Global Non-Evaporable Getter (NEG) Pumps Market Size, Share, Growth Analysis Product Type (Cartridge NEG Pumps, Modular NEG Pumps, Others), Pressure Range (Ultra-High Vacuum (UHV) Pumps, High Vacuum Pumps), Application (Pharmaceutical and Chemical, Industrial and Manufacturing, Electronics and Telecommunication, Others), Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Mar 2026

- Report ID: 181268

- Number of Pages: 311

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

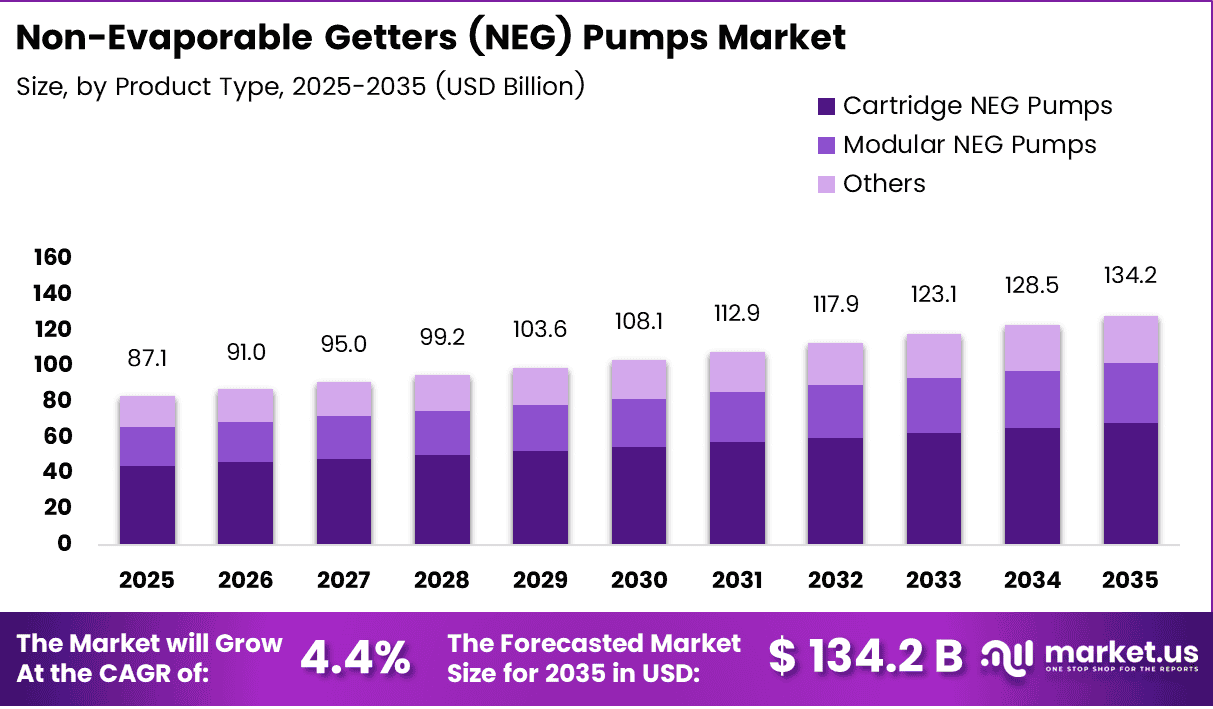

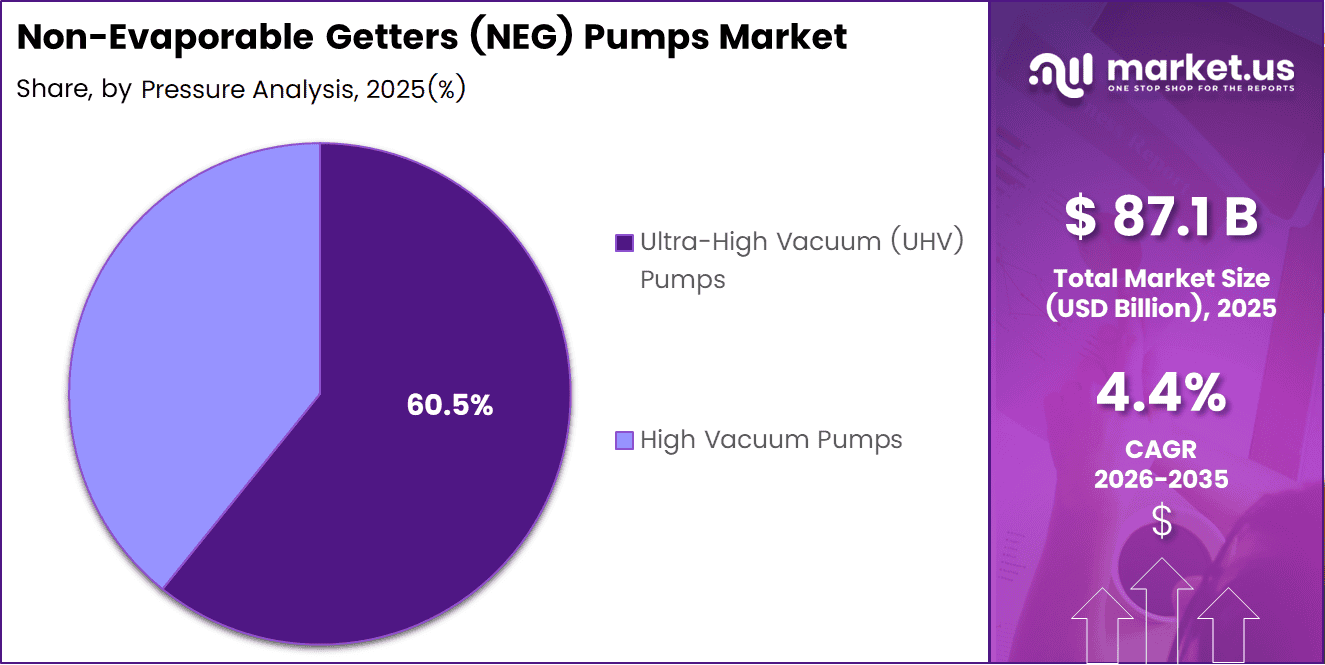

Global Non-Evaporable Getter (NEG) Pumps Market size is expected to be worth around USD 134.2 Billion by 2035 from USD 87.1 Billion in 2025, growing at a CAGR of 4.4% during the forecast period 2026 to 2035.

Non-Evaporable Getter (NEG) pumps are advanced vacuum solutions that use porous metallic alloys to sorb active gas molecules. They maintain ultra-high vacuum conditions by forming stable compounds with residual gases. Moreover, their ability to reduce chamber pressure to less than 10⁻¹² mbar makes them essential in precision environments.

NEG pumps are primarily composed of alloys containing zirconium, vanadium, titanium, aluminium, and iron. They operate through surface sorption without any moving parts or electrical connections. Consequently, they offer a clean, low-maintenance alternative to traditional mechanical or turbomolecular pumps in sensitive vacuum applications.

The market is witnessing strong growth driven by rising demand in particle accelerators, semiconductor fabrication, and fusion energy research. Governments and research institutions are increasing funding for large-scale physics infrastructure projects. Additionally, the rapid expansion of semiconductor manufacturing in Asia Pacific is creating sustained demand for NEG-based vacuum solutions.

Regulatory frameworks supporting clean energy research and advanced manufacturing are encouraging wider NEG adoption. Fusion energy programs in Europe and North America are receiving record public investment. Therefore, NEG pump manufacturers are scaling production capacity and developing new alloy formulations to meet emerging industrial needs.

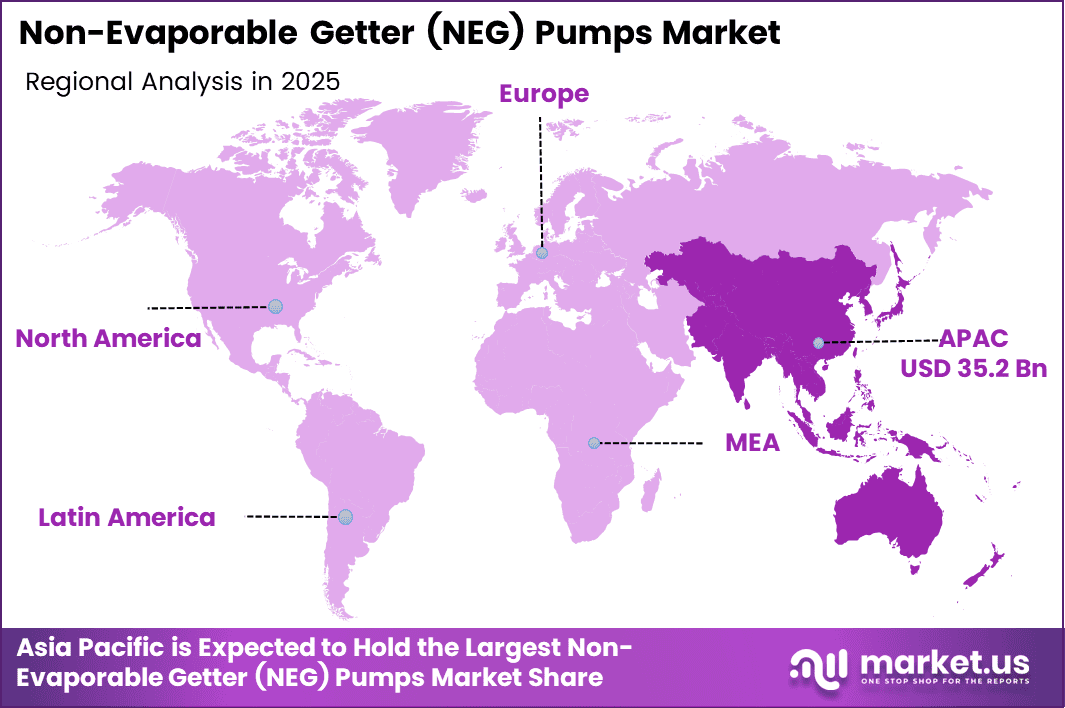

According to recent market data, Asia Pacific holds a dominant regional share of 40.5%, valued at approximately USD 35.2 Billion. The Tubegetter variant activates at temperatures from 550 K and operates between 0 and 800 K under HV/UHV conditions, expanding its usability across diverse industrial sectors.

Common NEG alloys such as St 707, containing 70% zirconium, and St 101, with 84% zirconium and 16% aluminium, demonstrate the material precision required in this market. Furthermore, ongoing R&D in zirconium-vanadium-iron alloy optimization is pushing activation performance toward lower temperatures, expanding application scope globally.

Key Takeaways

- The global NEG Pumps Market is projected to reach USD 134.2 Billion by 2035.

- Asia Pacific dominates the market with a 40.5% regional share.

- By Product Type, Cartridge NEG Pumps hold a leading share of 50.8%.

- By Pressure Range, Ultra-High Vacuum (UHV) Pumps account for 60.5% of the market.

- By Application, Electronics and Telecommunication holds a 35.6% share.

- NEG coatings can reduce pressure to less than 10⁻¹² mbar in HV/UHV conditions.

- The Tubegetter activates at temperatures starting from 550 K and operates up to 800 K.

Product Type Analysis

Cartridge NEG Pumps dominates with 50.8% due to compact design and ease of integration in vacuum systems.

In 2025, Cartridge NEG Pumps held a dominant market position in the Product Type segment of the Non-Evaporable Getter (NEG) Pumps Market, with a 50.8% share. Their compact form factor and straightforward installation make them the preferred choice across particle accelerators, semiconductor equipment, and analytical instruments requiring reliable ultra-high vacuum performance.

Modular NEG Pumps represent a growing segment valued for their scalability and flexibility in large vacuum systems. These pumps allow users to expand pumping capacity by adding modules without replacing entire assemblies. Consequently, they are gaining traction in industrial manufacturing and fusion research facilities where system upgrades are frequently required.

Others in this segment include customized and application-specific NEG pump configurations developed for niche use cases. These include thin-film getter systems for microelectronics packaging and tubegetter variants for narrow, hard-to-pump spaces. Additionally, this sub-segment is expanding as new industries adopt vacuum technology for advanced process applications.

Pressure Range Analysis

Ultra-High Vacuum (UHV) Pumps dominates with 60.5% due to widespread use in scientific research and semiconductor manufacturing.

In 2025, Ultra-High Vacuum (UHV) Pumps held a dominant market position in the Pressure Range segment of the Non-Evaporable Getter (NEG) Pumps Market, with a 60.5% share. Their ability to sustain pressure below 10⁻⁹ mbar makes them indispensable in particle physics, space simulation, and advanced lithography applications demanding the highest vacuum integrity.

High Vacuum Pumps serve a broad range of industrial and research applications where moderate vacuum levels are sufficient. They are widely used in coating systems, electron microscopy, and industrial drying processes. Moreover, their lower cost and simpler activation requirements make them accessible to a wider range of manufacturers and research facilities globally.

Application Analysis

Electronics and Telecommunication dominates with 35.6% due to high demand in semiconductor fabrication and display manufacturing.

In 2025, Electronics and Telecommunication held a dominant market position in the Application segment of the Non-Evaporable Getter (NEG) Pumps Market, with a 35.6% share. NEG pumps are critical in semiconductor wafer fabrication, thin-film deposition, and flat panel display production, where maintaining contamination-free ultra-high vacuum environments is essential to product quality.

Pharmaceutical and Chemical applications leverage NEG pump technology for controlled environment processing and analytical instrument operation. These sectors require consistent vacuum performance for drug synthesis, chromatography, and mass spectrometry systems. Additionally, growing biopharmaceutical production capacity worldwide is contributing to steady demand growth in this application segment.

Industrial and Manufacturing represents a broad application base including vacuum metallurgy, heat treatment, and coating equipment. NEG pumps help eliminate active gas contamination in production processes requiring clean vacuum conditions. Furthermore, automation-driven upgrades in manufacturing facilities are accelerating replacement cycles for older vacuum systems with more efficient NEG-based alternatives.

Others include emerging applications in quantum computing, fusion energy, and medical imaging. These sectors require specialized vacuum environments that standard pumps cannot reliably maintain. Consequently, NEG pump developers are actively designing solutions tailored to the specific pressure and temperature requirements of these high-growth application areas.

Key Market Segments

Product Type

- Cartridge NEG Pumps

- Modular NEG Pumps

- Others

Pressure Range

- Ultra-High Vacuum (UHV) Pumps

- High Vacuum Pumps

Application

- Pharmaceutical and Chemical

- Industrial and Manufacturing

- Electronics and Telecommunication

- Others

Drivers

Surging Demand for Ultra-High Vacuum Environments and Semiconductor Fabrication Drives NEG Pump Market Growth

The growing deployment of next-generation particle accelerators and synchrotron facilities is creating strong demand for reliable NEG pump solutions. Research programs in nuclear fusion and high-energy physics require sustained sub-atmospheric pressure stability. Consequently, procurement of advanced vacuum systems has increased significantly across publicly funded scientific institutions worldwide.

NEG technology is becoming integral to semiconductor wafer fabrication and advanced lithography equipment. As chip manufacturers push toward smaller process nodes, contamination-free vacuum environments are increasingly critical. Moreover, the global semiconductor capacity expansion, particularly in Asia Pacific and North America, is directly translating into higher NEG pump installations across fab facilities.

Space simulation and satellite testing applications are also accelerating NEG adoption. Aerospace agencies and private space companies require highly reliable vacuum environments to replicate orbital conditions. Therefore, rising investments in satellite manufacturing and launch infrastructure are contributing a growing share of demand to the NEG pump market globally.

Restraints

High Reactivation Costs and Limited Sorption Capacity Constrain Widespread NEG Pump Adoption

One of the primary challenges in the NEG pump market is the high cost associated with thermal reactivation cycles in continuous industrial operations. Regenerating getter materials requires controlled heating processes that can disrupt production schedules. Consequently, end-users in high-throughput manufacturing environments may delay system upgrades or seek alternative vacuum solutions with lower maintenance requirements.

Limited sorption capacity and pumping speed present significant scalability constraints for large-volume vacuum chambers. As industrial applications grow in physical scale, a single NEG unit often cannot meet the total gas load requirements. Moreover, designing distributed getter arrays to compensate adds engineering complexity and cost, reducing the economic appeal of NEG solutions for large-scale deployments.

The specialized nature of NEG alloy formulations also creates supply chain dependencies on critical raw materials such as zirconium and vanadium. Price volatility and geopolitical concentration of these metals can disrupt production planning. Therefore, manufacturers face ongoing pressure to qualify alternative alloy compositions or develop more material-efficient getter designs to mitigate supply risk.

Growth Factors

Quantum Computing, Fusion Energy, and MEMS Integration Unlock New Growth Avenues for NEG Pumps

The rapid expansion of quantum computing hardware is creating new demand for cryogenic ultra-high vacuum environments where NEG pumps offer a reliable solution. Quantum processors require extremely low-pressure conditions to minimize decoherence. Consequently, quantum technology developers are actively evaluating NEG pump integration as a standard component in next-generation computing infrastructure.

Fusion energy programs globally are investing in large-scale NEG pump arrays capable of handling hydrogen pumping speeds in the thousands of cubic meters per second. Recent advances in zirconium-vanadium-titanium-aluminium alloys have made large modular NEG pumps viable for fusion reactor environments. Moreover, government funding for fusion research is reaching record levels across the US, Europe, and Asia.

The miniaturization trend in electronics is driving interest in NEG integration within MEMS-based vacuum devices and compact medical imaging systems. Applications in PET scanners and MRI accelerator components require stable, maintenance-light vacuum solutions. Additionally, multi-layer NEG thin film architectures are being developed to extend pump lifetime in these demanding and space-constrained environments.

Emerging Trends

Advanced Alloy Development, Distributed Pump Arrays, and Sustainable Manufacturing Reshape the NEG Pump Market

R&D investment in zirconium-vanadium-iron alloy optimization is accelerating, with the goal of enabling effective NEG activation at lower temperatures. New alloy formulations like ZAO demonstrate higher pumping speeds and greater resistance to embrittlement over multiple reactivation cycles. Moreover, this trend is expanding the operational range of NEG pumps into applications previously dominated by conventional vacuum equipment.

A notable shift is underway from single turbomolecular pump configurations to distributed NEG pump arrays in beamline and accelerator systems. This approach improves pumping uniformity along long vacuum vessels and reduces overall system complexity. Additionally, in-situ NEG reactivation protocols are being widely adopted to minimize scheduled downtime in high-throughput industrial and research vacuum processing lines.

Sustainability is becoming a key factor in NEG manufacturing strategy. Producers are investing in processes that reduce rare-metal waste and improve material recovery from spent getter units. Furthermore, a new NEG pump geometry developed in March 2026, validated through Monte Carlo simulations, demonstrates enhanced pumping efficiency for fusion reactors, accelerators, synchrotrons, and extreme ultraviolet photolithography systems.

Regional Analysis

Asia Pacific Dominates the Non-Evaporable Getter (NEG) Pumps Market with a Market Share of 40.5%, Valued at USD 35.2 Billion

Asia Pacific leads the global NEG Pumps Market with a commanding share of 40.5%, valued at USD 35.2 Billion. The region’s dominance is driven by rapid semiconductor manufacturing expansion in China, South Korea, Japan, and Taiwan. Moreover, increasing government investment in scientific research infrastructure, particle physics, and fusion energy programs is further accelerating regional demand for advanced vacuum solutions.

North America Non-Evaporable Getter (NEG) Pumps Market Trends

North America represents a significant market supported by major national laboratories, defense research programs, and a robust semiconductor industry. The United States is a global leader in fusion energy investment and particle accelerator development. Additionally, growing adoption of NEG technology in aerospace testing and quantum computing facilities is contributing to steady market growth across the region.

Europe Non-Evaporable Getter (NEG) Pumps Market Trends

Europe holds a strong position in the NEG pump market, driven by world-class physics research institutions such as CERN and numerous national synchrotron facilities. Germany, France, and the UK are key contributors to regional vacuum technology demand. Furthermore, the European Union’s increased funding for clean energy research, including fusion and advanced manufacturing, is sustaining market momentum.

Latin America Non-Evaporable Getter (NEG) Pumps Market Trends

Latin America remains a smaller but developing market for NEG pump technology, with Brazil leading regional adoption in industrial manufacturing and research applications. Growing investments in electronics production and pharmaceutical processing are creating new demand drivers. However, market growth is moderated by limited domestic manufacturing capability and reliance on imported vacuum equipment and components.

Middle East and Africa Non-Evaporable Getter (NEG) Pumps Market Trends

The Middle East and Africa market is at an early stage of NEG pump adoption, with demand primarily emerging from industrial manufacturing and petrochemical processing sectors. Gulf Cooperation Council countries are investing in advanced manufacturing infrastructure as part of economic diversification programs. Consequently, demand for high-performance vacuum solutions including NEG pumps is expected to grow steadily over the forecast period.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

SAES Getters S.p.A. is the global leader in non-evaporable getter technology, offering a comprehensive portfolio of NEG pumps, coatings, and alloy materials. The company’s ZAO alloy formulation sets industry benchmarks for pumping speed and reactivation durability. Moreover, its recent acquisition by S.G.G. Holding and purchase of FMB Berlin reinforce its dominant position in the UHV market for particle accelerators and synchrotrons.

Edwards Vacuum is a major player in the NEG pump market, known for its hybrid vacuum solutions that combine getter and ion pump technologies. The company’s HyTan NEG-Ion Pump delivers high pumping speeds across a broad range of gases including hydrogen and noble gases. Additionally, Edwards leverages its global service network to support semiconductor and industrial customers across Asia Pacific, Europe, and North America.

Agilent Technologies provides NEG pump solutions primarily targeted at analytical instrumentation and scientific research applications. The company integrates getter technology into mass spectrometry, electron microscopy, and surface analysis systems. Furthermore, Agilent’s strong R&D capability and established relationships with leading research institutions position it as a reliable supplier in the high-precision vacuum technology segment.

Leybold GmbH, operating under the Atlas Copco group, offers a broad range of vacuum solutions including NEG-compatible systems for semiconductor, coating, and industrial applications. The company benefits from Atlas Copco’s global manufacturing and distribution infrastructure. Consequently, Leybold is well-positioned to serve growing demand in Asia Pacific and European markets where vacuum technology adoption in advanced manufacturing is accelerating.

Key Players

- SAES Getters S.p.A.

- Edwards Vacuum

- Agilent Technologies

- Leybold GmbH

- Gamma Vacuum

- Riber S.A.

- Osaka Vacuum Ltd.

- Pfeiffer Vacuum GmbH

- VACOM Vakuum Komponenten and Messtechnik GmbH

- Nor-Cal Products Inc.

Recent Developments

- March 2026 – A new NEG pump geometry was developed to exploit the topological enhancement effect, validated through systematic Monte Carlo simulations. The novel design is applicable to nuclear fusion reactors, particle accelerators, synchrotrons, and extreme ultraviolet photolithography systems, with the enhancement factor increasing as the sticking coefficient decreases.

- April 2024 – SAES Getters S.p.A. signed a binding Share Purchase Agreement to acquire 100% of FMB Feinwerk- und Messtechnik GmbH (FMB Berlin), a specialist in components and scientific instrumentation for synchrotrons and particle accelerators since 1990. The acquisition strengthens SAES Group’s leadership in the ultra-high vacuum sector for accelerator applications.

Report Scope

Report Features Description Market Value (2025) USD 87.1 Billion Forecast Revenue (2035) USD 134.2 Billion CAGR (2026-2035) 4.4% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered Product Type (Cartridge NEG Pumps, Modular NEG Pumps, Others), Pressure Range (Ultra-High Vacuum (UHV) Pumps, High Vacuum Pumps), Application (Pharmaceutical and Chemical, Industrial and Manufacturing, Electronics and Telecommunication, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape SAES Getters S.p.A., Edwards Vacuum, Agilent Technologies, Leybold GmbH, Gamma Vacuum, Riber S.A., Osaka Vacuum Ltd., Pfeiffer Vacuum GmbH, VACOM Vakuum Komponenten and Messtechnik GmbH, Nor-Cal Products Inc. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Pumps Market") Non-Evaporable Getter (NEG) Pumps MarketPublished date: Mar 2026add_shopping_cartBuy Now get_appDownload Sample

Non-Evaporable Getter (NEG) Pumps MarketPublished date: Mar 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- SAES Getters S.p.A.

- Edwards Vacuum

- Agilent Technologies

- Leybold GmbH

- Gamma Vacuum

- Riber S.A.

- Osaka Vacuum Ltd.

- Pfeiffer Vacuum GmbH

- VACOM Vakuum Komponenten and Messtechnik GmbH

- Nor-Cal Products Inc.

Our Clients

- 181268

- Mar 2026