Global Liquid Makeup Market Size, Share, Growth Analysis By Product (Foundation, Eye Products, Concealer, Lip Products, Others), By Distribution Channel (Offline, Online), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Feb 2026

- Report ID: 179555

- Number of Pages: 299

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

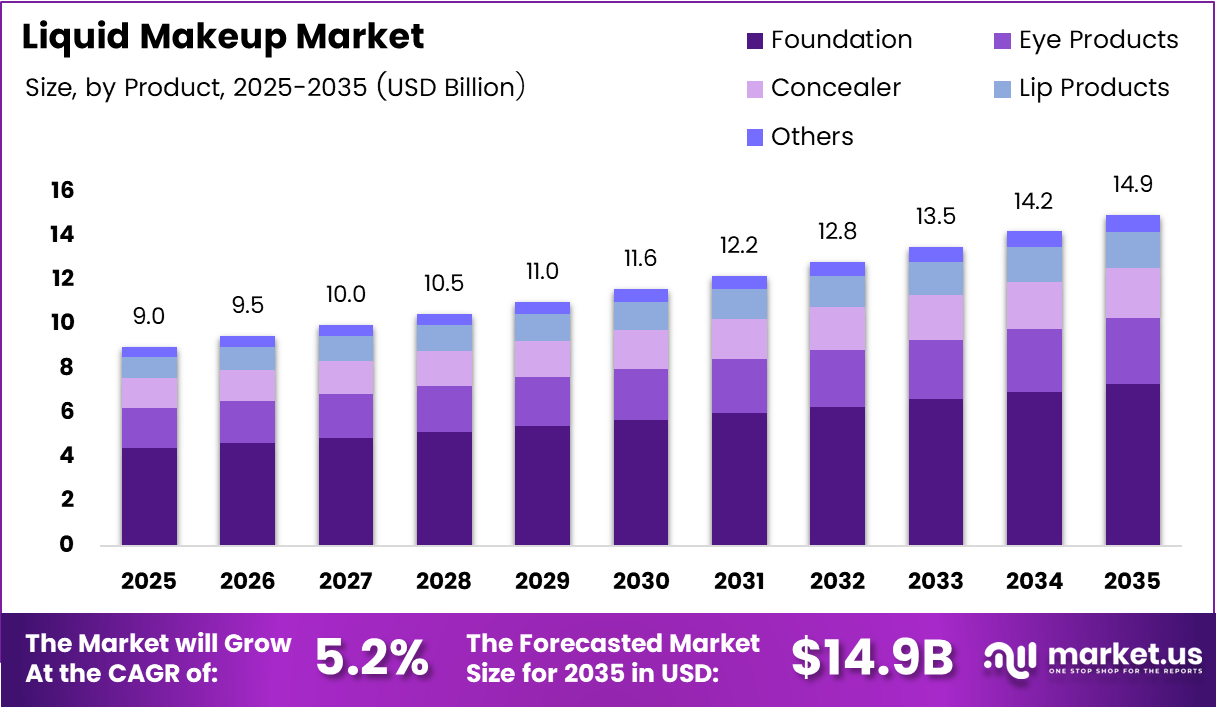

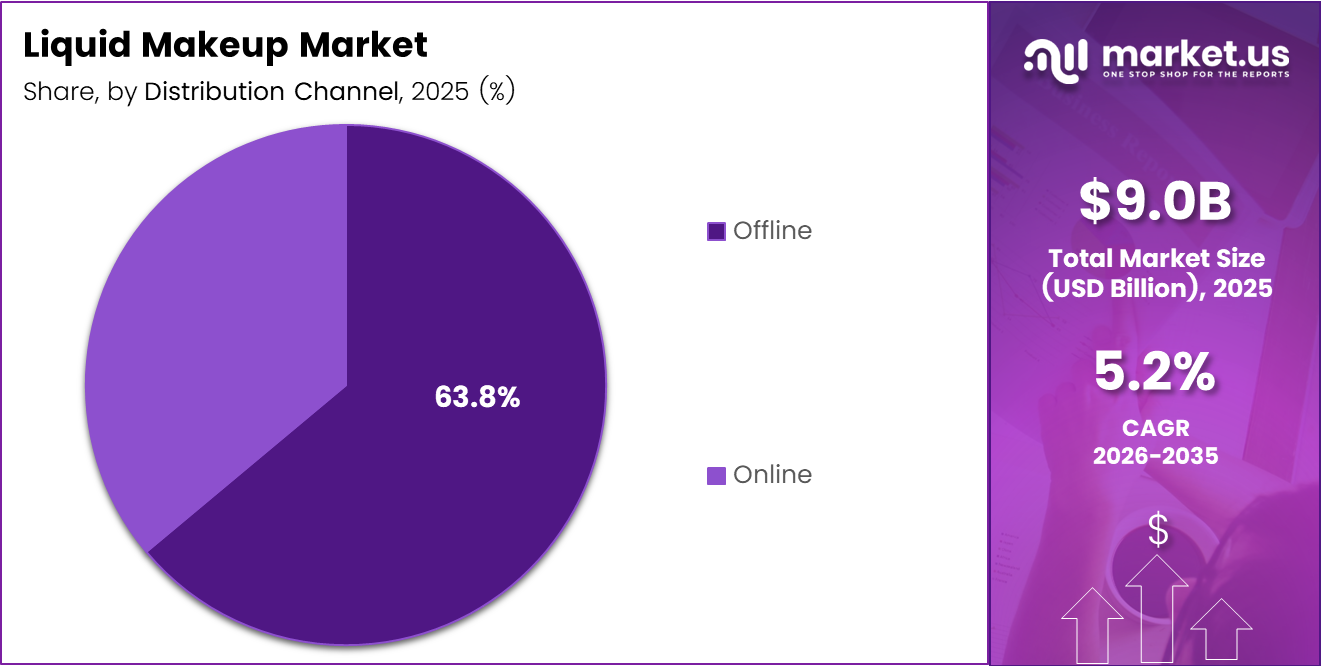

Global Liquid Makeup Market size is expected to be worth around USD 14.9 Billion by 2035 from USD 9.0 Billion in 2025, growing at a CAGR of 5.2% during the forecast period 2026 to 2035.

The liquid makeup market covers fluid-formulated cosmetic products including foundations, concealers, liquid eye products, and lip color. These products serve both everyday wear and professional use. Consumer preference now leans toward formulations that blend skincare and cosmetics, making this category structurally different from powder-based alternatives.

Foundation leads category sales and shapes the innovation pipeline for the entire segment. Brands now develop skin-tone-inclusive ranges to reach previously underserved demographics. This shift from one-size-fits-all to personalized shade systems reflects a structural change in how brands approach product development and customer acquisition.

Social media has reshaped how consumers discover and trial liquid makeup. Beauty tutorials on short-form video platforms accelerate product awareness from launch to purchase decision within days. This compression of the discovery-to-buy cycle gives brands with strong digital presence a measurable advantage over traditional retail-first competitors.

The professional grooming needs of working women worldwide continue to support category volume. As female workforce participation rises across Asia-Pacific and MENA economies, demand for reliable, long-wear liquid formulations increases in parallel. This demographic trend directly expands the addressable consumer base for mid-to-premium liquid makeup brands.

Product innovation now centers on hybrid formulations that combine foundation, serum, and SPF in a single product. In June 2025, Cénée Paris launched Rouge Hyaluronique, a hybrid liquid lipstick delivering +29% lip hydration after 28 days. This signals that hybrid cosmetic-skincare products are not a niche experiment but a commercially validated direction.

According to a report by Eugeng, energy-efficient practices in foundation filling machine production can save up to 30% in operational costs through reduced energy consumption. This means manufacturers investing in efficient production infrastructure now hold a structural cost advantage that compounds over time and compresses margins for less-equipped competitors.

According to Eugeng, 68% of manufacturers plan to adopt automation with real-time monitoring and data analytics to reduce errors and boost production efficiency in 2025. This shift toward smart manufacturing signals that production quality and consistency will become baseline competitive requirements, not differentiators, within the next two to three years.

Key Takeaways

- The global liquid makeup market was valued at USD 9.0 Billion in 2025 and is forecast to reach USD 14.9 Billion by 2035.

- The market will expand at a CAGR of 5.2% during the forecast period 2026 to 2035.

- By Product, Foundation dominated with a 48.3% share in 2025.

- By Distribution Channel, Offline channels led the market with a 63.8% share.

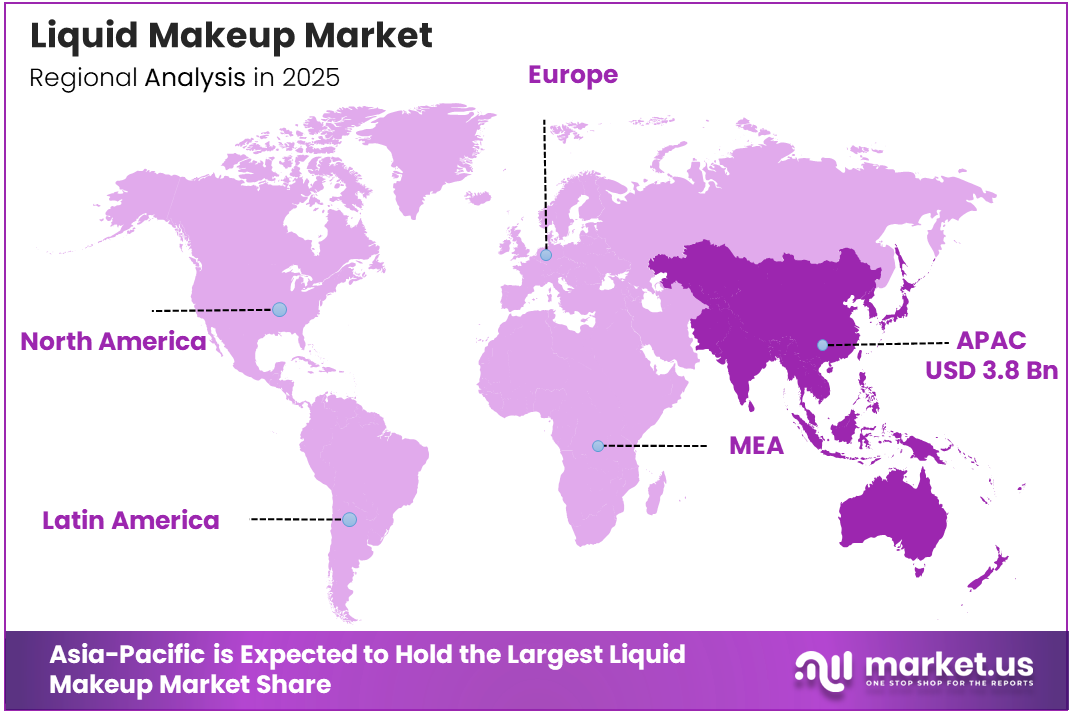

- Asia-Pacific held the largest regional share at 42.60%, valued at USD 3.8 Billion in 2025.

Product Analysis

Foundation dominates with 48.3% due to universal daily use and shade innovation.

In 2025, Foundation held a dominant market position in the By Product segment of the Liquid Makeup Market, with a 48.3% share. Its dominance reflects the category’s role as the core step in a full-face routine. Brands continue to invest in shade extension and skin-tone matching technology, making foundation the primary battleground for both shelf space and consumer loyalty.

Eye Products serve as the entry point for younger consumers exploring liquid makeup. Liquid eyeliners and eyeshadows offer visible impact with a smaller format price point, making them accessible trial products. Their role in the purchase funnel extends beyond standalone revenue — they frequently drive cross-category purchases including primers and concealers within the same brand.

Concealer carries strong repeat purchase behavior across all age groups. Consumers repurchase concealers more frequently than foundations due to higher daily usage intensity. This creates a stable, predictable revenue stream for brands, and positions concealer as a low-risk, high-loyalty SKU within a brand’s liquid makeup portfolio.

Lip Products in liquid format benefit from the hybrid cosmetic trend reshaping buyer expectations. Innovations like hyaluronic acid-infused liquid lipsticks — such as Cénée Paris’s Rouge Hyaluronique, which delivers +29% lip hydration after 28 days — signal that consumers now expect skincare performance from lip color. This raises the technical bar for all liquid lip product developers.

Others in the product mix include liquid blush, highlighter, and bronzer formats. These categories are growing in presence as part of the dewy, glass-skin finish trend. Their inclusion in brand portfolios signals a broader shift away from powder-based finishing products toward a fully liquid-based application routine.

Distribution Channel Analysis

Offline dominates with 63.8% due to tactile testing and in-store shade matching.

In 2025, Offline held a dominant market position in the By Distribution Channel segment of the Liquid Makeup Market, with a 63.8% share. Physical retail remains critical for liquid makeup because shade selection and texture evaluation require direct product contact. Consumers are reluctant to commit to full-size liquid foundation purchases without testing — a behavior that inherently favors brick-and-mortar formats over digital checkout.

Online distribution channels accelerate brand reach beyond the physical retail footprint. Direct-to-consumer platforms allow brands to gather first-party consumer data at the point of purchase, informing shade range expansion and formulation decisions. AI-powered shade matching tools now reduce the barrier of buying liquid makeup without a tester, making online the fastest-growing channel even as offline retains volume leadership.

Key Market Segments

By Product

- Foundation

- Eye Products

- Concealer

- Lip Products

- Others

By Distribution Channel

- Offline

- Online

Drivers

Hybrid Formulation Innovation and Professional Grooming Demand Accelerate Liquid Makeup Adoption

Consumer preference now favors liquid foundations that deliver a lightweight, skin-like finish with long-wearing performance. Brands respond by integrating SPF, hydration, and serum actives into single-product formulations. This product convergence shortens morning routines for working professionals while raising perceived value, which justifies premium price positioning across the foundation and concealer categories.

Working women represent the most commercially consistent buyer group in this market. As female workforce participation expands across Asia-Pacific and emerging economies, the daily demand for professional-grade liquid formulations strengthens. This demographic provides a structural volume floor that insulates the market from trend-driven fluctuations in consumer behavior.

According to Sciencedirect, switching to advanced biodegradable polymers such as PLA and WPC blends in cosmetic packaging reduces energy consumption by approximately 29.81% compared to traditional injection molding methods. This means brands adopting sustainable packaging now gain both an environmental credential and a measurable cost reduction — a rare combination that simultaneously satisfies regulatory pressure and investor scrutiny.

Restraints

Minimalist Beauty Trends and Regulatory Compliance Costs Constrain Market Expansion

Consumer interest in no-makeup aesthetics and simplified routines directly challenges the category’s volume growth. When consumers reduce their daily product count, liquid foundation and concealer are often the first products removed. This behavioral shift compresses repurchase frequency and forces brands to reformulate toward multi-benefit products that justify continued inclusion in a smaller routine.

Stringent cosmetic ingredient regulations across the EU, US, and APAC markets add significant cost and timeline to product development cycles. Clean label compliance requires ingredient substitutions that can alter texture and performance — the two attributes that drive consumer repurchase in liquid makeup. Smaller brands without dedicated regulatory teams face disproportionate compliance burden compared to large multinationals.

Together, these pressures create a two-sided squeeze on mid-tier brands: falling volume from minimalist trend adoption and rising costs from regulatory compliance. Brands that cannot absorb both pressures simultaneously face margin compression that limits their ability to invest in the shade range expansion and innovation needed to remain competitive.

Growth Factors

Inclusive Shade Expansion, Vegan Formulations, and D2C Channels Open New Revenue Segments

The expansion of vegan, cruelty-free, and dermatologically tested liquid makeup lines addresses a buyer segment that actively avoids conventional formulations. Retailers increasingly prioritize shelf space for certified clean products, which means brands with credible clean credentials gain distribution advantages that compound over time as retail gatekeepers align with consumer values.

Inclusive shade range development unlocks revenue from demographic groups historically underserved by mainstream cosmetic brands. Expanding from 20 to 50+ shades per foundation line is no longer a marketing choice — it is a market access requirement. Brands that commit to full-spectrum shade libraries capture loyalty from consumers who have experienced chronic mismatch and are unlikely to switch once a correct shade is found.

According to Sciencedirect, adoption of PLA in cosmetic packaging reduces lifecycle environmental impact by 18–30% and end-of-life impact by 26–42% compared to conventional plastics. For liquid makeup brands, this data point makes sustainable packaging a quantifiable operational commitment rather than a positioning claim, enabling credible ESG reporting and attracting sustainability-focused retail and investment partners.

Emerging Trends

AI Shade Matching, Sustainable Packaging, and Dewy Skin Aesthetics Reshape Liquid Makeup Product Strategy

The glass-skin and natural glow finish aesthetic drives reformulation across the foundation category. Consumers increasingly reject heavy-coverage, matte products in favor of formulations that create the appearance of healthy, luminous skin. This shift changes the performance benchmarks brands use to develop and market foundations, moving the conversation from coverage to skin quality enhancement.

AI-powered shade matching tools in online beauty retail remove the primary barrier to purchasing liquid makeup without physical testing. By reducing shade mismatch returns and increasing purchase confidence, these tools accelerate conversion rates in digital channels. Early adopters gain a measurable data advantage as AI tools generate shade preference data that directly informs future product line expansion decisions.

According to Sephora’s Global Impact Report, in-store collection programs gathered approximately 100 tonnes of beauty packaging empties in 2024, with expansion planned toward 100% valorization of unsold products by 2030. This trajectory signals that sustainable packaging and refillable liquid makeup formats will shift from optional brand differentiators to retail listing requirements within the next five years.

Regional Analysis

Asia-Pacific Dominates the Liquid Makeup Market with a Market Share of 42.60%, Valued at USD 3.8 Billion

Asia-Pacific held 42.60% of the global liquid makeup market in 2025, valued at USD 3.8 Billion. This leadership reflects the region’s combination of large urban consumer populations, high beauty spending among younger demographics in China, Japan, South Korea, and India, and a strong cultural emphasis on skincare-cosmetic routines that structurally favors liquid-format products over powder alternatives.

North America Liquid Makeup Market Trends

North America remains a premium product stronghold driven by mature retail infrastructure and high per-capita beauty spending. The US market sustains strong demand for shade-inclusive foundation lines and hybrid skincare-cosmetic formulations. Direct-to-consumer brand growth in this region has accelerated portfolio diversification beyond traditional department store distribution channels.

Europe Liquid Makeup Market Trends

Europe leads globally in clean beauty regulation compliance, making it the benchmark market for ingredient transparency and sustainable packaging adoption. EU cosmetic ingredient restrictions have pushed brands to reformulate faster than in other regions. This regulatory pressure gives Europe-compliant products a ready pathway into other markets adopting similar standards.

Latin America Liquid Makeup Market Trends

Latin America presents a structurally underpenetrated opportunity for liquid makeup brands, particularly in Brazil and Mexico where beauty spending per consumer is rising. Offline retail remains dominant, and drugstore and mass-market distribution channels control the majority of volume. Expanding mid-market shade ranges for diverse Latin skin tones represents the clearest entry strategy for new market participants.

Middle East and Africa Liquid Makeup Market Trends

The Middle East drives premium liquid makeup consumption through high-income urban populations in GCC countries. Long-wear and transfer-resistant formulations perform particularly well given the region’s climate and cultural application preferences. Africa remains an early-stage market where affordable, high-coverage liquid foundations hold the most immediate commercial potential as modern retail infrastructure expands.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Shiseido Co., Ltd. positions itself at the intersection of Japanese skincare science and global cosmetic retail. Its liquid makeup lines integrate high-performance skincare actives into foundation formulations, which aligns precisely with consumer demand for hybrid products. This science-led positioning commands premium price points and builds brand equity that is difficult for trend-driven competitors to replicate.

FENTY BEAUTY fundamentally restructured how the industry approaches shade inclusivity. By launching with 40 foundation shades at market entry, the brand set a new commercial standard that forced competitors to expand their own shade ranges. This strategic move created a loyalty moat among consumers who had previously experienced chronic shade exclusion, giving FENTY a durable consumer base with strong repeat purchase behavior.

Benefit Cosmetics LLC differentiates through category-specific product innovation and a strong in-store service model. Its brow and complexion product expertise drives consistent cross-category purchase behavior within its consumer base. By anchoring brand identity to specific complexion solutions rather than full-line cosmetics, Benefit reduces head-to-head competition with mass-market players across the entire liquid makeup category.

Estée Lauder Inc. leverages its multi-brand portfolio to compete simultaneously across prestige, mid-tier, and accessible luxury segments. Within liquid makeup, its foundation franchises maintain long product lifecycles supported by consistent reformulation investment. This portfolio breadth allows Estée Lauder to absorb category shifts — such as the move toward hybrid skincare-cosmetic products — without disrupting its core revenue base.

Key Players

- Shiseido Co., Ltd.

- FENTY BEAUTY

- Benefit Cosmetics LLC

- Estée Lauder Inc.

- Dior

- L’Oreal Paris

- The Avon Company

- KIKO

- HUDA BEAUTY

Recent Developments

- October 2025 — Wonderskin debuted Hyper-Bond Serum Foundation, a liquid serum-foundation hybrid that sets in 10–20 minutes to a breathable, second-skin finish. The product combines advanced skincare benefits with full-coverage makeup performance, reflecting accelerating consumer demand for multi-functional liquid formulations.

- September 2025 — Cénée Paris launched Teint Céramides, a buildable moisturizing liquid blush formulated with 91–94% natural-origin ingredients. The product incorporates ceramides and pre- and postbiotics to actively strengthen the skin barrier, positioning it as a skincare-first cosmetic product rather than a traditional color cosmetic.

Report Scope

Report Features Description Market Value (2025) USD 9.0 Billion Forecast Revenue (2035) USD 14.9 Billion CAGR (2026-2035) 5.2% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product (Foundation, Eye Products, Concealer, Lip Products, Others), By Distribution Channel (Offline, Online) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Shiseido Co., Ltd., FENTY BEAUTY, Benefit Cosmetics LLC, Estée Lauder Inc., Dior, L’Oreal Paris, The Avon Company, KIKO, HUDA BEAUTY Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- Shiseido Co., Ltd.

- FENTY BEAUTY

- Benefit Cosmetics LLC

- Estée Lauder Inc.

- Dior

- L'Oreal Paris

- The Avon Company

- KIKO

- HUDA BEAUTY

Our Clients

- 179555

- Feb 2026