Global Oxidizing Agents Market By Product Type (Hydrogen Peroxide, Sodium Hypochlorite, Potassium Permanganate, Chlorine, Ozone, and Others), By End-Use (Water And Wastewater Treatment, Pulp And Paper, Textiles, Household And Institutional Cleaning, Healthcare And Sterilization, Food And Beverage, Mining And Metals, Electronics, and Other End Uses), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2026-2035

- Published date: Mar 2026

- Report ID: 183463

- Number of Pages: 254

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

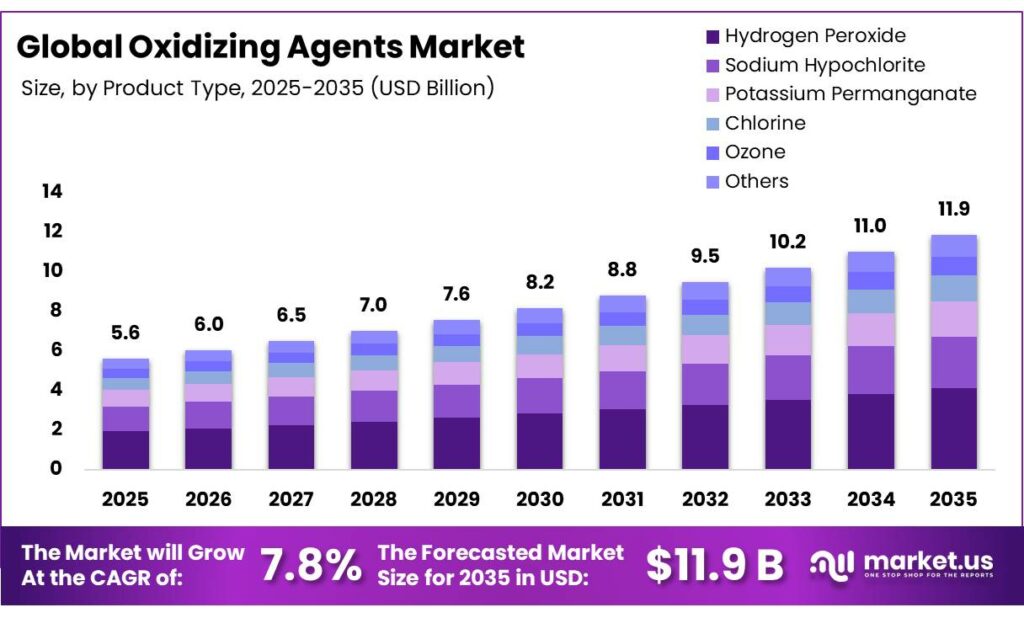

The Global Oxidizing Agents Market size is expected to be worth around USD 11.9 Billion by 2035, from USD 5.6 Billion in 2025, growing at a CAGR of 7.8% during the forecast period from 2026 to 2035. In 2025, Europe held a dominant market position, capturing more than a 37.4% share, holding USD 0.7 Billion revenue.

An oxidizing agent, or oxidizer, is a substance that causes oxidation by accepting electrons from another reactant in a redox reaction. The oxidizing agents market is primarily driven by regulatory requirements, industrial demand, and environmental considerations. These chemicals, including hydrogen peroxide, chlorine, sodium hypochlorite, potassium permanganate, and ozone, are extensively used in municipal and industrial water and wastewater treatment, where compliance with standards such as the U.S. EPA Safe Drinking Water Act, Clean Water Act, and EU Drinking Water Directive necessitates effective disinfection and control of chemical contaminants.

- According to a 2025 report by UNICEF, in 2024, 89 countries had already achieved universal access to at least basic drinking water. Thirty-one countries have achieved universal access to safely managed drinking water, and if current trends continue, 38 will have reached universal access by 2030.

Hydrogen peroxide is favored due to its strong oxidizing capacity, stability, and environmentally benign byproducts. Asia Pacific is the largest regional consumer, driven by industrial growth and stringent effluent regulations in countries such as China, India, and Thailand. Manufacturers focus on process innovation, high-purity formulations, and supply chain resilience to maintain competitiveness, while environmental and safety regulations influence product selection and operational practices. Adoption of eco-friendly formulations and regulatory compliance shape the sector’s strategic direction.

Key Takeaways:

- The global oxidizing agents market was valued at US$5.6 billion in 2025.

- The global oxidizing agents market is projected to grow at a CAGR of 7.8% and is estimated to reach US$11.9 million by 2035.

- Based on the types of oxidizing agents, hydrogen peroxide dominated the market, with a market share of around 34.8%.

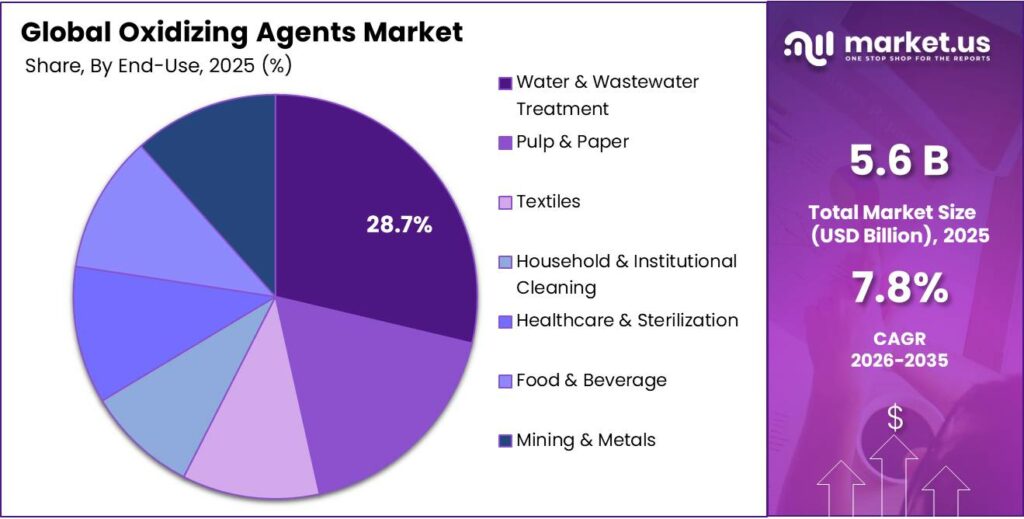

- Among the end-uses of oxidizing agents, the water & wastewater treatment industry held a major share in the market, 28.7% of the market share.

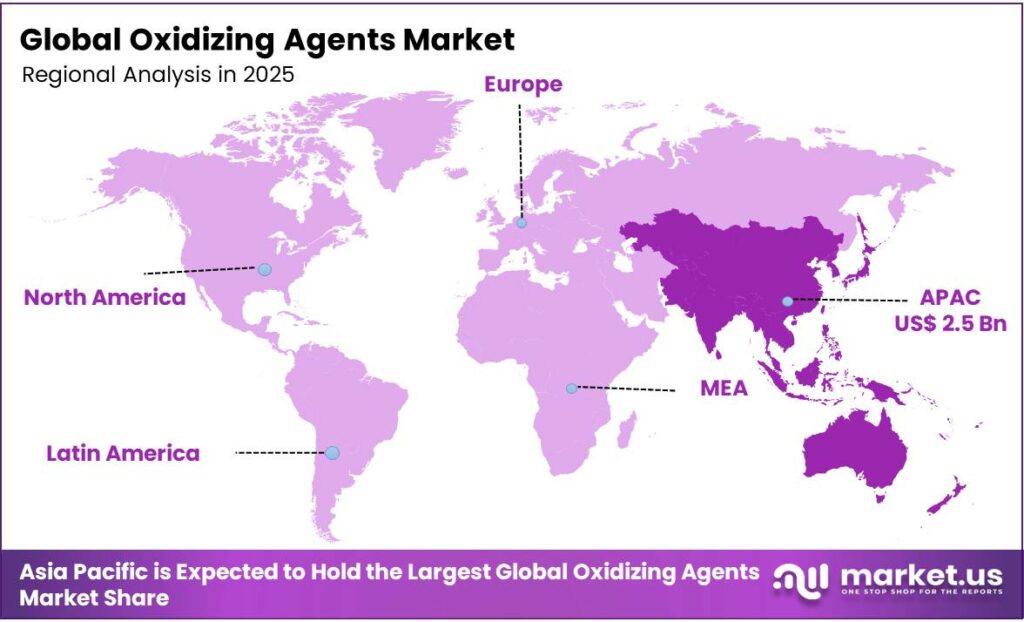

- In 2025, the Asia Pacific was the most dominant region in the oxidizing agents market, accounting for around 43.9% of the total global consumption.

Product Type Analysis

Hydrogen Peroxide Held the Largest Share in the Oxidizing Agents Market.

The oxidizing agents market is segmented based on product type into hydrogen peroxide, sodium hypochlorite, potassium permanganate, chlorine, ozone, and others. The hydrogen peroxide dominated the market, comprising around 34.8% of the market share, due to its strong oxidizing capacity combined with environmental and operational advantages.

Unlike chlorine or sodium hypochlorite, it does not form chlorinated disinfection byproducts such as trihalomethanes or haloacetic acids, making it safer for potable water and industrial effluent treatment.

In contrast with potassium permanganate, hydrogen peroxide is easier to handle, dose, and decompose, leaving only water and oxygen as benign byproducts, reducing secondary pollution risks.

Unlike ozone, which requires on-site generation and rapid use due to instability, hydrogen peroxide is stable in transport and storage, enabling flexible application across municipal, industrial, and chemical processes. Its compatibility with multiple water treatment processes and chemical synthesis pathways, coupled with regulatory acceptance, marks its widespread adoption as a preferred oxidant.

End-Use Analysis

Oxidizing Agents Are Mostly Utilized in the Water & Wastewater Treatment Industry.

Based on the end-uses of oxidizing agents, the market is divided into water & wastewater treatment, pulp & paper, textiles, household & institutional cleaning, healthcare & sterilization, food & beverage, mining & metals, electronics, and other end uses. The water & wastewater treatment industry dominated the oxidizing agents market, with a market share of 28.7%, due to the regulatory and public health imperatives associated with safe water supply.

Municipal and industrial water systems require reliable disinfection to eliminate pathogens and control chemical contaminants, as mandated by the U.S. EPA Safe Drinking Water Act and Clean Water Act, and equivalent standards globally. Oxidizing agents such as chlorine, hydrogen peroxide, and ozone are effective at achieving residual disinfectant levels, reducing biochemical oxygen demand (BOD), and preventing microbial regrowth.

While other sectors, such as pulp and paper, textiles, food processing, healthcare, and electronics, use oxidants, their applications are process-specific and less uniformly regulated, resulting in lower aggregate volumes. In contrast, water treatment represents a continuous, large-scale, and strictly regulated requirement, making it the primary consumer of oxidizing agents.

Key Market Segments:

By Product Type

- Hydrogen Peroxide

- Sodium Hypochlorite

- Potassium Permanganate

- Chlorine

- Ozone

- Others

By End-Use

- Water & Wastewater Treatment

- Pulp & Paper

- Textiles

- Household & Institutional Cleaning

- Healthcare & Sterilization

- Food & Beverage

- Mining & Metals

- Electronics

- Others

Drivers

Water Treatment Regulations Drive the Oxidizing Agents Market.

Water treatment regulations have emerged as a significant driver for the demand for oxidizing agents such as chlorine, ozone, and hydrogen peroxide, primarily through mandated water quality standards. The U.S. Environmental Protection Agency (EPA) Safe Drinking Water Act (SDWA) requires residual disinfectant levels in public water systems, such as haloacetic acids at 0.060 mg/L, compelling utilities to use oxidizing agents for pathogen and disinfection byproducts (DBPs) control.

- According to a study by UNICEF, between 2015 and 2024, 961 million people gained access to safely managed drinking water services, raising global coverage from 68% to 74%, due to the adoption of oxidative disinfection processes.

Additionally, the EPA’s regulation of PFAS at 4.0 parts per trillion (ppt) and reinforced wastewater standards for chemical oxygen demand (COD) under the Clean Water Act necessitate the use of strong oxidants for remediation. Furthermore, the European Union’s Drinking Water Directive (Directive (EU) 2020/2184) obliges member states to maintain microbial and chemical parameters, including free chlorine levels in potable water.

Restraints

Environmental and Regulatory Pressures Might Hamper the Demand for Conventional Oxidizing Agents.

Environmental and safety regulations increasingly challenge the conventional oxidizing agents market by imposing strict limits on disinfection byproducts (DBPs) and handling protocols. The U.S. Environmental Protection Agency (EPA) enforces National Primary Drinking Water Regulations that strictly limit DBPs formed by conventional oxidants.

Chlorine and chlorine-based compounds, widely used in water and wastewater treatment, are classified as hazardous under the U.S. Environmental Protection Agency’s Toxic Substances Control Act, requiring strict storage, handling, and disposal protocols. Legally enforceable maximum contaminant levels (MCLs) include 0.080 mg/L for total trihalomethanes (TTHMs), 0.060 mg/L for haloacetic acids (HAA5), and 1.0 mg/L for chlorite, a byproduct of chlorine dioxide.

Similarly, the European Chemicals Agency (ECHA) lists hydrogen peroxide under REACH Annex XVII restrictions for certain concentrations, emphasizing occupational exposure limits of 1 ppm as an 8-hour time-weighted average. Regulatory compliance necessitates continuous monitoring and safety infrastructure, increasing operational complexity.

Moreover, beyond water quality, the Occupational Safety and Health Administration (OSHA) mandates rigorous process safety management for highly hazardous chemicals. For instance, conventional oxidizers such as chlorine and hydrogen peroxide require mandatory safety data sheets (SDS) and employee training for all handlers.

Opportunity

Industrial Demand & Manufacturing Create Opportunities in the Oxidizing Agents Market.

Industrial demand and manufacturing processes present a structured opportunity for oxidizing agents in multiple sectors, particularly through the transition toward chlorine-free bleaching and high-purity chemical synthesis. In textile manufacturing, hydrogen peroxide is widely applied for bleaching, with the Indian Ministry of Textiles guidelines recommending 3-5g/L concentrations for cotton processing to achieve regulatory colorfastness standards.

Additionally, the chemical industry utilizes oxidizing agents in intermediate synthesis, such as nitric acid production and epoxide formation, where controlled peroxide dosing of 2-10% w/w is reported. Similarly, in pulp and paper production, the demand for hydrogen peroxide is driven by the adoption of elemental chlorine-free (ECF) and totally chlorine-free (TCF) bleaching sequences.

Furthermore, manufacturing expansions are increasingly targeting high-value and specialized grade oxidizing agents. For instance, in January 2024, Solvay expanded the hydrogen peroxide capacity of its Shandong Huatai Interox Chemical site in China. Building on its existing partnership with Huatai Chemical, the strategic alliance was to enable the site to produce 48 kilotons of photovoltaic-grade hydrogen peroxide annually.

Trends

Adoption of Sustainable and Eco-Friendly Formulations.

The oxidizing agents market is transitioning toward green oxidants, primarily driven by the replacement of chlorine-based chemicals with substances that decompose into non-toxic byproducts. The U.S. Environmental Protection Agency (EPA) Safer Choice program encourages the use of oxidants such as hydrogen peroxide over chlorine-based agents due to lower formation of disinfection byproducts, with approved formulations demonstrating less than 0.01 mg/L residual toxic byproducts in treated effluent.

Hydrogen peroxide is increasingly utilized as a sustainable alternative because it decomposes solely into water and oxygen. Similarly, in the European Union, the REACH Annex XVII framework restricts persistent organic pollutants in water treatment, promoting oxygen-based and enzymatic oxidants. Furthermore, strategic initiatives such as the myH₂O₂ project in Brazil enable the production of hydrogen peroxide directly at the point of use, eliminating long-distance transport emissions.

Moreover, industrial leaders have committed to aggressive climate plans, targeting a 50% reduction in Scope 1 and 2 greenhouse gas emissions by 2030 compared to 2019 levels. This trend is supported by the rise of bio-based specialty materials and mass-balance certified supply chains that reduce product carbon footprints by up to 100%.

Geopolitical Impact Analysis

Geopolitical Tensions Accelerate Strategic Production of Oxidizing Agents.

The geopolitical tensions influence the oxidizing agents market primarily through disruptions in raw material supply chains and trade restrictions. Chlorine and hydrogen peroxide production relies on feedstocks such as chlorine gas, caustic soda, and high-purity oxygen. China supplies over 60% of global caustic soda exports, while Europe imports approximately 45% of chlorine intermediates from non-EU countries.

Similarly, export controls and sanctions imposed in response to geopolitical conflicts, such as those on Russian chemical exports under EU Regulation 833/2014, restrict access to chlorine derivatives and potassium permanganate used in municipal and industrial treatment processes. Additionally, there exist supply vulnerabilities in hydrogen peroxide production in the US due to reliance on imported high-purity oxygen from regions affected by logistical bottlenecks.

These disruptions necessitate operational adjustments, including increased inventory management, alternative sourcing, and modifications in production scheduling. The geopolitical pressures create tangible constraints on the production, distribution, and consistent application of oxidizing agents.

Regional Analysis

Asia Pacific Held the Largest Share of the Global Oxidizing Agents Market.

In 2025, the Asia Pacific dominated the global oxidizing agents market, holding about 43.9% of the total global consumption, driven by industrial expansion, urban water treatment, and regulatory compliance. According to India’s Bureau of Indian Standards, most municipal water treatment plants employ chlorine or chlorine-based oxidants to maintain microbial standards.

China’s Ministry of Ecology and Environment mandates chemical oxygen demand (COD) limits of 50-100 mg/L in industrial effluents, prompting widespread use of hydrogen peroxide and ozone for wastewater oxidation. In Southeast Asia, in most kraft pulp mills in Thailand, elemental chlorine free (ECF) is used in pulp bleaching to meet BOD and TOC standards.

The region’s rapid industrialization and regulatory emphasis on water and wastewater quality, supported by extensive municipal and industrial adoption, position Asia Pacific as the leading market for oxidizing agents, reflecting both environmental compliance requirements and process integration across key sectors.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

A primary emphasis of manufacturers of oxidizing agents is on process innovation, such as developing energy-efficient production methods for hydrogen peroxide or ozone, which improve operational sustainability and reduce environmental compliance risks. Additionally, companies invest in product differentiation by offering stabilized, high-purity formulations suitable for municipal water treatment, industrial bleaching, or chemical synthesis, ensuring regulatory compliance with local and international standards.

Expansion of manufacturing infrastructure, including multi-site production and regional distribution centers, supports supply chain reliability amid raw material volatility. Similarly, firms prioritize safety protocols and worker training aligned with OSHA and REACH guidelines, which strengthens operational resilience and regulatory adherence.

The Major Players in The Industry

- BASF SE

- Solvay S.A.

- Evonik Industries AG

- AkzoNobel N.V.

- Arkema Group

- Dow Chemical

- Clariant AG

- Kemira Oyj

- Aditya Birla Chemicals

- PeroxyChem LLC

- Other Key Players

Key Development

- In June 2025, Solvay and BASF announced a collaborative effort aimed at significantly reducing scope 3 greenhouse gas emissions within the hydrogen peroxide supply chain. Solvay chose BASF as its primary supplier of aluminum chloride for its Linne Herten plant in the Netherlands. This key component is vital in the production of anthraquinone, an essential substance used in the manufacturing of hydrogen peroxide.

- In December 2023, Evonik announced the complete acquisition of Thai Peroxide Co., Ltd. (TPL), based in Saraburi, Thailand, marking the full takeover of its former joint venture. The acquisition follows the purchase of the 50% stake previously held by Aditya Birla Group entities and other partners. This move is expected to enhance Evonik’s hydrogen peroxide and peracetic acid specialties business in the Asia Pacific region.

Report Scope

Report Features Description Market Value (2025) US$5.6 Bn Forecast Revenue (2035) US$11.9 Bn CAGR (2025-2035) 7.8% Base Year for Estimation 2025 Historic Period 2021-2024 Forecast Period 2025-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product Type (Hydrogen Peroxide, Sodium Hypochlorite, Potassium Permanganate, Chlorine, Ozone, and Others), By End-Use (Water & Wastewater Treatment, Pulp & Paper, Textiles, Household & Institutional Cleaning, Healthcare & Sterilization, Food & Beverage, Mining & Metals, Electronics, and Other End Uses) Regional Analysis North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA Competitive Landscape BASF SE, Solvay S.A., Evonik Industries AG, AkzoNobel N.V., Arkema Group, Dow Chemical, Clariant AG, Kemira Oyj, Aditya Birla Chemicals, PeroxyChem LLC, and Other Players. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)

-

-

- BASF SE

- Solvay S.A.

- Evonik Industries AG

- AkzoNobel N.V.

- Arkema Group

- Dow Chemical

- Clariant AG

- Kemira Oyj

- Aditya Birla Chemicals

- PeroxyChem LLC

- Other Key Players

Our Clients

- 183463

- Mar 2026