Global Industrial Oil Market Size, Share, Growth Analysis Type (Mineral, Synthetic & Semi-Synthetic, Bio-based), Oil Type (Hydraulic Oils, Process Oil, Industrial Engine Oils, Gear Oils, Metal Working Fluids, Turbine and Circulating Oils, Refrigerating Oils, Compressor Oils, Others), Source (Crude Oil, Soybean, Rapeseed, Sunflower, Palm, Others), End Use (Energy Generation, Oil & Gas, Manufacturing, Automotive, Heavy Engineering Equipment, Others), Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Mar 2026

- Report ID: 180728

- Number of Pages: 346

- Format:

-

keyboard_arrow_up

Quick Navigation

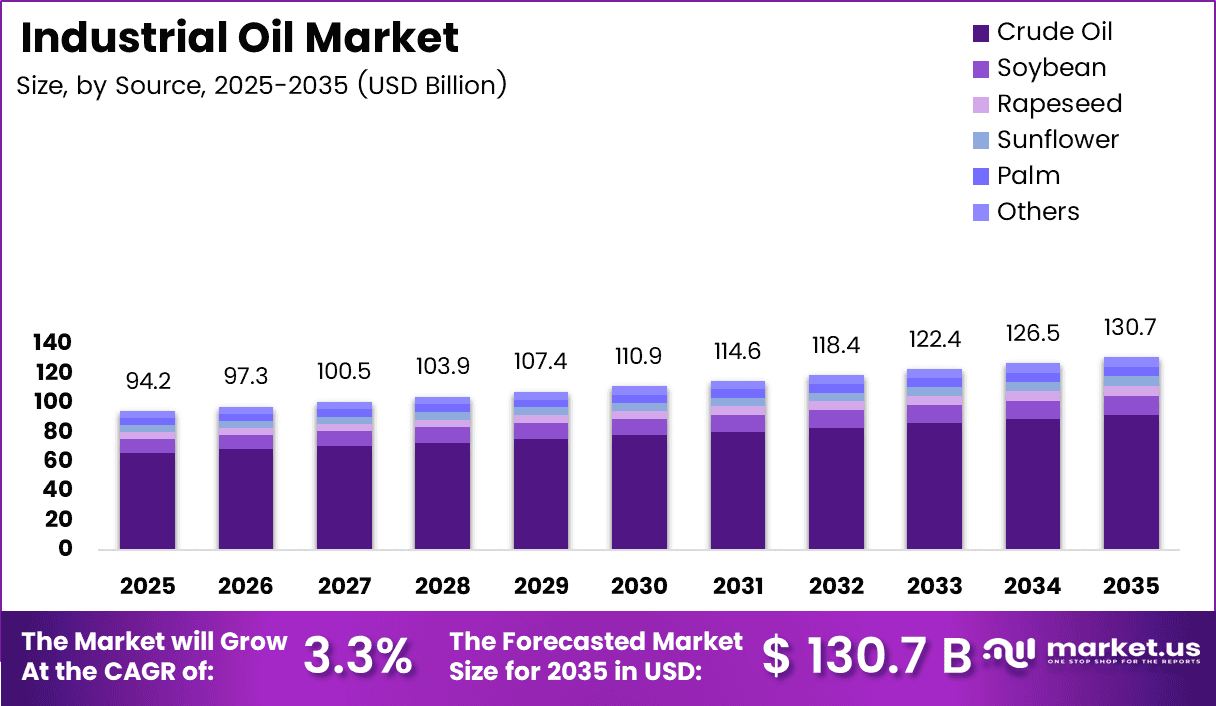

Global Industrial Oil Market size is expected to be worth around USD 130.7 Billion by 2035 from USD 94.2 Billion in 2025, growing at a CAGR of 3.3% during the forecast period 2026 to 2035.

Industrial oil refers to a broad range of lubricants, process fluids, and specialty oils used across heavy industries, manufacturing, energy generation, and automotive sectors. These oils reduce friction, prevent wear, and enhance operational efficiency in machinery and equipment. Moreover, they are essential for maintaining the performance and longevity of industrial assets.

The market covers several product types, including hydraulic oils, gear oils, turbine oils, compressor oils, and metal working fluids. These products are derived from mineral, synthetic, semi-synthetic, and bio-based sources. Consequently, the diversity of product types supports a wide range of end-use industries with varying performance requirements.

Growth in this market is primarily driven by expanding industrial activity across emerging economies, increasing demand from the energy generation and oil and gas sectors, and rising adoption of high-performance synthetic lubricants. Additionally, growing awareness of equipment maintenance and asset reliability continues to support steady market expansion.

Government regulations around environmental compliance and sustainability are reshaping sourcing strategies. Regulatory bodies in the European Union and Asia Pacific are promoting the use of bio-based and low-emission industrial oils. Therefore, manufacturers are increasingly investing in research and development to meet evolving environmental standards and customer requirements.

According to the U.S. Energy Information Administration, the United States imports approximately 7 million barrels of crude oil each day, with about 39 percent sourced from Canada and 11 percent from Mexico. This highlights the significance of stable crude oil supply chains for industrial lubricant production globally.

Furthermore, the U.S. net oil trade balance has improved significantly, reaching a positive 2.8 million barrels per day, compared to a deficit of 12 million barrels per day in the mid-2000s. This shift reflects stronger domestic production capacity, which in turn supports the availability and pricing of base oils used in industrial lubricant formulations.

Key Takeaways

- The global Industrial Oil Market is valued at USD 94.2 Billion in 2025.

- The market is projected to reach USD 130.7 Billion by 2035, growing at a CAGR of 3.3%.

- By Type, Mineral oil holds the dominant share at 64.5% in 2025.

- By Oil Type, Hydraulic Oils lead the segment with a 31.2% market share.

- By Source, Crude Oil dominates with a 70.4% share in the market.

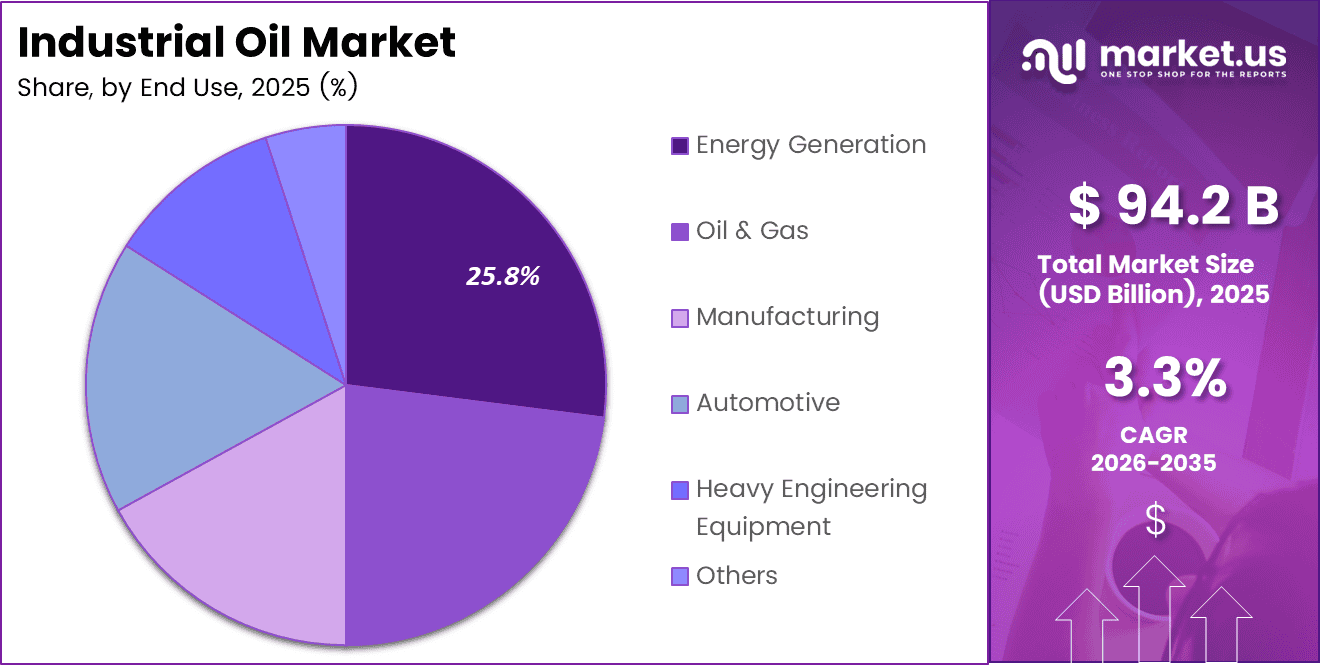

- By End Use, Energy Generation is the leading segment, capturing 25.8% of the market.

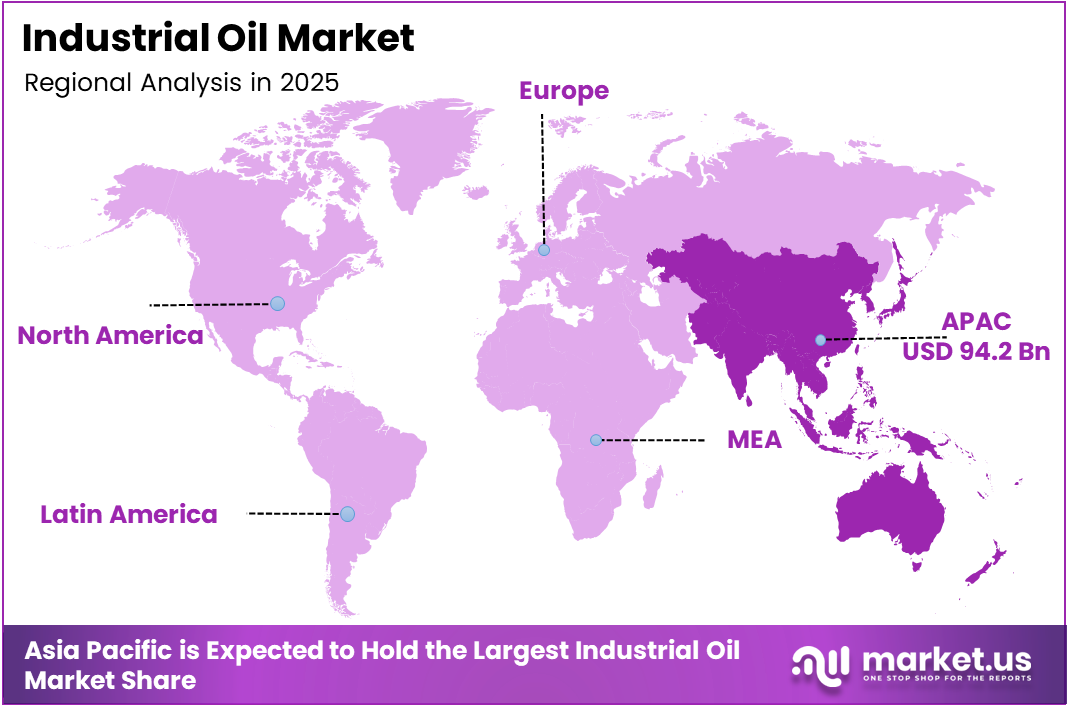

- Asia Pacific is the dominant region with a market share of 42.3%, valued at USD 94.2 Billion.

Type Analysis

Mineral dominates with 64.5% due to its widespread availability, cost-effectiveness, and established use across heavy industries.

In 2025, Mineral held a dominant market position in the Type segment of the Industrial Oil Market, with a 64.5% share. Mineral oils remain the most widely used type due to their cost efficiency, proven performance, and broad compatibility with existing industrial systems. Moreover, their availability from crude oil refining supports consistent supply at competitive pricing.

Synthetic and Semi-Synthetic oils are gaining significant traction across precision manufacturing and high-temperature applications. These oils offer superior thermal stability, extended service life, and reduced maintenance frequency. Consequently, industries such as aerospace, automotive, and advanced manufacturing are increasingly shifting toward synthetic formulations for critical equipment.

Bio-based industrial oils represent a growing segment driven by sustainability mandates and regulatory pressure. Derived from vegetable and plant-based sources, these oils offer biodegradability and lower toxicity. Additionally, increasing government support for green industrial practices is encouraging manufacturers to develop and adopt bio-based alternatives across multiple end-use sectors.

Oil Type Analysis

Hydraulic Oils dominate with 31.2% due to their critical role in powering fluid-driven machinery across industries.

In 2025, Hydraulic Oils held a dominant market position in the Oil Type segment of the Industrial Oil Market, with a 31.2% share. These oils are essential for transmitting power in hydraulic systems used across construction, mining, and manufacturing equipment. Moreover, the rapid expansion of heavy engineering globally continues to support strong demand for hydraulic lubricants.

Process Oil plays a vital role in polymer processing, rubber manufacturing, and textile industries. These oils act as softeners, plasticizers, and carriers in various production processes. Therefore, growth in the polymer and rubber sectors directly drives demand for high-quality process oils in both developed and emerging markets.

Industrial Engine Oils are widely used in stationary engines, power generators, and compressors deployed across energy and manufacturing facilities. These oils ensure smooth mechanical operation and reduce component wear under heavy loads. Additionally, increasing investments in backup power infrastructure and distributed energy systems are supporting consistent demand for industrial engine oils.

Gear Oils are designed for use in enclosed gear systems, including gearboxes, differentials, and axles in industrial machinery. They provide extreme pressure protection and thermal stability in demanding operating environments. Consequently, their use is widespread in steel plants, paper mills, and mining operations where gear-driven systems are critical.

Metal Working Fluids are used extensively in cutting, grinding, and forming operations across metalworking industries. These fluids improve surface finish quality and extend tool life. Furthermore, growing demand from precision engineering and automotive component manufacturing is driving adoption of advanced metalworking fluid formulations globally.

Turbine and Circulating Oils are used in steam and gas turbines as well as circulating lubrication systems in power plants. They offer oxidation resistance and demulsibility under high-stress conditions. Moreover, rising investments in power generation infrastructure in emerging economies are supporting steady demand for turbine-grade lubricants.

Refrigerating Oils are specifically formulated to work with refrigerants in industrial cooling and refrigeration systems. These oils maintain viscosity and chemical stability at low operating temperatures. Additionally, the expansion of cold chain logistics and industrial refrigeration facilities is contributing to growing demand in this sub-segment.

Compressor Oils are essential for lubricating air and gas compressors used across industries such as oil and gas, pharmaceuticals, and food processing. They prevent oxidation and carbon deposit formation. Therefore, growing reliance on compressed air systems in industrial automation and process manufacturing is supporting sustained demand for compressor oils.

The Others category includes specialty industrial lubricants such as chain oils, open gear compounds, and wire rope lubricants. These niche products serve specific applications across industries with unique operational demands. Consequently, their market share, though smaller, remains stable due to consistent requirement from specialized industrial segments.

Source Analysis

Crude Oil dominates with 70.4% due to its extensive refining infrastructure and cost-competitive base oil production.

In 2025, Crude Oil held a dominant market position in the Source segment of the Industrial Oil Market, with a 70.4% share. Crude oil-derived base stocks are the foundation of most mineral and synthetic lubricant products. Moreover, established refining networks globally ensure consistent availability and competitive pricing of crude-based industrial oils.

Soybean-based oils are widely used in bio-lubricant production due to their high oleic content and favorable environmental profile. These oils offer good lubricity and biodegradability. Additionally, strong soybean production in North America and South America supports reliable feedstock availability for bio-based industrial lubricant manufacturers.

Rapeseed oil is a leading feedstock for bio-industrial oils in Europe, where it is abundantly cultivated. It offers excellent cold-flow properties and strong oxidation stability. Consequently, European manufacturers increasingly rely on rapeseed-based formulations to meet sustainability regulations and customer demand for eco-friendly lubricants.

Sunflower oil is used as a base for specialty bio-lubricants due to its high linoleic content and light color. It finds application in food-grade and environmentally sensitive industrial settings. Furthermore, ongoing crop yield improvements in Eastern Europe and Asia are expanding the availability of sunflower oil for lubricant manufacturing.

Palm oil is used as a cost-effective bio-based feedstock in certain tropical and Asian markets. Its high saturated fat content provides thermal stability in lubricant applications. However, sustainability concerns around palm cultivation have prompted manufacturers to evaluate alternative bio-based feedstocks to align with environmental responsibility commitments.

The Others category includes sources such as castor oil, jatropha, and recycled base oils. These alternative feedstocks are gaining interest as the industry seeks to diversify supply and reduce dependence on petroleum. Therefore, increasing research into high-performance alternative base stocks is expected to expand options within this category over the forecast period.

End Use Analysis

Energy Generation dominates with 25.8% due to high lubricant consumption in turbines, generators, and power infrastructure.

In 2025, Energy Generation held a dominant market position in the End Use segment of the Industrial Oil Market, with a 25.8% share. Power plants, wind turbines, and hydroelectric facilities require large volumes of high-performance lubricants to ensure uninterrupted operations. Moreover, global investments in expanding energy capacity continue to drive consistent demand from this segment.

Oil and Gas remains a major end-use sector, consuming significant volumes of drilling fluids, compressor oils, and gear lubricants. These applications require oils with extreme pressure resistance and thermal durability. Consequently, ongoing upstream exploration and downstream processing activities sustain robust lubricant demand across the oil and gas value chain.

Manufacturing is a broad segment that includes metalworking, plastics processing, and general industrial operations. Lubricants used in this sector must meet strict performance and purity standards. Additionally, the rise of automated manufacturing lines and precision engineering has increased demand for specialty lubricants with enhanced cleanliness and extended service intervals.

Automotive end users rely on industrial oils for assembly line machinery, stamping equipment, and component testing systems. Unlike passenger vehicle engine oils, industrial automotive lubricants focus on equipment performance and uptime. Therefore, growth in vehicle production volumes globally directly correlates with increasing lubricant consumption at automotive manufacturing facilities.

Heavy Engineering Equipment includes mining, construction, and agricultural machinery that operates under extreme mechanical stress. These machines demand highly durable lubricants that resist contamination and maintain viscosity under load. Furthermore, increasing infrastructure development across Asia Pacific, Africa, and Latin America is fueling demand for high-performance lubricants in heavy equipment applications.

The Others category encompasses segments such as food and beverage processing, marine, and pharmaceutical industries. These sectors require specialized lubricants that meet safety, purity, and regulatory standards. Consequently, niche demand from food-grade and marine-grade lubricant applications continues to support this diverse category within the industrial oil market.

Key Market Segments

By Type

- Mineral

- Synthetic & Semi-Synthetic

- Bio-based

By Oil Type

- Hydraulic Oils

- Process Oil

- Industrial Engine Oils

- Gear Oils

- Metal Working Fluids

- Turbine and Circulating Oils

- Refrigerating Oils

- Compressor Oils

- Others

By Source

- Crude Oil

- Soybean

- Rapeseed

- Sunflower

- Palm

- Others

By End Use

- Energy Generation

- Oil & Gas

- Manufacturing

- Automotive

- Heavy Engineering Equipment

- Others

Drivers

Rising Industrial Activity and Equipment Maintenance Demand Drive Industrial Oil Market Growth

The expansion of industrial production across emerging economies is one of the most significant drivers of the industrial oil market. Rapid infrastructure development, increased manufacturing output, and growing energy investments are driving higher consumption of lubricants and process oils. Moreover, rising awareness of preventive maintenance is encouraging industries to invest in high-quality industrial oil products.

The energy generation sector plays a central role in sustaining demand. Power plants, wind turbines, and gas turbines require continuous lubrication to maintain efficiency and prevent mechanical failure. Consequently, growing global energy capacity additions, particularly in Asia Pacific and the Middle East, are generating consistent and large-volume demand for turbine, hydraulic, and circulating oils.

Additionally, the automotive and heavy engineering equipment industries are contributing to strong lubricant consumption. Assembly lines, stamping presses, and construction machinery all rely on industrial oils for smooth operations. Therefore, increasing vehicle production globally and ongoing infrastructure projects across developing economies are reinforcing demand for a wide range of industrial oil types and formulations.

Restraints

Environmental Regulations and Volatility in Crude Oil Prices Restrain Industrial Oil Market Growth

Stringent environmental regulations are placing significant pressure on conventional mineral oil manufacturers. Governments in Europe and North America are enforcing strict limits on the use of petroleum-derived lubricants due to concerns about soil and water contamination. Consequently, manufacturers face rising compliance costs and the need to reformulate products to meet evolving regulatory requirements.

Crude oil price volatility presents a major challenge for industrial oil producers. Since crude oil is the primary feedstock for mineral and many synthetic lubricants, fluctuations in global oil prices directly affect production costs and profit margins. Moreover, supply disruptions and geopolitical uncertainties can cause sudden cost increases, making it difficult for manufacturers to maintain stable pricing for customers.

Additionally, the growing adoption of electric machinery and dry lubrication technologies is beginning to reduce demand for conventional industrial oils in certain applications. Advanced manufacturing equipment increasingly requires less lubrication than traditional counterparts. Therefore, technology-driven changes in industrial operations may gradually limit the long-term volume growth potential of the industrial oil market in select segments.

Growth Factors

Adoption of Synthetic Lubricants and Sustainability Initiatives Accelerate Industrial Oil Market Expansion

The shift toward synthetic and semi-synthetic industrial oils is a key growth factor in this market. Synthetic oils offer superior oxidation resistance, extended drain intervals, and better performance at extreme temperatures. Moreover, as industries prioritize equipment longevity and operational efficiency, the adoption of high-performance synthetic lubricants continues to rise across manufacturing, energy, and automotive sectors.

Growing sustainability requirements are opening new opportunities for bio-based industrial oils. Companies are reformulating product lines using plant-based feedstocks such as soybean, rapeseed, and sunflower oils to reduce their environmental footprint. Consequently, the bio-lubricants segment is expected to grow faster than conventional oil types as regulatory pressures and corporate sustainability goals converge across global markets.

Furthermore, increasing investment in digitalization and smart maintenance is transforming how industrial oils are selected and managed. Predictive maintenance tools and oil condition monitoring systems are helping industries optimize lubricant usage and reduce waste. Therefore, this trend is not only improving operational efficiency but also expanding the market for premium, technically advanced industrial oil products over the forecast period.

Emerging Trends

Bio-Based Formulations and Digital Lubrication Management Are Reshaping the Industrial Oil Market

Bio-based and biodegradable industrial oils are emerging as a leading trend driven by sustainability mandates and environmental regulations. Industries operating in ecologically sensitive areas are actively replacing mineral oils with plant-derived alternatives. Moreover, the development of high-performance bio-lubricants with extended service life is removing previous performance barriers that limited their widespread adoption.

The integration of Internet of Things technology and oil condition monitoring systems is transforming industrial lubrication practices. Real-time data on viscosity, contamination levels, and temperature enables predictive maintenance decisions. Consequently, companies are reducing unplanned downtime and lubricant waste by transitioning from scheduled to condition-based oil change intervals, which is also driving demand for premium industrial oil products.

Additionally, the development of multi-functional industrial oils that combine lubrication, rust prevention, and corrosion protection into a single product is gaining momentum. These hybrid formulations reduce inventory complexity and simplify maintenance procedures. Therefore, manufacturers that invest in technically differentiated, multipurpose industrial oil solutions are positioning themselves to capture premium market segments and build stronger customer loyalty over time.

Regional Analysis

Asia Pacific Dominates the Industrial Oil Market with a Market Share of 42.3%, Valued at USD 94.2 Billion

Asia Pacific holds the largest share of the global industrial oil market, accounting for 42.3% of the total market, valued at USD 94.2 Billion in 2025. The region’s dominance is driven by rapid industrialization in China, India, and Southeast Asia, as well as massive energy infrastructure expansion. Moreover, strong growth in manufacturing, automotive production, and heavy engineering continues to sustain high lubricant consumption across the region.

North America Industrial Oil Market Trends

North America represents a mature but steadily growing market for industrial oils, supported by a large base of energy, manufacturing, and automotive industries. The United States is the largest consumer in the region, with significant demand from oil and gas operations and industrial machinery. Additionally, growing interest in synthetic and bio-based lubricants is supporting product premiumization across the region’s industrial sectors.

Europe Industrial Oil Market Trends

Europe maintains a strong industrial oil market characterized by high regulatory standards and a strong push toward sustainable lubrication solutions. Countries such as Germany, France, and the UK drive significant demand from precision manufacturing, automotive, and energy sectors. Furthermore, the European Union’s green industrial policies are accelerating the adoption of bio-based and low-emission industrial oil formulations across the region.

Middle East and Africa Industrial Oil Market Trends

The Middle East and Africa region is witnessing growing demand for industrial oils driven by expansion in oil and gas, construction, and power generation sectors. GCC countries are major consumers due to large-scale energy and infrastructure investments. Consequently, increasing diversification of Gulf economies and rising manufacturing activity in South Africa are creating new opportunities for industrial lubricant suppliers in this region.

Latin America Industrial Oil Market Trends

Latin America represents an emerging growth market for industrial oils, led by Brazil and Mexico with their sizeable manufacturing and automotive sectors. The region also benefits from significant mining and energy activities that require high volumes of specialty lubricants. Moreover, growing foreign direct investment in industrial infrastructure across Latin America is expected to support steady market growth throughout the forecast period.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

ExxonMobil Corporation is one of the world’s largest producers and distributors of industrial lubricants, offering a comprehensive portfolio of hydraulic oils, gear oils, turbine oils, and specialty fluids. The company leverages advanced base oil technology and a global supply chain to serve diverse industrial end-use sectors. Moreover, its commitment to synthetic and high-performance formulations positions it as a preferred partner for demanding industrial applications.

Shell plc maintains a strong global presence in the industrial oil market through its well-established lubricants division, offering products across all major oil types including hydraulic, compressor, and metalworking fluids. The company has made significant investments in developing bio-based and low-emission lubricant formulations to align with sustainability goals. Consequently, Shell continues to expand its market reach in Asia Pacific and emerging economies through strategic distribution partnerships.

TotalEnergies SE is a major player in the industrial lubricants segment, with a broad range of products catering to energy generation, manufacturing, and oil and gas applications. The company has been actively developing synthetic lubricant solutions that meet the performance requirements of modern industrial equipment. Additionally, TotalEnergies is investing in circular economy initiatives, including used oil re-refining, to strengthen its sustainability credentials in the global industrial oil market.

Chevron Corporation serves the industrial oil market through its well-regarded lubricants brand, offering products designed for hydraulic systems, compressors, turbines, and gear applications. The company’s research and development capabilities support continuous product innovation in response to evolving industry requirements. Furthermore, Chevron’s strong presence in the oil and gas sector provides it with unique insights into the lubrication needs of upstream and downstream industrial operations worldwide.

Key players

- ExxonMobil Corporation

- Shell plc

- TotalEnergies SE

- Chevron Corporation

- BP plc (Castrol Industrial)

- Fuchs Petrolub SE

- Idemitsu Kosan Co., Ltd.

- SK Lubricants

- Sinopec Limited

- Phillips 66 Lubricants

- Archer-Daniels-Midland Company

- Bunge Limited

- Gemtek Products

- Cargill, Incorporated

- AAK Kamani

- Other Key Players

Recent Developments

- January 2026 – HF Sinclair (DINO) completed the acquisition of Industrial Oils Unlimited, strengthening its specialty industrial lubricants portfolio. This strategic acquisition is expected to expand the company’s product capabilities and customer reach across key industrial end-use sectors in North America.

- October 2025 – SNF completed the acquisition of Syensqo’s Oil and Gas division, broadening its technology offering for customers in the oil and gas sector. The deal is designed to help clients enhance their operational processes while preserving natural resources through more efficient chemical and lubrication solutions.

Report Scope

Report Features Description Market Value (2025) USD 94.2 Billion Forecast Revenue (2035) USD 130.7 Billion CAGR (2026-2035) 3.3% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered Type (Mineral, Synthetic & Semi-Synthetic, Bio-based), Oil Type (Hydraulic Oils, Process Oil, Industrial Engine Oils, Gear Oils, Metal Working Fluids, Turbine and Circulating Oils, Refrigerating Oils, Compressor Oils, Others), Source (Crude Oil, Soybean, Rapeseed, Sunflower, Palm, Others), End Use (Energy Generation, Oil & Gas, Manufacturing, Automotive, Heavy Engineering Equipment, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape ExxonMobil Corporation, Shell plc, TotalEnergies SE, Chevron Corporation, BP plc (Castrol Industrial), Fuchs Petrolub SE, Idemitsu Kosan Co., Ltd., SK Lubricants, Sinopec Limited, Phillips 66 Lubricants, Archer-Daniels-Midland Company, Bunge Limited, Gemtek Products, Cargill, Incorporated, AAK Kamani, Other Key Players Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- ExxonMobil Corporation

- Shell plc

- TotalEnergies SE

- Chevron Corporation

- BP plc (Castrol Industrial)

- Fuchs Petrolub SE

- Idemitsu Kosan Co., Ltd.

- SK Lubricants

- Sinopec Limited

- Phillips 66 Lubricants

- Archer-Daniels-Midland Company

- Bunge Limited

- Gemtek Products

- Cargill, Incorporated

- AAK Kamani

- Other Key Players

Our Clients

- 180728

- Mar 2026