Global North America E-Bikes Market Size, Share, Growth Analysis, Propulsion Type (Pedal Assisted, Speed Pedelec, Throttle Assisted), Battery Type (Lithium-ion Battery, Lead Acid Battery, Others), Motor Placement (Hub (front/rear), Mid-drive), Drive Systems (Chain Drive, Belt Drive), Motor Power (Less than 250 W, 251 to 350 W, 351 to 500 W, 501 to 600 W, More than 600 W), Application Type (City/Urban, Cargo/Utility, Trekking/Mountain), End Use (Personal and Family Use, Commercial Delivery, Retail and Goods Delivery, Food and Beverage Delivery, Service Providers, Institutional, Others), Sales Channel (Offline, Online), Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Feb 2026

- Report ID: 178982

- Number of Pages: 376

- Format:

-

keyboard_arrow_up

Quick Navigation

- North America E-Bikes Market Overview

- Key Takeaways

- Propulsion Type Analysis

- Battery Type Analysis

- Motor Placement Analysis

- Drive Systems Analysis

- Motor Power Analysis

- Application Type Analysis

- End Use Analysis

- Sales Channel Analysis

- Key Market Segments

- Drivers

- Restraints

- Growth Factors

- Emerging Trends

- Key Company Insights

- Recent Developments

- Report Scope

North America E-Bikes Market Overview

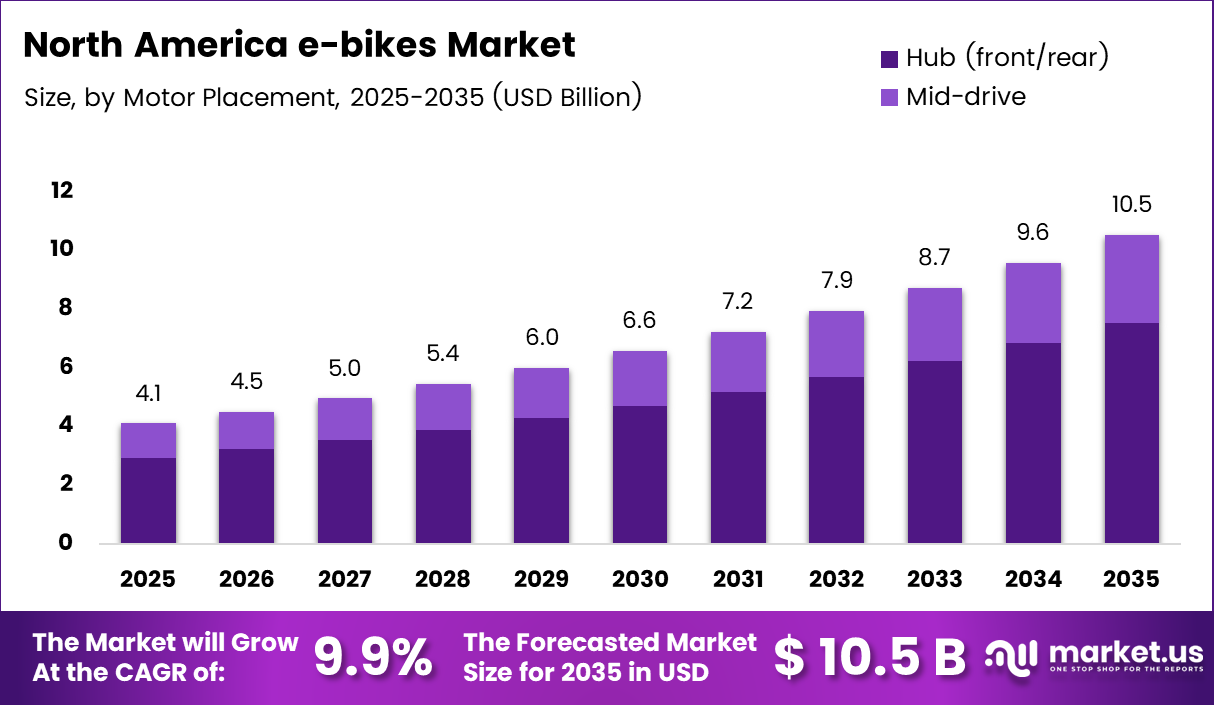

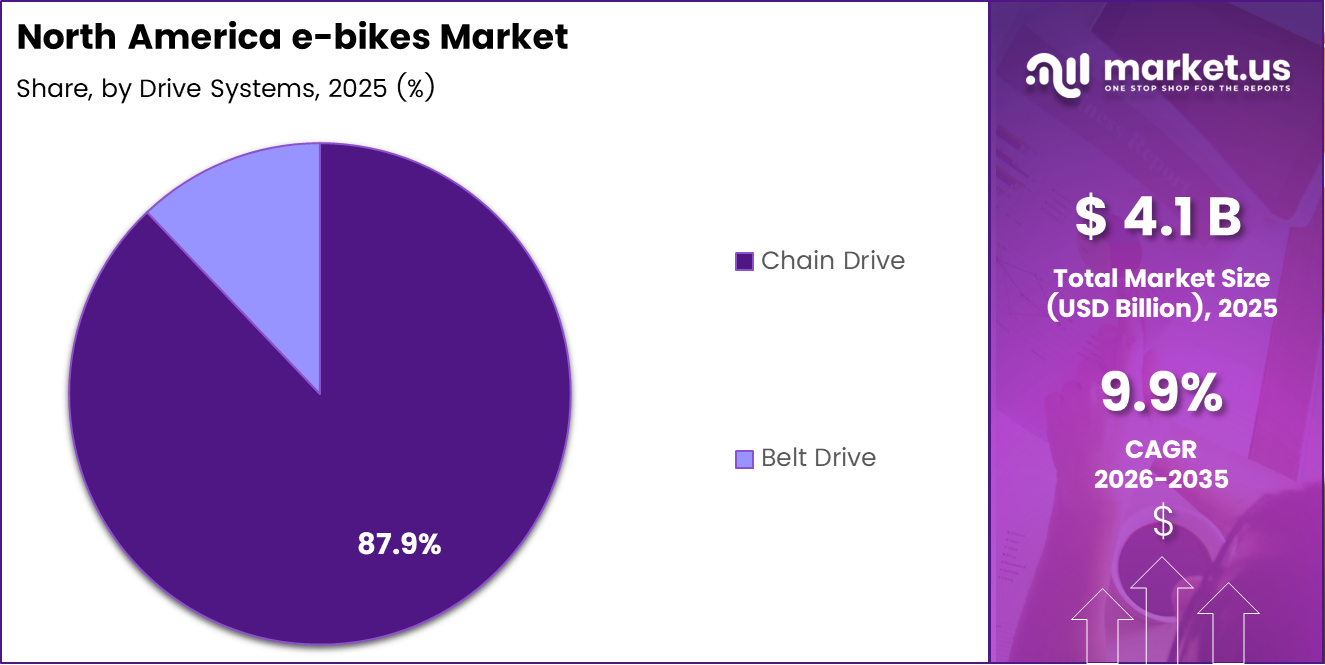

Global North America E-Bikes Market size is expected to be worth around USD 10.5 Billion by 2035 from USD 4.1 Billion in 2025, growing at a CAGR of 9.9% during the forecast period 2026 to 2035.

The North America e-bikes market refers to the industry encompassing electric bicycles equipped with pedal-assist or throttle-powered motors. These vehicles combine traditional cycling with battery-powered assistance, offering an efficient and sustainable mode of urban transportation. Most states define an e-bike as a bicycle with an electric motor less than 750 watts.

In North America, e-bikes are classified into three regulatory classes. Class 1 and Class 3 are pedal-assist only, with motor assistance up to 20 mph and 28 mph respectively. Class 2 supports both pedal-assist and throttle, providing assistance up to 20 mph. This classification framework helps regulate safe usage across states and provinces.

The market is experiencing strong growth driven by rising fuel prices, expanding urban cycling infrastructure, and growing health-conscious consumer behavior. Federal and state-level incentives supporting low-emission micro-mobility are further accelerating adoption. Consequently, e-bikes are becoming a preferred choice for daily urban commuting across major North American cities.

Government investment in sustainable transport infrastructure is creating a favorable policy environment for e-bike adoption. Bike lane expansions, tax credits, and emission reduction programs are actively supporting market growth. Moreover, commercial fleet operators and last-mile delivery businesses are increasingly integrating electric bicycles into their operations, unlocking new revenue streams.

According to Munich Re, most states classify an e-bike as having a motor not exceeding 750 watts and weighing 100 pounds or less. Additionally, data shows that 36% of e-bike-related injuries occur in children younger than 14, highlighting the need for better safety regulations and awareness programs in the region.

According to research cited by CAYIMBY, e-bikes offer 125% more carbon reduction potential than conventional bicycles. This significant environmental advantage is strengthening the case for wider adoption. Therefore, both individual consumers and institutional buyers are increasingly viewing e-bikes as a viable long-term mobility solution.

Key Takeaways

- The North America E-Bikes Market is valued at USD 4.1 Billion in 2025 and is projected to reach USD 10.5 Billion by 2035.

- The market is growing at a CAGR of 9.9% during the forecast period 2026 to 2035.

- By Propulsion Type, Pedal Assisted holds a dominant share of 58.3% in 2025.

- By Battery Type, Lithium-ion Battery leads with a market share of 89.1%.

- By Motor Placement, Hub (front/rear) dominates with a 71.4% share.

- By Drive Systems, Chain Drive holds the largest share at 87.9%.

- By Motor Power, the 251 to 350 W segment leads with a 38.2% share.

- By Application Type, City/Urban dominates with a 56.8% share.

- By End Use, Personal and Family Use accounts for 41.7% of the market.

- By Sales Channel, Offline sales lead with a 67.5% share.

Propulsion Type Analysis

Pedal Assisted dominates with 58.3% due to strong consumer preference for fitness-integrated commuting.

In 2025, Pedal Assisted held a dominant market position in the Propulsion Type segment of the North America E-Bikes Market, with a 58.3% share. This segment leads because riders value the natural cycling experience combined with motor support. Additionally, pedal-assist bikes comply with most state-level Class 1 and Class 3 regulations, making them widely accessible across urban and suburban areas.

Speed Pedelec is gaining momentum as a growing sub-segment within the propulsion category. These high-speed pedal-assist bikes are particularly popular among long-distance urban commuters. Consequently, their adoption is increasing in metro corridors where riders seek faster, regulation-compliant alternatives to conventional commuting options without needing a vehicle license.

Throttle Assisted e-bikes appeal to riders who prefer motor-only operation without continuous pedaling. This segment serves older consumers, delivery riders, and casual users who prioritize ease of use. However, regulatory restrictions in some states limit throttle-only usage, which has somewhat constrained broader adoption of this propulsion type across the region.

Battery Type Analysis

Lithium-ion Battery dominates with 89.1% due to superior energy density and long cycle life.

In 2025, Lithium-ion Battery held a dominant market position in the Battery Type segment of the North America E-Bikes Market, with an 89.1% share. These batteries deliver high energy density, lightweight design, and extended range, making them the preferred choice across all e-bike categories. Moreover, continuous innovation in lithium-ion technology is further improving charging speed and overall battery lifespan.

Lead Acid Battery remains a low-cost alternative used primarily in entry-level e-bike models. However, its heavier weight and shorter cycle life make it less competitive compared to lithium-ion options. Therefore, its market share continues to decline as consumers increasingly prioritize performance and range over initial purchase price in their buying decisions.

Others in this segment include emerging battery technologies such as solid-state and nickel-metal hydride variants. These technologies are currently at early development stages but show long-term promise for improving safety and sustainability. Additionally, ongoing research investments are expected to introduce newer battery alternatives into the North America e-bikes market over the coming years.

Motor Placement Analysis

Hub (front/rear) dominates with 71.4% due to cost efficiency and widespread model compatibility.

In 2025, Hub (front/rear) held a dominant market position in the Motor Placement segment of the North America E-Bikes Market, with a 71.4% share. Hub motors offer a simpler mechanical design and lower manufacturing cost, making them the standard choice across most consumer e-bike models. Moreover, their compatibility with a wide range of bicycle frames supports strong adoption across entry and mid-range segments.

Mid-drive motors are increasingly preferred by performance-oriented riders and mountain e-bike users. These motors deliver better weight distribution and more efficient power use, particularly on hilly terrain. Consequently, mid-drive systems are gaining traction among premium e-bike manufacturers targeting cyclists who demand a natural and responsive riding experience for both urban and off-road conditions.

Drive Systems Analysis

Chain Drive dominates with 87.9% due to cost-effectiveness and universal availability.

In 2025, Chain Drive held a dominant market position in the Drive Systems segment of the North America E-Bikes Market, with an 87.9% share. Chain drives are the industry standard due to their low cost, ease of maintenance, and compatibility with most e-bike motor systems. Additionally, the widespread availability of replacement parts and repair services across North America supports their continued market dominance.

Belt Drive systems are emerging as a premium alternative, offering cleaner operation and reduced maintenance requirements. These systems are particularly attractive for urban commuters who prioritize a low-maintenance ownership experience. However, higher manufacturing costs and limited compatibility with gear systems have restricted broader adoption, keeping belt drive as a niche option within the overall e-bike drive systems market.

Motor Power Analysis

251 to 350 W dominates with 38.2% due to optimal balance between performance and regulatory compliance.

In 2025, 251 to 350 W held a dominant market position in the Motor Power segment of the North America E-Bikes Market, with a 38.2% share. This power range aligns with Class 2 and Class 3 e-bike regulations in most states and delivers sufficient assistance for urban commuting. Moreover, these motors are energy-efficient and extend battery range, making them a top choice for daily riders across the region.

Less than 250 W motors serve entry-level riders and comply with the broadest set of state-level e-bike regulations across North America. These low-power systems are commonly found in recreational and casual-use e-bike models targeting first-time buyers. Additionally, their affordability makes them accessible to cost-sensitive consumer segments seeking a simple and practical introduction to electric bicycle ownership.

351 to 500 W motors target performance-oriented riders seeking more power for varied terrain and longer commuting distances. This segment is growing steadily alongside rising demand for cargo and trekking e-bike models. Consequently, manufacturers are expanding their mid-power motor offerings to meet the needs of riders who require stronger assistance without exceeding standard regulatory thresholds.

501 to 600 W motors are primarily used in specialized commercial delivery and heavy-duty utility e-bike applications requiring greater torque output. These motors support higher payload capacities, making them well suited for cargo-focused operators in urban logistics. However, regulatory restrictions in several states limit their use for standard on-road cycling, which constrains broader consumer adoption of this power category.

More than 600 W motors serve niche off-road, industrial, and high-performance e-bike applications that demand maximum power output. These systems are favored in rugged terrain environments where standard motor power levels are insufficient. Additionally, strict on-road usage restrictions in many North American jurisdictions mean this segment remains concentrated within specialized commercial and recreational off-road use cases rather than mainstream consumer markets.

Application Type Analysis

City/Urban dominates with 56.8% due to rising demand for sustainable daily commuting solutions.

In 2025, City/Urban held a dominant market position in the Application Type segment of the North America E-Bikes Market, with a 56.8% share. Urban e-bikes are purpose-built for daily city commuting, offering a practical and eco-friendly alternative to cars. Consequently, expanding bike lane infrastructure and growing traffic congestion in major cities are further accelerating adoption of urban e-bike models.

Cargo/Utility e-bikes are experiencing significant growth as businesses and families adopt them for goods transport and family mobility. This sub-segment is particularly gaining traction among small businesses seeking cost-efficient last-mile delivery options. Moreover, government incentives for commercial fleet electrification are encouraging more operators to integrate cargo e-bikes into their logistics networks across urban areas.

Trekking/Mountain e-bikes serve recreational and off-road users seeking performance-oriented models for trail and long-distance riding. This segment benefits from growing consumer interest in outdoor fitness activities and adventure travel. Additionally, improvements in motor power, suspension systems, and battery range are making trekking and mountain e-bikes increasingly capable and appealing to a broader range of active consumers.

End Use Analysis

Personal and Family Use dominates with 41.7% due to rising household adoption of sustainable mobility.

In 2025, Personal and Family Use held a dominant market position in the End Use segment of the North America E-Bikes Market, with a 41.7% share. Consumers are increasingly purchasing e-bikes as primary or supplemental transportation for daily errands, school commutes, and leisure riding. Moreover, the growing availability of family-friendly cargo e-bike models is broadening adoption among households with diverse mobility needs across urban and suburban areas.

Commercial Delivery operators are rapidly integrating e-bikes into their urban logistics networks to reduce fuel costs and improve delivery speed. The rise of same-day and on-demand delivery services is creating strong fleet demand across major North American cities. Additionally, government incentives supporting commercial fleet electrification are encouraging more logistics businesses to transition from conventional vehicles to electric bicycles.

Retail and Goods Delivery businesses are adopting e-bikes to navigate congested city streets more efficiently while lowering operational costs. These businesses benefit from the flexibility and lower maintenance requirements of electric bicycles compared to motor vehicles. Consequently, e-bikes are becoming a practical and cost-effective solution for small and mid-sized retail delivery operations across the region.

Food and Beverage Delivery platforms are among the fastest-growing adopters of e-bikes for urban order fulfillment. Riders benefit from faster navigation through traffic and lower per-delivery operating costs compared to motorcycles or cars. Moreover, the growing density of food delivery demand in metropolitan areas makes e-bikes an increasingly preferred choice for platform operators and independent delivery riders alike.

Service Providers such as maintenance contractors, utility field teams, and healthcare workers are deploying e-bikes to improve mobility in dense urban environments. E-bikes enable faster response times and reduced travel costs for service-oriented professionals. Additionally, their ability to access areas with vehicle restrictions makes them a highly practical mobility tool for a broad range of service provider use cases.

Institutional end users, including municipal agencies, universities, and campus operators, are deploying e-bike fleets for patrol, maintenance, and staff transportation functions. These organized fleet buyers contribute consistent and meaningful volume to the overall market. Furthermore, institutional procurement programs supported by sustainability mandates are accelerating structured fleet adoption across public sector and educational institutions throughout North America.

Others in this segment include tourism operators, event organizers, and hospitality businesses integrating e-bikes as experiential and guest mobility offerings. These buyers are diversifying the overall demand base beyond traditional commuter and delivery use cases. Consequently, the growing experiential economy and outdoor tourism sector are opening new commercial applications that are expected to expand further over the forecast period.

Sales Channel Analysis

Offline dominates with 67.5% due to consumer preference for in-store testing and expert guidance.

In 2025, Offline held a dominant market position in the Sales Channel segment of the North America E-Bikes Market, with a 67.5% share. Physical retail stores and specialty bicycle dealers remain the preferred buying channel, as consumers value the ability to test ride before purchasing. Additionally, in-store service support and financing options available at brick-and-mortar outlets strengthen offline sales performance across the region.

Online sales are growing rapidly as direct-to-consumer e-bike brands expand their smart retail presence. Consumers are increasingly comfortable purchasing e-bikes online, drawn by competitive pricing, home delivery, and customization options. Consequently, the online channel is expected to gain a larger share over the forecast period as brands invest in improved digital shopping experiences and virtual product demonstrations.

Key Market Segments

By Propulsion Type

- Pedal Assisted

- Speed Pedelec

- Throttle Assisted

By Battery Type

- Lithium-ion Battery

- Lead Acid Battery

- Others

By Motor Placement

- Hub (front/rear)

- Mid-drive

By Drive Systems

- Chain Drive

- Belt Drive

By Motor Power

- Less than 250 W

- 251 to 350 W

- 351 to 500 W

- 501 to 600 W

- More than 600 W

By Application Type

- City/Urban

- Cargo/Utility

- Trekking/Mountain

By End Use

- Personal and Family Use

- Commercial Delivery

- Retail and Goods Delivery

- Food and Beverage Delivery

- Service Providers

- Institutional

- Others

By Sales Channel

- Offline

- Online

Drivers

Government Incentives and Rising Fuel Costs Drive Strong E-Bike Market Growth

Federal and state-level incentives promoting low-emission micro-mobility are creating a strong policy foundation for e-bike adoption. These programs reduce purchase costs and encourage sustainable urban transport choices. Consequently, both individual commuters and institutional buyers are increasingly turning to e-bikes as a financially and environmentally viable transportation alternative.

Rising fuel prices are significantly improving the total cost of ownership advantage of electric bicycles over conventional vehicles. Commuters are recognizing the long-term savings associated with e-bike travel for daily urban commutes. Moreover, as gasoline prices remain volatile, the economic case for switching to electric bicycles continues to strengthen across major North American metropolitan areas.

Expansion of urban cycling infrastructure, including dedicated bike lanes and secure parking facilities, is making e-bike commuting more practical and safe. Additionally, a growing health-conscious population is favoring pedal-assist mobility for fitness-integrated daily travel. Therefore, these combined behavioral and infrastructure shifts are accelerating adoption and supporting sustained growth in the North America e-bikes market.

Restraints

High Upfront Costs and Regulatory Inconsistencies Limit Broader E-Bike Market Adoption

The high upfront cost of e-bikes compared to conventional bicycles remains a significant barrier to mass market penetration. Many entry-level consumers find the initial investment difficult to justify, particularly without strong financing options. Consequently, cost sensitivity among lower-income segments is limiting the rate at which e-bikes are being adopted across the broader North American population.

Regulatory inconsistencies across states and provinces regarding e-bike classification and usage create confusion for both consumers and retailers. Varying rules on motor power limits, age restrictions, and helmet requirements complicate product compliance and marketing. Therefore, manufacturers and brands operating across multiple jurisdictions must navigate a fragmented regulatory landscape that adds complexity to distribution and product development strategies.

These restraints collectively slow down the pace of market expansion, particularly in price-sensitive and underserved geographic segments. However, ongoing policy harmonization efforts at the federal level and increasing availability of affordable e-bike financing solutions are expected to gradually reduce these barriers. Moreover, growing consumer awareness may help overcome both the cost and regulatory challenges over the forecast period.

Growth Factors

Last-Mile Delivery Adoption and Smart Technology Integration Accelerate Market Expansion

Rapid adoption of e-bikes for last-mile delivery is creating significant commercial demand across the North America market. Logistics companies and delivery platforms are increasingly deploying electric bicycle fleets to reduce costs and improve urban delivery efficiency. Additionally, growing e-commerce volumes are pushing operators to find faster and more sustainable alternatives to traditional delivery vehicles in congested city environments.

Increasing demand for cargo and utility e-bikes among urban families and small businesses is expanding the market beyond individual commuters. These versatile models address practical needs such as grocery runs, school transport, and small-scale goods delivery. Consequently, cargo e-bike sales are growing at a faster pace as product designs improve and price points become more competitive for everyday buyers.

Integration of connected technologies and smart features such as GPS tracking, anti-theft systems, and app-based diagnostics is enhancing user experience. Moreover, rising penetration of e-bike subscription, leasing, and shared mobility business models is lowering access barriers. Therefore, these combined factors are broadening the consumer base and creating new revenue channels that support long-term growth in the North America e-bikes market.

Emerging Trends

Speed Pedelecs, Lightweight Batteries, and Direct-to-Consumer Models Reshape the E-Bike Market

Growing popularity of Class 3 speed pedelecs for long-distance urban commuting is reshaping consumer preferences in the North America e-bikes market. These high-speed models offer motor assistance up to 28 mph, making them ideal for riders covering longer daily distances. Moreover, regulatory acceptance of Class 3 bikes in more states is expanding their geographic reach and adoption rates.

A surge in lightweight lithium-ion battery innovations is improving range and reducing charging time for e-bike users. Manufacturers are investing in next-generation battery chemistries to deliver better performance at lower weights. Additionally, increasing consumer preference for fat tire and all-terrain e-bikes is driving demand for recreational models designed for diverse riding conditions beyond standard urban environments.

Expansion of direct-to-consumer e-bike brands leveraging online sales and customization models is transforming traditional retail dynamics. These brands offer competitive pricing, personalized configurations, and convenient home delivery. Consequently, the growing digital-first purchasing trend is encouraging more manufacturers to invest in online platforms, shifting how consumers discover, evaluate, and purchase e-bikes across North America.

Key Company Insights

Trek Bicycle Corporation is one of the most recognized names in the North America e-bikes market, offering a broad portfolio of electric bicycles for urban, recreational, and performance applications. The company has a strong dealer network across the United States and Canada. Moreover, Trek’s investment in bike-share infrastructure further reinforces its leadership position in the region’s sustainable urban mobility ecosystem.

Giant Manufacturing Co. is a globally integrated bicycle manufacturer with a significant presence in the North America e-bikes market. The company offers a wide range of pedal-assist and performance e-bike models across multiple price points. Additionally, Giant’s vertically integrated supply chain gives it a competitive cost advantage, enabling consistent product quality and broad market accessibility for both entry-level and premium buyers.

Rad Power Bikes has established itself as a leading direct-to-consumer e-bike brand in North America, known for offering feature-rich Class 2 electric bicycles at accessible price points. The company exclusively produces Class 2 models with batteries lasting 45 to 50 miles per charge. Consequently, its online-first retail model and strong customer service reputation have built a loyal and rapidly growing consumer base.

Specialized Bicycle Components is a premium e-bike manufacturer with a strong focus on performance-oriented electric mountain and road bikes. The company invests heavily in motor, battery, and frame technology to deliver industry-leading riding experiences. Moreover, Specialized maintains a robust global dealer network and brand presence that supports its competitive positioning in the higher-end segment of the North America e-bikes market.

Key players

- Trek Bicycle Corporation

- Giant Manufacturing Co.

- Rad Power Bikes

- Specialized Bicycle Components

- Cycling Sports Group, Inc. (Cannondale)

- Ride Aventon Inc.

- Yamaha Bicycles

- Bosch eBike Systems

- Shimano Inc.

- Riese and Müller

Recent Developments

- August 2025 – ENVO Drive acquired the iconic MoonBikes brand, marking a strategic expansion into winter electric snow mobility. This move strengthens ENVO Drive’s leadership position in the broader electric micro-mobility segment and diversifies its product portfolio beyond conventional e-bike offerings.

- September 2024 – Bicycle Transit Systems announced plans to acquire BCycle, a bike-share company, from Trek Bicycle Corporation. This acquisition positions Bicycle Transit Systems as a stronger player in the North American shared urban mobility and e-bike infrastructure market.

- June 2025 – Bird unveiled an enhanced fleet of scooters and e-bikes designed to meet growing demand for smarter urban mobility solutions. The updated fleet incorporates improved technology and design features aimed at increasing rider safety, comfort, and operational efficiency across Bird’s urban service network.

Report Scope

Report Features Description Market Value (2025) USD 4.1 Billion Forecast Revenue (2035) USD 10.5 Billion CAGR (2026-2035) 9.9% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered Propulsion Type (Pedal Assisted, Speed Pedelec, Throttle Assisted), Battery Type (Lithium-ion Battery, Lead Acid Battery, Others), Motor Placement (Hub (front/rear), Mid-drive), Drive Systems (Chain Drive, Belt Drive), Motor Power (Less than 250 W, 251 to 350 W, 351 to 500 W, 501 to 600 W, More than 600 W), Application Type (City/Urban, Cargo/Utility, Trekking/Mountain), End Use (Personal and Family Use, Commercial Delivery, Retail and Goods Delivery, Food and Beverage Delivery, Service Providers, Institutional, Others), Sales Channel (Offline, Online) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Trek Bicycle Corporation, Giant Manufacturing Co., Rad Power Bikes, Specialized Bicycle Components, Cycling Sports Group, Inc. (Cannondale), Ride Aventon Inc., Yamaha Bicycles, Bosch eBike Systems, Shimano Inc., Riese and Müller Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  North America e-bikes MarketPublished date: Feb 2026add_shopping_cartBuy Now get_appDownload Sample

North America e-bikes MarketPublished date: Feb 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Trek Bicycle Corporation

- Giant Manufacturing Co.

- Rad Power Bikes

- Specialized Bicycle Components

- Cycling Sports Group, Inc. (Cannondale)

- Ride Aventon Inc.

- Yamaha Bicycles

- Bosch eBike Systems

- Shimano Inc.

- Riese and Müller

Our Clients

- 178982

- Feb 2026