Global KYC Orchestration Platform Market By Component (Software/Platform, Services), By Deployment Mode (Cloud-based, On-premises), By Organization Size (Large Enterprises, Small and Medium-sized Enterprises (SMEs)), By Application (Customer Onboarding, Ongoing Due Diligence & Monitoring, Others), By End-User Industry (Banking, Insurance, FinTech & Crypto), By Regional Analysis, Global Trends and Opportunity, Future Outlook By 2025-2035

- Published date: Feb. 2026

- Report ID: 176906

- Number of Pages: 273

- Format:

-

keyboard_arrow_up

Quick Navigation

- Report Overview

- Top Market Takeaways

- Key Insights

- Drivers Impact Analysis

- Restraint Analysis

- By Component

- By Deployment Mode

- By Organization Size

- By Application

- By End User Industry

- Emerging Trends Analysis

- Growth Factors Analysis

- Opportunity Analysis

- Challenge Analysis

- Investor Type Impact Matrix

- Technology Enablement Analysis

- Key Market Segments

- Regional Analysis

- Competitive Analysis

- Future Outlook

- Recent Developments

- Report Scope

Report Overview

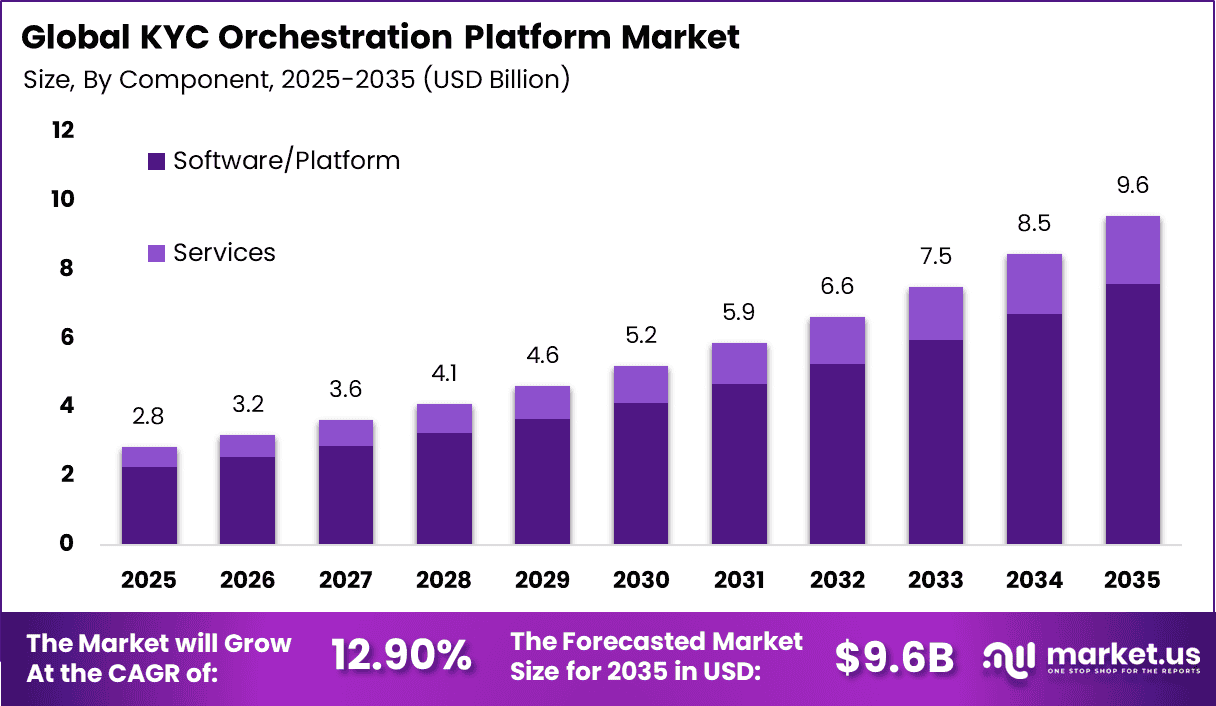

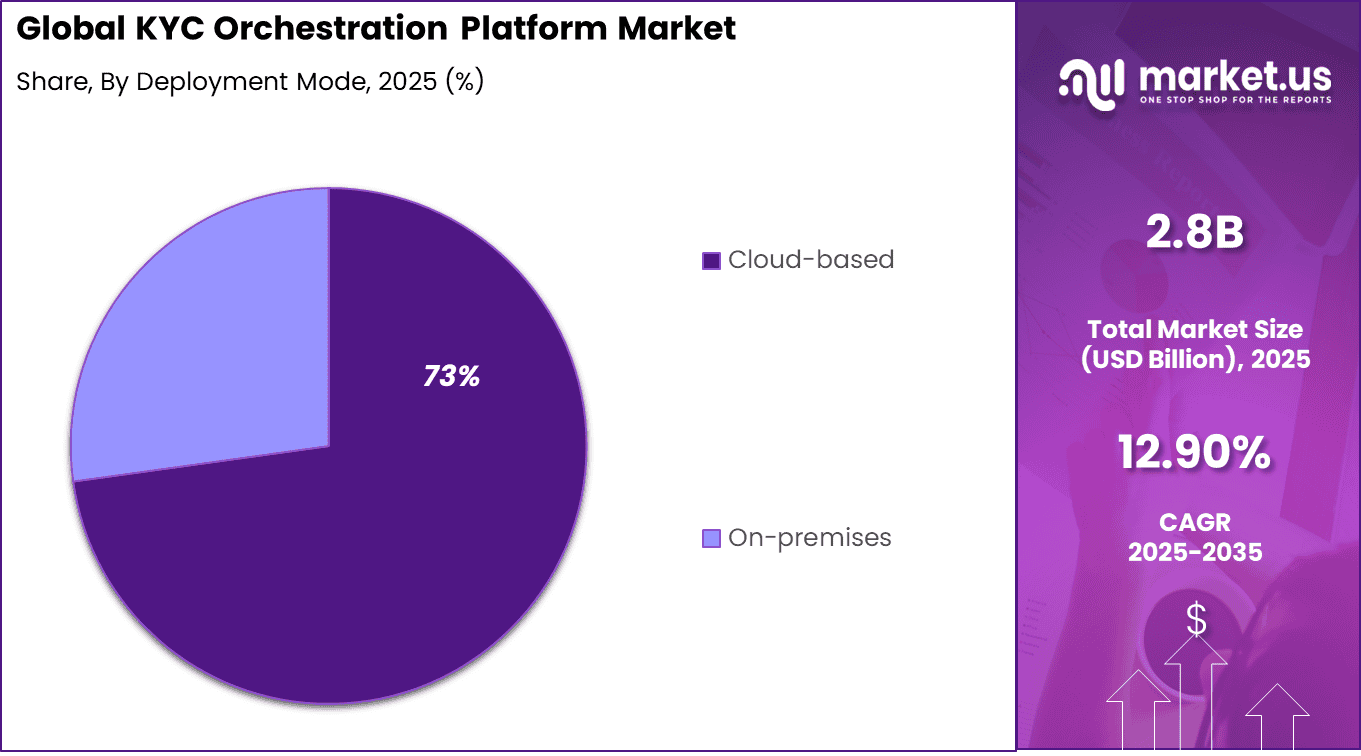

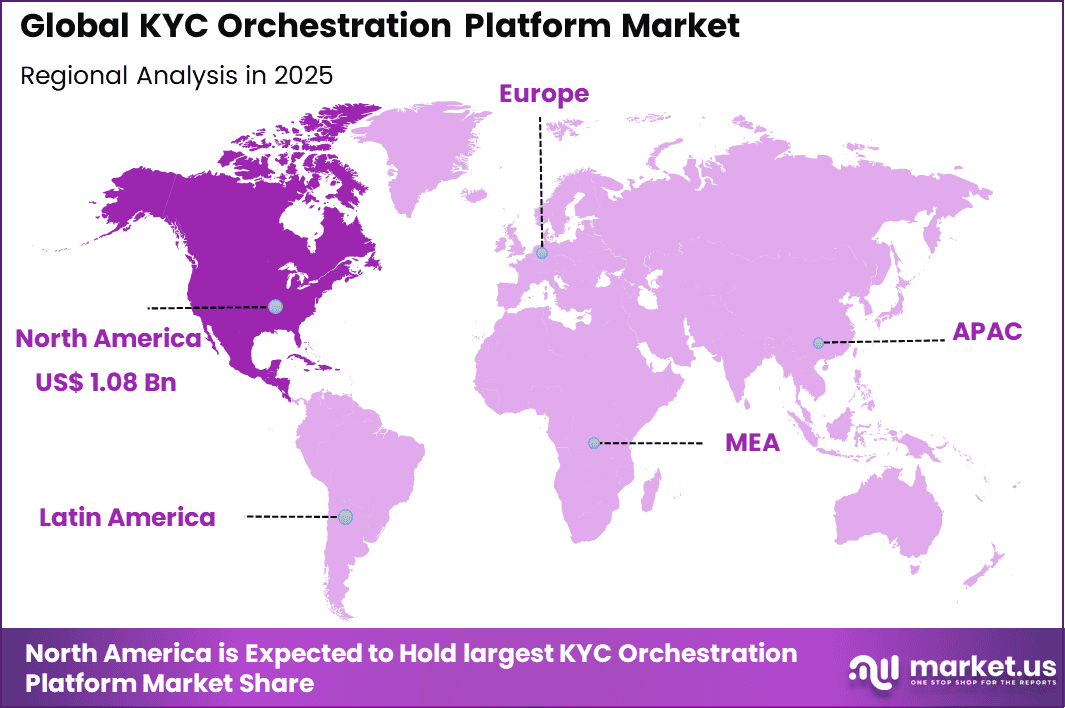

The Global KYC Orchestration Platform Market generated USD 2.8 billion in 2025 and is predicted to register growth from USD 3.2 billion in 2026 to about USD 9.6 billion by 2035, recording a CAGR of 12.90% throughout the forecast span. In 2025, North America held a dominant market position, capturing more than a 38.1% share, holding USD 1.08 Billion revenue.

The KYC Orchestration Platform Market refers to technology platforms that coordinate, manage, and automate the entire know your customer verification process across multiple data sources, checks, and workflows. These platforms sit above individual KYC tools and providers, acting as a control layer that routes identity verification steps dynamically. KYC orchestration allows organizations to customize verification journeys based on customer risk, geography, and product type.

A primary driver of the KYC orchestration platform market is tightening global regulatory standards related to financial crime, identity verification, and customer risk management. Regulators require robust processes to verify customer identities, screen for sanctions lists, and monitor accounts for suspicious activity. Non-compliance can result in substantial fines, legal exposure, and reputational damage.

Orchestration platforms centralise and standardise these compliance activities, reducing risk and demonstrating governance readiness. Demand for KYC orchestration platforms is strongest among financial institutions, fintech companies, and digital platforms with high onboarding volumes. These organizations process thousands of customer verifications daily across multiple products.

Orchestration reduces duplication and operational bottlenecks. This efficiency drives sustained demand. Demand is also growing among enterprises expanding into new markets. Each region introduces different identity verification requirements. Orchestration platforms allow organizations to adapt workflows without rebuilding systems. This scalability supports international growth strategies.

Top Market Takeaways

- By component, software/platform accounts for 79.3% of the market, integrating multiple verification sources for seamless identity workflows and regulatory compliance.

- By deployment mode, cloud-based solutions represent 72.8%, enabling scalability, real-time processing, and easy integration across global operations.

- By organization size, large enterprises hold 76.5% share, requiring sophisticated orchestration to manage high-volume onboarding and risk assessment.

- By application, customer onboarding captures 52.4%, streamlining document checks, biometric verification, and sanctions screening for faster approvals.

- By end-user industry, banking commands 68.7%, adopting these platforms to meet AML/KYC mandates while enhancing digital customer experiences.

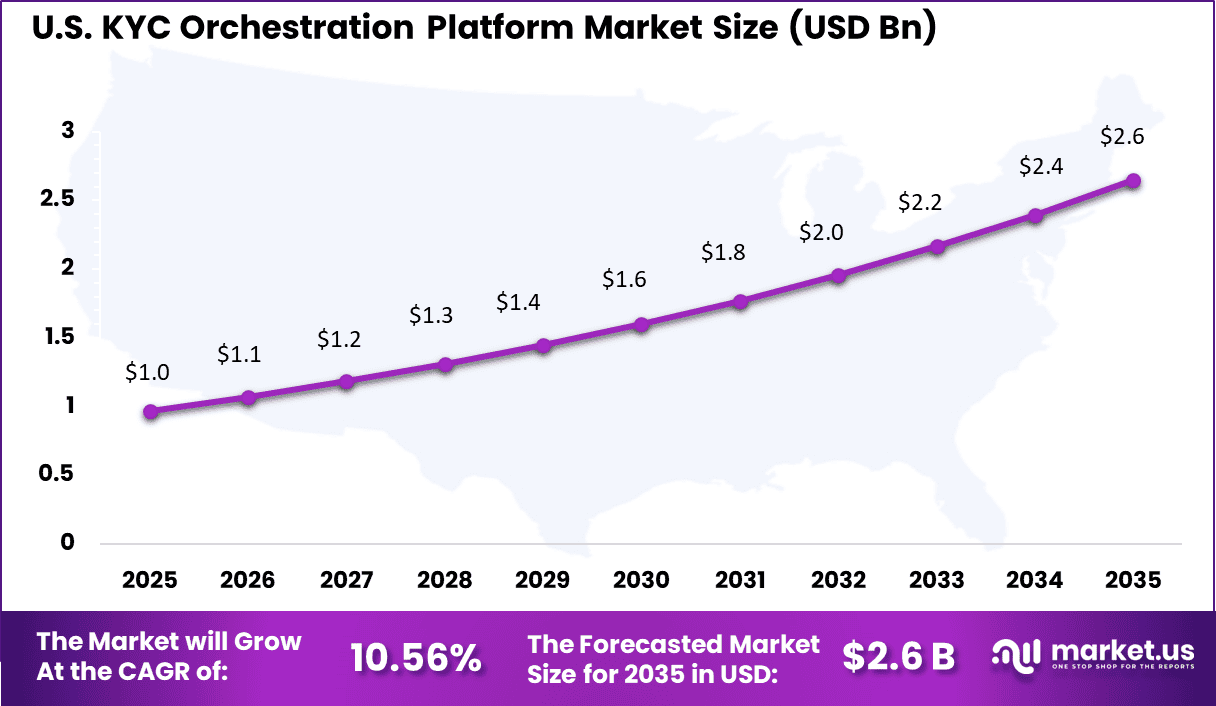

- By region, North America leads with 38.1% of the global market, where the U.S. is valued at USD 0.97 billion with a projected CAGR of 10.56%, fueled by stringent regulations and FinTech growth.

Key Insights

- More than 90% of B2B enterprises are expected to invest in identity verification software by 2034, reflecting growing concern over fraud and regulatory risk.

- In 2024, about 81% of US financial institutions adopted electronic KYC platforms, signaling strong digital onboarding momentum.

- Automated orchestration tools have reduced manual processing time by 60%, while some institutions lowered customer drop off rates from 25% to below 3% through faster onboarding.

- Organizations using automated KYC and AML systems report compliance cost reductions between 40% and 55%.

- AI driven verification platforms can lower risk analyst workload by up to 90% and achieve accuracy levels above 98%.

- Over the past decade, global fines related to KYC and AML failures reached USD 26 billion, underscoring the financial impact of non compliance.

- Jumio processes nearly 2 million verifications daily across 200 countries with 98% accuracy.

- Trulioo supports identity verification for 5 billion individuals and 300 million businesses worldwide.

- KYC Hub delivers verification in under 5 seconds and supports more than 10,000 ID document types.

- Alloy provides a codeless SDK for step up authentication and centralized reporting.

- Sumsub reports that 70% of fraud activity now occurs after the initial KYC stage, increasing demand for full cycle orchestration.

- Around 64% of US institutions have integrated biometric methods such as facial or fingerprint recognition into KYC workflows.

- Blockchain based identity systems have grown by 57%, reflecting interest in privacy enhancement and decentralized identity management.

- Nearly 70% of fintech firms rely on AI based verification software to enable instant and automated user validation.

Drivers Impact Analysis

Key Driver Impact on CAGR Forecast (~%) Geographic Relevance Impact Timeline Rising regulatory pressure on KYC, AML, and customer due diligence +3.9% North America, Europe Short to medium term Rapid growth of digital banking, fintech, and online onboarding +3.2% Global Medium term Increasing complexity of multi-vendor identity verification workflows +2.6% North America, Europe Medium term Demand for faster customer onboarding and lower drop-off rates +2.1% Global Short term Expansion of cross-border financial services and payments +1.7% Europe, Asia Pacific Medium to long term Restraint Analysis

Key Restraint Impact on CAGR Forecast (~%) Geographic Relevance Impact Timeline High implementation and integration costs for orchestration layers -2.7% Emerging Markets Short to medium term Data privacy and consent management challenges -2.3% Europe, North America Medium term Complexity in managing multiple verification vendors and rules -1.9% Global Medium term Limited awareness among small financial institutions -1.6% Asia Pacific, Latin America Medium term Long procurement cycles in regulated BFSI environments -1.3% North America, Europe Medium to long term By Component

Software and platform based solutions accounted for 79.3% of adoption, reflecting enterprise preference for centralized orchestration layers. These platforms manage identity checks, document verification, and risk scoring through configurable workflows. A single interface improves visibility across compliance operations. This reduces complexity for compliance teams.

Software platforms allow rapid integration of new verification services. Organizations can switch or add providers without redesigning processes. This flexibility supports regulatory changes and regional expansion. As compliance requirements evolve, software centric orchestration remains dominant.

Advanced analytics embedded within platforms further enhance value. Teams can monitor verification performance and bottlenecks. This improves process optimization and compliance outcomes. Software solutions continue to lead due to adaptability and scale.

By Deployment Mode

Cloud based deployment represented 73% of usage, driven by scalability and ease of integration. Cloud platforms support centralized orchestration across geographies and business units. Organizations benefit from faster deployment and reduced infrastructure management. This aligns with digital first compliance strategies. Cloud delivery enables real time updates to verification rules and workflows.

Compliance teams can respond quickly to regulatory changes. Centralized access also improves collaboration. These factors improve operational efficiency. Security standards in cloud environments have matured significantly. Encryption and access controls protect sensitive identity data. As a result, cloud based deployment has become widely accepted.

By Organization Size

Large enterprises accounted for 76.5% of adoption due to their high onboarding volumes and regulatory exposure. These organizations operate across multiple markets with varying compliance rules. Orchestration platforms help standardize processes while allowing local customization. This supports consistent compliance. Large enterprises also face higher costs from failed onboarding and fraud.

Automated orchestration reduces error rates and manual intervention. This improves efficiency and customer conversion. Investment capacity further supports adoption. Integration with existing compliance systems strengthens value. Large organizations embed orchestration platforms into broader risk frameworks. This reinforces their leading role in market adoption.

By Application

Customer onboarding accounted for 52.4% of usage, highlighting the importance of first touch compliance. Efficient onboarding is critical for customer acquisition and satisfaction. Orchestration platforms automate identity checks without excessive delays. This improves onboarding completion rates. Automated workflows reduce repetitive checks and rework.

Customers experience fewer interruptions during verification. This enhances trust and engagement. Onboarding remains the primary use case. As digital channels expand, onboarding volumes continue to rise. Orchestration platforms support scale without compromising compliance. This sustains strong adoption in this application area.

By End User Industry

Banking accounted for 68.7% of adoption due to strict regulatory requirements and high customer volumes. Banks must verify identity accurately while minimizing friction. KYC orchestration platforms support this balance. They improve compliance efficiency. Banks operate across multiple regulatory jurisdictions.

Orchestration platforms enable rule based routing based on location and risk. This reduces compliance gaps. Audit readiness is also improved. Digital banking growth has increased onboarding frequency. Automated orchestration helps manage this scale. Banking remains the dominant end user industry.

Emerging Trends Analysis

An emerging trend in the KYC orchestration platform market is the use of artificial intelligence for dynamic risk scoring and customer segmentation. AI models analyse multi-dimensional data including behavioural signals, transaction history, and device context to refine risk profiles. This enables more nuanced decisioning that adapts to evolving patterns. AI driven orchestration improves both compliance and customer experience.

Another trend is integration with digital identity wallets and decentralised identity frameworks. As self-sovereign identity and verifiable credentials gain traction, orchestration platforms are evolving to consume cryptographically secure identity attestations. This shift reduces reliance on document based checks and improves user privacy.

Growth Factors Analysis

One of the key growth factors for the KYC orchestration platform market is global expansion of digital financial services. Fintech adoption, cross-border payments, neobanks, and embedded finance solutions generate higher volumes of customer onboarding activity. Orchestration platforms support scale and compliance across these digital channels.

Another growth factor is rising regulatory scrutiny of financial crime and identity verification practices. Authorities increasingly expect real time monitoring, audit trails, and robust documentation. Orchestration solutions help organisations align operations with these expectations, reinforcing their role in compliance infrastructure.

Opportunity Analysis

A significant opportunity in the KYC orchestration platform market lies in modular and plug-and-play solutions that integrate with best-of-breed verification tools. Organisations want flexibility to choose identity verification vendors, screening data sources, and risk scoring engines that align with their risk profiles. Orchestration platforms that support modular integration and dynamic workflow design deliver higher value by enabling tailored compliance stacks.

Another opportunity is expansion into ongoing monitoring and lifecycle KYC. Rather than focusing solely on onboarding, orchestration platforms are evolving to support continuous identity verification, periodic refreshes, and risk-based alerts. This lifecycle approach improves long term compliance and reduces manual workloads associated with periodic reviews.

Challenge Analysis

A major challenge for the KYC orchestration platform market is ensuring data privacy and security while consolidating sensitive identity information. Orchestration systems process personal identifiers, document images, and risk scores across vendors. Protecting this data against breach, misuse, or unauthorised access is critical. Platforms must demonstrate strong encryption, access controls, and compliance with data protection regulations such as GDPR and CCPA.

Another challenge is balancing automation with human review. Fully automated workflows may speed processing but risk false positives or missed risk indicators. Organisations must design orchestration rules that escalate ambiguous cases to human analysts without creating bottlenecks. Effective rule design and continuous refinement are essential to optimise accuracy and efficiency.

Investor Type Impact Matrix

Investor Type Growth Sensitivity Risk Exposure Geographic Focus Investment Outlook KYC and compliance software providers Very High Medium North America, Europe Strong recurring SaaS revenue Fintech and digital banking platforms High Medium Global Strategic onboarding optimization Banks and financial institutions Medium Low to Medium Global Compliance-driven investment Private equity firms Medium Medium North America, Europe Platform consolidation opportunities Venture capital investors High High North America Innovation-led orchestration models Technology Enablement Analysis

Technology Enabler Impact on CAGR Forecast (~%) Primary Function Geographic Relevance Adoption Timeline API-based orchestration engines for KYC workflows +3.6% Vendor and rule coordination Global Short to medium term AI-driven decisioning and risk scoring +3.0% Faster and smarter approvals North America, Europe Medium term Modular integration with IDV, biometrics, and data providers +2.6% Flexible verification stacks Global Medium term Cloud-native compliance platforms +2.1% Scalability and cost efficiency Global Medium to long term Real-time monitoring and audit-ready reporting tools +1.8% Regulatory transparency Europe, North America Long term Key Market Segments

By Component

- Software/Platform

- Services

By Deployment Mode

- Cloud-based

- On-premises

By Organization Size

- Large Enterprises

- Small and Medium-sized Enterprises (SMEs)

By Application

- Customer Onboarding

- Ongoing Due Diligence & Monitoring

- Risk Assessment & Screening

- Case Management & Workflow Automation

- Others

By End-User Industry

- Banking

- Insurance

- FinTech & Crypto

- Other Financial Institutions

Regional Analysis

North America accounts for 38.1% of the KYC orchestration platform market, supported by strict regulatory expectations around customer due diligence and ongoing monitoring. Financial institutions in the region are adopting orchestration platforms to manage multiple identity verification, screening, and risk assessment workflows through a single control layer. Demand is driven by high onboarding volumes, frequent regulatory audits, and the need to improve compliance efficiency while maintaining customer experience.

The United States market is valued at USD 0.97 Bn and is growing at a CAGR of 10.56%, reflecting continued investment in scalable compliance infrastructure. Adoption is influenced by increasing complexity of KYC rules, rising digital account openings, and the need to reduce onboarding friction. Growth is further supported by wider use of automation and risk-based approaches that help institutions lower compliance costs and respond faster to regulatory changes.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Competitive Analysis

Risk intelligence and regulatory data providers such as Refinitiv, Moody’s Corporation, LexisNexis Risk Solutions, and Thomson Reuters Corporation play a central role in the KYC orchestration platform market. Their platforms aggregate watchlists, sanctions data, and adverse media. These capabilities enable centralized and automated onboarding workflows. Demand is driven by rising AML regulations and cross-border compliance complexity.

Digital identity verification providers such as Jumio Corporation, Trulioo Information Services, Inc., Onfido, Ltd., Mitek Systems, Inc., Acuant, Inc., IDology, Inc., and Shufti Pro, Ltd. strengthen customer due diligence processes. These vendors use biometric checks, document authentication, and liveness detection. Adoption is strong among fintech firms and digital banks seeking seamless onboarding.

Compliance workflow and transaction monitoring specialists such as ComplyAdvantage, Ltd., Exiger, LLC, NICE Actimize, Inc., and Fenergo, Ltd. provide orchestration and case management capabilities. Their platforms integrate multiple data sources into unified KYC frameworks. Other vendors expand innovation and regional reach, supporting steady growth of KYC orchestration solutions globally.

Top Key Players in the Market

- Refinitiv

- Moody’s Corporation

- LexisNexis Risk Solutions

- Thomson Reuters Corporation

- Jumio Corporation

- Trulioo Information Services, Inc.

- Onfido, Ltd.

- Mitek Systems, Inc.

- IDology, Inc.

- Acuant, Inc.

- Shufti Pro, Ltd.

- ComplyAdvantage, Ltd.

- Exiger, LLC

- NICE Actimize, Inc.

- Fenergo, Ltd.

- Others

Future Outlook

The future outlook for the KYC Orchestration Platform Market is strong as financial institutions seek more efficient ways to manage customer onboarding and compliance. Demand for KYC orchestration platforms is expected to rise because these systems help automate identity verification, reduce fraud risk, and ensure regulatory compliance.

Adoption of artificial intelligence, machine learning, and real-time data integration will improve accuracy and speed of customer checks. Growth can be attributed to stricter know-your-customer regulations, rising digital banking services, and the need to lower operational costs. Overall, the market is anticipated to expand as organizations prioritize secure, seamless, and compliant customer verification processes.

Recent Developments

- May, 2025 – Moody’s released guidance on perpetual KYC with AI‑driven monitoring, using entity data and automation to handle ongoing risk across client lifecycles while cutting false positives in orchestration platforms.

- March, 2025 – LSEG (owner of Refinitiv) acquired Global Data Consortium, a key digital ID verification data provider, to strengthen its KYC data and orchestration capabilities across global client onboarding workflows.

- January, 2025 – Jumio launched eKYC Checks as a new risk signal, validating name, address and DOB against independent sources in 50+ countries to meet EU AML/KYC rules and cut fraud in gaming and high‑risk payouts.

Report Scope

Report Features Description Market Value (2025) USD 2.8 Billion Forecast Revenue (2035) USD 9.6 Billion CAGR(2025-2035) 12.90% Base Year for Estimation 2024 Historic Period 2020-2024 Forecast Period 2025-2035 Report Coverage Revenue forecast, AI impact on Market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends Segments Covered By Component (Software/Platform, Services), By Deployment Mode (Cloud-based, On-premises), By Organization Size (Large Enterprises, Small and Medium-sized Enterprises (SMEs)), By Application (Customer Onboarding, Ongoing Due Diligence & Monitoring, Others), By End-User Industry (Banking, Insurance, FinTech & Crypto) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA Competitive Landscape Refinitiv, Moody’s Corporation, LexisNexis Risk Solutions, Thomson Reuters Corporation, Jumio Corporation, Trulioo Information Services, Inc., Onfido, Ltd., Mitek Systems, Inc., IDology, Inc., Acuant, Inc., Shufti Pro, Ltd., ComplyAdvantage, Ltd., Exiger, LLC, NICE Actimize, Inc., Fenergo, Ltd., Others Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  KYC Orchestration Platform MarketPublished date: Feb. 2026add_shopping_cartBuy Now get_appDownload Sample

KYC Orchestration Platform MarketPublished date: Feb. 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Refinitiv

- Moody's Corporation

- LexisNexis Risk Solutions

- Thomson Reuters Corporation

- Jumio Corporation

- Trulioo Information Services, Inc.

- Onfido, Ltd.

- Mitek Systems, Inc.

- IDology, Inc.

- Acuant, Inc.

- Shufti Pro, Ltd.

- ComplyAdvantage, Ltd.

- Exiger, LLC

- NICE Actimize, Inc.

- Fenergo, Ltd.

- Others

Our Clients

- 176906

- Feb. 2026