Global Oxidation and Corrosion Control Chemicals Market By Product Type (Oxidation Control Chemicals and Corrosion-Control Chemicals), By End-Use (Municipal Water Treatment and Industrial Water Treatment), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2025-2035

- Published date: Feb 2026

- Report ID: 179375

- Number of Pages: 198

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

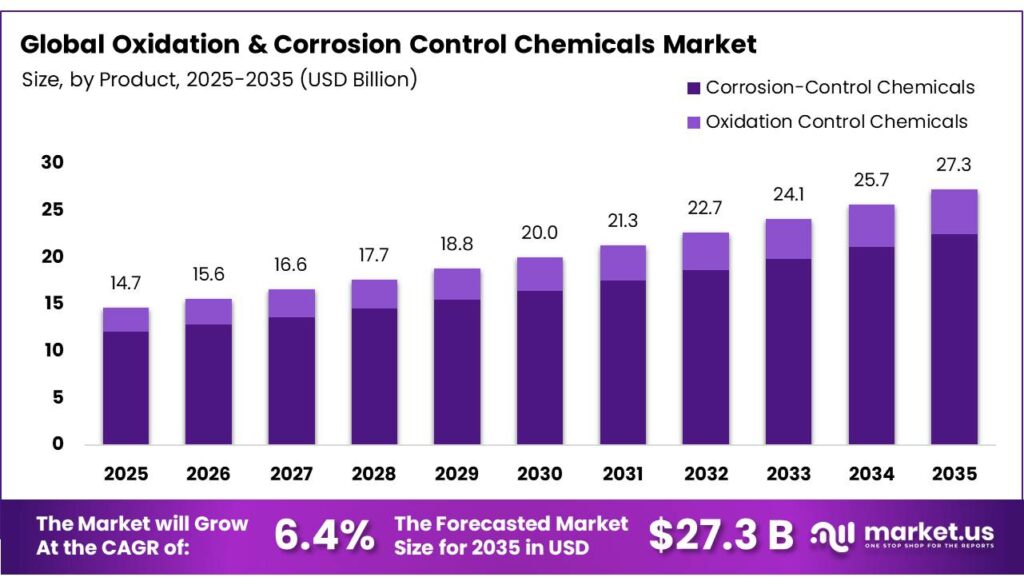

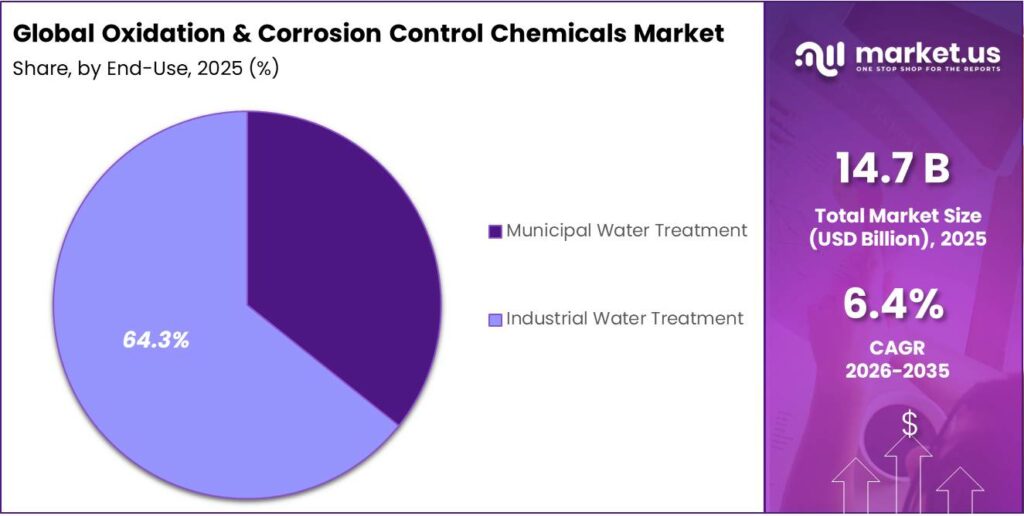

The Global Oxidation and Corrosion Control Chemicals Market is expected to be worth around USD 27.3 Billion by 2035, up from USD 14.7 Billion in 2025, at a CAGR of 6.4% from 2026 to 2035. The North America segment maintained 43.6%, supporting a Magnetorheological Fluids value of USD 31.9 Mn.

Oxidation and corrosion control chemicals are substances designed to prevent or slow the degradation of materials, primarily metals, caused by their reaction with the environment. While oxidation is a broad chemical process where a substance loses electrons, corrosion is the specific physical deterioration of metal resulting from that process.

- According to the World Corrosion Organization, corrosion around the globe causes damage of US$2.5 trillion annually, with several studies indicating that 25%-30% of these annual costs could be mitigated through optimized management practices.

The oxidation and corrosion control chemicals market is driven by the need to protect industrial infrastructure and equipment from damage caused by environmental factors such as moisture, temperature fluctuations, and chemical exposure. Corrosion inhibitors are more widely used than oxidation inhibitors, as corrosion is a pervasive issue across critical industries such as oil & gas, power generation, chemical processing, and manufacturing.

These chemicals are particularly crucial in industrial water treatment systems, where high temperatures and pressures accelerate wear on pipelines, turbines, and boilers. As industries push for more sustainable and eco-friendly solutions, there is a noticeable shift toward green inhibitors, driven by stringent environmental regulations and increased awareness of ecological impacts.

- The U.S. EPA’s 7th Drinking Water Infrastructure Needs Survey (2023) identifies a US$625 billion investment need for pipe replacement, treatment plant upgrades, storage tanks, and other key assets due to corrosion.

Asia Pacific emerges as the largest market, bolstered by rapid industrialization, significant infrastructure projects, and a growing demand in water-intensive sectors. In addition, geopolitical tensions, supply chain disruptions, and aging infrastructure influence the market dynamics, further emphasizing the demand for advanced corrosion control technologies.

Key Takeaways:

- The global oxidation and corrosion control chemicals market was valued at USD 14.7 billion in 2025.

- The global oxidation and corrosion control chemicals market is projected to grow at a CAGR of 6.4% and is estimated to reach USD 27.3 billion by 2035.

- Based on the product type, corrosion-control chemicals dominated the market, with a market share of around 82.4%.

- Among the end-uses of oxidation and corrosion control chemicals, the industrial water treatment industry held a major share in the market, 64.3% of the market share.

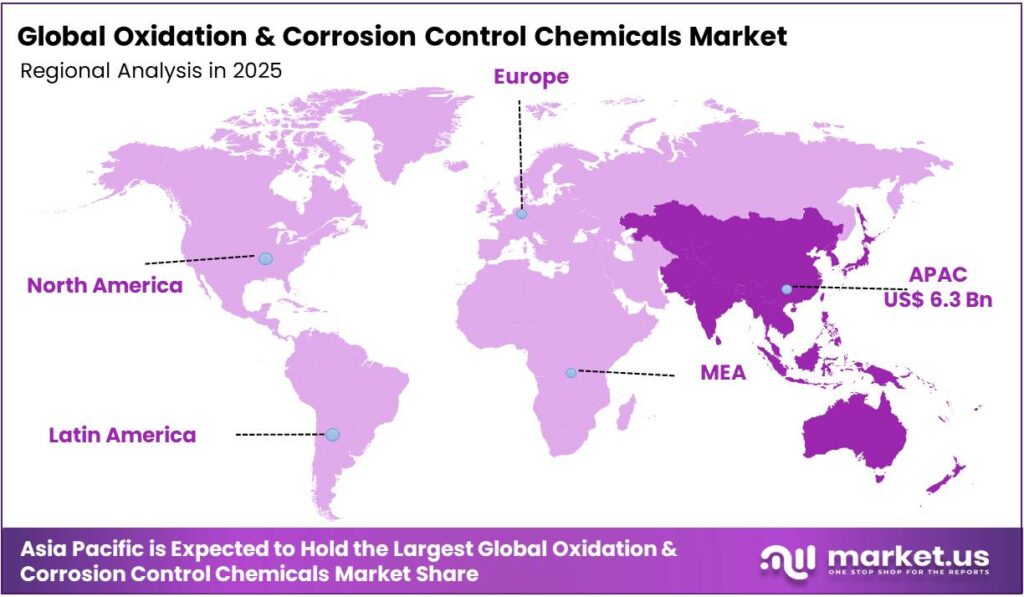

- In 2025, the Asia Pacific was the most dominant region in the oxidation and corrosion control chemicals market, accounting for around 42.6% of the total global consumption.

Product Type Analysis

Corrosion Control Chemicals Held the Largest Share in the Market.

The oxidation and corrosion control chemicals market is segmented based on product type into oxidation control chemicals and corrosion-control chemicals. The corrosion control chemicals dominated the market, comprising around 82.4% of the market share, primarily due to the broader and more frequent occurrence of corrosion in industrial settings. Corrosion, particularly in metals and alloys, is a widespread issue across industries such as oil & gas, power generation, and infrastructure, which are exposed to water, air, and other reactive substances.

The need to prevent corrosion to protect equipment, pipelines, and structures is critical to ensuring operational efficiency, safety, and longevity, driving the demand for these chemicals. In contrast, oxidation is more commonly a concern in specific applications, such as in certain food preservation, industrial coatings, and some chemical processes, limiting its widespread use. The extensive need for corrosion prevention in high-risk industries explains the broader adoption of corrosion control chemicals.

End-Use Analysis

The Oxidation and Corrosion Control Chemicals Are Mostly Utilized in Industrial Water Treatment.

Based on the end-uses of oxidation and corrosion control chemicals, the market is divided into municipal water treatment and industrial water treatment. The industrial water treatment sector dominated the market, with a market share of 64.3%, due to the different water quality requirements and the nature of the processes involved. Industrial water systems, especially in sectors such as power generation, oil & gas, and chemical processing, face high water temperatures, pressure, and chemical exposure, which accelerate corrosion and oxidation.

In contrast, municipal water treatment focuses primarily on ensuring safe drinking water through disinfection and filtration, where corrosion and oxidation issues are less prevalent. Additionally, the scale and cost of implementing specialized inhibitors in municipal systems are typically higher, making it less economically viable compared to industrial applications, where the risks and costs of equipment failure due to corrosion are far greater.

Key Market Segments:

By Product Type

- Oxidation Control Chemicals

- Potassium Permanganate

- Sodium Permanganate

- Hydrogen Peroxide

- Chlorine and Chlorine Compounds

- Others

- Corrosion-Control Chemicals

- Phosphates

- Others

By End-Use

- Municipal Water Treatment

- Industrial Water Treatment

- Pulp and Paper

- Mining

- Power Generation

- Oil and Gas

- Chemicals and Petrochemicals

- Food and Beverage

- Others

Drivers

Stricter Environmental & Safety Regulations Drive the Oxidation and Corrosion Control Chemicals Market.

Stricter environmental and safety regulations are significant drivers in the oxidation and corrosion control chemicals market. Regulatory bodies such as the U.S. Environmental Protection Agency (EPA) and the European Chemicals Agency (ECHA) impose stringent guidelines on the use and disposal of chemicals to minimize environmental impacts. For instance, EPA rules, such as the Lead and Copper Rule Improvements (LCRI), lower the lead action level to 10 ppb and require replacement of lead service lines by December 2037.

Similarly, EU REACH mandates registration for chemicals produced or imported over one ton annually, and restricts hazardous substances such as lead carbonates. These regulations push industries to adopt corrosion inhibitors and anti-oxidation chemicals that comply with these laws. In addition, regulations such as the Occupational Safety and Health Administration (OSHA) standards require safer chemical handling practices, particularly in industries such as oil and gas, which are significant consumers of such chemicals. The implementation of stricter rules results in higher demand for environmentally safer and more effective corrosion protection solutions.

Restraints

Economic and Operational Hurdles Might Hamper the Demand for Oxidation and Corrosion Control Chemicals.

Economic and operational hurdles significantly challenge the oxidation and corrosion control chemicals market. A primary issue is the fluctuating prices of raw materials, such as zinc, titanium, and phosphates, which are crucial for manufacturing corrosion inhibitors. According to the U.S. Geological Survey (USGS), the price of zinc has experienced volatility due to global supply chain disruptions, impacting production costs for corrosion-related chemicals.

- Under the U.S. EPA Lead and Copper Rule Improvements (LCRI), annual quantified costs for corrosion control technology are estimated between US$39.1 million and US$45.1 million.

Additionally, manufacturers face challenges in scaling production to meet regulatory compliance and increasing demand while maintaining cost-efficiency. The European Chemicals Agency (ECHA) has noted that complying with REACH regulations, including the testing and approval of new chemicals, can be expensive and time-consuming for manufacturers.

Moreover, the high costs associated with maintaining safety standards, such as those required by OSHA for chemical handling, add to operational complexity. These economic pressures, compounded by regulatory compliance costs, present substantial barriers to innovation and market expansion in the oxidation and corrosion control chemicals sector.

Opportunity

Industrial Expansion and Aging Water Infrastructure Create Opportunities in the Market.

Industrial expansion in water-intensive sectors, including oil & gas, power generation, and chemical processing, presents significant opportunities for the oxidation and corrosion control chemicals market. The oil and gas production and power generation rely heavily on water for cooling and extraction processes, making them prone to corrosion, increasing the demand for corrosion control chemicals. The International Energy Agency (IEA) notes that power generation alone accounts for nearly 50% of industrial water use globally, further stressing the need for effective corrosion inhibitors.

- According to a study by the EPA, aging water infrastructure, such as leaky pipes and water mains, is estimated to result in the loss of 2.1 trillion gallons of treated drinking water in the U.S. each year.

Moreover, aging water infrastructure, especially in developed nations, exacerbates corrosion-related issues. According to the American Water Works Association (AWWA), over 6 million miles of water pipelines in the U.S. are at risk of failure due to corrosion, urging the need for maintenance solutions. These challenges present growth prospects for chemical solutions that can extend the life of infrastructure and industrial systems by mitigating oxidation and corrosion, particularly in sectors with high water usage.

Trends

Rapid Shift Towards Sustainable and Green Inhibitors.

The rapid shift towards sustainable and green inhibitors is a significant trend in the oxidation and corrosion control chemicals market. This shift is primarily driven by increasingly stringent environmental regulations. The European Chemicals Agency (ECHA) and the U.S. Environmental Protection Agency (EPA) have pushed for the reduction of toxic substances in industrial chemicals, encouraging the adoption of more environmentally friendly corrosion inhibitors. For instance, the EPA’s Green Chemistry program promotes the development of safer, biodegradable alternatives.

Traditional corrosion inhibitors often contain heavy metals or toxic organic compounds that pose risks to aquatic life. Green inhibitors are increasingly derived from renewable biomass, including plant extracts utilizing phytochemicals such as alkaloids, tannins, and polyphenols, and biopolymers employing natural structures such as chitosan, cellulose, and lignin, which do not bioaccumulate.

Consequently, industries such as oil & gas and power generation are actively seeking corrosion inhibitors that meet these environmental standards. There is a rise in the use of eco-friendly corrosion control solutions in energy production systems, particularly in water-intensive applications cooling towers, where conventional inhibitors often have high environmental impacts.

Geopolitical Impact Analysis

Geopolitical Tensions Are Impacting the Oxidation and Corrosion Control Chemicals Market Due to Disrupted Supply Chains.

The geopolitical tensions are having a noticeable impact on the oxidation and corrosion control chemicals market, primarily through disruptions in supply chains and increased production costs. As evidenced by the U.S. Department of State, ongoing conflicts, such as the Russia-Ukraine war, have caused significant disruptions in the global supply of critical raw materials, including titanium and nickel, which are vital for the production of corrosion inhibitors.

These shortages, particularly in the European and North American markets, have led to volatility in material prices, with titanium prices rising significantly since the onset of the conflict. Additionally, sanctions and trade restrictions between countries such as the U.S. and China have resulted in delays in the import and export of essential chemical components, further complicating manufacturing processes.

The disruptions to the supply of rare earth metals, often used in corrosion-resistant alloys, have created supply bottlenecks. Furthermore, geopolitical instability influences investments in infrastructure and industrial development. According to the European Commission, the uncertainty has slowed large-scale projects, particularly in water-intensive industries such as oil & gas and power generation, where corrosion control is critical. This shift in priorities may delay demand for new chemical solutions.

Regional Analysis

Asia Pacific Held the Largest Share of the Global Oxidation and Corrosion Control Chemicals Market.

In 2025, the Asia Pacific dominated the global oxidation and corrosion control chemicals market, holding about 42.6% of the total global consumption, driven by the region’s robust industrial growth and increasing infrastructure investments. The rapid industrialization, particularly in China and India, has amplified the need for corrosion protection in sectors such as manufacturing, oil & gas, and power generation. China, as the world’s largest producer of steel and a major consumer of corrosion inhibitors, has seen significant demand due to its expansive infrastructure projects.

Additionally, the region’s water-intensive industries are major consumers of corrosion inhibitors for cooling systems and pipelines. Furthermore, the push for renewable energy projects in the region further increases the demand for sustainable and efficient corrosion control solutions. These factors position Asia Pacific as the dominant market in the global corrosion control chemicals sector.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Manufacturers of oxidation and corrosion control chemicals focus on product innovation, with a strong emphasis on developing more environmentally friendly and sustainable solutions that comply with increasingly strict regulations, such as REACH and EPA standards. Additionally, investment in research and development (R&D) is emphasized to create high-performance inhibitors tailored to specific industries, such as oil & gas or power generation.

Similarly, manufacturers pursue strategic partnerships with end-users to customize solutions for particular corrosion challenges. Furthermore, there is a focus on supply chain optimization to mitigate raw material price volatility and disruptions, while geographic expansion into emerging markets, particularly in the Asia Pacific, is another critical strategy to capture growing demand in industrial sectors.

The following are some of the major players in the industry

- Arkema

- BASF SE

- Buckman

- Chongqing Changyuan Group Limited

- Dow

- Ecolab Inc.

- Italmatch Chemicals

- Kemira

- Kurita Water Industries Ltd.

- Magnesia Chemicals LLP

- Nouryon

- Shannon Chemical Corp.

- SNF

- Solenis

- Solvay

- Universal Water Chemicals Pvt. Ltd.

- Veolia

- Veralto

- Xylem

- Other Key Players

Key Development

- In June 2025, Solenis and NCH Corporation announced that they entered into a definitive agreement under which Solenis acquired 100% of NCH’s shares, forming a customer-focused provider of water and hygiene solutions.

- In August 2025, SNF, a global leader in water-soluble polymers, completed the acquisition of Obsidian Chemical Solutions LLC, a Midland-based supplier of specialty chemicals serving the oil and gas sector. This acquisition strengthens SNF’s capabilities in delivering tailored chemical formulations for applications including stimulation, acidizing, drill-out operations, cementing, and water treatment.

Report Scope:

Report Features Description Market Value (2025) US$14.7 Bn Forecast Revenue (2035) US$27.3 Bn CAGR (2026-2035) 6.4% Base Year for Estimation 2025 Historic Period 2021-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product Type (Oxidation Control Chemicals and Corrosion-Control Chemicals), By End-Use (Municipal Water Treatment and Industrial Water Treatment) Regional Analysis North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA Competitive Landscape Arkema, BASF SE, Buckman, Chongqing Changyuan Group Limited, Dow, Ecolab Inc., Italmatch Chemicals, Kemira, Kurita Water Industries Ltd., Magnesia Chemicals LLP, Nouryon, Shannon Chemical Corp., SNF, Solenis, Solvay, Universal Water Chemicals Pvt. Ltd., Veolia, Veralto, Xylem, and Other Players. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)  Oxidation and Corrosion Control Chemicals MarketPublished date: Feb 2026add_shopping_cartBuy Now get_appDownload Sample

Oxidation and Corrosion Control Chemicals MarketPublished date: Feb 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Arkema

- BASF SE

- Buckman

- Chongqing Changyuan Group Limited

- Dow

- Ecolab Inc.

- Italmatch Chemicals

- Kemira

- Kurita Water Industries Ltd.

- Magnesia Chemicals LLP

- Nouryon

- Shannon Chemical Corp.

- SNF

- Solenis

- Solvay

- Universal Water Chemicals Pvt. Ltd.

- Veolia

- Veralto

- Xylem

- Other Key Players

Our Clients

- 179375

- Feb 2026