Global Mineral Oil Market Size, Share, Growth Analysis By Type (Paraffinic Oil, Naphthenic Oil, Aromatic Oil), By Grade (Technical Oil, White Oil), By End-User (Personal Care, Food and Beverages, Pharmaceutical, Others) , By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2025-2034

- Published date: Feb 2026

- Report ID: 179491

- Number of Pages: 308

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

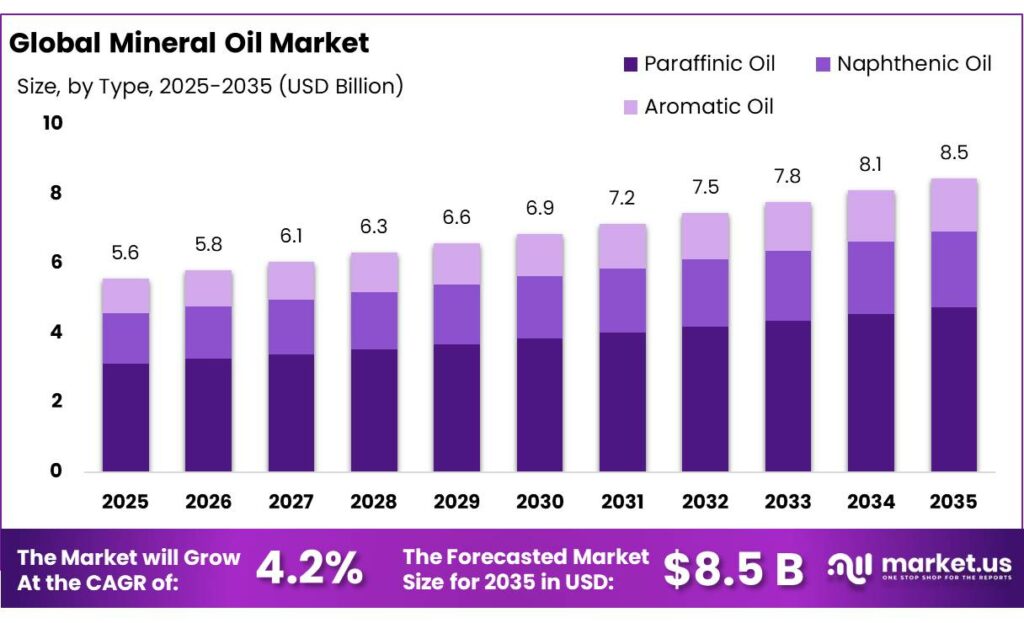

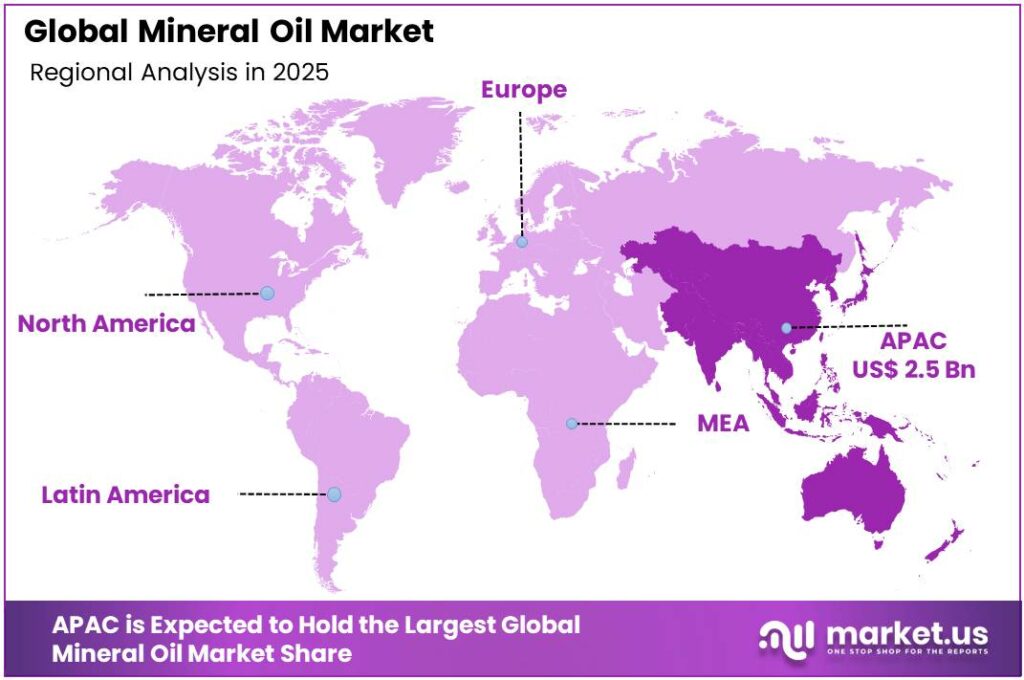

The Global Mineral Oil Market is expected to be worth around USD 8.5 Billion by 2035, up from USD 5.6 Billion in 2025, at a CAGR of 4.2% from 2026 to 2035. The Asia Pacific segment maintained 46.1%, supporting a Mineral Oil value of USD 2.5 Bn.

Mineral oil in the food industry refers primarily to highly refined “white” or food-grade mineral oils, which are mixtures of paraffinic and naphthenic hydrocarbons purified to remove aromatic fractions and meet pharmacopeial and food-additive standards.

The Joint FAO/WHO Expert Committee on Food Additives (JECFA) defines food-grade mineral oil as a mixture of highly refined paraffinic and naphthenic hydrocarbons with a boiling point above 350 °C and lists it as a glazing agent, lubricant and release agent under INS 905d. JECFA has established acceptable daily intakes of 0–20 mg/kg body weight per day for high-viscosity food-grade mineral oil and 0–10 mg/kg body weight per day for medium-viscosity food-grade mineral oil, providing a toxicological benchmark for global regulators and manufacturers.

From an industrial perspective, food-grade mineral oils sit within an expanding global agrifood system that generated around USD 3.8 trillion of agriculture value added in 2022, up from USD 3.0 trillion in 2013, an average annual increase of 2.9 percent according to FAO macro indicators. As food and beverage plants scale and automate, mineral-oil-based lubricants and release agents are widely used in mixers, conveyors, canning lines, and packaging equipment.

Regulatory authorities have intensified surveillance of mineral oil hydrocarbons (MOH) in food. EFSA’s 2023 update on MOH risk assessment analysed 80 632 analytical results from 2011–2021, which, after data cleaning, yielded 73 122 results covering 7 840 food samples across Europe.

For mineral oil saturated hydrocarbons (MOSH), EFSA estimated the highest dietary exposure in young consumers at 0.085–0.126 mg/kg body weight per day on average, with 95th-percentile exposures of 0.157–0.212 mg/kg body weight per day, and concluded that current MOSH exposure does not raise health concerns but warrants continued control.

Government and NGO testing has highlighted contamination hotspots and driven initiatives. A Foodwatch campaign tested 152 branded products in five European countries and found MOAH residues in 19 products, or 12.5 percent of the sample, at concentrations ranging from 0.63 to 82 mg/kg of food, prompting calls for stricter limits. In response, the European Commission and Member States have stepped up monitoring; a 2024 AGRINFO briefing notes that EFSA’s 2023 evaluation considered 6 120 MOAH sample results, 90 percent of which were submitted after 2017 following EU recommendations for intensified surveillance.

Parallel Codex work in the Committee on Fats and Oils has reconfirmed high-viscosity mineral oil (ADI 0–20 mg/kg body weight per day) and medium-viscosity mineral oil (ADI 0–10 mg/kg body weight per day) as acceptable previous cargoes for edible oils, anchoring global trade rules. In the United States, FDA’s 21 CFR 172.878 permits white mineral oil as a direct food additive in defined uses, such as a release and anti-sticking agent in hard candy up to 500 ppm, and as a component of tablet coatings, creating a clear compliance framework for manufacturers.

Key Takeaways

- Mineral Oil Market is expected to be worth around USD 8.5 Billion by 2035, up from USD 5.6 Billion in 2025, at a CAGR of 4.2%.

- Paraffinic Oil held a dominant market position, capturing more than a 56.2% share.

- Technical Oil held a dominant market position, capturing more than a 67.3% share.

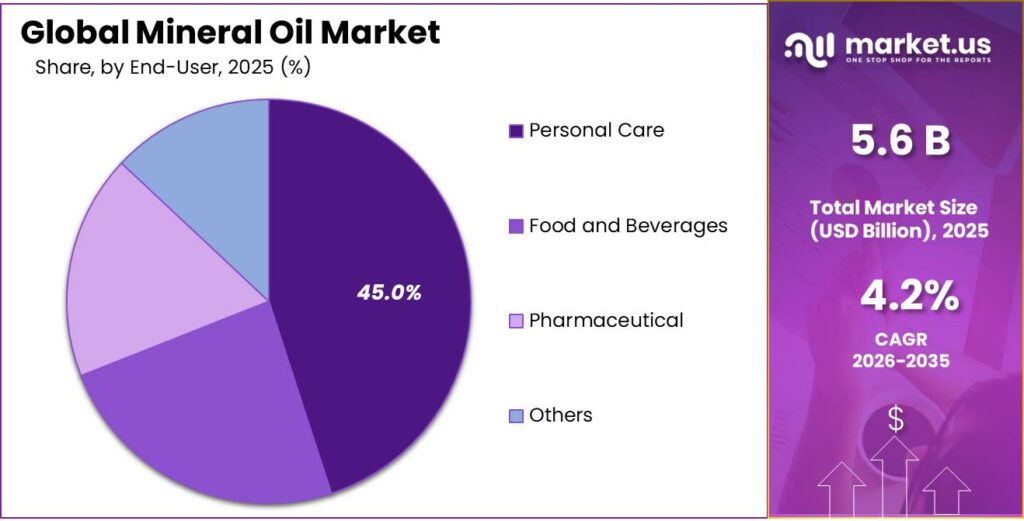

- Personal Care held a dominant market position, capturing more than a 45.6% share.

- Asia Pacific is the clear backbone of the global mineral oil market, with Asia Pacific dominating at around 46.1% of market share, equivalent to roughly USD 2.5 billion.

By Type Analysis

Paraffinic Oil leads the market with a strong 56.2% share in 2024

In 2024, Paraffinic Oil held a dominant market position, capturing more than a 56.2% share, driven by its broad usability, high purity levels, and strong adoption across industrial, automotive, and process-lubrication applications. Its thermal stability and oxidation resistance made it a preferred base fluid for manufacturers seeking consistent performance at scale.

Throughout 2024, demand remained steady across transportation, power equipment, metalworking, and general manufacturing, as industries continued to shift toward cleaner, more stable mineral-oil formulations. Paraffinic oil’s ability to maintain viscosity under varying temperatures also strengthened its acceptance in engine oils and hydraulic systems, supporting its commanding presence during the year.

By Grade Analysis

Technical Oil dominates with 67.3% share, reflecting its wide industrial utility

In 2024, Technical Oil held a dominant market position, capturing more than a 67.3% share, supported by its extensive use in manufacturing, processing industries, metalworking fluids, textiles, rubber production, and general machinery lubrication. Its versatility, cost-effectiveness, and stable performance in high-temperature and continuous-operation environments made it the preferred grade for industrial users.

Throughout 2024, demand was further supported by rising production activities across chemicals, plastics, automotive components, and heavy machinery, all of which rely on technical-grade mineral oils for lubrication, heat transfer, and equipment protection. Industries also favored this grade for its reliability in bulk applications where consistent performance matters more than ultra-high purity, reinforcing its strong lead in the market.

By End-User Analysis

Personal Care leads the market with 45.6% share, supported by strong consumer demand

In 2024, Personal Care held a dominant market position, capturing more than a 45.6% share, driven by the rising use of mineral oil in skincare, haircare, baby care, and cosmetic formulations. The segment benefited from mineral oil’s purity, non-reactive nature, and proven safety profile when refined to cosmetic-grade standards.

Throughout 2024, manufacturers leveraged mineral oil for its ability to provide smooth texture, enhance moisture retention, and stabilize formulations in creams, lotions, ointments, makeup removers, and petroleum jelly products. Growing demand for affordable and gentle skincare solutions across both mass and dermatology-backed brands helped personal care retain its leading market position. Additionally, baby oils and sensitive-skin products continued to rely on highly refined mineral oils due to their mildness and long-standing consumer trust.

Key Market Segments

By Type

- Paraffinic Oil

- Naphthenic Oil

- Aromatic Oil

By Grade

- Technical Oil

- White Oil

By End-User

- Personal Care

- Food and Beverages

- Pharmaceutical

- Others

Emerging Trends

Increased focus on mineral oil hydrocarbon (MOH) monitoring and contamination control in food systems

One of the most noteworthy trends shaping the mineral oil sector today is the expanded regulatory and scientific focus on monitoring mineral oil hydrocarbons (MOH) in the food chain, particularly in processed foods and food contact materials. This trend is not just about numbers; it reflects rising public concern and growing government action aimed at making food safer for consumers.

Recent work by the European Food Safety Authority (EFSA) captures this shift clearly. In its updated risk assessment published in 2023, EFSA drew on a massive dataset of 92,851 analytical results on mineral oil saturated hydrocarbons (MOSH) and mineral oil aromatic hydrocarbons (MOAH) submitted by food authorities and laboratories across Europe. These occurrence data span a wide range of foods and provide the most detailed view of MOH exposure in the region to date.

The detailed monitoring has been accompanied by practical regulatory actions. Since the European Commission Recommendation (EU) 2017/84, EU Member States have systematically been sampling and testing food products, food contact materials, and related production equipment for MOH contamination. Monitoring does not happen in isolation; food business operators, manufacturers and processors are actively involved, indicating a more collaborative approach to managing mineral oil exposures in food.

For the mineral oil industry specifically, this trend has a dual effect. On the one hand, increased monitoring raises awareness of unwanted MOH contamination, leading some food companies to seek alternative processing fluids or stricter control methods. On the other hand, it creates demand for higher-purity mineral oil products that meet tightened specifications, better analytical documentation, and traceable quality assurance systems that food producers can trust when audited by regulators or third-party certifiers.

Drivers

Expanding And Tightly Regulated Global Food Production

One of the strongest long-term drivers for mineral oil demand is the sheer scale and industrialisation of the global food system. Food today moves through long, complex value chains that rely on conveyors, mixers, fillers, ovens, mills and packaging lines – and most of that equipment needs reliable lubrication, release agents and protective fluids based on highly refined mineral oils.

- According to the Food and Agriculture Organization (FAO), global agriculture value added reached USD 4.0 trillion in 2023, up from USD 3.9 trillion in 2022, a year-on-year increase of 2.6% in real terms.

The impact of this scale is visible in the numbers reported by leading food manufacturers. Nestlé, one of the world’s largest food and beverage groups, generated CHF 91.4 billion in sales in 2024 (reported as CHF 91,354 million), with operations spanning beverages, nutrition, confectionery and pet care, all of which depend on high-throughput factories and automated lines.

Government regulation is not dampening this demand; instead, it is reshaping it toward cleaner, better-controlled grades of mineral oil. In the European Union, the European Food Safety Authority (EFSA) updated its risk assessment on mineral oil hydrocarbons (MOH) in food in 2023, highlighting that MOH can enter food via machinery lubricants, processing aids and food contact materials and recommending that exposure be kept as low as reasonably achievable. A 2024 AGRINFO briefing summarising this work notes that EFSA’s evaluation drew on 6,120 food samples with MOAH data, 90% of them submitted after 2017 as monitoring intensified across member states.

In the United States, the Food and Drug Administration (FDA) has long provided a clear legal framework for white mineral oil in food through 21 CFR 172.878. The regulation allows white mineral oil in defined uses, for example as a release, sealing and polishing agent in confectionery at levels not exceeding 0.2% of the finished product, and as a dust control agent on grains at levels no more than 0.02% by weight of grain.

Restraints

Rising Health Worries And Tighter Food-Safety Limits On Mineral Oil Hydrocarbons

A major brake on the mineral oil market today is growing concern about mineral oil hydrocarbons (MOSH/MOAH) in the food chain and the wave of regulation that follows. What used to be seen as a routine lubricant or release agent is now under far closer scrutiny, especially in Europe, where food authorities, NGOs and consumers are all pushing in the same direction: keep mineral oil residues in food as low as technically possible. For mineral oil suppliers, that means some traditional uses are shrinking, specifications are getting tougher every year, and customers are demanding cleaner alternatives.

Consumer campaigns have made the issue very visible. In one widely cited set of tests, the NGO Foodwatch analysed 120 dry food products and found that 83% of the samples contained more than 2 mg of MOSH per kilogram of food, while MOAH was detected in 43% of the samples. A later Foodwatch summary reports that 43% of products tested were contaminated with potentially carcinogenic mineral oil components, underlining how common these residues are in everyday foods like rice, pasta and breakfast cereals.

Regulators have taken note. The European Food Safety Authority (EFSA) has repeatedly highlighted that mineral oil aromatic hydrocarbons (MOAH) are the real concern. EFSA explains that some MOAH with three or more aromatic rings may act as genotoxic carcinogens, meaning they can damage DNA and potentially cause cancer, and that for such substances no safe exposure level can be defined.

On the policy side, the European Commission has moved from recommendations to concrete control tools. Following Commission Recommendation (EU) 2017/84, EU countries started systematically monitoring mineral oil hydrocarbons in food and food-contact materials. By 2023, EFSA’s evaluation was drawing on 6,120 food samples with MOAH data, 90% of which were submitted after 2017, reflecting how strongly monitoring has ramped up. EU Member States agreed indicative “limits of quantification” for MOAH of 0.5 mg/kg for low-fat foods (≤4% fat), 1 mg/kg for foods with 4–50% fat, and 2 mg/kg for fats and oils or foods with more than 50% fat, and committed to withdraw or recall products that exceed these levels.

Opportunity

Rising Global Food Production and Processing Drives Mineral Oil Demand

One of the clearest and most human reasons mineral oil has strong growth potential lies in the sheer scale and ongoing expansion of global food production. As more food is grown, processed, packaged, and distributed around the world, demand for dependable industrial fluids like mineral oil – especially in plant machinery, conveyors, lubricants and release agents – grows alongside.

Tthe Food and Agriculture Organization of the United Nations (FAO) shows that the global harvested area for primary crops reached 1.5 billion hectares in 2024, with significant increases in both oil crops and staple foods. Oil crops alone grew by 50 percent since 2010, rising to 1.2 billion tonnes of production in 2024, while cereals production hit 3.1 billion tonnes in the same year. Agricultural output like this drives expansive food processing that in turn relies on mineral-oil-based technologies in machinery and packaging systems.

Human stories underscore this shift: as small producers adopt modern milling, canning and packaging operations to serve urbanizing populations, more equipment is installed in processing facilities ranging from vegetable oil refineries to bakery lines. Every new conveyor, oven or filler requires lubrication that is safe, stable and able to operate non-stop. Highly refined mineral oils, including technical and food-grade variants, fit this need economically and reliably. The FAO’s continued investment in measuring these trends, through platforms like FAOSTAT which collects agricultural production and trade data from 245+ countries and territories, speaks to the increasing transparency and professionalisation of agriculture and food processing worldwide.

Government initiatives aligned with food security and production expansion only amplify this effect. Many countries are prioritising infrastructure upgrades in food processing and storage as part of national agricultural strategies. Although not always explicit about mineral oils, such programs indirectly support machinery and industrial lubricants demand. For example, Brazil’s Plano Safra 2025/2026 allocated R$ 516.2 billion (Brazilian reais) in subsidised credit to growers and processors, enabling investment in modern equipment and facilities that rely on quality lubrication and operational fluids.

At the same time, the growth of value-adding sectors such as aquaculture and specialty food production further increases demand for processing infrastructure. The FAO has set ambitious targets like a 35 percent increase in global aquaculture production by 2030, partly to help fight hunger and undernourishment. Growth like this expands cold-chain systems, feed processing lines and packaging – all of which depend on dependable industrial fluids.

Regional Insights

Asia Pacific leads the mineral oil market with a 46.1% share, reflecting its deep industrial and energy needs

Asia Pacific is the clear backbone of the global mineral oil market, with Asia Pacific dominating at around 46.1% of market share, equivalent to roughly USD 2.5 billion in value, supported by its huge energy appetite, fast-growing vehicle base and intensive manufacturing. The region is now the world’s main energy consumer: the Energy Institute’s Statistical Review of World Energy reports that Asia Pacific accounts for 47% of total global energy demand and has driven around 65% of the global increase in energy demand in recent years, underlining how central the region is to fuel and lubricant consumption.

On the industrial side, Asia and Oceania have become a manufacturing powerhouse. According to the UNIDO Industrial Statistics Factsheet for Asia and Oceania (2025), manufactured goods made up 82.8% of the region’s total merchandise exports in 2024, highlighting the weight of factory-based, energy-intensive activity in the regional economy.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

ExxonMobil operates in over 60 countries and manages more than 20 refineries and petrochemical complexes worldwide. The company employs nearly 62,000 people and supplies a broad range of mineral-oil-based lubricants, transformer oils and industrial fluids under its global brands. With advanced R&D capabilities and large-scale base-oil production exceeding 40,000 barrels per day across multiple facilities, ExxonMobil remains a dominant supplier to automotive, manufacturing, energy and marine sectors requiring highly refined, consistent-quality mineral oil formulations.

Shell operates across 70+ countries and maintains more than 46,000 service stations, making it one of the world’s largest lubricant suppliers. Its workforce of over 90,000 employees supports production of mineral-oil-based engine oils, hydraulic fluids, gear oils and industrial lubricants. Shell’s global blending plants exceed 50 facilities, enabling consistent supply to automotive, construction, marine and manufacturing sectors. The company’s mineral-oil portfolio benefits from strong research capabilities, advanced additive integration and a deep global distribution network.

BP operates in more than 70 countries, supplying fuels, lubricants and mineral-oil-based industrial solutions. The company manages over 18,000 retail sites globally and supports production across several large refineries and petrochemical facilities. With a workforce of nearly 70,000 employees, BP leverages its integrated supply chain to serve automotive, industrial and manufacturing sectors. Its mineral-oil offerings benefit from strong logistics, a global distribution footprint and deep technical capabilities, strengthening its position in fast-growing Asian and North American markets.

Top Key Players Outlook

- British Petroleum

- RENKERT OIL

- Exxon Mobil Corporation

- Sonneborn LLC

- Shell PLC

- Petro-Canada

- ENEOS Xplora Inc.

- SINOPEC Group

- Seojin Chemical

- Sasol

Recent Industry Developments

In 2025, BP announced a planned sale of a 65% stake in its Castrol lubricants business valued at about USD 6 billion, demonstrating clear strategic value in its lubricant portfolio, which includes mineral-oil-based oils used globally in automotive and industrial markets.

In 2024, Shell reported revenue of approximately USD 284.31 billion, with operations spanning more than 70 countries and a workforce of around 96,000 people, giving it one of the widest industrial footprints in the energy and lubricant space.

Report Scope

Report Features Description Market Value (2025) USD 5.6 Bn Forecast Revenue (2035) USD 8.5 Bn CAGR (2026-2035) 4.2% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Type (Paraffinic Oil, Naphthenic Oil, Aromatic Oil), By Grade (Technical Oil, White Oil), By End-User (Personal Care, Food and Beverages, Pharmaceutical, Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA Competitive Landscape British Petroleum, RENKERT OIL, Exxon Mobil Corporation, Sonneborn LLC, Shell PLC, Petro-Canada, ENEOS Xplora Inc., SINOPEC Group, Seojin Chemical, Sasol Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- British Petroleum

- RENKERT OIL

- Exxon Mobil Corporation

- Sonneborn LLC

- Shell PLC

- Petro-Canada

- ENEOS Xplora Inc.

- SINOPEC Group

- Seojin Chemical

- Sasol

Our Clients

- 179491

- Feb 2026