Global K-Beauty Products Market Size, Share, Growth Analysis By Product (Skin Care, Hair Care, Makeup, Others), By End-User (Women, Men), By Distribution Channel (Supermarkets & Hypermarkets, Mass Merchandiser, Specialty Retailer, Convenience Stores, Online, Pharmacy & Drug Stores, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Feb 2026

- Report ID: 178398

- Number of Pages: 272

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

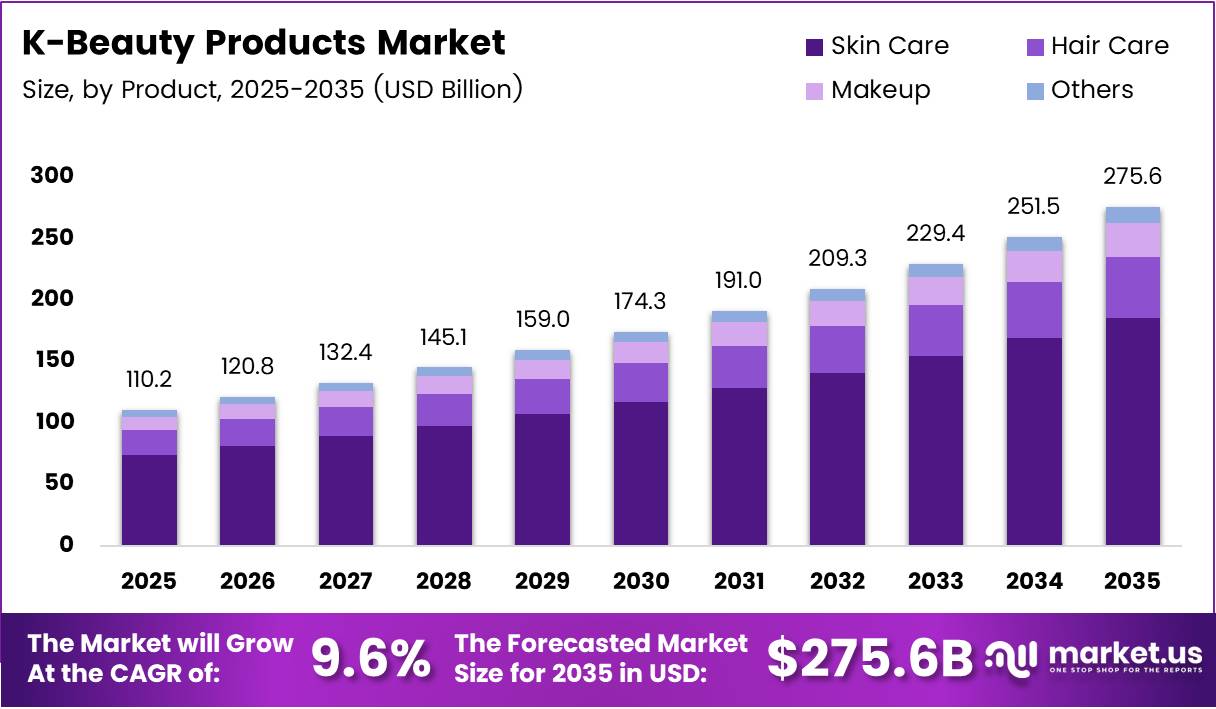

Global K-Beauty Products Market size is expected to be worth around USD 275.6 Billion by 2035 from USD 110.2 Billion in 2025, growing at a CAGR of 9.6% during the forecast period 2026 to 2035.

The K-beauty products market encompasses Korean-origin cosmetics and personal care items — spanning skincare, haircare, color cosmetics, and functional beauty solutions. These products distinguish themselves through ingredient-forward formulations, multi-step routines, and technology-backed claims. The category has moved from niche import status to mainstream shelf placement in global retail chains across North America, Europe, and Asia Pacific.

What drives the market’s structural durability is not just consumer preference but export infrastructure. South Korea has built a cosmetics manufacturing and export ecosystem that now competes directly with France and the United States in global export rankings. This scale creates pricing power, supply chain depth, and innovation velocity that smaller regional competitors cannot easily match.

Government alignment amplifies commercial momentum. In November 2025, the Korean government announced programs specifically designed to help domestic cosmetics firms expand into global retail networks and overseas online channels — a direct policy intervention that lowers market entry barriers for Korean brands targeting new geographies.

The premium skincare segment acts as the profit engine for leading Korean beauty groups. Operating margins expand when premium and derma-category products drive a larger share of the revenue mix. This margin dynamic creates an incentive for brands to invest in clinical positioning, which in turn raises the category’s credibility among Western consumers who previously associated Korean beauty primarily with affordability.

Cross-border e-commerce is the distribution lever that unlocks emerging markets fastest. Digital platforms remove the need for physical retail infrastructure, allowing Korean brands to test and scale in new geographies before committing to brick-and-mortar investment. This asymmetry between distribution cost and market reach explains why K-beauty has penetrated markets across Africa, Eastern Europe, and Latin America faster than most legacy cosmetics categories.

According to Korea JoongAng Daily, South Korean cosmetics exports reached US$10.28 billion in 2024, up 20.6% year-over-year. This export scale confirms that global buyer adoption is broad-based, not confined to one region — a structural signal that the market’s growth trajectory rests on diversified demand rather than single-market concentration risk.

According to Korea JoongAng Daily, total cosmetics exports surpassed US$11.43 billion in 2025, up 12.3% year-over-year, with skincare alone accounting for approximately US$8.54 billion — roughly 75% of total exports. Skincare’s dominance within the export basket signals that prestige and functional skincare, not color cosmetics, remain the primary demand driver for international buyers purchasing Korean beauty products.

Key Takeaways

- The global K-Beauty Products Market was valued at USD 110.2 Billion in 2025 and is forecast to reach USD 275.6 Billion by 2035.

- The market advances at a CAGR of 9.6% during the forecast period 2026 to 2035.

- By Product, Skin Care leads with a 67.3% share, reflecting global prioritization of skincare routines.

- By End-User, Women account for 67.9% of market demand, though the Men’s segment is adding share.

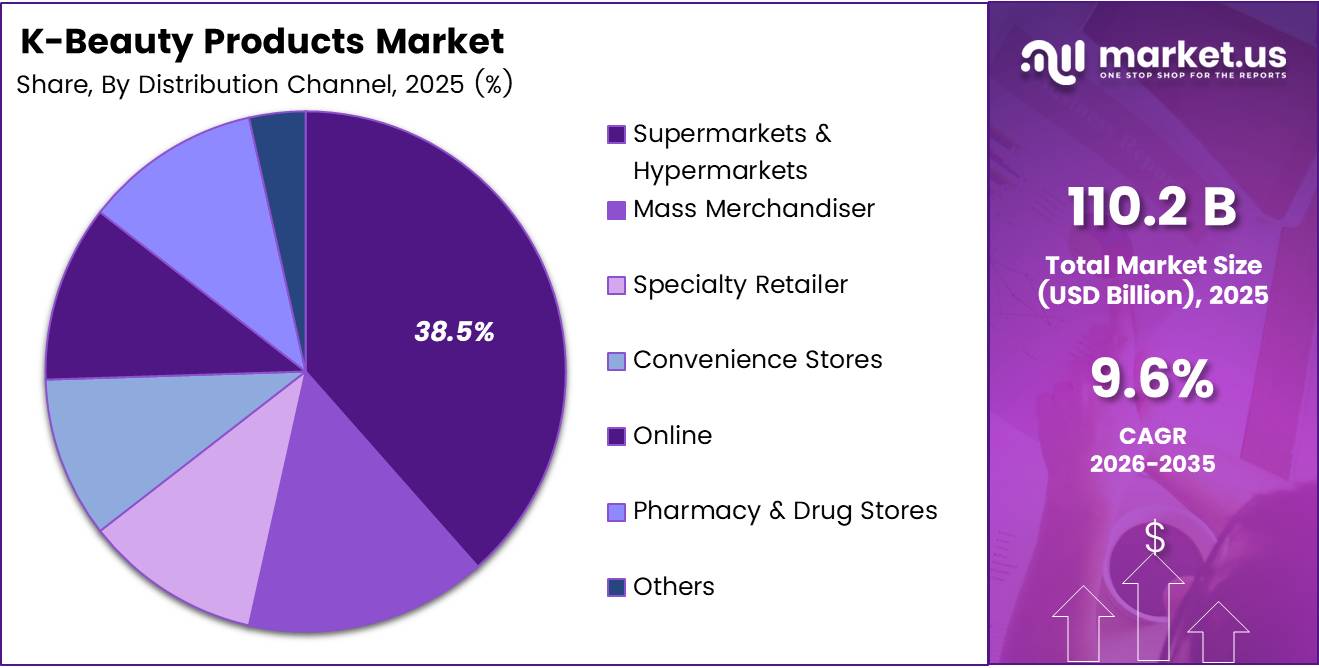

- By Distribution Channel, Supermarkets and Hypermarkets hold a 38.5% share as the dominant retail format.

- North America dominates regionally with a 39.70% share, valued at USD 43.7 Billion.

- In 2025, South Korea exported cosmetics to 202 countries, up from 172 the prior year, per Korea JoongAng Daily.

- K-beauty M&A activity exceeded KRW 3 trillion in 2025, with 21 deals completed January through October.

Product Analysis

Skin Care dominates with 67.3% due to routine-driven repeat purchase behavior.

In 2025, Skin Care held a dominant market position in the By Product segment of the K-Beauty Products Market, with a 67.3% share. According to asiae.co.kr, basic skincare production in South Korea reached ₩10.3 trillion, representing 58.7% of total cosmetics production. This production scale confirms that skincare is not just a consumer preference — it is the manufacturing backbone of the entire K-beauty export system.

Cleanser serves as the entry point for consumers adopting K-beauty routines. Most multi-step Korean skincare regimens begin with a double-cleanse protocol — oil-based followed by water-based formulas. This sequential logic drives repeated unit purchases and builds category loyalty faster than single-product cosmetics segments typically achieve.

Moisturizer carries consistent volume across all consumer demographics. Korean moisturizer formats — including gel creams, sleeping packs, and emulsions — offer differentiated textures that Western equivalents rarely replicate at comparable price points. This format diversity sustains shelf space in both mass and premium retail channels simultaneously.

Serum differentiates through active ingredient concentration and clinical positioning. Serum SKUs command the highest average selling prices within the skincare segment. Amorepacific’s September 2025 global expansion strategy, which explicitly targeted bio-beauty and premium skincare, reflects how serum-led product development underpins margin expansion for leading Korean beauty groups.

Sunscreen benefits from consumer awareness of UV protection as a non-negotiable daily step. Korean sun protection formats — including essence sunscreens and tinted SPF products — introduced texture innovations that reshaped buyer expectations in Western markets. This category captures both functional and cosmetic positioning, widening its addressable buyer base.

Others within skincare include toners, essences, exfoliators, and eye creams. These products occupy the mid-funnel of the Korean skincare routine and generate consistent repurchase cycles. Their presence signals that the K-beauty skincare segment sells systems, not single products — a structural advantage over single-SKU beauty brands.

Hair Care carries the highest growth potential within the non-skincare product segments. Korean haircare innovations — including scalp-focused treatments and fermented ingredient formulas — address gaps that mass-market Western haircare brands leave unmet. This positions Korean haircare as a premiumization vehicle for buyers already loyal to K-beauty skincare.

Shampoo represents the volume anchor of the haircare sub-segment. Scalp health positioning differentiates Korean shampoo from conventional cleansing formulas. Buyers who enter the K-beauty haircare category through shampoo typically migrate toward higher-margin conditioning and serum products over time, building the category’s lifetime value per customer.

Conditioner extends the scalp and strand health narrative established by shampoo. Korean conditioners frequently incorporate fermented ingredients, botanical actives, and heat-protection claims that justify premium pricing relative to global mass-market equivalents. This allows Korean brands to maintain margin even at competitive retail price points.

Serums within haircare mirror the skincare serum model — high active concentration, clinical claims, and premium positioning. Hair serum adoption among K-beauty buyers reflects a category maturation pattern where consumers transfer their skincare ingredient literacy into haircare purchasing decisions.

Others in haircare encompass scalp treatments, hair masks, and leave-in formulas. These products address specific hair concerns that standard shampoo and conditioner cannot fully resolve, creating an upsell layer within Korean haircare retail assortments. Their growing international presence signals that Korean haircare is moving beyond basic cleansing into therapeutic territory.

Makeup records structurally lower share than skincare but benefits from accelerating category innovation. Color cosmetics production in South Korea reached ₩2.68 trillion in 2024, up 51.4% year-over-year, signaling that Korean makeup manufacturing is scaling at a pace that will support international distribution expansion over the forecast period.

Base Makeup in the K-beauty segment spans cushion compacts, BB creams, and skin-tint formulas. These formats effectively merged skincare benefits with coverage, creating a hybrid product category that Korean brands pioneered globally. Base makeup retains high brand differentiation because format innovation — not just formula — drives purchase decisions.

Eye Makeup benefits from Korean beauty’s influence on global eyeliner and mascara aesthetics. The “straight brow” and “puppy eye” looks disseminated through K-content have directly translated into eye product sales outside South Korea. Cultural content remains the strongest unpaid distribution channel for Korean eye makeup products.

Lip Products record the fastest export growth within the makeup sub-segment. Lipstick exports grew 42.9% year-over-year in 2025, confirming that Korean lip formulations — including gradient tints and glass-finish glosses — address a global consumer preference not fully satisfied by Western lip product formats.

Others in makeup includes setting sprays, blushes, and highlighters. These products function as basket-builders in retail and e-commerce environments. Their inclusion in K-beauty assortments broadens the category’s appeal beyond skincare-first buyers, drawing color cosmetics consumers deeper into the Korean beauty ecosystem.

End-User Analysis

Women dominate with 67.9% due to skincare routine adoption and repeat purchase frequency.

In 2025, Women held a dominant market position in the By End-User segment of the K-Beauty Products Market, with a 67.9% share. Women’s consumption concentrates in skincare routines, where multi-step regimens generate four to six product purchases per cycle. This basket depth explains the segment’s outsized revenue share relative to the broader beauty market.

Men represent the fastest-shifting end-user segment within K-beauty. Korean skincare culture has normalized grooming routines for men more effectively than most Western markets, creating a replicable blueprint for global expansion. Male buyers enter the category through BB creams, toners, and sunscreens — products with low barrier-to-entry and clear functional benefits.

Distribution Channel Analysis

Supermarkets and Hypermarkets dominate with 38.5% due to mass accessibility and impulse purchase behavior.

In 2025, Supermarkets and Hypermarkets held a dominant market position in the By Distribution Channel segment of the K-Beauty Products Market, with a 38.5% share. Large-format retail provides K-beauty brands with high-footfall environments where product discovery converts efficiently to trial purchase. This channel’s dominance reflects the category’s successful transition from specialty import to mainstream consumer goods.

Mass Merchandiser channels extend K-beauty’s reach into value-conscious consumer segments. These retailers carry curated K-beauty assortments at accessible price points, introducing the category to buyers who would not seek out specialty beauty retailers. Mass merchandiser placement signals that Korean beauty has achieved sufficient brand recognition to compete on generalist shelves.

Specialty Retailer channels carry the highest average transaction value within K-beauty distribution. Dedicated beauty retailers provide the depth of assortment — multiple brands, extensive SKUs, and in-store education — that converts category-curious buyers into multi-product routine adopters. Specialty placement builds brand equity that supports premium pricing across other channels.

Convenience Stores serve as high-frequency repeat purchase points for consumable K-beauty products. In markets where Korean convenience retail culture has exported alongside beauty products — particularly across Southeast Asia — this channel builds brand touchpoints without requiring significant retailer investment. However, limited shelf space restricts SKU depth and brand storytelling.

Online channels enable K-beauty’s fastest international geographic penetration. Digital platforms remove physical shelf constraints and allow smaller Korean brands to reach global consumers without distributor partnerships. Amorepacific’s September 2025 long-term expansion strategy specifically prioritized digital channel expansion alongside AI transformation, confirming that online is a strategic priority — not just a secondary channel — for major Korean beauty groups.

Pharmacy and Drug Stores reinforce K-beauty’s clinical and derma positioning. Placement alongside pharmaceutical skincare products signals ingredient efficacy to buyers who prioritize function over aesthetics. This channel matters most for functional skincare and derma-category products, where clinical association translates directly into price premium acceptance.

Others in distribution include duty-free retail, direct sales, and pop-up formats. Duty-free channels remain significant for Korean beauty brands given South Korea’s position as a major global travel hub. These channels provide high-margin, impulse-driven purchases from international travelers who discover K-beauty before seeking it through home-market channels.

Key Market Segments

By Product

- Skin Care

- Cleanser

- Moisturizer

- Serum

- Sunscreen

- Others

- Hair Care

- Shampoo

- Conditioner

- Serums

- Others

- Makeup

- Base Makeup

- Eye Makeup

- Lip Products

- Others

- Others

By End-User

- Women

- Men

By Distribution Channel

- Supermarkets & Hypermarkets

- Mass Merchandiser

- Specialty Retailer

- Convenience Stores

- Online

- Pharmacy & Drug Stores

- Others

Drivers

Accelerating Export Scale Builds Global Retail Presence for Korean Beauty Brands

Korean cosmetics exports reached $5.51 billion in January through June 2025, up 14.8% year-over-year, covering 176 countries in that period alone. This export breadth means Korean beauty brands now hold shelf space across geographies that most Western beauty incumbents entered over decades. The volume creates distribution leverage that individual brand-level marketing cannot replicate.

The U.S. market illustrates the compounding effect of export scale. U.S. cosmetics imports from South Korea doubled over four years, confirming sustained buyer commitment rather than short-cycle trend adoption. Moreover, Poland emerged as a high-velocity new market — growing from $3 million in 2023 to $150 million in H1 2025 alone — signaling that Eastern European markets are entering an active adoption phase for Korean beauty products.

For investors and brand operators, export diversification across 176-plus countries reduces single-market revenue risk. In October 2025, Kolmar Korea was selected to lead a government AI Factory project to build autonomous AI-driven cosmetics manufacturing systems, running 2025 through 2029. This state-backed manufacturing investment ensures supply chain scalability keeps pace with export demand expansion, protecting Korean brands’ ability to fulfill global orders at competitive cost.

Premium Skincare Profitability Signals a Structural Shift in K-Beauty Margin Architecture

Amorepacific reported FY2025 consolidated revenue of KRW 4.6232 trillion, with operating profit reaching KRW 368 billion — a 47.6% year-over-year increase. This profit recovery, driven by global premium skincare and derma categories, confirms that Korean beauty’s value proposition has shifted from price competitiveness to ingredient authority. Brands able to sustain premium positioning will capture disproportionate margin.

Premium skincare’s profitability advantage stems from ingredient differentiation and clinical positioning. Korean brands have developed proprietary actives — fermented extracts, biotechnology-derived compounds, and patented delivery systems — that justify higher retail prices in Western markets. Consequently, premium skincare commands a price premium that offsets Korea’s relatively higher manufacturing labor costs compared to Southeast Asian alternatives.

The margin expansion dynamic creates a self-reinforcing investment cycle. Higher operating profits fund R&D into next-generation ingredient platforms, which support future premium launches. Therefore, the Korean beauty brands currently investing in derma and bio-beauty categories are building moats that will be difficult for commodity-positioned competitors to breach over the forecast horizon.

Restraints

China Market Revenue Decline Exposes Concentration Risk in K-Beauty’s Largest Historical Export Destination

China’s export value declined by $130 million year-over-year in H1 2025, reducing its share of Korean cosmetics exports to approximately 10%. This contraction reflects a combination of Chinese consumer nationalism, domestic brand competition, and slowing premium beauty spending in China’s urban markets. For Korean brands historically dependent on China as the primary overseas revenue source, this creates a structural revenue gap requiring active reallocation.

The China slowdown compresses the revenue base precisely when Korean beauty companies are investing in global expansion. Operating cost structures built around China-volume economics — including logistics, warehousing, and trade marketing — become inefficient as China revenue shrinks. This creates a transitional margin squeeze that affects mid-sized Korean brands more severely than large groups with already-diversified geographic revenue bases.

However, the China deceleration is accelerating strategic reorientation. Korean brands are redirecting sales resources toward the U.S., Japan, Southeast Asia, and emerging markets in Eastern Europe and the Middle East. This reallocation involves new retail partnerships, localized marketing investment, and adapted product assortments — costs that weigh on near-term profitability even as they build long-run revenue resilience.

Growth Factors

Derma and Medical Skincare Globalization Creates a High-Margin Expansion Lane Beyond Conventional K-Beauty

Overseas revenue for leading Korean beauty brands grew 15% year-over-year in 2025, with derma product expansion identified as a primary contributor. The derma category — functional, clinically validated skincare positioned at pharmacy and specialty retail channels — carries a higher average selling price and lower promotional spend than mass-market Korean beauty. This margin profile makes derma globalization among the most capital-efficient expansion strategies available to Korean beauty groups.

EMEA revenue expanded 42% year-over-year in 2025 via new retail touchpoints and digital channel development. Europe’s regulatory framework for cosmetic claims, while demanding, creates a quality signal that Korean derma brands can leverage. European consumers already familiar with dermatologist-recommended brands from French and German cosmeceutical players represent a ready audience for Korean clinical skincare positioned at comparable or lower price points.

Americas regional revenue grew 20% year-over-year in 2025, supported by premium lip and skincare demand. The beauty device and cosmetics revenue at major Korean beauty-tech players grew triple digits year-over-year in 2025, confirming that the next growth frontier combines physical product with technology-enhanced application experiences. Brands that integrate devices with consumable refill products extend customer lifetime value and build switching costs unavailable to conventional cosmetics competitors.

Emerging Trends

Sheet Mask and Lip Product Export Acceleration Signals Format-Led Global Demand for Korean Beauty Rituals

Lipstick exports grew 42.9% year-over-year and sheet mask exports grew 33.4% year-over-year in 2025. These growth rates confirm that format innovation — not just ingredient differentiation — drives global buyer preference for Korean beauty. Sheet masks translate complex skincare routines into a single-use ritual that requires no expertise, reducing adoption friction for new-to-K-beauty consumers globally.

The cultural export flywheel compounds format-driven adoption. The Korean government attributed record export growth to global K-content popularity — films, music, and streaming series — boosting cosmetics adoption internationally. This content-to-commerce connection means that Korean beauty brands benefit from media distribution that no competitor can buy, because it is embedded in cultural entertainment rather than paid advertising.

Some leading K-beauty players generated 78% of total sales from overseas markets in 2025. This international revenue dominance reshapes how Korean beauty companies structure their organizations — prioritizing global supply chains, multilingual digital platforms, and region-specific product adaptation over domestic market defense. Early movers who build international infrastructure now will hold distribution advantages when the next cohort of markets enters active K-beauty adoption.

Regional Analysis

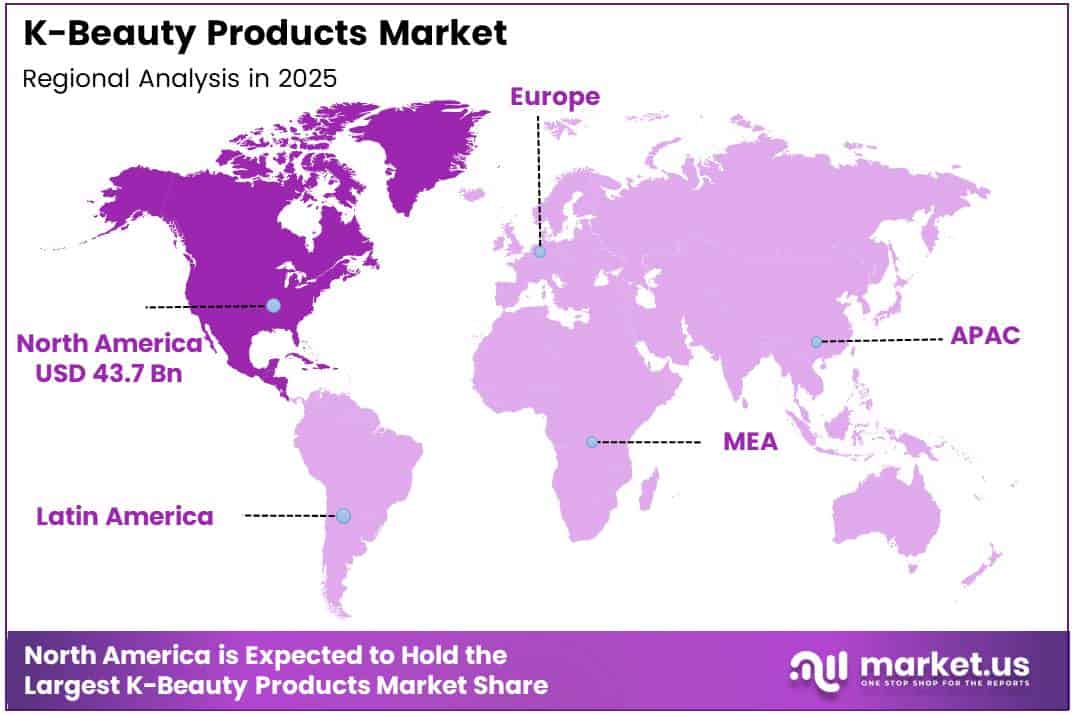

North America Dominates the K-Beauty Products Market with a Market Share of 39.70%, Valued at USD 43.7 Billion

North America leads the K-Beauty Products Market with a 39.70% share, valued at USD 43.7 billion. This dominance reflects mature retail infrastructure, high per-capita beauty spending, and an early-adopter consumer base that validated K-beauty’s premium positioning in the U.S. market. Americas regional revenue grew 20% year-over-year in 2025, confirming that North American demand is not plateauing but accelerating into broader demographic and channel penetration.

Europe K-Beauty Products Market Trends

Europe represents the market’s fastest-scaling Western geography. EMEA revenue for leading Korean beauty exporters expanded 42% year-over-year in 2025, driven by new retail channel entry and digital commerce investment. Poland’s emergence — growing from $3 million to $150 million in K-beauty imports within roughly eighteen months — illustrates Eastern Europe’s compressed adoption curve and signals that European market penetration extends well beyond traditional Western fashion capitals.

Asia Pacific K-Beauty Products Market Trends

Asia Pacific combines South Korea’s domestic production base with the region’s largest consumer markets. Japan received US$1.1 billion in Korean cosmetics exports in 2025, reflecting sustained demand despite longstanding competitive tension between Japanese and Korean beauty brands. China, at US$2.0 billion in 2025 exports, remains significant in volume terms despite the year-over-year revenue decline — indicating that Chinese consumer demand persists even as Korean brands diversify away from China dependence.

Latin America K-Beauty Products Market Trends

Latin America is an emerging adoption market for Korean beauty products, with cross-border e-commerce serving as the primary entry channel. Korea’s export data confirms coverage now spans well beyond traditional distributor-served markets, reaching Brazil, Mexico, and smaller regional markets through digital platforms. However, physical retail infrastructure remains underdeveloped relative to North America and Europe, meaning online channels will define Korean beauty’s Latin American market structure for the near term.

Middle East and Africa K-Beauty Products Market Trends

The Middle East and Africa region benefits from Korean beauty’s ingredient-first positioning, which aligns with premium beauty preferences among Gulf Cooperation Council consumers. South Korea’s export reach expanding to over 202 countries in 2025 implicitly includes GCC and African market access. Halal certification compatibility and heat-resistant formulation development will determine how quickly Korean beauty brands convert regional product awareness into sustained retail revenue.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

AMOREPACIFIC holds the strongest global premium positioning among Korean beauty groups. Its FY2025 consolidated revenue of KRW 4.6232 trillion and operating profit of KRW 368 billion — up 47.6% year-over-year — reflect a deliberate pivot toward global premium skincare and derma categories. Its September 2025 announcement of a long-term strategy encompassing bio-beauty, AI transformation, and beauty devices signals that Amorepacific is building a diversified technology-led portfolio rather than defending a pure cosmetics position.

LG HOUSEHOLD & HEALTH CARE LTD. operates with scale advantages that smaller Korean beauty players cannot replicate. Its FY2024 consolidated revenue of KRW 7.9 trillion and beauty segment revenue of KRW 2.8 trillion position it as the largest Korean beauty conglomerate by consolidated turnover. Overseas beauty and cosmetics sales reached KRW 2,048 billion in 2024, representing 30.9% of total revenue — a share that signals genuine international business weight rather than marginal export dependency.

BANILLA CO competes through focused product positioning in high-visibility K-beauty categories including cleansing balms and color cosmetics. The brand’s strength lies in cult-product status for specific SKUs that generate disproportionate brand awareness relative to overall revenue scale. This concentrated product authority allows BANILLA CO to punch above its weight in international specialty retail and online channels where hero-product discoverability drives conversion.

Clio occupies a differentiated position as a Korean beauty brand with proven color cosmetics competence alongside skincare. This dual-category presence gives Clio flexibility in international retail assortments where buyers seek complete routine solutions from a single brand. Clio’s distribution in both specialty beauty retailers and online platforms provides resilience against single-channel concentration risk while building brand recognition across multiple consumer touchpoints.

Key Players

- BANILLA CO

- AMOREPACIFIC

- The Crème Shop

- Clio

- Able C&C

- The Face Shop, Inc.

- TolyMoly

- LG HOUSEHOLD & HEALTH CARE LTD.

Recent Developments

- September 2025 — KKR acquired Korean cosmetics container manufacturer Samhwa Co. for KRW 733 billion (approximately $526.6 million), marking one of the largest private equity transactions in the K-beauty packaging supply chain. This deal reflects growing investor conviction in the structural growth of Korean cosmetics manufacturing infrastructure beyond finished goods.

- September 2025 — Blackstone reportedly agreed to invest in Korean haircare company JUNO, with financial terms undisclosed. This investment signals that global private equity firms are extending their K-beauty value chain interest from skincare into haircare, a category where Korean brands are building international presence.

- December 2024 — L’Oréal agreed to acquire South Korean skincare brand Dr.G via Gowoonsesang Cosmetics from Migros, aiming to strengthen its global K-beauty portfolio. This acquisition confirms that multinational beauty conglomerates view Korean derma-skincare brands as strategic acquisitions rather than competitive threats.

- June 2025 — Kolmar Korea partnered with Tmall Global to support Korean beauty brands expanding into China via cross-border e-commerce. This partnership creates a structured digital entry point for Korean brands targeting Chinese consumers despite the broader China market revenue softness in physical retail channels.

- January–October 2025 — K-beauty M&A activity exceeded KRW 3 trillion, with 21 deals completed — up approximately 26.9% year-over-year. This consolidation pace across the value chain signals that the K-beauty sector is entering a maturation phase where scale and strategic fit replace organic growth as the primary value creation mechanism.

Report Scope

Report Features Description Market Value (2025) USD 110.2 Billion Forecast Revenue (2035) USD 275.6 Billion CAGR (2026-2035) 9.6% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product (Skin Care, Hair Care, Makeup, Others), By End-User (Women, Men), By Distribution Channel (Supermarkets & Hypermarkets, Mass Merchandiser, Specialty Retailer, Convenience Stores, Online, Pharmacy & Drug Stores, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape BANILLA CO, AMOREPACIFIC, The Crème Shop, Clio, Able C&C, The Face Shop Inc., TolyMoly, LG HOUSEHOLD & HEALTH CARE LTD. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- BANILLA CO

- AMOREPACIFIC

- The Crème Shop

- Clio

- Able C&C

- The Face Shop, Inc.

- TolyMoly

- LG HOUSEHOLD & HEALTH CARE LTD.

Our Clients

- 178398

- Feb 2026