Global Natural Food Preservatives Market Size, Share Analysis Report By Product (Edible Oil, Rosemary Extracts, Natamycin, Vinegar, Chitosan, Others), By Function (Antimicrobial, Antioxidant), By Application (Seafood, Meat And Poultry Products, Bakery Products, Dairy Products, Beverages, Snacks, Fruits And Vegetables, Others) , By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2026-2035

- Published date: Mar 2026

- Report ID: 181529

- Number of Pages: 263

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

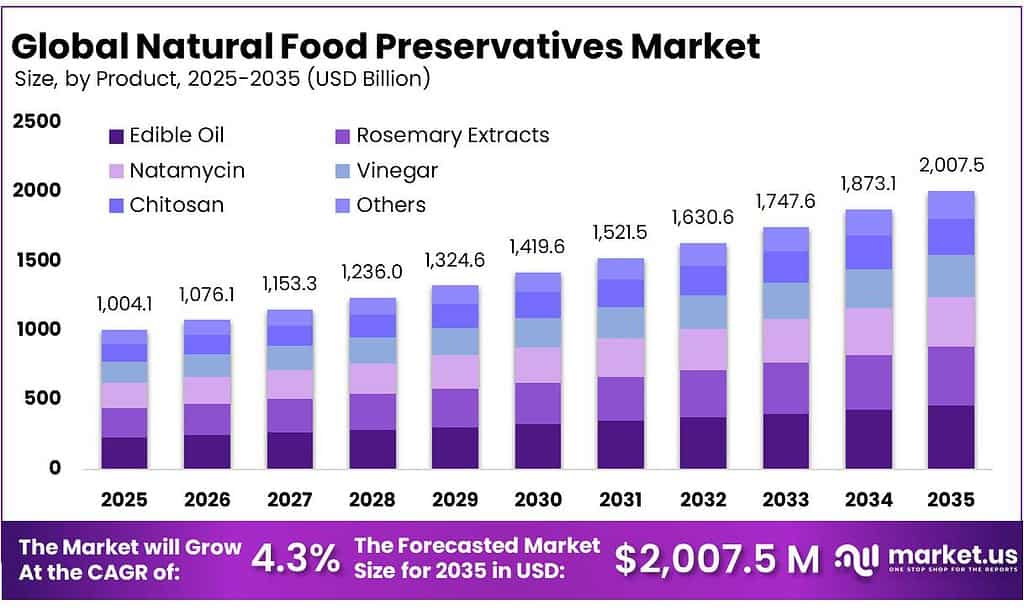

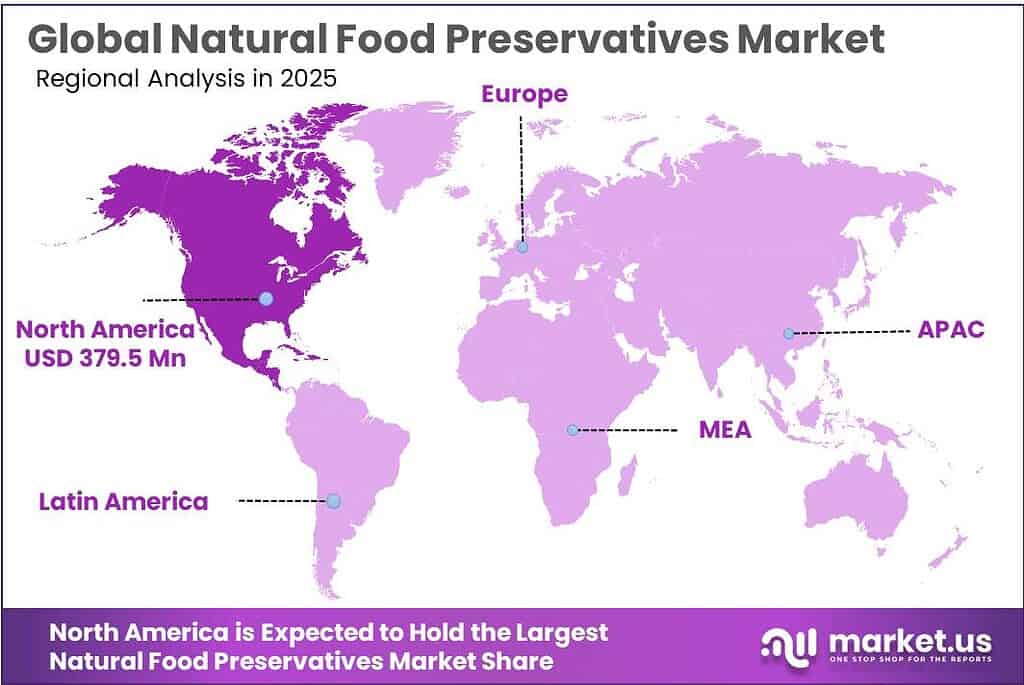

The Global Natural Food Preservatives Market size is expected to be worth around USD 2,007.5 Million by 2035, from USD 1,004.1 Million in 2025, growing at a CAGR of 7.2% during the forecast period from 2026 to 2035. In 2025, North America held a dominant market position, capturing more than a 37.8% share, holding USD 379.5 Million revenue.

Natural food preservatives are moving from a niche formulation choice to a strategic requirement across the global food value chain. The category is being shaped by two structural pressures: shelf-life extension and food safety. FAO states that 13.2% of food is lost between harvest and retail, while another 19% is wasted at retail, food service, and household level; separately, WHO estimates that unsafe food causes 600 million illnesses and 420,000 deaths every year.

The industrial scenario is increasingly led by ingredient platforms that combine scale, regulatory capability, and application know-how. Naturex S.A., now integrated into Givaudan, entered the group with EUR 405 million in 2017 sales, 16 production sites, and 1,700 employees; this matters because Givaudan’s Taste & Wellbeing division later reached CHF 3,752 million in 2024 sales, showing how botanical and natural-ingredient capabilities have become part of a much larger global solutions engine. Handary, founded in Brussels in 2009, states that it has designed 26 natural shelf-life ingredient brands. Cargill adds industrial depth with 160,000+ employees, operations in 70 countries, service to 125 countries, and $160 billion in fiscal 2024 revenue.

In the European Union, the 2025 amendment of the Waste Framework Directive introduced binding 2030 targets requiring a 10% reduction of food waste in processing and manufacturing and a 30% per-capita reduction at retail and consumption stages. In the United States, FDA’s food traceability rule framework continues to push faster identification and removal of contaminated products, and a 2025 proposal would move compliance from January 20, 2026 to July 20, 2028, giving industry more time to build interoperable systems.

The FDA refreshed its Food Labeling Guide on 15 January 2025, underscoring that manufacturers must stay current as regulations change, while the UK Food Standards Agency updated its food-additives guidance on 16 July 2025, reiterating that preservatives are used to keep food safer for longer and that additives are safety-assessed before use. In the EU, 2025 amendments continued to update the additive framework under Regulation (EC) No 1333/2008. Together, these government-led actions are pushing formulators toward traceable, label-friendly preservation systems with stronger technical documentation.

Cargill, while broader than preservatives alone, announced in July 2025 a regenerative agriculture collaboration spanning 240,000 acres through 2030, a move that can strengthen long-term plant-derived ingredient supply chains. Collectively, these developments support a positive medium-term outlook for natural food preservatives.

Key Takeaways

- Natural Food Preservatives Market size is expected to be worth around USD 2,007.5 Million by 2035, from USD 1,004.1 Million in 2025, growing at a CAGR of 7.2%.

- Edible Oil held a dominant market position, capturing more than a 23.7% share.

- Antimicrobial held a dominant market position, capturing more than a 67.1% share.

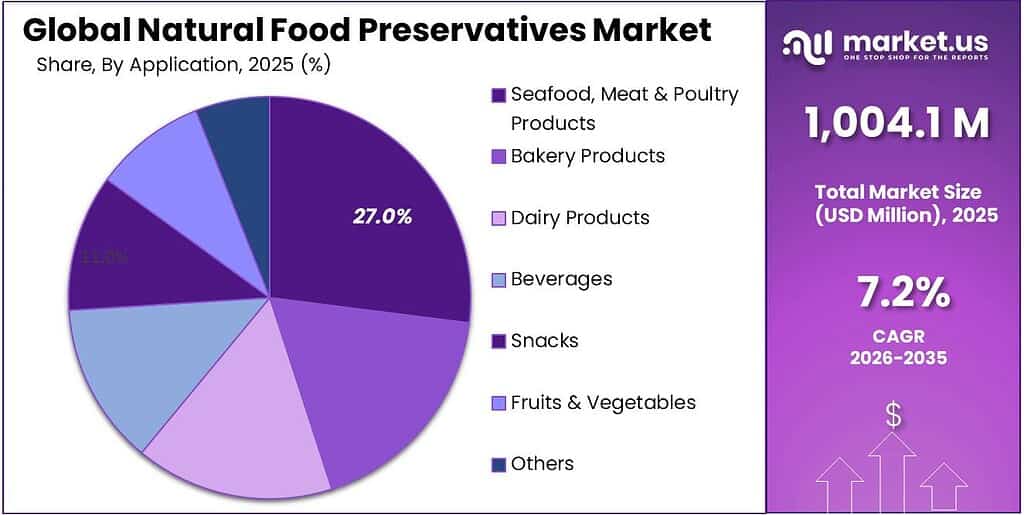

- Seafood, Meat & Poultry Products held a dominant market position, capturing more than a 27.4% share.

- North America emerged as the dominating region in the natural food preservatives market, accounting for nearly 37.8% share, valued at around USD 379.5 million.

By Product Analysis

Edible Oil dominates with 23.7% share driven by oxidation control needs and extended shelf life

In 2025, Edible Oil held a dominant market position, capturing more than a 23.7% share. This segment continues to lead because oils and fats are highly prone to oxidation, which directly affects taste, aroma, and safety. As a result, food manufacturers are increasingly relying on natural preservatives such as tocopherols, rosemary extract, and green tea extract to maintain product stability. The demand is especially strong in packaged snacks, processed foods, and ready-to-eat meals where oil stability plays a critical role in shelf life. Clean-label expectations are also pushing producers to replace synthetic antioxidants with plant-based alternatives.

By Function Analysis

Antimicrobial leads strongly with 67.1% share as food safety remains top priority

In 2025, Antimicrobial held a dominant market position, capturing more than a 67.1% share. This segment is leading mainly because controlling microbial growth is one of the biggest challenges in food preservation. Natural antimicrobial agents such as vinegar, cultured sugar, plant extracts, and fermentation-based ingredients are widely used to prevent spoilage caused by bacteria, yeast, and mold. Food manufacturers are depending on these solutions to maintain product safety while also meeting clean-label expectations. The demand is especially strong in meat, dairy, bakery, and ready-to-eat categories where shelf life and hygiene are critical for both retailers and consumers.

By Application Analysis

Seafood, Meat & Poultry Products lead with 27.4% share due to high spoilage sensitivity

In 2025, Seafood, Meat & Poultry Products held a dominant market position, capturing more than a 27.4% share. This segment leads mainly because these products are highly perishable and prone to rapid microbial growth and oxidation. Natural preservatives such as plant extracts, organic acids, and fermentation-based solutions are widely used to maintain freshness, color, and safety. Meat and seafood producers are under constant pressure to extend shelf life without using synthetic additives, especially as consumers are becoming more aware of ingredient labels. This has increased the use of natural antimicrobial and antioxidant systems in both fresh and processed protein products.

Key Market Segments

By Product

- Edible Oil

- Rosemary Extracts

- Natamycin

- Vinegar

- Chitosan

- Others

By Function

- Antimicrobial

- Antioxidant

By Application

- Seafood, Meat & Poultry Products

- Bakery Products

- Dairy Products

- Beverages

- Snacks

- Fruits & Vegetables

- Others

Emerging Trends

Clean-label and plant-based food trends are reshaping pulp demand globally

One of the most noticeable latest trends in the fruit and vegetable pulp market is the strong shift toward clean-label and plant-based food products. Consumers today are paying more attention to what goes into their food, and they prefer ingredients that are natural, simple, and easy to understand. This is clearly reflected in the growing use of fruit pulp in beverages, dairy alternatives, baby food, and bakery products. Fruit pulp fits perfectly into this trend because it is derived directly from fruits and vegetables without heavy processing.

Global food systems are also shifting toward plant-based diets, which is increasing the use of fruit and vegetable-based ingredients. Many food companies are reformulating their products to remove artificial additives and replace them with natural alternatives like pulp. This trend is not just limited to developed markets but is becoming global.

Advanced processing and technology adoption are improving pulp quality and usage

Governments and global food bodies are also encouraging modernization in food processing to reduce waste and improve efficiency. The FAO highlights that processing helps extend shelf life and preserve nutrients, making it a key solution in managing growing food production. With global fruit production rising steadily, companies are investing more in processing technologies to handle large volumes efficiently. These advancements are making pulp more reliable, consistent, and suitable for a wide range of applications. As technology continues to improve, it is expected that pulp will play an even bigger role in the future of processed and convenience foods.

Drivers

Rising global fruit production is pushing demand for pulp processing

One of the biggest driving factors for fruit and vegetable pulp is the sheer rise in global production. According to the FAO, global fruit and vegetable production reached around 2.1 billion tonnes in 2023, showing how massive the raw material base has become. This growth has been consistent over time, with fruit production alone increasing by about 63% between 2000 and 2022. When such large volumes are produced, not all of it can be consumed fresh.

Governments and food organizations are also encouraging processing to reduce post-harvest losses and improve value addition. FAO data highlights that agricultural output continues to expand, with cultivated crop areas reaching 1.5 billion hectares in 2024, indicating strong supply availability. As production grows faster than fresh consumption capacity, industries are turning to pulp processing to convert excess produce into stable, usable forms for beverages, baby food, and packaged products.

Food waste reduction is accelerating pulp adoption across industries

Another major driver is the need to reduce food waste, which has become a global concern. The FAO estimates that around 1.3 billion tonnes of food is wasted every year, which is nearly one-third of all food produced for human consumption. Fruits and vegetables contribute heavily to this waste because they are highly perishable and sensitive to storage conditions. Converting them into pulp helps extend shelf life and makes transportation and storage much easier, especially for export-oriented food supply chains.

Governments and international bodies are actively promoting food waste reduction strategies, which indirectly support pulp processing industries. By turning fresh produce into pulp, companies can stabilize seasonal supply, reduce losses, and ensure year-round availability of ingredients. This is particularly important for juice manufacturers, dairy-based beverages, and processed food companies that depend on consistent raw material quality.

Restraints

High perishability and heavy post-harvest losses limit pulp processing efficiency

One of the biggest restraining factors for the fruit and vegetable pulp industry is the extremely high level of post-harvest losses. Fruits and vegetables are naturally delicate and begin to spoil quickly if not handled, stored, or processed properly. According to the FAO, fruits and vegetables have the highest loss rate among all food categories, reaching about 25.4% globally in 2023. This means a large portion of raw material never even reaches processing units. For pulp manufacturers, this creates uncertainty in raw material availability and quality.

This issue becomes even more serious when supply chains are long or poorly managed. Many regions still lack proper cold storage, transport systems, and handling infrastructure. Because of this, processors often face fluctuations in supply, forcing them to either pay higher prices for better-quality produce or deal with inconsistent inputs. Government bodies like the FAO continue to promote better post-harvest management practices, but the gap between production and efficient processing still exists.

Supply chain inefficiencies and waste reduce profitability across the value chain

Another major challenge is the inefficiency in the overall supply chain, which directly impacts the pulp business. Globally, about 13.2% of food is lost between harvest and retail stages, even before reaching consumers. When it comes specifically to fruits and vegetables, total losses can go even higher, often ranging between 25% to 50% across the supply chain. This creates a serious gap between production and usable raw material for processing industries like pulp manufacturing.

Opportunity

Growing demand for healthy beverages is creating strong opportunities for pulp usage

One of the biggest growth opportunities for the fruit and vegetable pulp industry comes from the rising demand for healthy and natural beverages. Consumers are slowly moving away from sugary carbonated drinks and looking for drinks made from real fruits and vegetables. According to industry data, the global juice market produced around 67.6 billion litres in 2022, showing how large the consumption base already is. At the same time, about 21% of consumers globally increased their intake of juices, smoothies, and juice drinks in recent years, mainly due to health awareness and lifestyle changes.

This shift is directly supporting the demand for fruit pulp, as pulp is the base ingredient for juices, smoothies, and functional drinks. Governments and health organizations are also encouraging higher fruit intake as part of balanced diets, which indirectly supports juice and pulp consumption.

Processing and value addition of fruits is expanding industrial opportunities

Another strong growth opportunity lies in the increasing focus on processing and value addition of fruits and vegetables. A significant share of global fruit production is already being used for processing. For example, the FAO highlights that about one-third of global citrus production is processed rather than consumed fresh. This clearly shows the importance of processing industries like pulp in managing large-scale agricultural output. In addition, global fruit and vegetable production reached about 2.1 billion tonnes in 2023, providing a massive raw material base for processing industries.

Governments and international organizations are promoting food processing as a way to reduce waste and improve farmer income. By converting fresh produce into pulp, industries can store and transport fruits more efficiently while maintaining quality.

Regional Insights

North America dominates the natural food preservatives market with 37.8% share supported by strong clean-label demand and regulatory backing

North America emerged as the dominating region in the natural food preservatives market, accounting for nearly 37.8% share, valued at around USD 379.5 million, supported by a well-established food processing industry and strong regulatory oversight. The region benefits from high consumer awareness around food safety and ingredient transparency, which is pushing manufacturers to shift toward natural preservation systems. The United States leads within the region, supported by its large packaged food sector and evolving labeling standards.

Consumers in the region increasingly prefer products free from artificial additives, which directly supports the adoption of natural preservatives in categories like bakery, dairy, meat, and beverages. Regulatory initiatives also play a major role. The U.S. Food and Drug Administration (FDA), which oversees nearly 80% of the U.S. food supply, continues to push for improved labeling transparency and safer ingredient use.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Naturex S.A. has built a strong position in natural preservatives through its plant-based ingredient portfolio. The company reported revenues of over USD 125 million in 2007 and operated with more than 1,700 employees before its acquisition. Its integration into Givaudan, which now operates in over 162 locations globally, has strengthened its reach and innovation capabilities.

Cargill is one of the largest global players in food ingredients and preservation solutions, with USD 154 billion revenue in 2025 and operations across 70 countries. The company employs over 155,000 people and delivers products to more than 125 markets worldwide. Cargill offers natural preservatives through its food ingredients portfolio, including antioxidant blends and natural flavor systems that extend shelf life.

Kalsec Inc. is known for its natural spice extracts and antioxidant solutions used widely in food preservation. The company focuses on plant-based ingredients such as rosemary extract, which is commonly used to extend shelf life in meat and snack products. Kalsec operates globally with production and research facilities supporting customers in multiple regions.

Top Key Players Outlook

- Naturex S.A

- Handary S.A.

- Cargill, Incorporated

- Kalsec Inc.

- Ita Food Improvers

- DSM

- Kerry Group Plc.

- Tate & Lyle PLC

- Kemin Industries, Inc.

Recent Industry Developments

In 2026, Naturex is estimated to generate around USD 176 million in annual revenue and operates with close to 500–1,700 employees globally, depending on integration structure within Givaudan.

In 2026, Cargill says it has about 155,000 employees across 70 countries/regions, which gives it strong scale to supply food manufacturers globally.

Report Scope

Report Features Description Market Value (2025) USD 1,004.1 Mn Forecast Revenue (2035) USD 2,007.5 Mn CAGR (2026-2035) 7.2% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product (Edible Oil, Rosemary Extracts, Natamycin, Vinegar, Chitosan, Others), By Function (Antimicrobial, Antioxidant), By Application (Seafood, Meat And Poultry Products, Bakery Products, Dairy Products, Beverages, Snacks, Fruits And Vegetables, Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA Competitive Landscape Naturex S.A, Handary S.A., Cargill, Incorporated, Kalsec Inc., Ita Food Improvers, DSM, Kerry Group Plc., Tate & Lyle PLC, Kemin Industries, Inc. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Natural Food Preservatives MarketPublished date: Mar 2026add_shopping_cartBuy Now get_appDownload Sample

Natural Food Preservatives MarketPublished date: Mar 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Naturex S.A

- Handary S.A.

- Cargill, Incorporated

- Kalsec Inc.

- Ita Food Improvers

- DSM

- Kerry Group Plc.

- Tate & Lyle PLC

- Kemin Industries, Inc.

Our Clients

- 181529

- Mar 2026