on Pesticide Ingredients and Formulations

One of the major restraining factors for the pesticide inert ingredients market is the growing regulatory pressure on pesticide formulations and chemical additives used in agriculture. Governments and environmental agencies across the world are tightening regulations to ensure that pesticide products are safe for human health, food systems, and the environment. While these regulations mainly focus on active ingredients, inert ingredients used in pesticide formulations are also coming under greater scrutiny.

Regulatory oversight for pesticide ingredients is particularly strong in regions such as North America and Europe. In the United States, the U.S. Environmental Protection Agency (EPA) regulates pesticide formulations under the Federal Insecticide, Fungicide, and Rodenticide Act (FIFRA). The agency evaluates both active and inert ingredients before allowing pesticide products to be sold or used in agriculture. EPA data shows that the agency has over 4,000 approved inert ingredients that can be used in pesticide formulations, but each of these substances must meet strict safety standards and may be reviewed periodically for environmental or health risks.

In recent years, regulatory actions have become more focused on removing chemicals that may pose long-term environmental concerns. For example, in 2022 the EPA announced the removal of 12 PFAS-related chemicals from the approved list of inert ingredients used in pesticide products. These substances were removed due to concerns about persistence in the environment and potential risks to water systems and human health. Decisions like this can create challenges for pesticide manufacturers, who must invest time and resources in reformulating products with alternative ingredients.

Europe has also implemented strong policies that affect pesticide formulation components. The European Union’s Farm to Fork Strategy, part of the broader European Green Deal, aims to reduce the use and risk of chemical pesticides by 50% by the year 2030. This policy encourages farmers and agricultural companies to adopt safer pest management solutions and promotes stricter evaluation of pesticide ingredients used in crop protection products.

Opportunity

Rising Demand for High-Efficiency and Sustainable Pesticide Formulations

One major growth opportunity for the pesticide inert ingredients industry comes from the increasing demand for more efficient and environmentally responsible pesticide formulations. Farmers around the world are under pressure to protect crop yields while also reducing chemical waste and environmental impact. Because of this, agricultural producers and pesticide manufacturers are focusing on improved formulations that deliver better performance with smaller quantities of active ingredients.

The importance of efficient crop protection is closely connected to the scale of pesticide use in global agriculture. According to the Food and Agriculture Organization (FAO), global pesticide use reached 3.73 million tonnes of active ingredients in 2023, demonstrating the extensive reliance on crop protection products across farming systems worldwide. In addition, FAO reports that the average pesticide application intensity reached 2.40 kilograms per hectare of cropland in 2023.

Another factor supporting growth opportunities for inert ingredients is the increasing global need for food production. FAO projections indicate that the world population could reach around 9.1 billion by 2050, and meeting the food requirements of this population will require about 70% more food production compared with earlier levels. To support this demand, cereal production alone may need to increase to around 3 billion tonnes annually by 2050, compared with roughly 2.1 billion tonnes in earlier decades.

Government initiatives and international agricultural programs are also encouraging the development of safer and more efficient pesticide technologies. Organizations such as the FAO promote Integrated Pest Management (IPM) strategies that focus on using pesticides more efficiently while reducing environmental risks. Under these programs, pesticide formulations are being redesigned to deliver targeted pest control with minimal environmental impact. Advanced inert ingredients play an important role in this shift because they help improve pesticide delivery systems, allowing farmers to achieve better pest control results with lower application rates.

Regional Insights

North America dominates the Pesticide Inert Ingredients Market with 45.70% share, valued at about USD 2.1 Bn

North America emerged as the dominating region in the pesticide inert ingredients market, accounting for nearly 45.70% of the global share with an estimated value of about USD 2.1 billion. The region’s leadership is mainly driven by its highly advanced agricultural sector, large-scale commercial farming practices, and strong demand for efficient crop protection products.

The United States represents the largest contributor within the North American market due to its extensive use of agrochemicals in major crop systems such as corn, soybean, wheat, and cotton. According to global agricultural statistics, the United States uses more than 407,000 tonnes of pesticides annually, making it one of the largest pesticide-consuming countries worldwide.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

BASF SE plays a significant role in the pesticide inert ingredients market through its extensive portfolio of formulation additives such as surfactants, solvents, and dispersing agents used in crop protection products. In 2024, the company reported global sales of around €68.9 billion, with its Agricultural Solutions division generating about €10.1 billion in revenue. BASF operates in more than 90 countries and runs over 230 production sites worldwide, enabling strong supply of formulation ingredients.Dow Inc. is a major supplier of specialty chemicals and formulation materials used in pesticide products, including emulsifiers, solvents, and surfactants. In 2024, Dow reported net sales of about USD 44.6 billion, supported by operations in over 160 countries. The company operates approximately 104 manufacturing sites across 31 countries, ensuring strong global distribution capabilities. Dow’s Performance Materials and Coatings segment provides several ingredients used in agrochemical formulations.Halliburton Company is one of the largest providers of hydraulic fracturing services, delivering chemicals, crosslinkers, surfactants and fluid systems across major shale basins. Operating in over 70 countries with more than 40,000 employees, the company generated revenues above $23 billion recently. Halliburton handles thousands of fracturing stages annually, offering fluid systems designed for long-reach horizontal wells. Its R&D investment exceeds $400 million per year, helping it develop high-efficiency, low-residue fracking chemistries that improve production and reduce environmental impact.Top Key Players Outlook

- BASF SE

- Dow Inc.

- Solvay SA

- Clariant AG

- Croda International

- Stepan Company

- Huntsman Corporation

- Evonik Industries

- Ashland Inc

- Borregaard ASA

- Elkem ASA

- CHT Group

- Ethox Chemicals, LLC

- Momentive Performance Materials Inc

- Lamberti SpA

Recent Industry Developments

In 2024, Halliburton reported total annual revenue of USD 22.9 billion, with its fluids and stimulation technologies playing a key role in the Completion and Production segment that accounted for more than $12 billion of the business, showing how central these solutions are to its operations.

In 2024, Dow delivered about $43 billion in sales, reflecting its scale and diversified chemicals business.

Report Scope

Report Features Description Market Value (2025) USD 4.8 Bn Forecast Revenue (2035) USD 10.3 Bn CAGR (2026-2035) 8.1% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Source (Synthetic, Bio-based), By Ingredient Function (Surfactants, Oil-based Oils and Methylated Seed Oils, Emulsifiers, Suspension and Drift Control Agents, Buffers and Water Conditioners), By Form (Liquid, Solid), By Pesticide Type (Herbicides, Insecticides, Fungicides, Others), By Crop Type (Cereals and Grains, Fruits and Vegetables, Oilseeds and Pulses, Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA Competitive Landscape BASF SE, Dow Inc., Solvay SA, Clariant AG, Croda International, Stepan Company, Huntsman Corporation, Evonik Industries, Ashland Inc, Borregaard ASA, Elkem ASA, CHT Group, Ethox Chemicals, LLC, Momentive Performance Materials Inc, Lamberti SpA Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Pesticide Inert Ingredients MarketPublished date: Mar 2026add_shopping_cartBuy Now get_appDownload Sample

Pesticide Inert Ingredients MarketPublished date: Mar 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- BASF SE

- Dow Inc.

- Solvay SA

- Clariant AG

- Croda International

- Stepan Company

- Huntsman Corporation

- Evonik Industries

- Ashland Inc

- Borregaard ASA

- Elkem ASA

- CHT Group

- Ethox Chemicals, LLC

- Momentive Performance Materials Inc

- Lamberti SpA

Our Clients

- 180543

- Mar 2026