Global Magnesium Market By Compound Type (Magnesium Metal, Magnesium Alloy, Magnesium Oxide, Magnesium Chloride, Magnesium Hydroxide, Magnesium Sulfate, Magnesium Carbonate, and Others), By Application (Metal Processing, Automotive, Refractories, Rubber Processing, Pulp and Paper Processing, Chemical Intermediate, Aerospace and Defense, Electronics, and Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2025-2035

- Published date: Feb 2026

- Report ID: 179745

- Number of Pages: 300

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

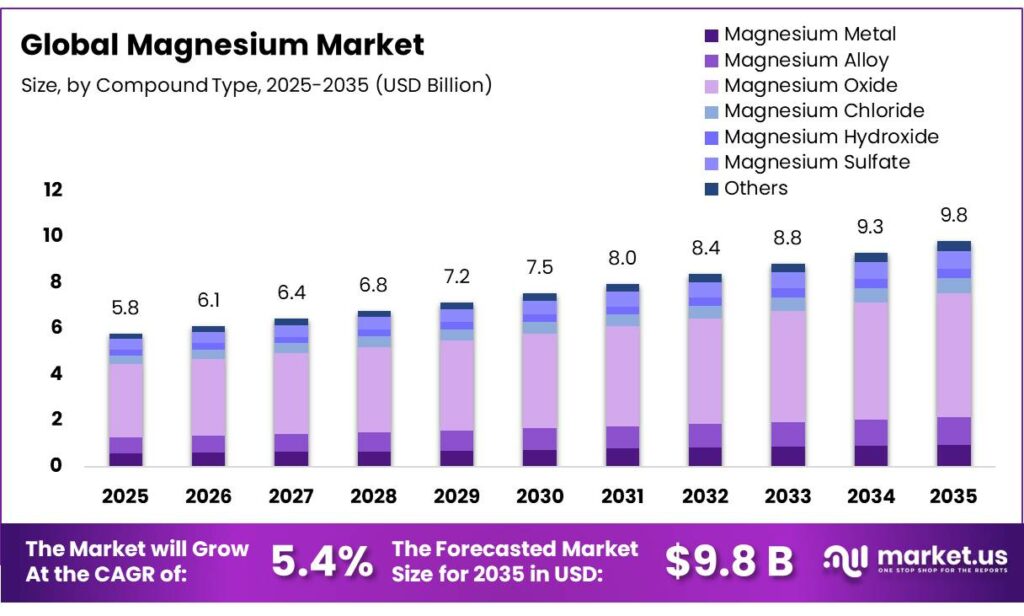

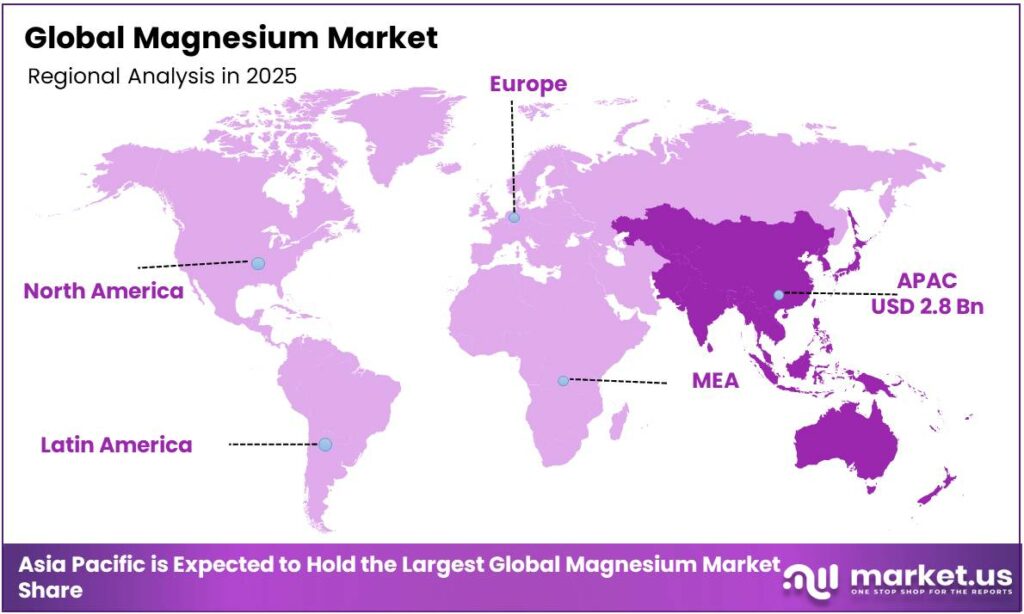

The Global Magnesium Market is expected to be worth around USD 9.8 Billion by 2035, up from USD 5.8 Billion in 2025, at a CAGR of 5.4% from 2026 to 2035. The Asia Pacific segment maintained 48.9%, supporting a Magnesium value of USD 2.8 Bn.

Magnesium is a versatile element that serves as a lightweight structural metal in industry and a critical essential mineral in the human body. It is a shiny, silvery-white metal that is roughly one-third lighter than aluminum. Magnesium is a vital nutrient for all living organisms. In plants, it is the central atom in chlorophyll, enabling photosynthesis. In the human body, it is a helper molecule (cofactor) for over 300 to 600 biochemical reactions, as cited in the National Institutes of Health (NIH).

- According to the United States Geological Survey (USGS), the global production of magnesium reached around 1.1 million metric tons, and the smelter capacity of around 1.8 million metric tons.

The magnesium market is fundamentally driven by its industrial versatility and concentration of supply in the Asia Pacific, particularly China. Magnesium oxide dominates consumption due to its high melting point, chemical stability, and broad applicability in refractories, construction materials, and environmental applications, while magnesium metal and alloys are primarily used in automotive, aerospace, and aluminum alloying.

- According to the USGS, the total recycled quantity of magnesium in the US alone in 2023 was 108,000 metric tons, valued at US$1.1 billion.

In addition, secondary recovery and recycling of magnesium scrap are increasingly significant, with recycled material providing energy-efficient alternatives to primary production.

Similarly, market dynamics are influenced by geopolitical factors, given the heavy concentration of production, and by competition from substitute materials such as aluminum, plastics, and calcium compounds in specific applications. The magnesium market is characterized by industrial specialization, high dependence on Asia Pacific supply, and strategic emphasis on efficiency, recycling, and material diversification.

Key Takeaways:

- The global magnesium market was valued at USD 5.8 billion in 2025.

- The global magnesium market is projected to grow at a CAGR of 5.4% and is estimated to reach USD 9.8 billion by 2035.

- Based on the compound type, magnesium oxide dominated the market, with a market share of around 54.7%.

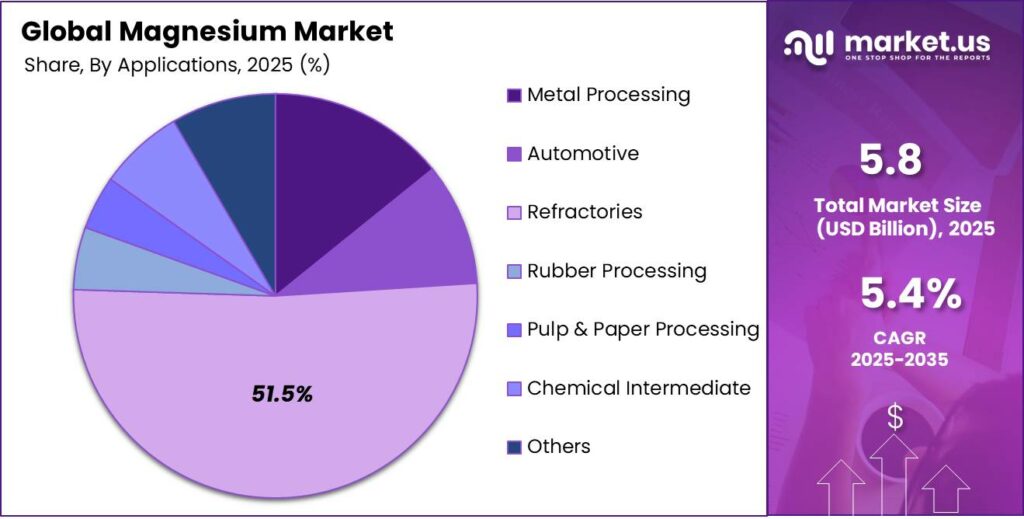

- Among the applications of magnesium, the refractories held a major share in the market, 51.5% of the market share.

- In 2025, the Asia Pacific was the most dominant region in the magnesium market, accounting for around 48.9% of the total global consumption.

Compound Type Analysis

Magnesium Oxide Held the Largest Share in the Market.

The magnesium market is segmented based on compound type into magnesium metal, magnesium alloy, magnesium oxide (MgO), magnesium chloride, magnesium hydroxide, magnesium sulfate, magnesium carbonate, and others. The magnesium oxide dominated the market, comprising around 54.7% of the market share, due to its chemical stability, high melting point of about 2,800 °C, non-combustibility, and broad functional versatility.

Unlike magnesium metal and alloys, which are lightweight but reactive, MgO is thermally stable and suitable for refractory linings in furnaces, kilns, and steelmaking vessels. Similarly, compared with magnesium chloride or magnesium sulfate, which are highly soluble and primarily used in de-icing, fertilizers, or chemical processing, MgO serves in construction materials, environmental remediation, electrical insulation, and pharmaceuticals.

Furthermore, magnesium hydroxide shares some neutralizing properties but decomposes at lower temperatures, limiting high-temperature industrial use. Magnesium carbonate is used as a filler or antacid but lacks MgO’s refractory strength. The combination of thermal resistance, chemical inertness, insulation capability, and cross-sector applicability makes magnesium oxide the most industrially versatile magnesium compound.

Application Analysis

Magnesium is Mostly Utilized in Refractories.

Based on the applications of magnesium, the market is divided into metal processing, automotive, refractories, rubber processing, pulp and paper processing, chemical intermediate, aerospace and defense, electronics, and others. The refractories dominated the magnesium market, with a market share of 51.5%. Most magnesium used in refractories is in the form of magnesium oxide (MgO) because its intrinsic material properties align directly with high-temperature industrial requirements.

Additionally, refractory applications consume large material volumes per installation, as linings must withstand continuous thermal and chemical stress and require periodic replacement. In contrast, metal processing and automotive applications primarily use magnesium metal or alloys, which are volume-efficient structural materials.

Similarly, rubber, pulp and paper, and chemical uses often involve smaller quantities of magnesium compounds for niche functional roles. The combination of bulk material intensity, durability requirements, and thermal stability makes refractory applications the dominant end use for magnesium oxide relative to other sectors.

Key Market Segments:

By Compound Type

- Magnesium Metal

- Magnesium Alloy

- Magnesium Oxide

- Magnesium Chloride

- Magnesium Hydroxide

- Magnesium Sulfate

- Magnesium Carbonate

- Others

By Application

- Metal Processing

- Automotive

- Refractories

- Rubber Processing

- Pulp and Paper Processing

- Chemical Intermediate

- Aerospace and Defense

- Electronics

- Others

Drivers

Metal Alloys and Steel Production Drive the Magnesium Market.

The magnesium market is primarily sustained by its application as an alloying agent and a chemical reagent in metallurgical processes, specifically within aluminum-base alloys and steel desulfurization. According to the U.S. Geological Survey (USGS), aluminum-base alloys accounted for 52% of secondary magnesium recovery and 18% of primary magnesium metal consumption in 2024. These alloys are critical for the packaging industry and the transportation sector, where aluminum-magnesium alloys provide high strength-to-weight ratios.

Additionally, magnesium additions to iron and steel transform graphite morphology in cast irons and assist in removing sulfur and oxygen impurities from molten blast-furnace iron, improving the mechanical properties of final products.

Magnesium metal consumption for the desulfurization of iron and steel represented 4% of primary magnesium use in 2024. These applications, automotive castings, alloying, and desulfurization, are major drivers of magnesium consumption in the metals and steel sectors.

Restraints

Competition from Substitute Materials for Specific Industries Might Hamper the Demand for Magnesium.

Competition from substitute materials presents a structural challenge to magnesium market expansion, particularly where cost-efficiency and corrosion resistance outweigh weight-reduction advantages. The higher relative costs remain a primary disadvantage for magnesium compared to its leading substitutes. For instance, aluminum and zinc metals serve as the primary substitutes for magnesium in castings and wrought products. Aluminum alloys are often preferred by automakers due to their lower production costs and well-established manufacturing infrastructure.

Similarly, in steel production, calcium carbide is a functional substitute for magnesium in desulfurization. While magnesium is chemically preferred to avoid acetylene production, calcium carbide remains a viable alternative based on availability and price. Furthermore, advanced carbon fiber and glass-reinforced polymers compete directly with magnesium in aerospace and ground transportation. Composites offer superior corrosion resistance and durability, addressing a key technical vulnerability of magnesium.

The U.S. Department of Energy (DOE) identifies low ductility, price instability, and joining difficulties in multi-material systems as major barriers to the market. The existence of technically and economically viable substitutes in defined end-use segments constrains material choice and necessitates ongoing evaluation of magnesium’s relative performance and cost.

Opportunity

Application of Magnesium in Construction and Battery Industries Creates Opportunities in the Market.

The magnesium market is currently buoyed by emerging high-growth opportunities in specialized construction materials and next-generation battery chemistries, driven by sustainability mandates and technical safety advantages. For instance, magnesium-based cements, specifically magnesium oxysulfate (MOS) and magnesium oxychloride (MOC), are increasingly utilized as low-carbon alternatives to Portland cement. MOS cements demonstrate rapid setting times, up to 60% reduction compared to standard blends, and high early compressive strength, reaching 18-23 MPa.

- According to the Global Cement and Concrete Association, alternatives to Portland cement are essential to meet 2050 net-zero targets, as the traditional sector contributes 8% of global CO₂ emissions.

Additionally, magnesium is a strategic candidate for post-lithium energy storage due to its geostrategic neutrality and inherent safety. Research published by Argonne National Laboratory and Tohoku University highlights that Mg-ion batteries eliminate dendrite formation, reducing thermal runaway risks by approximately 40% compared to lithium-ion counterparts.

Similarly, it offers a high volumetric energy density of about 3833 Ah/L and double the valence charge, making it optimal for grid-scale storage. Rechargeable magnesium battery chemistries, including magnesium-sulfur and magnesium-ion systems, are subjects of ongoing research due to attributes such as abundant anode material and the absence of dendrite formation.

Trends

Increased Recycling of Magnesium.

Increased recycling of magnesium, particularly from high-volume aluminum alloys and automotive scrap, is a significant trend driven by sustainability mandates and the energy-intensive nature of primary production.

According to the U.S. Geological Survey (USGS) Mineral Commodity Summaries, secondary magnesium recovery in the United States in 2023 consisted of about 100,000 tons, with approximately 75,000 tons from new scrap and 25,000 tons from old scrap.

Magnesium recycling uses substantially less energy than primary extraction. The recycled magnesium alloys require about 5%-10% of the energy needed for primary production, reflecting a quantifiable environmental efficiency benefit. The increased recycling is an operational trend in the magnesium supply chain, with recognized energy advantages defining its role in metal sourcing.

Geopolitical Impact Analysis

Geopolitical Tensions Are Impacting the Magnesium Market Due to Concentrated Production.

The magnesium supply chains are demonstrably affected by geopolitical tensions, primarily due to the metal’s status as a critical raw material for strategic industries, concentration of production, and export policy responses by major producers. China accounts for a major share of global primary magnesium output, making global supply highly concentrated in one geopolitical jurisdiction. This structural concentration exposes international manufacturing systems to political risk when regional policy shifts occur.

The International Energy Agency (IEA) notes that export restrictions on critical minerals, including magnesium and its compounds, have increased fivefold since 2017, directly impacting supply security for non-producing regions such as the EU and North America. China has introduced export restrictions on several critical minerals, argued to be in part a response to trade tensions, and institutional risk assessments have identified magnesium alongside antimony and bismuth as commodities with high supply-chain vulnerability to geopolitical factors.

While magnesium is not subject to the same explicit export bans as some minerals, its production concentration and the inclusion of magnesium in geopolitical risk assessments linked to critical mineral supply disruption reveal systemic sensitivity. Past disruptions in Chinese magnesium output, driven by environmental regulation enforcement, have caused sharp global price volatility and supply uncertainty in downstream industries heavily reliant on magnesium alloys.

Regional Analysis

Asia Pacific Held the Largest Share of the Global Magnesium Market.

In 2025, the Asia Pacific dominated the global magnesium market, led by China, holding about 48.9% of the total global consumption. The region serves as the primary production hub and the largest consumption center, driven by integrated supply chains in the automotive, electronics, and metallurgy sectors. According to the U.S. Geological Survey (USGS) 2025 Mineral Commodity Summaries, Asia Pacific, specifically China, maintains a near-monopoly on primary production.

- China produced approximately 950 thousand metric tons of magnesium in 2025, which accounted for around 86.4% of the global total.

China’s dominant role reflects its scale of downstream industrial use across sectors such as automotive die-casting, aluminum alloying, and industrial manufacturing. China’s aluminum industry is the world’s largest, consuming magnesium as a critical hardening agent. Similarly, China is the largest producer of EVs, and demand for magnesium die-cast parts for lightweighting of EVS is a primary market driver.

Additionally, Asia Pacific leads in the production of computers, communications, and consumer electronics (3C). Magnesium’s high electromagnetic shielding and heat dissipation properties make it the preferred material for high-end laptop and smartphone casings produced in the region. The concentration of production and consumption in the Asia Pacific, particularly China’s overwhelming share of output and use, positions the region as the principal global hub for magnesium industrial activity, underpinned by trade flows and consumption.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis:

Magnesium manufacturers focus on operational integration, process efficiency, product specialization, and supply security to strengthen competitive positioning. Producers emphasize vertical integration across mining, calcination, and smelting to control raw-material inputs and reduce supply risk.

Additionally, manufacturers invest in alloy development tailored for automotive die-casting, aerospace components, and aluminum alloying, enhancing mechanical performance, corrosion resistance, and castability to differentiate products. Furthermore, expanding secondary magnesium recovery and closed-loop recycling agreements with die-casters support cost control and sustainability compliance.

The Major Players in The Industry

- Alloys International, Inc.

- AMACOR

- American Elements

- Baowu Magnesium Industry Technology Co., Ltd.

- Bhagyanagar Magnesium

- Bunty LLC

- Compass Minerals

- Deusa International GmbH

- Exclusive Magnesium

- Grecian Magnesite

- ICL Group

- Jagannath Company

- Luxfer MEL Technologies

- Magontec Group

- Mani Agro Chem

- US Magnesium LLC

- Other Key Players

Key Development:

- In January 2026, the state of Utah successfully bid US$30 million to acquire the assets of U.S. Magnesium, LLC, the US’s sole primary magnesium producer, following its Chapter 11 bankruptcy filing in September 2025.

- In July 2025, Grecian Magnesite announced the successful commissioning and commencement of operations of a second X-ray-based mineral processing line at its Yerakini mine in northern Greece. This strategic investment effectively doubles the company’s magnesite sorting capacity and represents a significant advancement in its circular mining strategy.

Report Scope

Report Features Description Market Value (2025) US$5.8 Bn Forecast Revenue (2035) US$9.8 Bn CAGR (2025-2035) 5.4% Base Year for Estimation 2025 Historic Period 2021-2024 Forecast Period 2025-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Compound Type (Magnesium Metal, Magnesium Alloy, Magnesium Oxide, Magnesium Chloride, Magnesium Hydroxide, Magnesium Sulfate, Magnesium Carbonate, and Others), By Application (Metal Processing, Automotive, Refractories, Rubber Processing, Pulp and Paper Processing, Chemical Intermediate, Aerospace and Defense, Electronics, and Others) Regional Analysis North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA Competitive Landscape Alloys International, Inc., AMACOR, American Elements, Baowu Magnesium Industry Technology Co., Ltd., Bhagyanagar Magnesium, Bunty LLC, Compass Minerals, Deusa International GmbH, Exclusive Magnesium, Grecian Magnesite, ICL Group, Jagannath Company, Luxfer MEL Technologies, Magontec Group, Mani Agro Chem, US Magnesium LLC, and Other Players. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)

-

-

- Alloys International, Inc.

- AMACOR

- American Elements

- Baowu Magnesium Industry Technology Co., Ltd.

- Bhagyanagar Magnesium

- Bunty LLC

- Compass Minerals

- Deusa International GmbH

- Exclusive Magnesium

- Grecian Magnesite

- ICL Group

- Jagannath Company

- Luxfer MEL Technologies

- Magontec Group

- Mani Agro Chem

- US Magnesium LLC

- Other Key Players

Our Clients

- 179745

- Feb 2026