Global Keratin Hair Care Products Market Size, Share, Growth Analysis By Product (Shampoo, Conditioner, Hair Mask, Serum & Oil, Treatments, Others), By End Use (Individuals, Professionals), By Distribution Channel (Supermarkets & Hypermarkets, Specialty Beauty Stores, Pharmacies & Drugstores, Online, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Mar 2026

- Report ID: 181606

- Number of Pages: 312

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

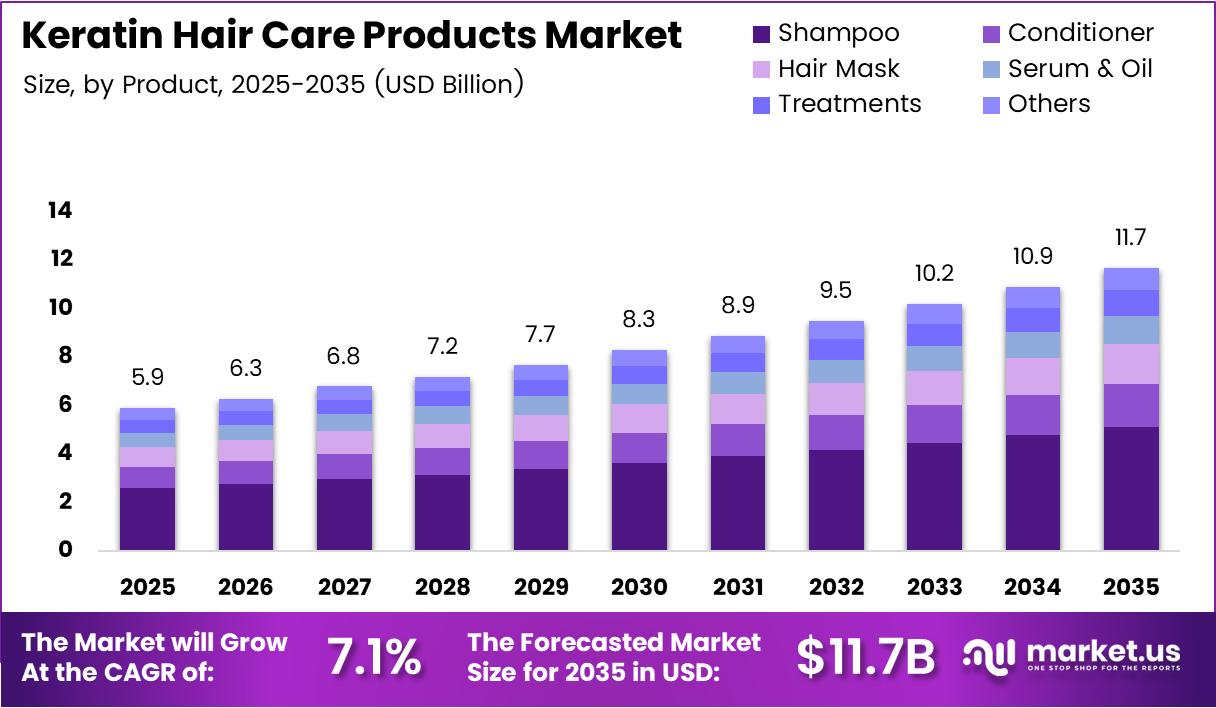

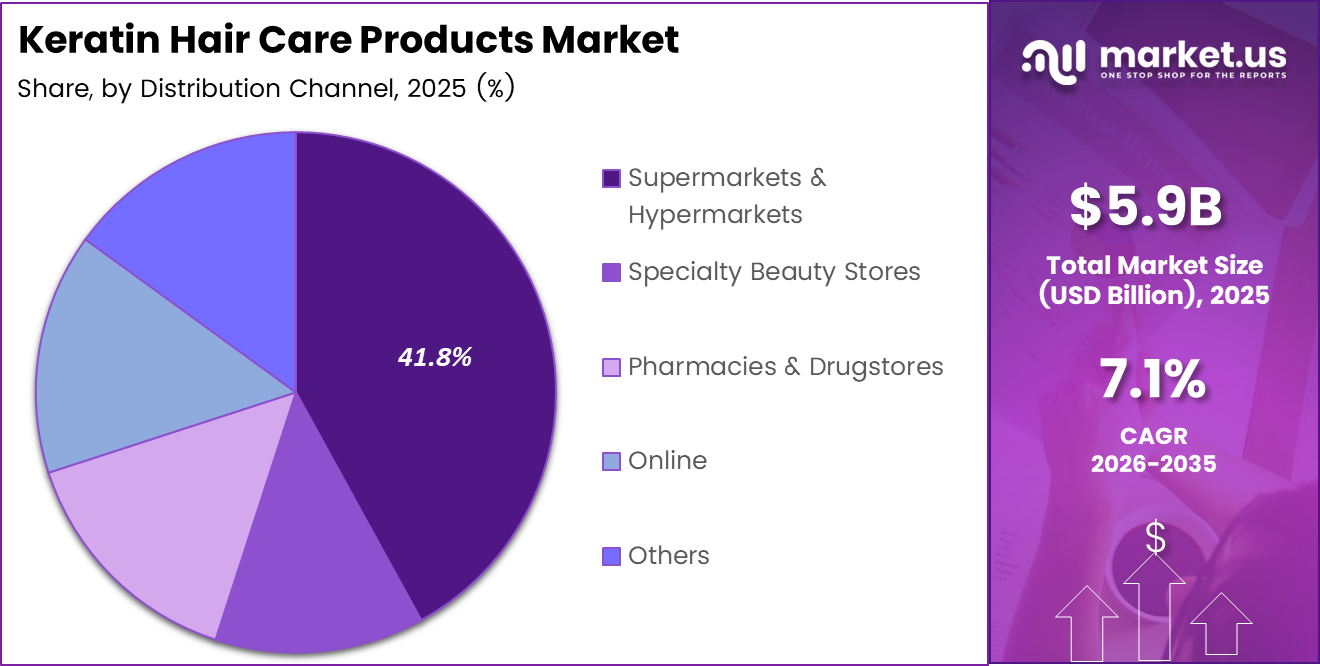

Global Keratin Hair Care Products Market size is expected to be worth around USD 11.7 Billion by 2035 from USD 5.9 Billion in 2025, growing at a CAGR of 7.1% during the forecast period 2026 to 2035.

The keratin hair care products market covers shampoos, conditioners, hair masks, serums, oils, and professional treatments formulated with keratin proteins to repair, strengthen, and smooth hair. These products address structural damage caused by heat styling, chemical processing, and environmental stress. The market spans both retail consumer products and professional salon-grade formulations.

Consumer behavior has shifted decisively toward damage-repair over cosmetic styling. Buyers no longer accept surface-level conditioning — they seek products that deliver measurable structural restoration. This shift elevates keratin from a premium ingredient to an expected standard across price tiers, compressing margins for generic players and rewarding those with clinical proof points.

Social media platforms have materially compressed the adoption cycle for keratin-based solutions. Treatment techniques once exclusive to salons now reach mass audiences through tutorial-driven content, converting passive interest into active purchase decisions. This compression benefits both professional brands expanding into retail and direct-to-consumer brands entering the professional channel.

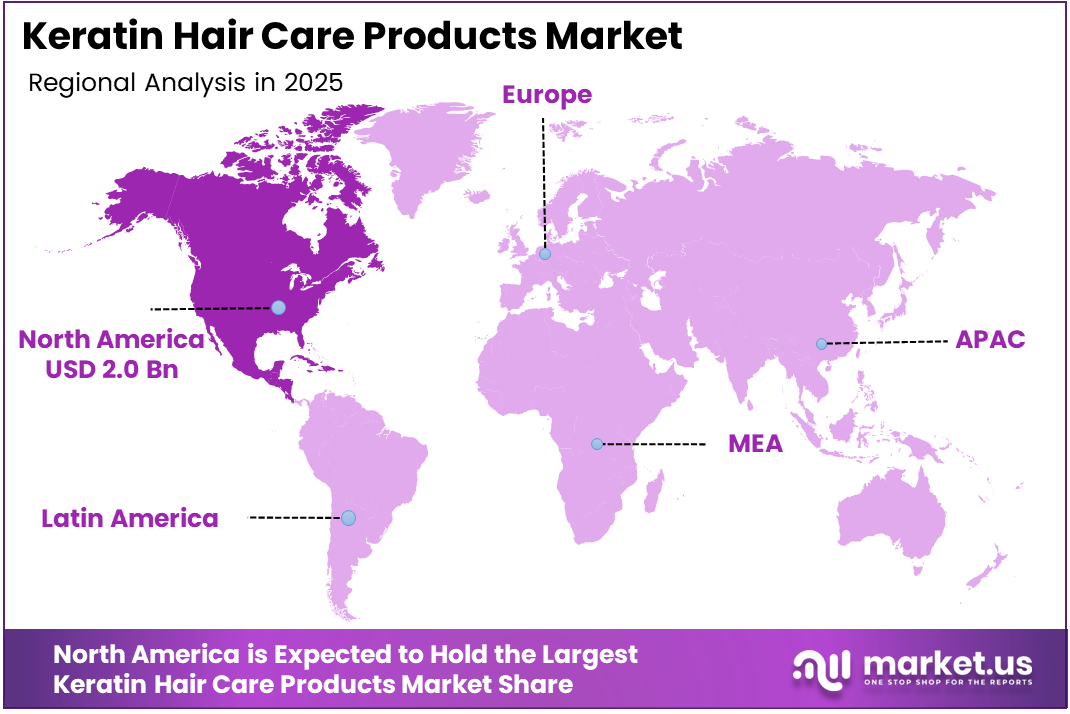

North America leads the market with a 34.70% share, valued at USD 2.0 Billion. This reflects early consumer willingness to pay a premium for clinically validated hair repair, combined with a mature salon infrastructure that accelerates professional product trial and retail conversion. These structural conditions are now replicating across Western Europe and urban Asia Pacific markets.

Formaldehyde concerns have created a product development imperative. Clean-label and formaldehyde-free keratin lines are no longer optional — they represent the compliance floor for brands seeking shelf space in regulated markets and for professional chains managing liability exposure. Brands without clean reformulations face growing distribution restrictions.

According to an academic research paper published in Cell Reports Physical Science (2025), KP::Resilin(1) peptide-keratin treatment preserves color strength above 94% after heat damage, compared to approximately 70% in untreated dyed hair. This 24-percentage-point gap quantifies the commercial case for peptide-enhanced keratin: color longevity directly reduces reservice frequency, making these formulations economically defensible at premium price points.

According to a manufacturer technical report by Croda (2025), KeraBio K31 biomimetic keratin ingredient delivers 100% stronger hair repair than the leading bond builder. This benchmark signals that next-generation biomimetic ingredients are pulling ahead of established bond-building chemistry — a shift that reorders the competitive hierarchy for prestige hair care formulation.

Key Takeaways

- The global Keratin Hair Care Products Market was valued at USD 5.9 Billion in 2025 and is forecast to reach USD 11.7 Billion by 2035.

- The market advances at a CAGR of 7.1% over the forecast period 2026 to 2035.

- By Product, Shampoo dominates with a 43.2% share in 2025.

- By End Use, Individuals hold the largest share at 72.5% in 2025.

- By Distribution Channel, Supermarkets and Hypermarkets lead with a 41.8% share in 2025.

- North America dominates regionally with a 34.70% share, valued at USD 2.0 Billion in 2025.

Product Analysis

Shampoo dominates with 43.2% due to daily-use frequency and mass retail reach.

In 2025, Shampoo held a dominant market position in the By Product segment of the Keratin Hair Care Products Market, with a 43.2% share. Daily usage patterns make shampoo the highest-volume entry point for keratin delivery, allowing brands to build consumer familiarity and repeat purchase loyalty at a lower price threshold than treatments or serums.

Conditioner functions as the logical cross-sell to keratin shampoo buyers. Consumers who adopt keratin shampoo typically add conditioner within the same purchase cycle, raising basket size without requiring a separate category persuasion. This behavioral linkage makes conditioner a reliable revenue multiplier for brands with strong shampoo shelf positions.

Hair Mask carries the highest per-unit value among rinse-off keratin formats. Masks target consumers seeking an intensified weekly treatment rather than daily maintenance, positioning them in the premium tier. Their higher active-ingredient concentration justifies elevated pricing and reinforces the damage-repair narrative that defines this market’s premium segment.

Serum and Oil formats address leave-in keratin delivery, appealing to consumers who style frequently and require continuous frizz control between wash cycles. These products extend keratin’s daily touchpoint beyond the shower, increasing brand exposure and reinforcing the perception of a complete hair care system rather than a single product solution.

Treatments represent the highest-commitment keratin format, encompassing both professional salon services and at-home treatment kits designed for structural correction of severely damaged hair. Their longer processing times and higher price points position them as a considered purchase, attracting consumers who have exhausted standard conditioning options and seek clinical-grade results.

Others within the product segment include styling products, primers, and protection sprays that incorporate keratin as a secondary functional ingredient. While individually small in volume, this grouping reflects the broadening application of keratin beyond core hair care into adjacent styling and finishing categories.

End-User Analysis

Individuals dominate with 72.5% due to mass retail accessibility and home-use convenience.

In 2025, Individuals held a dominant market position in the By End Use segment of the Keratin Hair Care Products Market, with a 72.5% share. The proliferation of salon-grade keratin formulations in retail formats has enabled home users to replicate professional results independently. This retail premiumization trend compresses the performance gap between home and salon treatments, sustaining volume at the individual buyer level.

Professionals — including salons, stylists, and trichology clinics — represent the higher-revenue-per-unit segment despite their smaller volume share. Professional buyers purchase in bulk, demand clinically supported performance claims, and act as credibility anchors for retail brands. A brand’s presence in professional channels directly elevates its perceived authority in the consumer segment, making professional adoption a strategic distribution priority.

Distribution Channel Analysis

Supermarkets and Hypermarkets dominate with 41.8% due to high footfall and broad brand availability.

In 2025, Supermarkets and Hypermarkets held a dominant market position in the By Distribution Channel segment of the Keratin Hair Care Products Market, with a 41.8% share. These outlets provide keratin hair care brands with maximum consumer reach, placing products alongside everyday shopping decisions rather than requiring a dedicated beauty trip. Mass retail shelf presence also drives impulse trial among consumers not actively seeking keratin-specific solutions.

Specialty Beauty Stores serve a higher-intent buyer who enters with a defined category need. These channels allow brands to present a full product range, support staff-assisted consultation, and stock professional-grade formulations that mass retail typically excludes. For premium keratin brands, specialty retail delivers higher conversion rates and a more receptive audience for technically complex product claims.

Pharmacies and Drugstores carry keratin hair care products within a health and personal care framework, attracting consumers who equate the channel with safety and clinical credibility. This positioning benefits formaldehyde-free and dermatologist-recommended lines, allowing brands to separate themselves from salon-chemical stigma and reach health-conscious buyers who might otherwise avoid traditional keratin treatments.

Online channels enable direct-to-consumer keratin brands to reach buyers who research ingredients actively and seek formulations unavailable in local retail. E-commerce also removes geographic distribution barriers, allowing specialist keratin brands — particularly those serving textured hair or offering customizable treatment kits — to build national and international sales without physical shelf investment.

Others in distribution include direct salon supply, subscription box services, and brand-owned boutiques. These channels collectively represent a smaller but strategically significant share, as they serve the most loyal and high-frequency buyers within the keratin category.

Key Market Segments

By Product

- Shampoo

- Conditioner

- Hair Mask

- Serum & Oil

- Treatments

- Others

By End Use

- Individuals

- Professionals

By Distribution Channel

- Supermarkets & Hypermarkets

- Specialty Beauty Stores

- Pharmacies & Drugstores

- Online

- Others

Drivers

Home-Use Demand and Social Media Influence Accelerate Adoption of Keratin Hair Repair Products

Consumers now expect salon-quality frizz control and hair smoothing at home, creating sustained volume demand for retail keratin formats. This behavioral shift has pushed mass-market and premium brands alike to reformulate with higher active concentrations — raising the performance bar across the entire product category and compressing the performance gap between at-home and professional treatments.

Social media beauty content has collapsed the traditional awareness-to-purchase funnel for keratin products. Platform-native tutorials demonstrate treatment results visually, converting passive viewers into active buyers at a speed traditional advertising cannot match. According to research published in Cell Reports Physical Science (2025), KP::Resilin(1) peptide-keratin treatment results in a 3.3% lower free thiol content in damaged hair versus untreated samples — a measurable structural outcome that brands can now communicate credibly in digital content, validating performance claims to an increasingly ingredient-literate consumer base.

Professional salon expansion in urban markets further reinforces retail demand. Consumers who receive salon keratin treatments actively seek maintenance products to extend results between appointments, creating a recurring retail revenue stream for brands with both professional and consumer product lines. In February 2024, Unilever completed the acquisition of K18, a premium biotech haircare brand whose K18Peptide molecule repairs hair damage at the molecular level — signaling that the largest FMCG players now view scientifically validated keratin technology as a core portfolio asset rather than a niche positioning.

Restraints

Formaldehyde Safety Concerns and High Product Costs Restrict Market Reach

Formaldehyde and its releasing agents, present in many professional keratin treatment formulations, have triggered regulatory scrutiny and consumer avoidance across multiple markets. Health agencies in North America and Europe have issued exposure warnings for salon environments, prompting professional chains to restrict or remove non-compliant formulations. This regulatory pressure directly limits the addressable market for traditional keratin treatment products.

Consumer safety awareness compounds the regulatory constraint. Social media channels that amplify keratin product benefits also circulate ingredient warnings, creating a split buyer response — interest in keratin outcomes alongside rejection of specific chemical processes. Brands that cannot demonstrate clean formulation credentials face a growing segment of buyers who will choose an inferior performing but safer alternative over a clinically superior but chemically complex product.

High product costs further narrow accessibility, particularly in price-sensitive markets across Asia Pacific, Latin America, and Africa. Professional keratin treatments can cost multiples of standard salon services, while premium at-home kits remain inaccessible to median-income consumers. This affordability gap concentrates keratin adoption in higher-income urban demographics, limiting volume potential and leaving a structurally large but currently underserved consumer base outside the market’s reach.

Growth Factors

Clean Formulations, Men’s Grooming Expansion, and Emerging Market Penetration Open New Revenue Channels

Formaldehyde-free and clean-label keratin product development addresses the compliance barrier directly, converting a restraint into a growth lever. Brands that reformulate with safer keratin delivery systems — such as hydrolyzed peptides and biomimetic ingredients — unlock distribution in regulated pharmacy and specialty channels previously inaccessible to conventional treatment products. According to a manufacturer technical report by Croda (2025), KeraBio K31 biomimetic keratin achieves full efficacy at just 0.05% active inclusion level and is 99% naturally derived under ISO 16128 standards — demonstrating that high-performance clean formulation is technically achievable and commercially viable at scale.

Men’s grooming presents an underutilized revenue opportunity within the keratin category. Male consumers increasingly engage with structured hair care routines, and keratin’s anti-frizz, smoothing, and strength benefits translate directly to male hair concerns. Brands that develop male-positioned keratin lines or extend existing formulations into gender-neutral packaging can capture incremental volume without requiring new manufacturing infrastructure.

Emerging markets with rising disposable income — particularly urban centers across Southeast Asia, the Middle East, and Latin America — represent the next geographic expansion wave for keratin products. Growing beauty awareness in these regions, combined with an expanding middle class and rising salon density, creates the conditions for volume adoption. Integration of keratin with natural and organic ingredients further strengthens appeal in markets where botanical claims resonate strongly with local consumer preferences.

Emerging Trends

Multi-Functional Formulations and Vegan Positioning Redefine Keratin Product Standards

At-home keratin treatment kits have transitioned from niche specialty products to mainstream retail fixtures. The DIY format addresses both the cost barrier of professional treatments and the convenience preference of time-pressured consumers. This shift forces professional brands to compete on formulation depth rather than channel exclusivity, reordering the competitive logic of the keratin category.

Vegan and cruelty-free keratin alternatives are no longer a fringe positioning — they reflect a structural shift in purchase criteria across multiple consumer segments. In February 2024, Cécred launched its foundational collection featuring the patent-pending Bioactive Keratin Ferment technology, derived from wool keratin, honey, and lactobacillus. This launch signals that even celebrity-backed brands now anchor their keratin credentials in biotechnology and clean sourcing, setting a new expectation for what a credible keratin product narrative requires.

According to a manufacturer technical blog by Keratin Complex (2025), the KCEXPRESS system completes two high-performance services — color and smoothing — in less time than a traditional single-process color service. This efficiency benchmark illustrates the broader trend toward multi-functional keratin formulations that combine hair repair with heat protection, color locking, and conditioning in a single step. Products that deliver compound benefits per application reduce treatment time and strengthen the consumer’s economic case for premium keratin solutions.

Regional Analysis

North America Dominates the Keratin Hair Care Products Market with a Market Share of 34.70%, Valued at USD 2.0 Billion

North America commands a 34.70% share of the global keratin hair care products market, valued at USD 2.0 Billion in 2025. Early consumer adoption of premium hair care, a dense professional salon network, and strong retail infrastructure across supermarkets and specialty beauty channels collectively sustain this lead. Regulatory pressure on formaldehyde has also accelerated clean-label reformulation, positioning North American brands as global compliance benchmarks.

Europe Keratin Hair Care Products Market Trends

Europe represents a mature and regulation-driven market where ingredient transparency requirements have shaped product development ahead of most other regions. The EU’s cosmetic safety framework has effectively mandated clean reformulation, creating a market where formaldehyde-free keratin products hold a structural advantage. Germany, France, and the UK anchor demand, supported by a professional salon culture that validates product performance for retail buyers.

Asia Pacific Keratin Hair Care Products Market Trends

Asia Pacific is the highest-potential volume market for keratin hair care, driven by a large urban consumer base, rising beauty expenditure, and a cultural emphasis on smooth, frizz-free hair particularly across Southeast Asia and East Asia. China, India, and South Korea lead adoption, with e-commerce platforms providing cost-effective distribution access for both domestic and international brands targeting ingredient-aware younger consumers.

Middle East and Africa Keratin Hair Care Products Market Trends

The Middle East and Africa market is shaped by high humidity climates that create persistent frizz and hair texture concerns, making keratin smoothing solutions functionally relevant rather than aspirational. Gulf Cooperation Council markets show the highest near-term commercial potential, supported by consumer willingness to pay for salon-quality results and a growing specialty beauty retail sector in key urban centers.

Latin America Keratin Hair Care Products Market Trends

Latin America, particularly Brazil, has historically been a foundational market for professional keratin treatments, given the region’s curl and wave hair texture profile and established salon treatment culture. Brazil’s domestic keratin treatment industry generates both local consumption and export product flows. Rising middle-class income and growing e-commerce penetration across Mexico and the broader region are extending retail keratin access beyond traditional salon delivery.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

L’Oréal S.A. commands the keratin hair care category through its multi-brand architecture, distributing keratin-infused formulations across mass, professional, and prestige tiers simultaneously. This tiered strategy allows L’Oréal to capture consumer spend at every price point while using its professional division as a product validation engine that elevates retail brand credibility across the full portfolio.

Unilever reinforced its keratin positioning materially in February 2024 through the acquisition of K18, a premium biotech haircare brand built on the K18Peptide molecule — a biomimetic compound that repairs hair damage at the molecular level. This acquisition signals Unilever’s strategic pivot from surface conditioning claims toward scientifically substantiated structural repair, repositioning the company in the premium keratin segment against specialist challengers.

Keratin Complex operates as a specialist professional brand with a direct pipeline between salon-validated formulations and retail extension. Its Express Color and Smoothing System, launched in September 2025, demonstrates a product development strategy focused on reducing service time without sacrificing results — a commercially critical differentiator for salons managing throughput under rising labor cost pressure.

Henkel AG & Co. KGaA leverages its dual presence in professional and consumer beauty to cross-deploy keratin innovation across both channels. Henkel’s scale in European and emerging markets provides distribution reach that specialist keratin brands cannot replicate independently, making it a structural beneficiary of formaldehyde-free reformulation trends that are reshaping shelf assortment across regulated markets.

Key Players

- L’Oréal S.A.

- Unilever

- Keratin Complex

- Henkel AG & Co. KGaA

- Cliove Organics

- Kerotin Hair Care

- GK Hair USA

- Gussi Hair LLC

- Nutree Cosmetics

- Novex Hair Care

Recent Developments

- September 2025 — Keratin Complex launched The Perfect Color Service, an Express Color and Smoothing System combining KeraLuminous10 10-minute permanent color powered by Signature Keratin and KC FASTLOCK technology with a 15-minute KCEXPRESS anti-frizz treatment, delivering color-locked, frizz-free results in less time than a traditional single-process color service.

- October 2025 — Croda released breakthrough performance data for its KeraBio K31 biomimetic keratin ingredient, demonstrating 100% stronger hair repair than the leading bond builder at just 0.05% active inclusion level, with the ingredient confirmed as 99% naturally derived under ISO 16128 standards, effectively resetting hair to a virgin profile.

- October 2025 — Joy Group completed the acquisition of Italian dermatological haircare brand Foltène, known for its proprietary complexes that promote keratin repair, healthy hair growth, and clinically proven thicker, fuller hair through anti-hair-loss ampoules and shampoos, expanding Joy Group’s position in clinically substantiated keratin-adjacent hair health solutions.

Report Scope

Report Features Description Market Value (2025) USD 5.9 Billion Forecast Revenue (2035) USD 11.7 Billion CAGR (2026-2035) 7.1% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product (Shampoo, Conditioner, Hair Mask, Serum & Oil, Treatments, Others), By End Use (Individuals, Professionals), By Distribution Channel (Supermarkets & Hypermarkets, Specialty Beauty Stores, Pharmacies & Drugstores, Online, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape L’Oréal S.A., Unilever, Keratin Complex, Henkel AG & Co. KGaA, Cliove Organics, Kerotin Hair Care, GK Hair USA, Gussi Hair LLC, Nutree Cosmetics, Novex Hair Care Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Keratin Hair Care Products MarketPublished date: Mar 2026add_shopping_cartBuy Now get_appDownload Sample

Keratin Hair Care Products MarketPublished date: Mar 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- L'Oréal S.A.

- Unilever

- Keratin Complex

- Henkel AG & Co. KGaA

- Cliove Organics

- Kerotin Hair Care

- GK Hair USA

- Gussi Hair LLC

- Nutree Cosmetics

- Novex Hair Care

Our Clients

- 181606

- Mar 2026