Global Military Thermal Imaging Market Size, Share, Growth Analysis By Platform (Land, Air, Naval), By Technology (Uncooled Thermal Imaging, Cooled Thermal Imaging), By Application (Surveillance, Target Acquisition, Search and Rescue, Border Security), By End Use (Defense, Homeland Security), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Apr 2026

- Report ID: 183776

- Number of Pages: 300

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

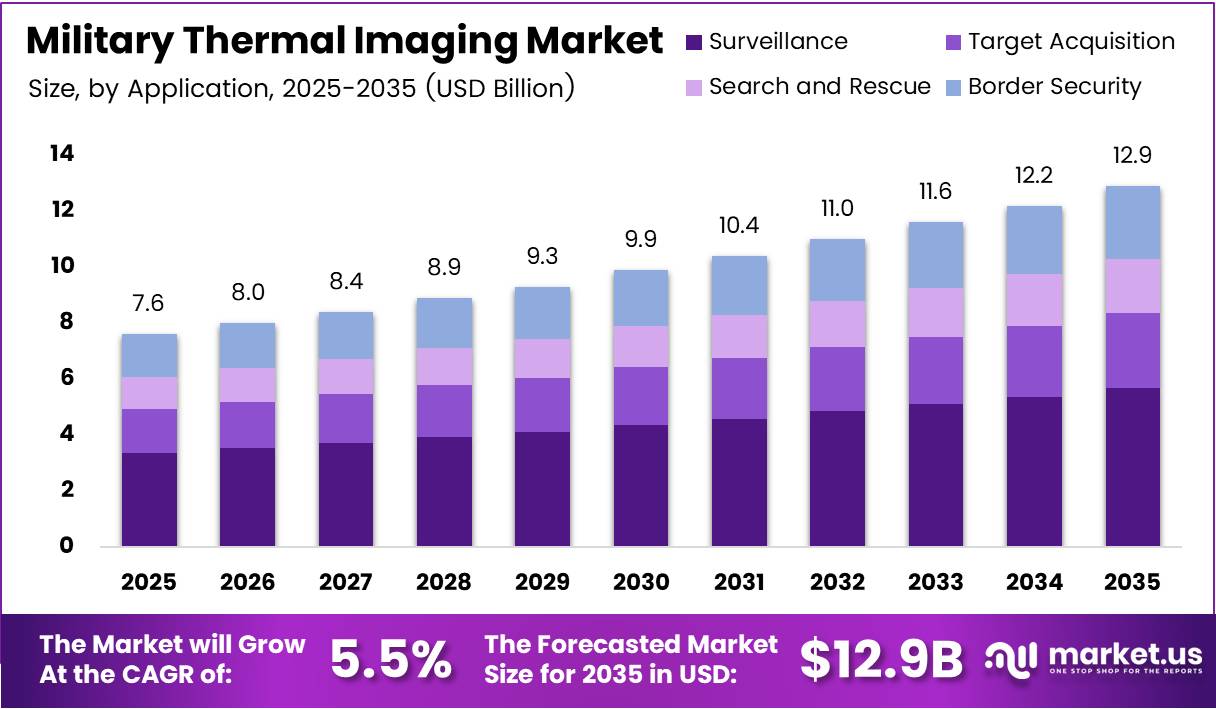

Global Military Thermal Imaging Market size is expected to be worth around USD 12.9 Billion by 2035 from USD 7.6 Billion in 2025, growing at a CAGR of 5.5% during the forecast period 2026 to 2035.

Military thermal imaging technology enables armed forces to detect, identify, and engage targets regardless of light conditions or time of day. Defense procurement agencies across North America, Europe, and Asia Pacific treat thermal imaging systems as non-negotiable components of modern battlefield readiness. This baseline demand insulates the market from discretionary budget cuts.

The market spans a broad operational spectrum, from individual soldier weapon sights to airborne surveillance pods and naval fire control systems. Each platform category carries distinct procurement cycles and vendor relationships. This diversity means that a slowdown in one platform segment rarely translates into a market-wide contraction, giving suppliers a structurally resilient revenue base.

Defense modernization programs across NATO member states and Indo-Pacific allies are actively replacing analog and first-generation night-vision equipment with digital thermal systems. These upgrade cycles create predictable, multi-year contract flows rather than one-time purchase events. For vendors with established government relationships, this translates directly into sustained backlog visibility.

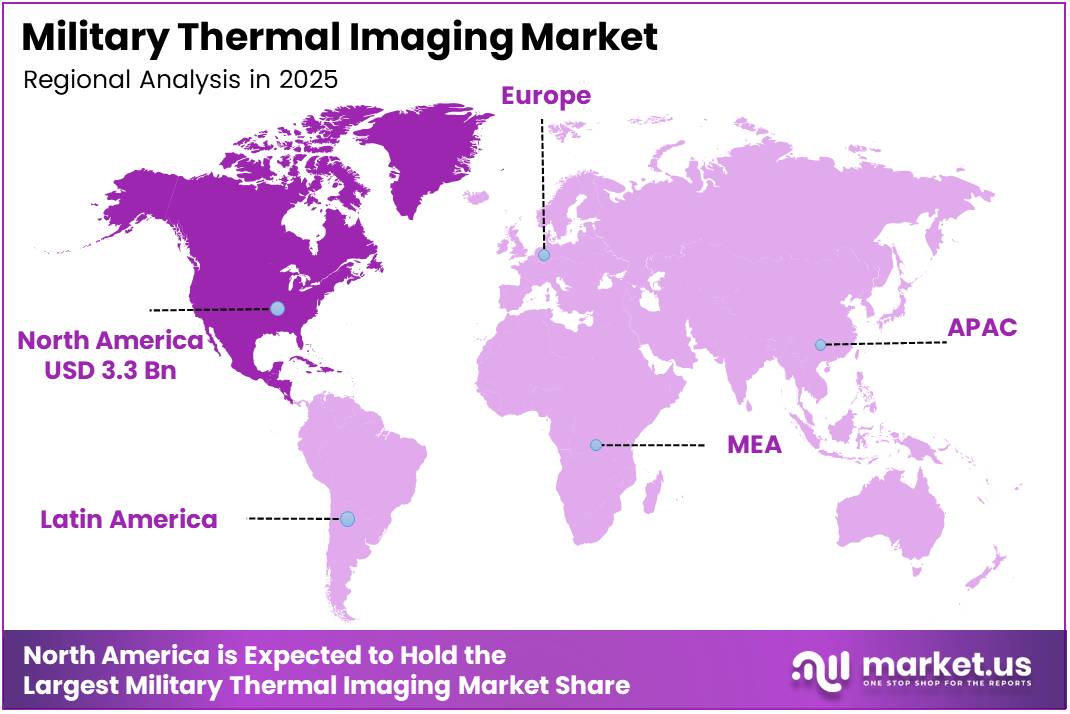

North America holds the dominant regional position, accounting for 43.8% of global market share, valued at approximately USD 3.3 Billion. The U.S. defense budget scale and mature procurement infrastructure allow American agencies to absorb large-volume orders that would strain procurement systems in smaller markets. This concentration also means that U.S. policy shifts carry disproportionate influence over global supplier strategies.

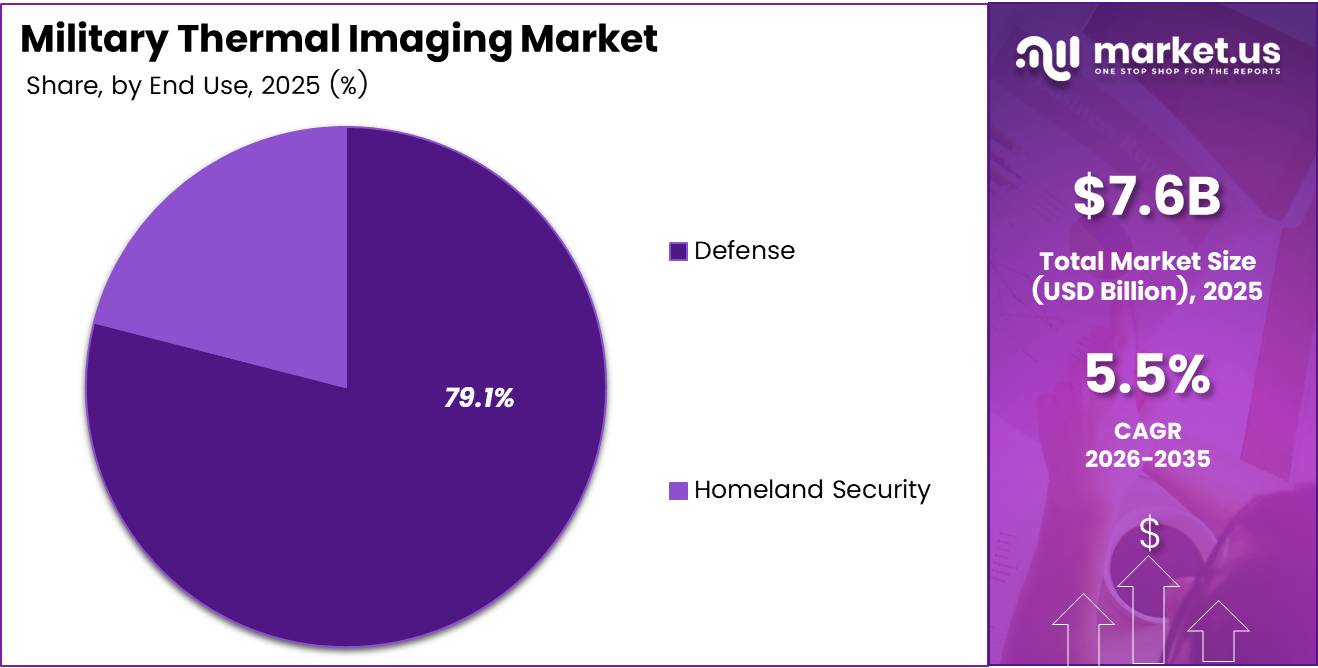

Uncooled thermal imaging leads the technology segment with a 63.9% share, reflecting a structural preference for lower-cost, lower-maintenance systems suited to infantry and vehicle applications. The defense segment commands 79.1% of end-use share, confirming that military buyers — not homeland security agencies — set the pace of procurement and technology requirements in this market.

According to Nature Scientific Reports, uncooled microbolometer detectors for military thermal systems achieve a Noise Equivalent Temperature Difference (NETD) below 50 mK and thermal response times under 10 ms at 17×17 µm pixel pitch in the LWIR band. This sensor performance level — now achievable at production scale — means procurement agencies can specify military-grade sensitivity without paying the premium previously associated with cooled systems, expanding the addressable budget pool for thermal upgrades.

In August 2024, Leonardo DRS secured a USD 117 million order from the U.S. Army for next-generation Family of Weapon Sights–Individual (FWS-I) uncooled thermal weapon sights. This single contract illustrates how individual soldier thermal programs now command nine-figure budgets, signaling that infantry-level thermal capability has moved from a specialized capability to a standard equipment line item in major military budgets.

Key Takeaways

- The global Military Thermal Imaging Market was valued at USD 7.6 Billion in 2025 and is forecast to reach USD 12.9 Billion by 2035.

- The market grows at a CAGR of 5.5% during the forecast period 2026 to 2035.

- By Platform, the Land segment holds the largest share at 42.8%, reflecting high volumes of ground vehicle and infantry equipment procurement.

- By Technology, Uncooled Thermal Imaging dominates with 63.9% share due to lower cost and maintenance advantages over cooled alternatives.

- By Application, Surveillance leads with 42.7% share, driven by persistent ISR requirements across all military branches.

- By End Use, the Defense segment accounts for 79.1% of market share, confirming military budgets as the primary demand engine.

- North America leads all regions with 43.8% market share, valued at approximately USD 3.3 Billion.

Product Analysis

Land dominates with 42.8% due to high ground force thermal equipment volumes.

In 2025, Land held a dominant market position in the By Platform segment of the Military Thermal Imaging Market, with a 42.8% share. Ground forces represent the largest and most frequently equipped branch of any military. Armored vehicles, weapon sights, and forward observer systems all require thermal capability, creating a procurement volume that air and naval platforms cannot match individually.

Air platforms carry some of the highest per-unit thermal imaging values in the military market. Aircraft-mounted targeting pods, forward-looking infrared systems, and UAV payloads demand high-resolution sensors capable of operating at altitude and speed. Consequently, while the Air segment trails Land in unit volume, it contributes disproportionately to revenue per contract, making it a high-margin growth area for sensor manufacturers.

Naval thermal imaging addresses a distinct set of operational requirements, including long-range maritime surveillance, anti-piracy operations, and above-deck fire control. Naval procurement cycles tend to be longer than land programs and tied closely to shipbuilding schedules. However, the integration of thermal systems into new vessel classes creates durable, multi-decade replacement demand that provides vendors with extended program lifetime revenue.

Technology Analysis

Uncooled Thermal Imaging dominates with 63.9% due to cost efficiency and lower field maintenance burden.

In 2025, Uncooled Thermal Imaging held a dominant market position in the By Technology segment of the Military Thermal Imaging Market, with a 63.9% share. According to Nature Scientific Reports, these systems now achieve NETD below 50 mK and response times under 10 ms, reaching performance levels that previously required cooled systems. This performance convergence removes the core technical objection to uncooled adoption and accelerates procurement across infantry and vehicle applications.

Cooled Thermal Imaging retains a critical role wherever maximum detection range and sensitivity are non-negotiable. Targeting systems for combat aircraft, long-range artillery fire control, and missile seekers rely on cooled sensors because their superior sensitivity supports engagement at distances where uncooled systems cannot consistently resolve targets. Despite their higher cost and mechanical complexity, cooled systems remain entrenched in high-value, mission-critical platform integrations where performance specifications are set by operational doctrine rather than budget constraints.

Application Analysis

Surveillance dominates with 42.7% due to persistent ISR demand across all force levels.

In 2025, Surveillance held a dominant market position in the By Application segment of the Military Thermal Imaging Market, with a 42.7% share. Modern military doctrine places persistent intelligence, surveillance, and reconnaissance at the center of all operational planning. Thermal imaging systems support surveillance continuously, regardless of weather or light conditions, making them indispensable for forward observation posts, perimeter security, and strategic monitoring.

Target Acquisition represents one of the highest-performance application categories in the market. Systems designed for target acquisition must resolve and classify threats at maximum range with minimal false-positive rates. This requirement drives demand for high-resolution sensors — as LinkedIn technical analysis notes, upgrading from a 640×480 sensor to a 1280×1024 sensor more than doubles identification range from approximately 365 meters to 780 meters. That performance gap justifies premium procurement budgets for this application category.

Search and Rescue applications extend thermal imaging procurement beyond combat roles into humanitarian and disaster response missions. Military units deployed for search and rescue operations rely on airborne and ground-based thermal systems to locate survivors in low-visibility environments. This dual-use demand profile means search and rescue thermal budgets often survive force restructuring cycles that cut purely offensive capabilities.

Border Security sits at the intersection of military and law enforcement procurement, creating a broader buyer base than purely combat-oriented applications. Thermal surveillance towers, vehicle-mounted systems, and handheld imagers all serve border security operations. This application segment benefits from homeland security budget allocations that are structurally separate from traditional defense spending, effectively widening the funding sources available to vendors.

End-Use Analysis

Defense dominates with 79.1% due to scale of military platform integration programs.

In 2025, Defense held a dominant market position in the By End Use segment of the Military Thermal Imaging Market, with a 79.1% share. The scale of military procurement programs — covering individual soldiers, ground vehicles, aircraft, and naval vessels simultaneously — generates a demand volume that no other end-use category approaches. Defense ministries also drive the technology specifications that the entire market develops around, giving them structural influence beyond their purchasing share.

Homeland Security represents a distinct and supplementary demand channel, covering border patrol agencies, coast guards, and national police forces with military-grade equipment needs. While homeland security budgets are smaller than defense allocations, they operate on independent procurement cycles. This independence means homeland security orders can partially offset slowdowns in core defense spending, giving vendors a meaningful buffer against single-budget dependency.

Key Market Segments

By Platform

- Land

- Air

- Naval

By Technology

- Uncooled Thermal Imaging

- Cooled Thermal Imaging

By Application

- Surveillance

- Target Acquisition

- Search and Rescue

- Border Security

By End Use

- Defense

- Homeland Security

Drivers

Defense Modernization Programs and Expanding Border Security Mandates Drive Thermal Imaging Procurement

Armed forces worldwide are replacing first-generation night-vision equipment with advanced thermal imaging systems as part of structured modernization programs targeting enhanced situational awareness. These upgrade cycles are multi-year, budget-committed programs — not discretionary purchases — which means procurement activity continues even during periods of broader defense spending restraint. For vendors with approved supplier status, this creates durable, forecastable contract pipelines.

Night vision and surveillance capability gaps identified in recent operational reviews have pushed defense ministries to accelerate thermal integration into armored vehicles and combat aircraft. According to LinkedIn technical analysis, upgrading from a 640×480 to a 1280×1024 sensor more than doubles identification range from 365 meters to 780 meters. That measurable performance jump gives procurement planners a concrete ROI case for investing in higher-specification systems, shortening budget approval timelines.

Rising border security concerns add a second independent procurement stream that reinforces defense spending. Governments that are politically constrained from expanding traditional defense budgets often increase homeland security and border surveillance allocations. Thermal imaging satisfies both spending categories simultaneously, allowing the same product line to address multiple budget pools. This dual eligibility structurally reduces vendor revenue concentration risk.

Restraints

High System Costs and Environmental Performance Gaps Limit Procurement Scale and Operational Deployment

Military-grade thermal imaging systems carry procurement prices and lifecycle maintenance costs that create genuine barriers for smaller defense budgets. Nations operating constrained defense spending — including many emerging market allies — cannot procure thermal systems at the volume and specification level that major NATO members can. This cost sensitivity concentrates advanced thermal capability among a relatively small group of high-spending defense markets and slows global adoption rates.

Performance degradation in extreme weather and harsh environmental conditions represents a technical constraint that procurement agencies cannot engineer around through budget decisions alone. Dense fog, heavy rain, and significant temperature differentials between a target and its surroundings all reduce effective detection range and image clarity. For military planners relying on thermal systems in equatorial or arctic environments, this limitation forces supplementary sensor investments that add to total system cost.

Together, these two restraints — high upfront cost and environment-conditional performance — create a procurement hesitancy that is most visible in mid-tier defense budgets. These buyers want the capability but cannot absorb the full system cost for all platforms simultaneously. Consequently, they prioritize thermal integration into a subset of critical platforms rather than achieving the full-force coverage that top-tier militaries pursue, which caps total addressable procurement volume in the near term.

Growth Factors

UAV Integration and Multi-Spectral Sensor Investment Open New High-Value Market Segments

Unmanned aerial vehicles have become a primary delivery platform for military thermal imaging capability, particularly for reconnaissance and persistent surveillance missions where manned aircraft carry unacceptable crew risk. The UAV thermal imaging segment combines the Air platform’s high revenue-per-unit profile with the volume characteristics of surveillance applications. This intersection creates one of the most commercially attractive growth segments in the broader market over the forecast period.

In October 2024, Thales secured selection by the Canadian Armed Forces to supply Sophie Ultima long-range handheld thermal imagers under Canada’s Night Vision Systems Modernization project — the first contract under that program. This award illustrates a wider pattern: allied nations are initiating structured thermal modernization programs that will generate sequential contracts across multiple equipment categories over several years, not single-event purchases.

Investments in multi-spectral and long-wave infrared imaging technologies expand what thermal systems can detect and classify, moving them beyond simple heat-source identification toward material discrimination and detailed threat characterization. For vendors, this capability expansion justifies premium pricing and creates upgrade cycles within existing customer relationships. Additionally, the development of lightweight thermal devices specifically for infantry soldiers addresses the largest single user population in any military, suggesting that this sub-segment carries substantial unit volume potential.

Emerging Trends

AI-Powered Processing and Augmented Reality Integration Redefine Thermal System Value Propositions

Artificial intelligence integration into thermal imaging processing pipelines shifts the system’s primary value from raw sensor data to actionable target intelligence. AI-powered target detection and tracking reduces the cognitive burden on individual operators and shortens the sensor-to-decision cycle. For procurement agencies evaluating system-level effectiveness rather than component-level specifications, this software-defined capability improvement can justify platform upgrades even when underlying sensor hardware has not changed.

Augmented reality integration with thermal imaging represents a convergence that fundamentally changes how soldiers receive and act on thermal data. Rather than viewing a separate thermal display, warfighters can receive overlaid thermal imagery directly in their field of view through AR-enabled headsets. This integration reduces reaction time in contact scenarios and removes the visual attention penalty associated with consulting secondary displays, creating a performance argument for AR-thermal systems that extends beyond novelty.

Demand for compact and portable thermal equipment reflects a structural shift in how militaries conceive of thermal access — moving from platform-mounted systems available only to specific operators toward individual-level capability distributed across an entire unit. High-resolution infrared sensor advancements are enabling this miniaturization without proportional performance loss. Vendors that solve the size-weight-power constraint for individual soldier systems will capture the broadest addressable user base in the market.

Regional Analysis

North America Dominates the Military Thermal Imaging Market with a Market Share of 43.8%, Valued at USD 3.3 Billion

North America holds 43.8% of global market share, valued at USD 3.3 Billion, supported by the scale of U.S. Department of Defense thermal procurement programs and mature defense industrial infrastructure. The U.S. Army’s multi-year FWS-I program, the Navy’s shipboard sensor upgrades, and Air Force targeting pod programs collectively sustain procurement volume that no other single national market can replicate. This concentration makes North America the reference market for global thermal imaging specifications.

Europe Military Thermal Imaging Market Trends

Europe represents the second-largest regional market, driven by NATO interoperability requirements and accelerating defense modernization across Germany, France, and the UK following geopolitical reassessments since 2022. Member states are increasing defense budgets toward the NATO 2% GDP target, with thermal imaging systems appearing consistently in equipment priority lists. This political commitment to higher defense spending translates directly into near-term procurement acceleration for European buyers.

Asia Pacific Military Thermal Imaging Market Trends

Asia Pacific is expanding thermal procurement driven by territorial disputes, maritime security concerns, and competing military modernization programs across China, India, South Korea, and Japan. India’s November 2025 tender for night-vision weapon sights with integrated thermal capability signals that large-population militaries are now moving thermal from specialized units to broader force-wide equipment standards. This transition from niche to standard equipment multiplies addressable unit volumes substantially.

Middle East and Africa Military Thermal Imaging Market Trends

Middle East defense spending on advanced surveillance and border monitoring systems sustains thermal imaging procurement across the GCC bloc. Ongoing regional security concerns and counter-terrorism operational requirements create demand for both fixed-installation thermal systems and vehicle-mounted platforms. Gulf state defense modernization programs frequently include thermal imaging as a core component of situational awareness infrastructure investments across land and maritime domains.

Latin America Military Thermal Imaging Market Trends

Latin America represents a developing market for military thermal imaging, with procurement concentrated among Brazil and Mexico. Counter-narcotics operations, border surveillance, and internal security missions create demand for tactical-grade thermal systems, though budgetary constraints slow the transition to the highest-specification military platforms. Incremental procurement of mid-tier thermal systems characterizes this region’s near-term market profile.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Raytheon positions itself at the intersection of sensor hardware and integrated weapons systems, giving it a structural advantage in programs where thermal imaging is bundled into broader platform contracts rather than procured as a standalone component. This systems integration capability means Raytheon competes not just on sensor performance but on program management scale — a barrier that pure sensor manufacturers cannot easily replicate. Their footprint across U.S. Army, Navy, and Air Force programs provides multi-branch revenue diversification.

Thales leverages its position as a preferred supplier to multiple European NATO members and allied nations, translating political relationships into durable contract pipelines. Their October 2024 selection by the Canadian Armed Forces for Sophie Ultima thermal imagers under the Night Vision Systems Modernization project demonstrates their ability to win first contracts in newly initiated national programs — a strategically important capability that opens multi-year follow-on procurement opportunities across allied defense markets.

FLIR Systems built its competitive positioning on the broadest product range in the thermal imaging industry, spanning military, commercial, and law enforcement applications. This breadth creates cross-market manufacturing scale that reduces per-unit production costs compared to purely military-focused competitors. In the military segment specifically, FLIR’s uncooled sensor expertise aligns directly with the dominant technology segment, giving them volume advantages in the product category that commands 63.9% of market share.

L3Harris Technologies differentiates through its electronic warfare and communications integration capabilities, allowing it to position thermal imaging as one element of a broader situational awareness package rather than a standalone purchase. This bundling strategy raises switching costs for military customers and increases average contract value per program. Their engagement across intelligence, surveillance, and reconnaissance platform categories provides exposure to the surveillance application segment that holds 42.7% of market share by application.

Key Players

- Raytheon

- Thales

- FLIR Systems

- L3Harris Technologies

- Northrop Grumman

- BAE Systems

- Leonardo

- Elbit Systems

- Hensoldt

Recent Developments

- 2024 – Theon Sensors reported approximately USD 50 million of new orders as its IRIS thermal clip-on sight gained commercial traction, with existing NYX, Mikron, and Argus night-vision users adding IRIS to extend their systems with thermal capability. This retrofit adoption pattern confirms that upgrade-path procurement — rather than full system replacement — represents a significant and underestimated revenue stream for thermal imaging vendors.

- November 2025 – The Indian Army issued a tender for night-vision weapon sights with integrated thermal capability, covering supply, installation, testing, and training. This tender signals that India — one of the world’s largest military forces by personnel — is moving thermal weapon sights toward broader infantry issue, potentially representing one of the largest single-nation thermal procurement programs outside the United States.

- 2024 – Leonardo DRS confirmed continued deliveries under the U.S. Army’s FWS-I IDIQ framework, sustaining multi-year procurement of uncooled thermal weapon sights to equip individual soldiers with day-night targeting capability. The IDIQ structure of this contract confirms that the U.S. Army treats individual soldier thermal sights as an ongoing standard equipment program rather than a one-time acquisition, creating predictable annual delivery volumes for the vendor.

Report Scope

Report Features Description Market Value (2025) USD 7.6 Billion Forecast Revenue (2035) USD 12.9 Billion CAGR (2026-2035) 5.5% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Platform (Land, Air, Naval), By Technology (Uncooled Thermal Imaging, Cooled Thermal Imaging), By Application (Surveillance, Target Acquisition, Search and Rescue, Border Security), By End Use (Defense, Homeland Security) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Raytheon, Thales, FLIR Systems, L3Harris Technologies, Northrop Grumman, BAE Systems, Leonardo, Elbit Systems, Hensoldt Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Military Thermal Imaging MarketPublished date: Apr 2026add_shopping_cartBuy Now get_appDownload Sample

Military Thermal Imaging MarketPublished date: Apr 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Raytheon

- Thales

- FLIR Systems

- L3Harris Technologies

- Northrop Grumman

- BAE Systems

- Leonardo

- Elbit Systems

- Hensoldt

Our Clients

- 183776

- Apr 2026