Global Modern Data Stack Market Size, Share and Analysis Report By Component (Software/Solutions, Services), By Deployment Mode (Cloud-based, On-premises), By Organization Size (Large Enterprises, Small and Medium-sized Enterprises), By Technology Layer (Data Ingestion and Integrationm, Data Storage and Warehousing, Data Transformation and Modeling, Data Analysis and Visualization, Data Orchestration and Observability, Others), By End-User Industry (Technology and Software, Financial Services, Retail and E-commerce, Media and Advertising, Others), By Regional Analysis, Global Trends and Opportunity, Future Outlook By 2025-2035

- Published date: Feb. 2026

- Report ID: 177913

- Number of Pages: 354

- Format:

-

keyboard_arrow_up

Quick Navigation

- Report Overview

- Key Takeaway

- By Component

- By Deployment Mode

- By Organization Size

- By Technology Layer

- By End User Industry

- Regional Analysis

- Driver Analysis

- Restraint Analysis

- Opportunity Analysis

- Challenge Analysis

- Top Emerging Trends

- Customer Impact: Trends and Disruptors

- Key Market Segments

- Key Players Analysis

- Recent Developments

- Report Scope

Report Overview

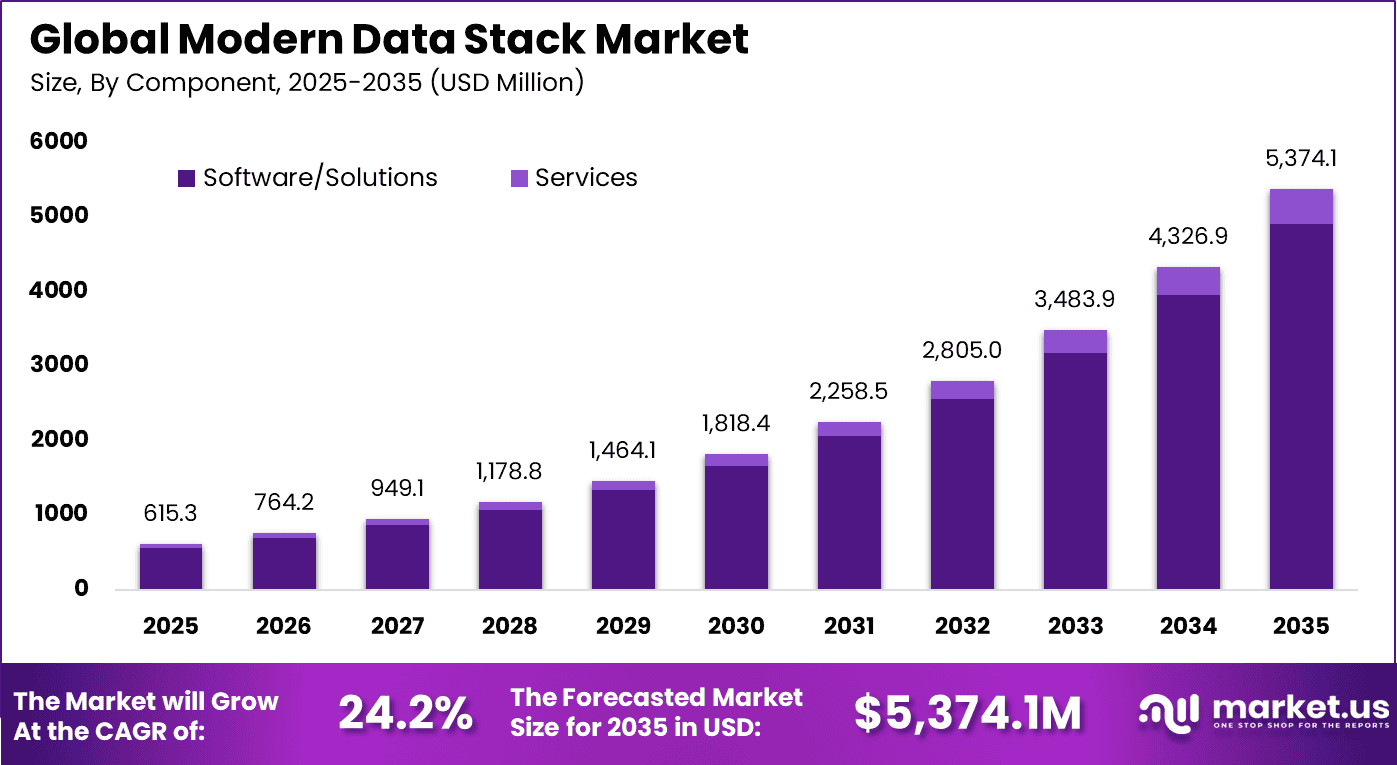

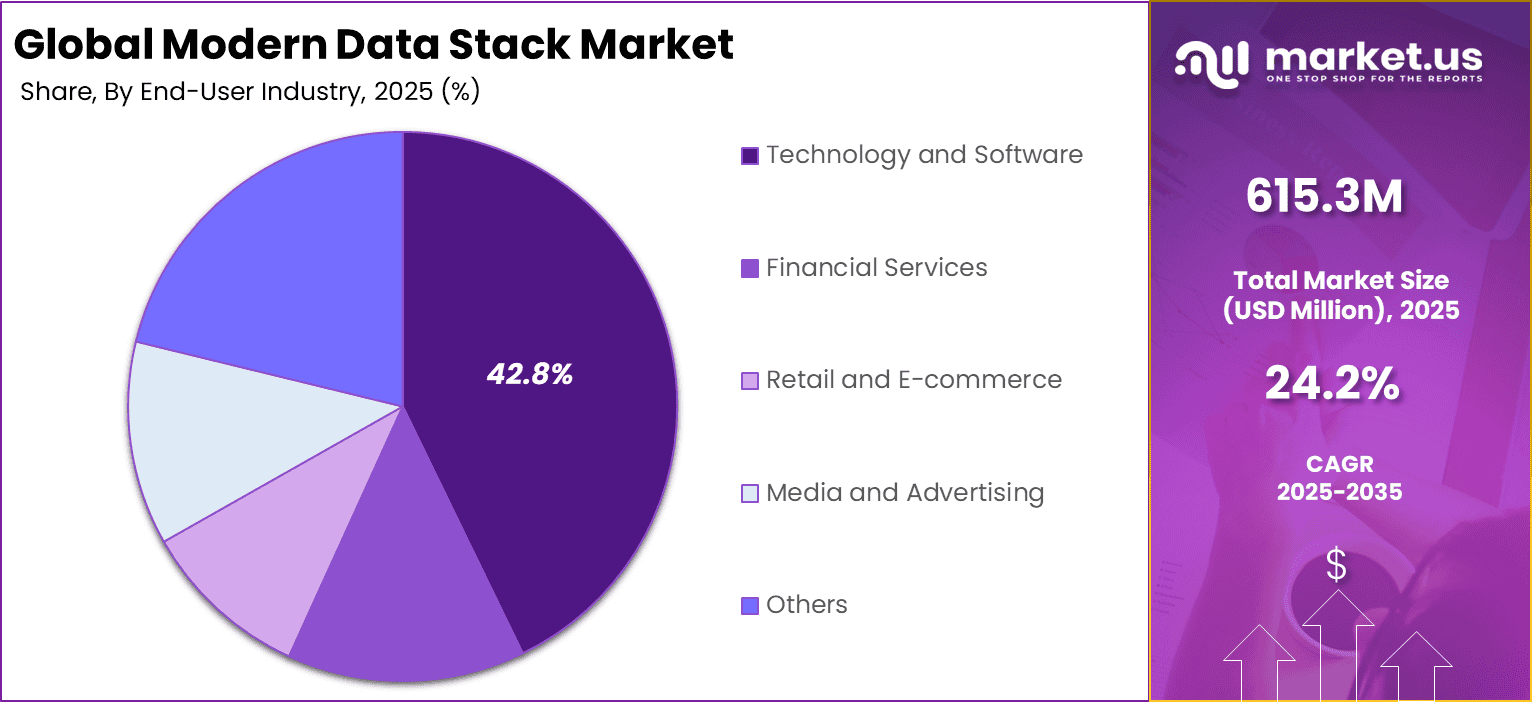

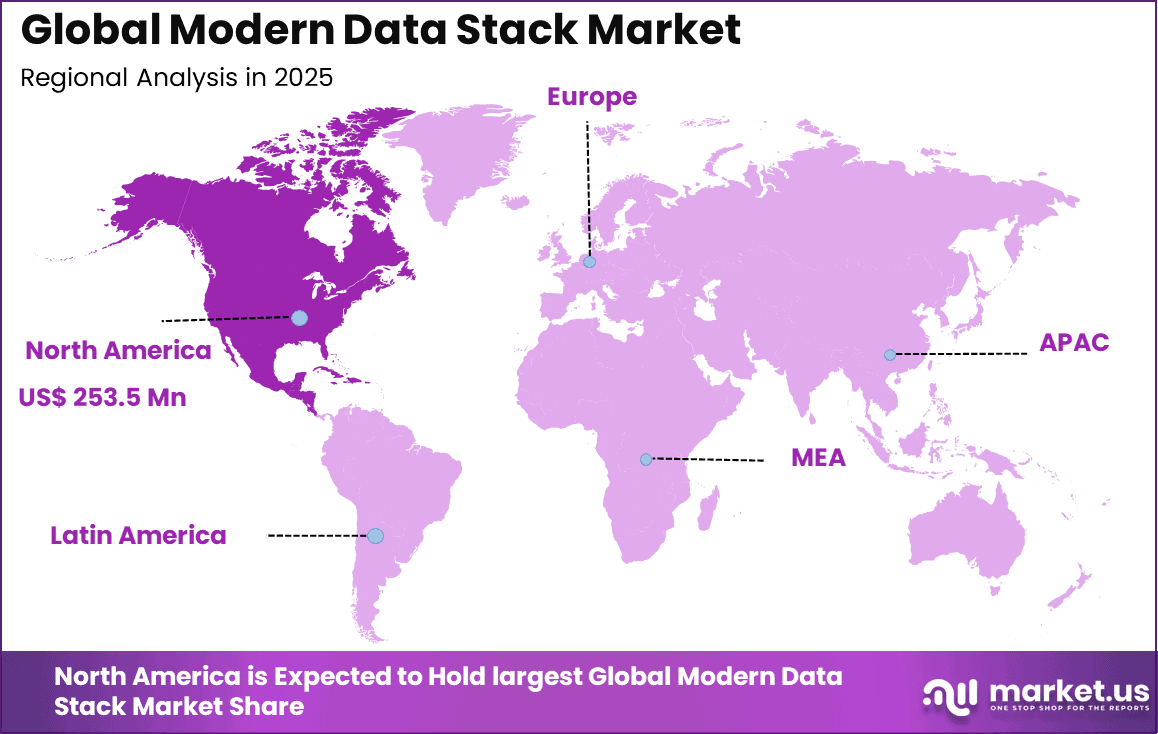

The Global Modern Data Stack Market size is expected to be worth around USD 5,374.1 million by 2035, from USD 615.3 million in 2025, growing at a CAGR of 24.2% during the forecast period from 2025 to 2035. North America held a dominant market position, capturing more than a 41.2% share, holding USD 253.5 million in revenue.

The Modern Data Stack Market refers to a cloud based ecosystem of data ingestion, storage, transformation, orchestration, analytics, and governance technologies that operate as modular components instead of a single monolithic platform. These tools connect through standardized interfaces and allow data to move continuously from operational sources to analytical applications. The architecture typically includes ingestion connectors, cloud warehouses, transformation layers, and visualization environments working together in a coordinated workflow.

In many enterprises, analytical workloads now operate outside legacy enterprise data warehouses, and more than 65% of new analytics environments are deployed directly in cloud storage platforms. The modern stack supports this shift by separating compute from storage and enabling elastic processing capacity. Organizations adopt it to support faster experimentation and collaborative analytics across engineering and business teams. As a result, the market is defined by interoperability and automation rather than hardware infrastructure.

One major driver is the need for real time and near real time analytics. Businesses require up to date information for pricing, logistics, and customer engagement decisions. Traditional batch processing systems cannot support this speed requirement, leading to the adoption of streaming ingestion and automated transformation layers. The modern stack enables continuous updates and reduces reporting latency.

Modern data stack adoption is accelerating alongside rapid data expansion. Around 90% of the world’s data has been generated within the last two years, and annual data creation is projected to reach 181 zettabytes by 2025, representing a 150% increase from 2023. This surge is driving organizations to adopt scalable cloud based data architectures capable of handling large volumes and diverse data types.

Adoption patterns show strong accessibility across company sizes. Among studied deployments, 52% of organizations had fewer than 100 employees, while 10% had more than 500, indicating usage across both small and large enterprises. From a business perspective, 45% of users operate in B2B environments and 42% in B2C, demonstrating broad applicability across industries and customer models.

For instance, in October 2025, Fivetran and dbt Labs merged in an all-stock deal reaching $600M ARR, creating a unified open data infrastructure leader that integrates automated movement with AI-ready transformation.

Key Takeaway

- By component, software and solutions dominated the Modern Data Stack Market with a 91.4% share, reflecting strong demand for integrated analytics and data engineering platforms.

- By deployment mode, cloud based infrastructure led with a 94.7% share, supported by scalability, flexibility, and native integration with digital applications.

- By organization size, small and medium sized enterprises accounted for 58.3% of total adoption, driven by demand for agile and cost efficient data platforms.

- By technology layer, data storage and warehousing represented 31.6% of the market, highlighting the importance of centralized and scalable data repositories.

- By end user industry, technology and software companies held a 42.8% share, supported by continuous product innovation and high data generation.

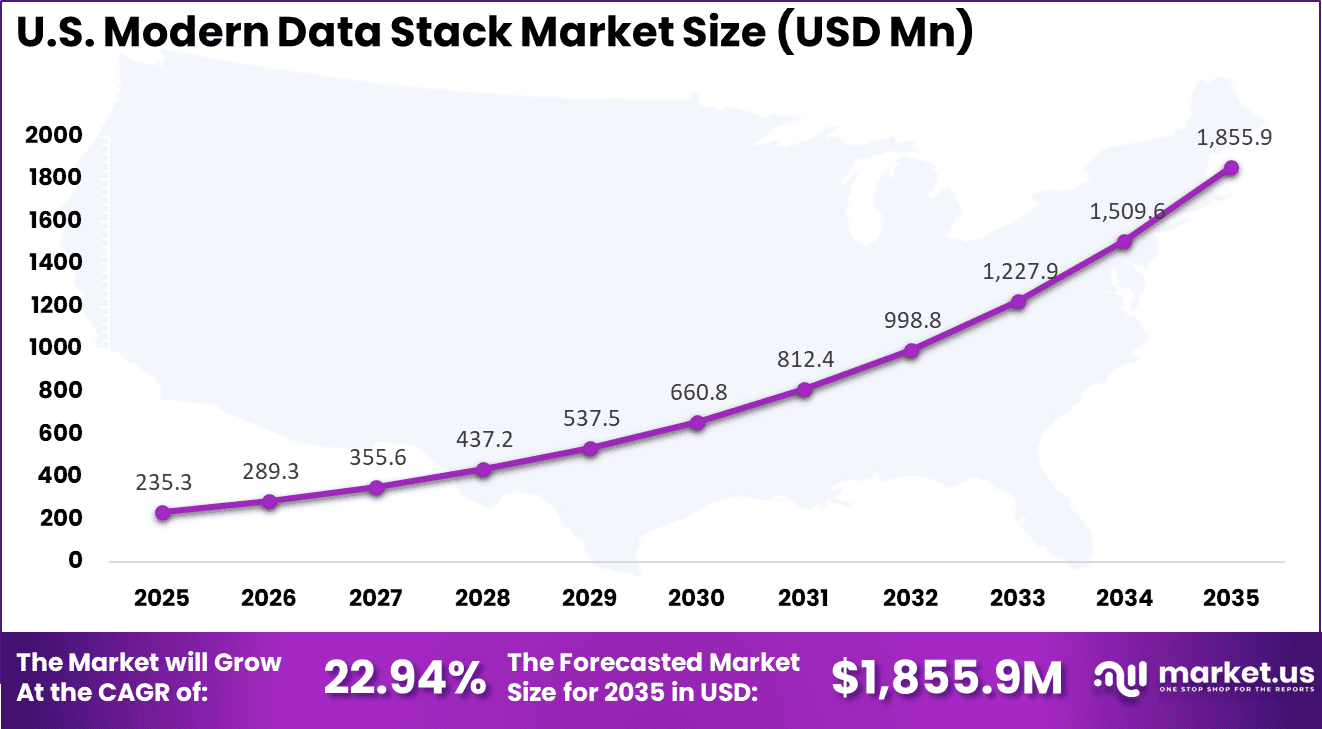

- Regionally, North America accounted for 41.2% of the market, with the US valued at USD 235.3 million and recording a CAGR of 22.94%, reflecting strong investment in cloud native data ecosystems.

By Component

Software and solution platforms accounted for 91.4% of implementations. Organizations emphasize integrated platforms that coordinate ingestion, transformation, orchestration, and analytics across distributed environments. These solutions automate pipeline monitoring, metadata tracking, and performance optimization. The result is consistent data availability for reporting and operational applications.

The shift toward software centric architecture reduces manual engineering work and improves operational transparency. Automated lineage tracking allows teams to understand how datasets evolve across workflows. This improves trust in analytics outputs and supports regulatory documentation. Operational reliability improves because failures are detected early within pipelines.

Standardized interfaces also enable faster integration with analytics tools and business applications. Data teams can build reusable workflows without rebuilding infrastructure repeatedly. This reduces maintenance complexity and operational overhead. The architecture therefore supports scalable analytics operations across organizations.

For Instance, in January 2026, Airbyte released new open-source connectors, boosting software versatility. Teams now handle more sources with less code, fitting seamlessly into stacks like Snowflake and Databricks. This update drives software growth by emphasizing community-driven tools that prevent lock-in.

By Deployment Mode

Cloud based deployment held 94.7% share due to demand for elastic processing and storage scalability. Data volumes fluctuate significantly across digital platforms, requiring dynamic resource allocation. Hosted environments enable ingestion and transformation processes to scale automatically based on workload intensity. This ensures uninterrupted analytical operations.

Distributed data sources such as applications, sensors, and transactions feed continuously into analytical systems. Cloud infrastructure centralizes data access across geographic locations. Teams analyze consolidated datasets rather than isolated regional repositories. This enhances data consistency across business units.

Operational maintenance also becomes simplified because infrastructure updates are managed centrally. Organizations focus on analytics development rather than hardware administration. Continuous availability and redundancy further strengthen adoption. Hosted deployment therefore aligns with modern analytics operational requirements.

For instance, in December 2025, Snowflake teamed with Fivetran, dbt, and Sigma for full cloud stack acceleration. This partnership delivers speed and simplicity on Snowflake’s AI Data Cloud, pushing cloud adoption through integrated, scalable services.

By Organization Size

Small and medium sized enterprises represented 58.3% adoption. These organizations prefer modular architectures because they avoid large upfront infrastructure investment. Subscription based platforms allow gradual expansion as data usage grows. This makes advanced analytics accessible without extensive internal engineering teams.

Operational efficiency improves because smaller teams rely on automation instead of manual data management. Prebuilt connectors accelerate integration with applications and digital services. This reduces implementation timelines and technical complexity. Businesses therefore achieve faster analytical capability deployment.

Competitive pressure also encourages adoption among growing firms. Data driven decision making supports marketing optimization, customer retention, and operational planning. Flexible architecture allows experimentation without operational disruption. The model supports growth aligned with business expansion.

For Instance, in October 2025, dbt Labs, via a merger with Fivetran, added hosted dbt Core for SMEs. This cuts vendors from stacks, making transformation accessible for smaller orgs chasing efficiency. Growth aids SMEs ditching monoliths for modular tools.

By Technology Layer

Data storage and warehousing accounted for 31.6% of technological focus. Reliable centralized storage remains essential for analytics and reporting accuracy. Organizations consolidate structured and semi structured datasets into analytical repositories for consistent access. This supports enterprise wide data standardization.

Warehousing layers also enable historical analysis across long operational periods. Teams evaluate trends and operational performance using stable datasets. Query performance improvements support interactive dashboards and reporting tools. Analytical productivity increases as data retrieval becomes faster.

Integration with transformation and governance layers further improves data reliability. Validation and schema management maintain consistent data definitions across departments. This ensures analytical outputs remain comparable across timeframes. Storage and warehousing therefore form the operational backbone of modern analytics environments.

For Instance, in February 2026, Monte Carlo advanced observability for warehouses like Snowflake. ML-powered monitoring spots issues in storage layers early, ensuring data freshness. It bolsters this layer by adding proactive quality for growing datasets.

By End User Industry

The technology and software sector accounted for 42.8% of adoption. Digital service providers rely heavily on product analytics, customer behavior analysis, and operational monitoring. Modern data architecture supports continuous measurement of user interactions and system performance. This enables rapid product iteration cycles.

Software platforms generate high frequency event streams requiring scalable ingestion and processing. Modular architectures allow efficient management of application telemetry and customer activity data. Teams analyze product usage patterns to improve functionality and reliability. Analytical insights therefore directly influence product development decisions.

Continuous deployment environments also require synchronized analytics pipelines. Observability across data layers ensures new releases do not disrupt reporting accuracy. The architecture therefore supports agile operational practices. Adoption continues to expand within digital product organizations.

For Instance, in December 2025, Confluent integrated its Kafka streaming with modern stacks, enabling tech firms to process real-time app data at scale. This helps software companies build responsive systems for user analytics. It grows industry use by bridging event streams to warehouses seamlessly.

Regional Analysis

North America held 41.2% share of adoption due to widespread digital transformation initiatives and mature cloud infrastructure. Organizations across industries integrate analytics into operational workflows to support decision making. Skilled technical workforce and advanced technology adoption accelerate implementation. The region demonstrates strong reliance on data driven operations.

For instance, in June 2025, Databricks from San Francisco enhanced North America’s data leadership through Data + AI Summit announcements, including Lakebase, Unity Catalog governance for Iceberg/Delta formats, and Agent Bricks, creating AI-ready unified data foundations for real-time workloads and open standards interoperability.

The United States contributed USD 235.3 Mn with an estimated growth rate of 22.94% annually. Businesses prioritize scalable analytics platforms to manage increasing digital interactions and transaction data. Investment continues in architectures that improve data accessibility and reliability. Adoption expands as organizations shift toward continuous analytical operations.

For instance, in February 2026, Snowflake reinforced U.S. dominance in the Modern Data Stack by launching Snowflake Intelligence and Cortex AISQL at Summit 2025, consolidating ETL, analytics, and AI into a unified platform that challenges fragmented stacks.

Driver Analysis

Cloud-Native Data Operations Expansion

A primary growth driver is the rapid migration of business workloads toward cloud infrastructure. Cloud environments allow scalable storage and parallel processing, enabling organizations to analyze growing data volumes efficiently. The modern data stack supports this transition because its components are designed to operate across distributed systems and dynamic workloads.

Another driver is the demand for real-time analytics across operations such as digital services, finance, and supply management. Organizations increasingly rely on immediate insights rather than delayed reports to maintain service quality and operational continuity. Continuous data pipelines provide visibility into ongoing activity, making analytics part of daily workflows rather than a periodic function.

Restraint Analysis

Integration and Governance Complexity

Despite flexibility benefits, integration across multiple tools creates operational complexity. Data definitions, access permissions, and transformation logic must remain consistent across all layers, otherwise conflicting results may occur. Managing interoperability therefore requires strong governance frameworks and skilled technical oversight.

Security and compliance responsibilities also act as a restraint. Distributed architectures increase the number of access points where sensitive information is handled. Without coordinated policies and monitoring, organizations may face exposure risks or regulatory compliance challenges.

Opportunity Analysis

Data Democratization and Advanced Analytics

The architecture enables wider access to data within organizations. Business users can explore and interpret information through standardized interfaces without deep technical expertise, which increases analytical participation across departments. As more employees engage with data, operational improvements and process optimization opportunities expand.

Another opportunity comes from combining analytics with machine learning workflows. Clean, structured data pipelines support predictive models and automated decision systems. This alignment allows organizations to transform historical reporting into forward-looking intelligence and operational forecasting.

Challenge Analysis

Cost Control and Data Quality Assurance

Managing operational costs becomes challenging because multiple specialized components must be coordinated efficiently. Improper data movement or redundant storage can increase resource usage and operational overhead. Continuous optimization is required to maintain efficiency while scaling analytics operations.

Ensuring reliable data quality across the pipeline is also difficult. Data passes through ingestion, transformation, and consumption layers where errors can propagate if not detected early. Organizations must implement validation processes to maintain analytical accuracy and trust.

Top Emerging Trends

A notable trend is the shift toward automated data transformation and testing. Continuous validation checks are being embedded directly into pipelines so that inconsistencies are detected during processing rather than after reporting. This reduces manual intervention and improves reliability of analytical outputs.

Another emerging trend is hybrid processing where operational analytics and historical analysis operate together. Real-time processing supports immediate decisions while centralized storage enables long-term strategic evaluation. The combined model balances speed and depth of insight.

Customer Impact: Trends and Disruptors

Users benefit from faster access to reliable information because data flows continuously from source to dashboard. Operational teams can respond to events quickly and reduce delays in service delivery or planning activities. Improved transparency strengthens trust in internal reporting.

The shift also changes the role of analytics from specialized technical function to routine operational tool. Departments interact with data directly, enabling evidence-based decisions at multiple levels of the organization. This broader participation reshapes how businesses manage performance and customer engagement.

Key Market Segments

By Component

- Software/Solutions

- Services

By Deployment Mode

- Cloud-based

- On-premises

By Organization Size

- Large Enterprises

- Small and Medium-sized Enterprises

By Technology Layer

- Data Ingestion and Integration

- Data Storage and Warehousing

- Data Transformation and Modeling

- Data Analysis and Visualization

- Data Orchestration and Observability

- Others

By End-User Industry

- Technology and Software

- Financial Services

- Retail and E-commerce

- Media and Advertising

- Others

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Cloud data platform leaders such as Snowflake and Databricks anchor the modern data stack market. Amazon Web Services, Microsoft, and Google provide scalable storage, compute, and managed analytics services. These vendors support separation of storage and compute, elastic scaling, and integrated AI workloads. Demand is driven by cloud migration and the need for unified analytics across structured and unstructured data.

Data integration and transformation providers such as Fivetran, Stitch, and Airbyte streamline data movement into cloud warehouses. dbt Labs enables analytics engineering and version-controlled transformations. Confluent supports real-time data pipelines. These players benefit from rising adoption of ELT architectures and API-driven data ecosystems.

Business intelligence and observability vendors such as Looker, Tableau, Mode, Preset, and Monte Carlo enhance analytics consumption and data reliability. These tools improve dashboard accuracy and governance. Other vendors expand innovation and ecosystem integration, supporting steady growth of the modern data stack across enterprises.

Top Key Players in the Market

- Snowflake

- Databricks

- Amazon Web Services

- Microsoft

- Fivetran

- dbt Labs

- Confluent

- Stitch

- Airbyte

- Looker

- Tableau

- Mode

- Preset

- Monte Carlo

- Others

Recent Developments

- In January 2026, ClickHouse launched a native, enterprise-grade Postgres service tightly integrated with its real-time analytics platform, creating a unified data stack for modern applications. Built with Ubicloud, this offering combines Postgres for transactions with ClickHouse for analytics, delivering 10x faster performance via NVMe storage and seamless CDC syncs.

- In September 2025, Airbyte was named a Leader in Snowflake’s Modern Marketing Data Stack Report for Integration & Modeling. The San Francisco-based open data platform excels at moving structured and unstructured data to Snowflake AI Data Cloud, supporting AI-ready marketing pipelines.

- In April 2025, Fivetran acquired Census to add reverse ETL capabilities, enabling governed, real-time data activation back into business apps. This expands end-to-end data movement across modern stacks.

Report Scope

Report Features Description Market Value (2025) USD 615.3 Million Forecast Revenue (2035) USD 5,374.1 Million CAGR(2025-2035) 24.2% Base Year for Estimation 2024 Historic Period 2020-2024 Forecast Period 2025-2035 Report Coverage Revenue forecast, AI impact on Market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends Segments Covered By Component (Software/Solutions, Services), By Deployment Mode (Cloud-based, On-premises), By Organization Size (Large Enterprises, Small and Medium-sized Enterprises), By Technology Layer (Data Ingestion and Integrationm, Data Storage and Warehousing, Data Transformation and Modeling, Data Analysis and Visualization, Data Orchestration and Observability, Others), By End-User Industry (Technology and Software, Financial Services, Retail and E-commerce, Media and Advertising, Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA Competitive Landscape Snowflake, Databricks, Google, Amazon Web Services, Microsoft, Fivetran, dbt Labs, Confluent, Stitch, Airbyte, Looker, Tableau, Mode, Preset, Monte Carlo, Others Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- Snowflake

- Databricks

- Amazon Web Services

- Microsoft

- Fivetran

- dbt Labs

- Confluent

- Stitch

- Airbyte

- Looker

- Tableau

- Mode

- Preset

- Monte Carlo

- Others

Our Clients

- 177913

- Feb. 2026