Global Nail Care Products Market Size, Share, Growth Analysis By Product (Nail Polish, Artificial Nail & Accessories, Others), By End-use (Salon, Household), By Distribution Channel (Online, Offline), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Feb 2026

- Report ID: 179561

- Number of Pages: 387

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

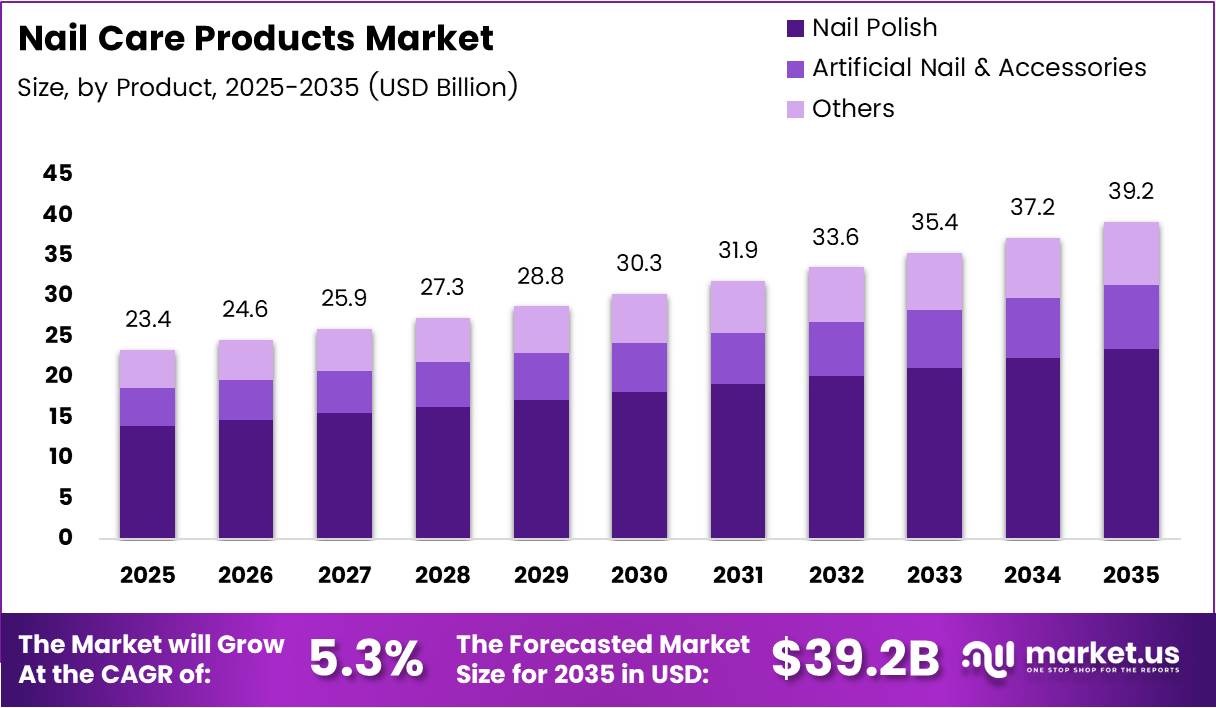

Global Nail Care Products Market size is expected to be worth around USD 39.2 Billion by 2035 from USD 23.4 Billion in 2025, growing at a CAGR of 5.3% during the forecast period 2026 to 2035.

The nail care products market covers a broad category of beauty and personal care offerings — including nail polish, artificial nails, nail treatments, cuticle care, and accessories. These products serve both professional salon environments and everyday household consumers, making the market structurally diversified across channels and end-users.

Consumer behavior in this market has shifted decisively toward self-expression and self-care routines. Nail aesthetics now function as a mainstream fashion statement rather than an occasional indulgence. This behavioral shift expands the addressable market beyond traditional salon clients to include millions of at-home users investing in regular nail care.

Premium product formulations command growing wallet share as buyers trade up from basic polish to gel systems, dip powders, and treatment-infused nail solutions. This premiumization signals that price sensitivity is declining among core consumer segments — a structural advantage for brands that can credibly justify higher price points through ingredient quality or performance claims.

E-commerce has fundamentally changed how nail care products reach consumers. Online channels now account for 64.5% of distribution, which means brands that invested early in direct-to-consumer infrastructure hold a structural distribution advantage over those relying on traditional retail shelf placement.

In February 2024, Apheon acquired a majority stake in Fiabila, the global leader in nail polish development and manufacturing with 10 production sites worldwide. This consolidation signals that upstream supply chain control is becoming a competitive priority, as formulators with proprietary manufacturing capabilities will set the pace for ingredient innovation.

According to Apheon’s 2024–2025 Sustainability Report, Fiabila nail polish and colored formulas achieve up to 86% natural origin ingredients. This figure reveals that sustainable formulation is no longer an aspirational goal — it is now a measurable, production-level standard that buyers and regulators will increasingly require from all market participants.

Additionally, Fiabila’s operations demonstrate that sustainability extends beyond ingredients — 68% of dirty solvents are reused on-site for cleaning manufacturing tanks, with the remainder recycled externally. This operational model reduces waste costs and strengthens ESG credentials, positioning manufacturers with such practices to meet tightening EU cosmetics sustainability directives ahead of competitors.

Key Takeaways

- The Global Nail Care Products Market is valued at USD 23.4 Billion in 2025 and is forecast to reach USD 39.2 Billion by 2035.

- The market advances at a CAGR of 5.3% during the forecast period 2026 to 2035.

- By Product, Nail Polish leads with a 58.3% market share in 2025.

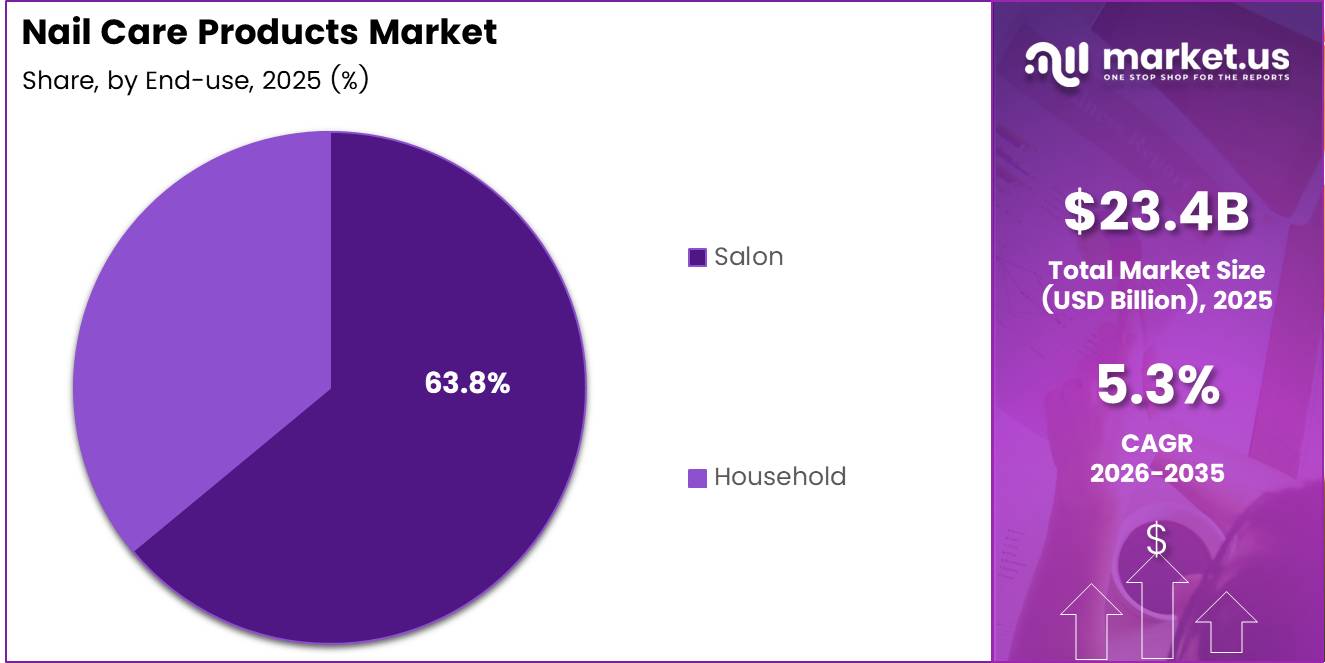

- By End-use, Salon dominates with a 63.8% share, reflecting the central role of professional nail services.

- By Distribution Channel, Online holds a 64.5% share, confirming the digital shift in beauty retail.

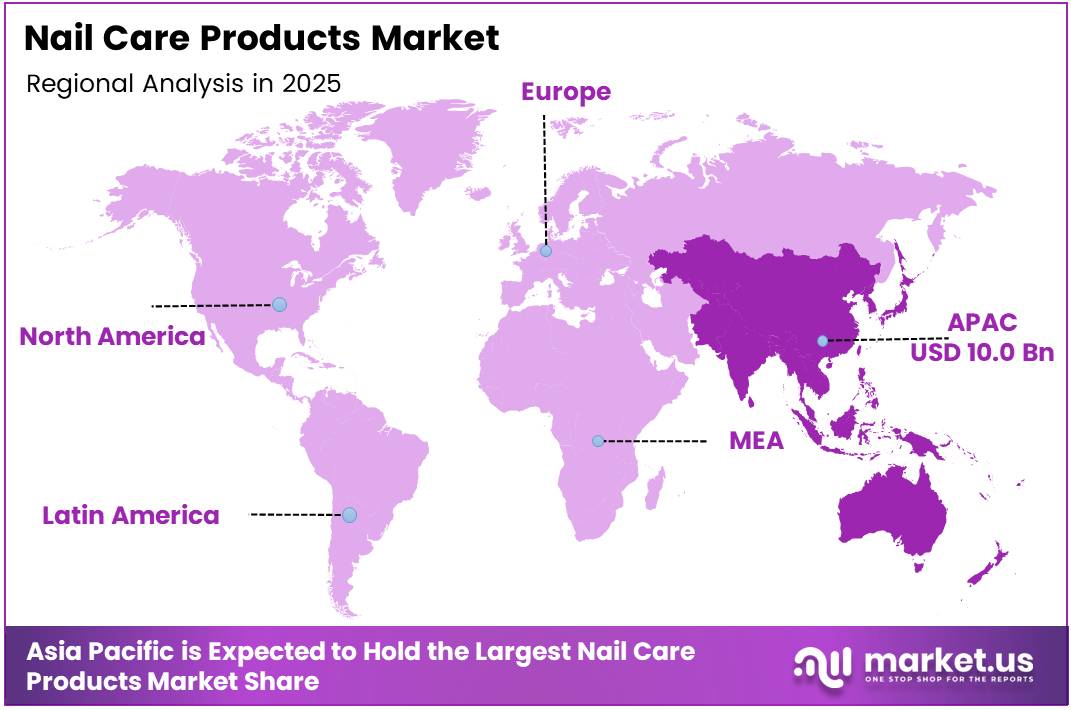

- Asia Pacific leads all regions with a 42.80% share, valued at USD 10.0 Billion in 2025.

Product Analysis

Nail Polish dominates with 58.3% due to universal household and salon adoption.

In 2025, Nail Polish held a dominant market position in the By Product segment of the Nail Care Products Market, with a 58.3% share. Its dominance reflects decades of established consumer behavior — nail polish remains the lowest-barrier entry point into nail aesthetics, accessible across income levels, geographies, and usage occasions. In January 2025, OPI launched its RapiDry collection in 30 shades with a 9-free vegan formula delivering smudge-proof results in 60 seconds, demonstrating that innovation within this category continues to raise the performance bar.

Artificial Nails and Accessories serve as the high-growth complement to traditional nail polish. This sub-segment captures consumers seeking longer-lasting, salon-quality results at home, particularly through press-on systems and gel extensions. Its expansion is tied directly to the at-home manicure movement, where consumers prioritize convenience and durability over the cost and time of professional visits.

Others within the product segment includes nail treatments, base coats, top coats, cuticle care, and nail strengtheners. These products generate repeat purchase cycles independent of color trends, providing category stability. Brands that integrate skincare-active ingredients — such as keratin-strengthening or antioxidant compounds — into this sub-segment command premium pricing and defend margin against commodity alternatives.

End-Use Analysis

Salon dominates with 63.8% due to professional service demand and treatment volume.

In 2025, Salon held a dominant market position in the By End-use segment of the Nail Care Products Market, with a 63.8% share. Professional salons consume nail care products at far higher volumes than individual households — a single salon operator requires consistent restocking of polish, gel systems, treatments, and accessories across multiple client appointments daily. This volume-driven demand gives salon-focused brands predictable B2B revenue streams that offset the volatility of consumer retail cycles.

Household end-use represents the fastest-expanding demand pool in the market. Rising at-home manicure adoption — accelerated by social media tutorials, affordable press-on systems, and direct-to-consumer brand accessibility — means household buyers now influence product formulation decisions. Brands that designed products exclusively for salon professionals are reformulating for ease of home application, confirming that household demand now shapes R&D priorities.

Distribution Channel Analysis

Online dominates with 64.5% due to direct-to-consumer brand access and convenience.

In 2025, Online held a dominant market position in the By Distribution Channel segment of the Nail Care Products Market, with a 64.5% share. E-commerce gives nail care brands the ability to reach consumers directly, collect behavioral data, and build subscription-based replenishment models — revenue structures unavailable through traditional retail. This channel dominance also lowers the barrier for indie and challenger brands to compete against established players without requiring shelf space in physical stores.

Offline distribution retains relevance in markets where product tactility drives purchase decisions — consumers selecting shades or testing textures in-store before committing. However, offline’s shrinking share signals that brands relying solely on physical retail are structurally exposed. The strategic response is an omnichannel approach: offline for discovery and brand experience, online for repeat purchase and loyalty capture.

Key Market Segments

By Product

- Nail Polish

- Artificial Nail & Accessories

- Others

By End-use

- Salon

- Household

By Distribution Channel

- Online

- Offline

Drivers

Professional Salon Culture and At-Home Manicure Adoption Expand the Nail Care Consumer Base

Professional salon culture has normalized nail care as a routine personal grooming service rather than a luxury occasion. This shift increases per-capita spending frequency — consumers now book nail appointments monthly rather than seasonally. For product manufacturers, this means salon operators require continuous restocking, creating a stable B2B volume channel that runs independently of trend cycles.

Simultaneously, at-home manicure adoption has added an entirely new consumer layer to the market. Social media platforms amplify nail aesthetics, turning nail design into participatory content rather than passive observation. In November 2024, Helen of Troy announced its agreement to acquire Olive & June, a pioneering omnichannel DIY nail care brand spanning polish, artificial nails, tools, and treatments, for $240 million — a direct signal that major industry players are investing capital to capture this at-home consumer segment.

According to Apheon’s 2024–2025 Sustainability Report, 46% of Fiabila’s main suppliers carry EcoVadis certification. This supply chain transparency reflects the premium ingredient standards that professional and consumer buyers now demand — and it demonstrates that sustainable sourcing is becoming a procurement prerequisite, not just a marketing claim. Brands without traceable supply chains face increasing buyer scrutiny.

Restraints

Chemical Safety Regulations and Toxic Ingredient Concerns Constrain Formulation Flexibility

Regulatory bodies across the EU, US, and Asia-Pacific maintain active ingredient restriction lists for nail care formulations. Compounds such as formaldehyde, toluene, and dibutyl phthalate face outright bans or concentration caps in multiple markets. For manufacturers, compliance requires continuous reformulation investment — adding cost and time-to-market pressure that smaller brands struggle to absorb.

Consumer awareness of toxic compounds in nail products has shifted from niche concern to mainstream purchasing criterion. Buyers actively seek “10-free,” “12-free,” or vegan-certified labels, forcing brands to reformulate existing SKUs while maintaining performance parity. Fiabila addressed this directly by significantly reducing nitrosamine levels in thixotropic bases — a technical challenge that illustrates how ingredient safety compliance demands laboratory-level expertise, not just label changes.

According to Apheon’s 2024–2025 Sustainability Report, Fiabila’s nail care manufacturing operations report a carbon footprint of 1,218 tCO₂ (Scope 1 and 2), equivalent to 11 tCO₂ per €m of sales. This benchmark reveals that even sustainability-focused manufacturers carry measurable environmental costs — and as carbon disclosure requirements expand globally, manufacturers without clear reduction roadmaps face regulatory and reputational risk.

Growth Factors

Plant-Based Formulations, Smart Nail Devices, and AI-Powered Personalization Open New Revenue Streams

The shift to plant-based and non-toxic nail care formulations is not a niche preference — it is a market repositioning. Brands that credibly deliver high-performance products with clean ingredient stacks can command premium price points, enter retail channels that restrict conventional formulations, and qualify for sustainability-linked procurement. This creates a differentiated margin structure unavailable to brands that remain reliant on synthetic formulations.

Smart nail devices, particularly LED-based home gel curing systems, transfer professional-grade results into the household channel. The O’NAIL AI Technology Lamp — launched as a 2025 model — became the world’s first AI-powered nail curing lamp, selectively curing only the nail surface while avoiding heat exposure to surrounding skin. This precision technology raises household product performance expectations and creates a hardware-plus-consumables revenue model that generates recurring sales beyond the initial device purchase.

According to available funding data, in May 2025, Blank Beauty closed an oversubscribed $6.5 million Series A round with strategic investment from Epson and Kirker Enterprises to advance AI and robotics for on-demand custom nail polish. This funding validates investor confidence in AI-driven personalization as a scalable commercial model — and signals that the next competitive frontier in nail care is custom color formulation, not just color selection.

Emerging Trends

Gel Systems, Press-On Innovation, and Skincare-Infused Nail Products Redefine Performance Expectations

Long-lasting gel and dip powder nail systems have moved from salon exclusives to at-home staples, fundamentally changing what consumers expect from a manicure. In May 2025, Mylee unveiled its Gel Nail Wraps — a 100% real gel, lamp-free system delivering up to 14-day chip-resistant wear in 20 wraps per pack. This launch demonstrates that the performance gap between salon and home application is closing, which compresses the salon-only market and rewards brands that lead in at-home innovation.

Minimalist and nude nail aesthetics, amplified by social media influencers, have shifted formulation priorities away from bold pigmentation toward texture, finish, and longevity. This trend benefits base coat and treatment product categories, which support any shade application. Brands that pivot R&D toward performance-enhancing formulations — rather than competing solely on color breadth — capture share across both trend-driven and trend-neutral consumer groups.

According to Apheon’s 2024–2025 Sustainability Report, Fiabila delivers 100% vegan formulas with full ingredient traceability and elimination of harmful compounds across its production chain. This standard illustrates that cross-category innovation — combining nail care with skincare-active ingredients — is already production-ready at scale. Brands that integrate this approach into mainstream SKUs, rather than positioning it as a premium tier, will capture the widest consumer base in the next product cycle.

Regional Analysis

Asia Pacific Dominates the Nail Care Products Market with a Market Share of 42.80%, Valued at USD 10.0 Billion

Asia Pacific holds a 42.80% share of the global nail care products market, valued at USD 10.0 Billion in 2025. This position reflects a structural combination of high population density, a deeply embedded beauty and personal care culture in markets like South Korea, Japan, and China, and a rapidly expanding middle class in India and Southeast Asia. The region’s nail art culture — which sets global aesthetic trends — also makes Asia Pacific a product innovation testing ground before global rollout.

North America Nail Care Products Market Trends

North America maintains a strong market position, anchored by mature professional salon infrastructure and high per-capita beauty spending. The region’s omnichannel retail ecosystem — where brands like Olive & June operate across physical and digital touchpoints — reflects the most advanced direct-to-consumer nail care model globally. Strategic acquisitions, such as Helen of Troy’s $240 million purchase of Olive & June, confirm that North America remains the primary arena for high-value brand consolidation.

Europe Nail Care Products Market Trends

Europe’s nail care market operates under the most stringent chemical safety frameworks globally, making it the region where clean and vegan formulation standards carry the highest commercial value. Brands that achieve EU compliance certification effectively unlock a quality benchmark recognized in import markets worldwide. European consumers also lead in demand for eco-certified and sustainably packaged nail care products, creating a premium segment with durable pricing power.

Latin America Nail Care Products Market Trends

Latin America presents a volume-driven opportunity, particularly in Brazil and Mexico, where beauty culture is deeply embedded and professional nail services are widely accessible across income levels. Urban salon density in Brazilian metropolitan areas is among the highest globally. However, currency volatility and import tariff structures constrain the penetration of premium international brands, making locally manufactured or locally distributed products structurally more competitive in this region.

Middle East and Africa Nail Care Products Market Trends

The Middle East and Africa region shows demand concentration in GCC countries, where high disposable income and an established luxury beauty retail infrastructure support premium nail care sales. South Africa functions as the primary sub-Saharan distribution hub. Across the broader region, the transition from professional salon dependency toward at-home nail care — driven by e-commerce accessibility — is creating new entry points for direct-to-consumer nail care brands.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

L’Oréal Groupe operates across the full nail care value chain — from mass-market to professional — giving it unmatched channel coverage that few competitors can replicate. Its ability to cross-leverage R&D investments across skincare and nail care formulation allows faster clean-ingredient reformulation than single-category brands. This scale advantage positions L’Oréal to absorb regulatory reformulation costs that constrain smaller rivals.

AMERICAN INTERNATIONAL INDUSTRIES occupies a strategically distinct position as a manufacturer and distributor serving both professional salon brands and private label customers. This dual-channel model diversifies revenue exposure while giving the company direct visibility into professional demand trends before they reach consumer markets. Its manufacturing depth creates a structural barrier against challenger brands that rely on contract manufacturing.

Coty Inc. competes through a diversified brand portfolio that spans professional nail care and mass consumer segments simultaneously. This portfolio breadth lets Coty capture demand across the full price spectrum, reducing revenue concentration risk in any single segment. However, managing brand coherence across such a wide price range requires disciplined segmentation — brands that blur positioning risk cannibalizing each other’s share.

Olive & June built its competitive position through an omnichannel DIY model that converts salon-quality results into an at-home format accessible to everyday consumers. In December 2024, Helen of Troy completed its acquisition of Olive & June for $240 million, validating the brand’s direct-to-consumer architecture as a scalable commercial platform. This acquisition integrates Olive & June’s consumer loyalty and product innovation pipeline into Helen of Troy’s distribution infrastructure.

Key Players

- L’Oréal Groupe

- AMERICAN INTERNATIONAL INDUSTRIES

- Coty Inc.

- Olive & June

- ORLY International, Inc.

- The Estée Lauder Companies

- Creative Nail Design Inc.

- NSI Nails

- LCN USA

- Cosnova GmbH

Recent Developments

- December 2024 – Helen of Troy completed the acquisition of Olive & June, a pioneering omnichannel DIY nail care brand covering polish, artificial nails, tools, treatments, and care, for $240 million including a $15 million earnout, marking its entry into the nail care category.

- May 2025 – Blank Beauty closed an oversubscribed $6.5 million Series A funding round with strategic investment from Epson and Kirker Enterprises to advance AI and robotics for on-demand custom nail polish formulation.

- April 2025 – Fiabila launched SPF50+ Base & Top, the first hybrid UV-protective nail care treatment enriched with marine plant extracts and antioxidants to prevent keratin damage from UV and pollution while extending color longevity.

- August 2025 – Londontown launched its Fall 2025 Perfect Pour nail polish collection featuring four coffee-inspired shades in 21+ free formulas with Florium Complex for hydration and nail strength.

- October 2025 – Olive & June launched Builder Gel, an at-home strengthening and lengthening system delivering flexible, long-lasting nails for up to 21 days in 16 neutral milky shades, with no glue or tips required.

- December 2025 – Fiabila launched SPF50+ Nude Veil, a tinted high-protection nail care treatment combining UVA/UVB Nail Guard Tech, marine antioxidants, and Kera-Shield complex, shown in studies to reduce oxidative keratin damage by 83%.

Report Scope

Report Features Description Market Value (2025) USD 23.4 Billion Forecast Revenue (2035) USD 39.2 Billion CAGR (2026-2035) 5.3% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product (Nail Polish, Artificial Nail & Accessories, Others), By End-use (Salon, Household), By Distribution Channel (Online, Offline) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape L’Oréal Groupe, AMERICAN INTERNATIONAL INDUSTRIES, Coty Inc., Olive & June, ORLY International Inc., The Estée Lauder Companies, Creative Nail Design Inc., NSI Nails, LCN USA, Cosnova GmbH Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- L'Oréal Groupe

- AMERICAN INTERNATIONAL INDUSTRIES

- Coty Inc.

- Olive & June

- ORLY International, Inc.

- The Estée Lauder Companies

- Creative Nail Design Inc.

- NSI Nails

- LCN USA

- Cosnova GmbH

Our Clients

- 179561

- Feb 2026