Global Multiprotocol Storage Market By Component (Hardware, Software, Services), By Storage Type (File Storage, Block Storage, Object Storage, Network Attached Storage (NAS), Storage Area Network (SAN), Computed Storage), By Deployment Mode (Public Cloud, Private Cloud, Hybrid Cloud), By Organization Size (Large Enterprises, Small and Medium-sized Enterprises), By Protocol Type (Network File System (NFS), Server Message Block (SMB), Others), By End-User Industry (Banking, Financial Services, and Insurance (BFSI), Others), By Regional Analysis, Global Trends and Opportunity, Future Outlook By 2025-2035

- Published date: Feb. 2026

- Report ID: 178791

- Number of Pages: 281

- Format:

-

keyboard_arrow_up

Quick Navigation

- Report Overview

- Top Market Takeaways

- Drivers Impact Analysis

- Restraints Impact Analysis

- By Component

- By Deployment Mode

- By Organization Size

- By End User Industry

- Investor Type Impact Matrix

- Technology Enablement Analysis

- Emerging Trends Analysis

- Growth Factors

- Opportunity Analysis

- Challenge Analysis

- Key Market Segments

- Regional Analysis

- Competitive Analysis

- Future Outlook

- Recent Developments

- Report Scope

Report Overview

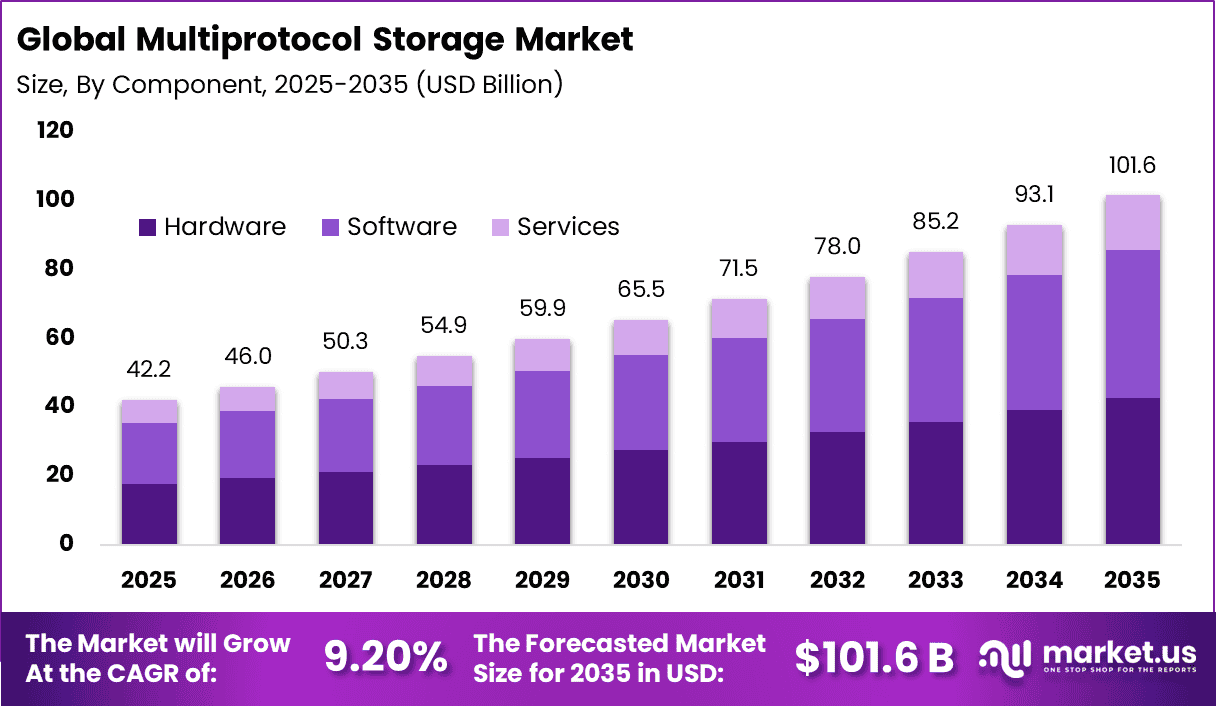

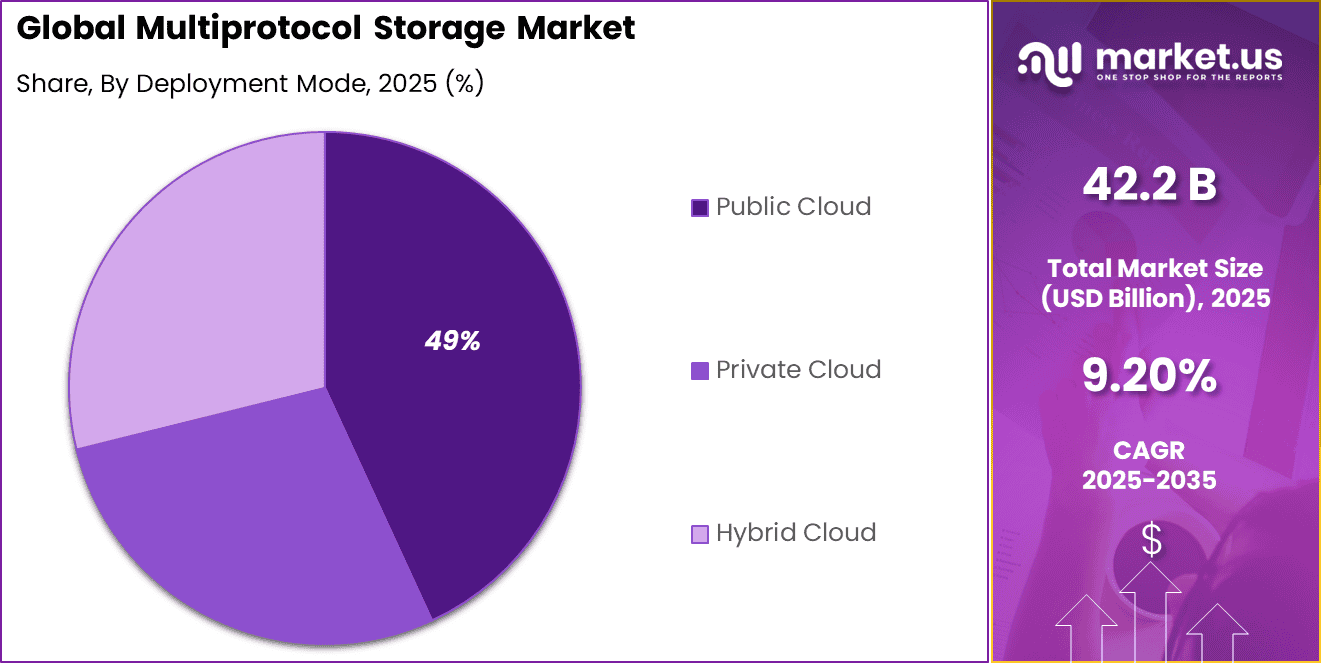

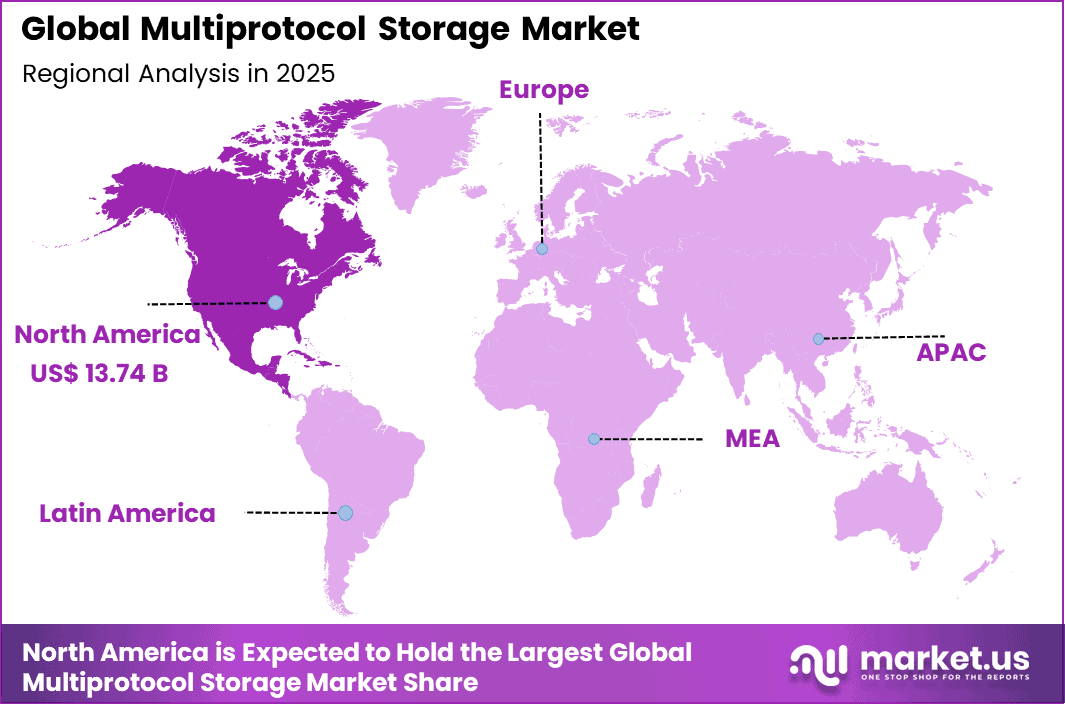

The Global Multiprotocol Storage Market generated USD 42.2 billion in 2025 and is predicted to register growth from USD 46 billion in 2026 to about USD 101.6 billion by 2035, recording a CAGR of 9.20% throughout the forecast span. In 2025, North America held a dominan market position, capturing more than a 32.6% share, holding USD 13.74 Billion revenue.

The Multiprotocol Storage Market refers to storage systems that support multiple data access protocols within a unified architecture. These systems allow organizations to manage block, file, and object storage workloads using a common platform. By supporting protocols such as Fibre Channel, iSCSI, NFS, SMB, and object interfaces, multiprotocol storage reduces infrastructure silos and improves operational flexibility.

Enterprises are increasingly dealing with hybrid workloads that combine legacy applications, virtualized environments, containerized platforms, and cloud-native systems. Multiprotocol storage enables seamless data access across these environments without requiring separate hardware stacks. This unified approach simplifies management, enhances data mobility, and supports consistent performance across diverse enterprise workloads.

A key driver of the Multiprotocol Storage Market is the increasing proliferation of diverse applications and data types within enterprise IT environments. Modern workloads include structured databases, unstructured file systems, virtualised servers, and content rich digital assets that require different storage access methods. Multiprotocol systems support these varied needs without the need for separate protocol specific arrays, enabling unified management and improved data governance.

Demand for multiprotocol storage is particularly strong among enterprises with heterogeneous IT environments and dynamic workload requirements. Large enterprises with legacy systems, virtualised infrastructures, and mixed application portfolios prioritise unified storage solutions that can reduce complexity and administrative overhead. These organisations benefit from consolidated storage platforms that support both legacy access methods and modern data services.

Top Market Takeaways

- By component, hardware accounts for 42.0% of the market, providing unified storage arrays that support block, file, and object protocols simultaneously for hybrid workloads.

- By deployment mode, public cloud represents 49.3%, enabling elastic scaling, pay-per-use economics, and seamless multi-protocol access across distributed data centers.

- By organization size, large enterprises hold 58.4% share, requiring multiprotocol flexibility for complex data migrations and tiered storage strategies.

- By end-user industry, BFSI captures 25.0%, leveraging unified storage for transaction databases, compliance archives, and real-time analytics.

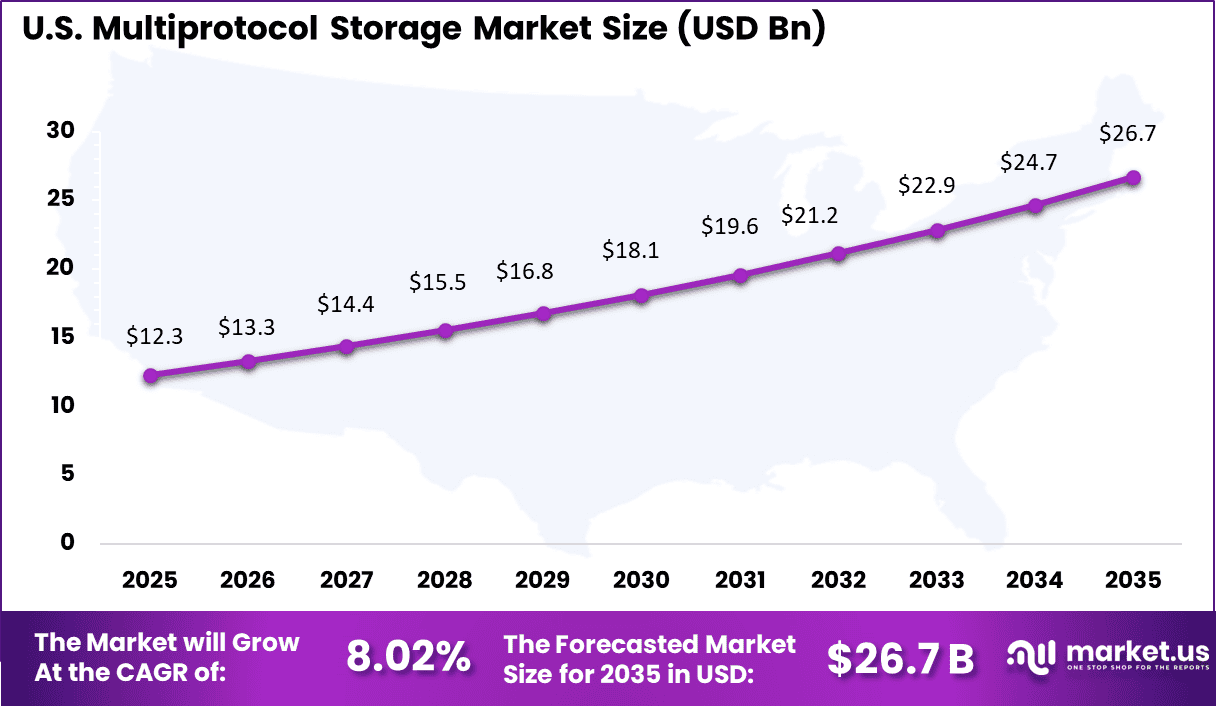

- By region, North America leads with 32.6% of the global market, where the U.S. is valued at USD 12.33 billion with a projected CAGR of 8.02%, driven by cloud repatriation and data sovereignty demands.

Drivers Impact Analysis

Key Driver Impact on CAGR Forecast (~%) Geographic Relevance Impact Timeline Growing enterprise demand for unified storage across SAN, NAS, and object protocols +2.6% North America, Europe Short to medium term Expansion of hybrid cloud and multi-cloud data architectures +2.3% Global Medium term Rising data volumes from AI, analytics, and IoT workloads +2.0% Asia Pacific, North America Medium term Need for cost-efficient storage consolidation +1.8% Global Medium term Increasing adoption of software-defined storage platforms +1.5% North America, Europe Medium to long term Restraints Impact Analysis

Key Restraint Impact on CAGR Forecast (~%) Geographic Relevance Impact Timeline High capital expenditure for enterprise-grade storage systems -2.4% Emerging Markets Short to medium term Complexity of managing multi-protocol environments -2.1% Global Medium term Migration challenges from legacy storage systems -1.8% North America, Europe Medium term Vendor lock-in and interoperability concerns -1.6% Global Medium term Power consumption and data center space constraints -1.3% Europe, North America Medium to long term By Component

Hardware accounting for 42.0% indicates that physical storage infrastructure remains a foundational element of multiprotocol systems. Enterprises continue to invest in high-performance storage arrays, controllers, and networking equipment to handle mission-critical workloads. Despite the growth of software-defined storage, hardware reliability and throughput remain central to enterprise deployment decisions.

Advanced storage hardware now integrates flash acceleration, NVMe support, and intelligent caching mechanisms. These improvements enhance latency-sensitive applications such as financial transactions and analytics workloads. Hardware innovation supports sustained demand, especially among large enterprises operating complex data centers.

Additionally, integrated appliances that combine compute, storage, and networking capabilities are gaining traction. These systems reduce deployment complexity and provide predictable performance benchmarks across multiple protocols.

By Deployment Mode

Public cloud representing 49.3% reflects the growing adoption of cloud-based storage services that support multiprotocol access. Enterprises are shifting workloads to cloud platforms that offer scalable object, file, and block storage under a unified service model. Cloud deployment reduces capital expenditure and provides elastic capacity.

Hybrid cloud strategies further strengthen this segment. Organizations often maintain on-premises storage while extending workloads to public cloud platforms for backup, disaster recovery, and analytics. Multiprotocol compatibility ensures smooth data movement between environments.

Cloud providers continue to enhance performance tiers and security frameworks, making public cloud storage suitable even for regulated industries. This flexibility supports consistent growth in cloud-based multiprotocol deployments.

By Organization Size

Large enterprises accounting for 58.4% demonstrate stronger adoption due to higher data complexity and volume. These organizations operate across multiple business units and geographic regions, requiring centralized storage systems that can support varied application requirements. Multiprotocol storage allows large enterprises to consolidate infrastructure and reduce management overhead.

It enables unified monitoring and governance across structured and unstructured data environments. This consolidation supports cost optimization and improved resource allocation. Large enterprises also prioritize high availability and disaster recovery capabilities. Multiprotocol systems often include built-in redundancy and replication features, aligning with stringent uptime requirements.

By End User Industry

The BFSI sector holding 25.0% reflects its heavy dependence on secure and high-performance storage environments. Financial institutions manage large volumes of transactional data, regulatory records, and customer information. Multiprotocol storage supports diverse workloads ranging from core banking systems to digital payment platforms.

Regulatory compliance requirements further drive adoption in this sector. Secure data management, encryption capabilities, and audit-ready logging features are critical. Multiprotocol systems provide centralized control that simplifies compliance monitoring.

Additionally, digital banking transformation initiatives are expanding data generation. Real-time analytics, fraud detection systems, and mobile banking platforms require scalable storage architectures capable of handling mixed workloads.

Investor Type Impact Matrix

Investor Type Growth Sensitivity Risk Exposure Geographic Focus Investment Outlook Enterprise storage hardware vendors High Medium North America, Asia Pacific Infrastructure refresh cycle opportunity Cloud service providers Medium to High Medium Global Hybrid storage integration Private equity firms Medium Medium North America, Europe Consolidation of storage solution providers Venture capital investors Medium High North America Innovation in software-defined storage Semiconductor and controller manufacturers Medium Medium Asia Pacific Component ecosystem growth Technology Enablement Analysis

Technology Enabler Impact on CAGR Forecast (~%) Primary Function Geographic Relevance Adoption Timeline Software-defined storage and virtualization technologies +2.9% Protocol flexibility and scalability Global Short to medium term NVMe and high-speed interconnect integration +2.5% Performance optimization North America, Asia Pacific Medium term Cloud-native storage orchestration tools +2.2% Hybrid environment management Global Medium term AI-driven storage performance analytics +1.9% Predictive capacity planning North America, Europe Medium to long term Data tiering and compression technologies +1.6% Cost efficiency and optimization Global Long term Emerging Trends Analysis

The Multiprotocol Storage market is witnessing growing adoption of unified storage architectures that support block, file, and object protocols within a single platform. Enterprises are consolidating storage infrastructure to reduce operational complexity and improve resource utilization. This unified approach enables flexible data access across diverse workloads such as databases, virtual machines, and analytics applications.

As hybrid and multi cloud environments expand, multiprotocol compatibility is becoming a standard enterprise requirement. Another emerging trend is the integration of software defined storage and automation capabilities. Organizations are deploying intelligent storage systems that dynamically allocate capacity and optimize performance based on workload demand. Automation tools are improving data tiering and lifecycle management.

Growth Factors

Growth in this market is being supported by an increase in data generation across industries, which is driving demand for flexible and scalable storage solutions. Organizations are seeking storage platforms that can adapt to evolving workloads without requiring separate infrastructure silos. The rise of hybrid cloud and edge computing is contributing to this demand, as enterprises require consistent access to data across on premise and distributed environments.

Another factor is the trend toward data consolidation, where companies prefer to manage all forms of data within a unified architecture to reduce operational complexity. In addition, improvements in data management capabilities, such as embedded analytics, tiering, and policy based automation, are enhancing the value proposition of multiprotocol systems. As data driven decision making becomes central to business operations, investments in versatile storage solutions are being prioritized.

Opportunity Analysis

A major opportunity lies in expanding cloud hybrid storage solutions. Enterprises are increasingly combining on premises and cloud storage to optimize cost and performance. Multiprotocol systems that enable seamless data mobility between environments are gaining attention. Vendors offering flexible deployment models can capture growing hybrid demand.

Another opportunity exists in supporting data intensive applications such as artificial intelligence and big data analytics. These workloads require high performance and scalable storage architectures. Multiprotocol platforms can efficiently manage structured and unstructured data simultaneously. This capability positions the market for sustained long term growth.

Challenge Analysis

A primary challenge in the Multiprotocol Storage market is maintaining consistent performance across diverse protocols. Different workloads may have varying latency and throughput requirements. Balancing resource allocation without compromising efficiency requires advanced optimization mechanisms. Performance inconsistency can affect enterprise operations.

Another challenge involves ensuring data security and compliance across multiple access protocols. Unified systems must enforce consistent encryption, access control, and monitoring policies. Managing these controls across complex environments can increase administrative burden. Strong governance frameworks are essential for sustained reliability.

Key Market Segments

By Component

- Hardware

- Software

- Services

By Storage Type

- File Storage

- Block Storage

- Object Storage

- Network Attached Storage (NAS)

- Storage Area Network (SAN)

- Computed Storage

By Deployment Mode

- Public Cloud

- Private Cloud

- Hybrid Cloud

By Organization Size

- Large Enterprises

- Small and Medium-sized Enterprises (SMEs)

By Protocol Type

- Network File System (NFS)

- Server Message Block (SMB)

- iSCSI

- Fibre Channel

- Object Storage Protocols

- Others

By End-User Industry

- Banking, Financial Services, and Insurance (BFSI)

- IT and Telecommunications

- Healthcare

- Manufacturing

- Retail and E-commerce

- Media and Entertainment

- Government and Public Sector

- Transportation and Logistics

- Energy and Utilities

- Education

- Others

Regional Analysis

North America accounts for 32.6% of the multiprotocol storage market, supported by strong enterprise IT infrastructure and high adoption of hybrid cloud environments. Organizations in the region are deploying multiprotocol storage systems to support diverse workloads across file, block, and object storage within a unified architecture. Demand is driven by increasing data volumes, need for flexible storage management, and growing emphasis on interoperability across legacy and modern applications.

The United States market is valued at USD 12.33 Bn and is expanding at a CAGR of 8.02%, reflecting steady investment in scalable and performance-oriented storage solutions. Adoption is influenced by rising enterprise data growth, expansion of virtualized environments, and the need to optimize storage costs without compromising performance. Growth is further supported by integration of multiprotocol systems within cloud data centers, disaster recovery frameworks, and high-availability enterprise applications.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Competitive Analysis

The Multiprotocol Storage market is led by established enterprise storage providers such as NetApp, Dell EMC, Hewlett Packard Enterprise, IBM, Cisco Systems, Hitachi, Huawei Technologies, and Western Digital. These companies compete on performance reliability, support for file and block protocols, and integration with hybrid cloud and data center environments. Their solutions are widely adopted by large enterprises that require unified storage systems capable of handling diverse workloads with high availability and strong data protection.

Specialized and emerging providers including Zadara Storage, NTT Communications, Quantum, DataDirect Networks, Pivot3, Exablox, StorOne, and others compete through flexible deployment models and cost efficient architectures. Competition in this segment is driven by scalability, simplified management, and support for modern applications such as virtualization and analytics. These vendors are often selected by organizations seeking adaptable storage platforms without complex infrastructure expansion.

Top Key Players in the Market

- NetApp, Inc.

- Dell EMC

- Hewlett Packard Enterprise Company

- IBM Corporation

- Cisco Systems, Inc.

- Hitachi, Ltd.

- Huawei Technologies Co., Ltd.

- Zadara Storage

- NTT Communications Corporation

- Quantum Corporation

- DataDirect Networks

- Pivot3, Inc.

- Exablox

- Western Digital Corporation

- StorOne

- Others

Future Outlook

The future outlook for the Multiprotocol Storage Market is positive as organizations increasingly need flexible and efficient ways to store and manage data. Demand for multiprotocol storage solutions is expected to grow because these systems support multiple storage protocols, making it easier to handle diverse data types and workloads.

Adoption of scalable architectures, integration with cloud platforms, and improved performance features will support broader use across enterprises. Growth can be attributed to rising data volumes, digital transformation efforts, and the need for unified storage management. Overall, the market is expected to expand as businesses prioritize adaptable and high-performance storage solutions.

Recent Developments

- November 2025, NetApp: ONTAP release notes highlighted continued upgrades around NVMe protocol support, security hardening, and performance analytics. For multiprotocol buyers, ONTAP’s steady expansion of NVMe and unified file services supports mixed workloads where NFS and SMB run alongside higher-speed block access.

- 2025, Dell Technologies (PowerStore): PowerStore continued positioning as a unified platform that supports block and file with NFS, SMB, iSCSI, and NVMe-oF. This alignment is important because multiprotocol storage refresh cycles are increasingly driven by the need to consolidate SAN and NAS into one operational model.

Report Scope

Report Features Description Market Value (2025) USD 42.2 Billion Forecast Revenue (2035) USD 101.6 Billion CAGR(2025-2035) 9.20% Base Year for Estimation 2024 Historic Period 2020-2024 Forecast Period 2025-2035 Report Coverage Revenue forecast, AI impact on Market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends Segments Covered By Component (Hardware, Software, Services), By Storage Type (File Storage, Block Storage, Object Storage, Network Attached Storage (NAS), Storage Area Network (SAN), Computed Storage), By Deployment Mode (Public Cloud, Private Cloud, Hybrid Cloud), By Organization Size (Large Enterprises, Small and Medium-sized Enterprises), By Protocol Type (Network File System (NFS), Server Message Block (SMB), Others), By End-User Industry (Banking, Financial Services, and Insurance (BFSI), Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA Competitive Landscape NetApp, Inc., Dell EMC, Hewlett Packard Enterprise Company, IBM Corporation, Cisco Systems, Inc., Hitachi, Ltd., Huawei Technologies Co., Ltd., Zadara Storage, NTT Communications Corporation, Quantum Corporation, DataDirect Networks, Pivot3, Inc., Exablox, Western Digital Corporation, StorOne, Others Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Multiprotocol Storage MarketPublished date: Feb. 2026add_shopping_cartBuy Now get_appDownload Sample

Multiprotocol Storage MarketPublished date: Feb. 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- NetApp, Inc.

- Dell EMC

- Hewlett Packard Enterprise Company

- IBM Corporation

- Cisco Systems, Inc.

- Hitachi, Ltd.

- Huawei Technologies Co., Ltd.

- Zadara Storage

- NTT Communications Corporation

- Quantum Corporation

- DataDirect Networks

- Pivot3, Inc.

- Exablox

- Western Digital Corporation

- StorOne

- Others

Our Clients

- 178791

- Feb. 2026