Global Homeland Security and Emergency Management Market Size, Share, Growth Analysis By Technology (Facial Recognition Cameras, Thermal Imaging Technology, AI-based Solutions, C2 Solutions, Blockchain Solutions, Others), By Vertical (Homeland Security, Emergency Management), By Solution (Systems, Services), By Installation (New Installation, Upgrade), By End-Use (Law Enforcement and Intelligence Gathering, Cybersecurity, Aviation Security, Maritime Security, Critical Infrastructure Security, Risk and Emergency Services, Border Security, CBRNE Security), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Apr 2026

- Report ID: 184103

- Number of Pages: 251

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

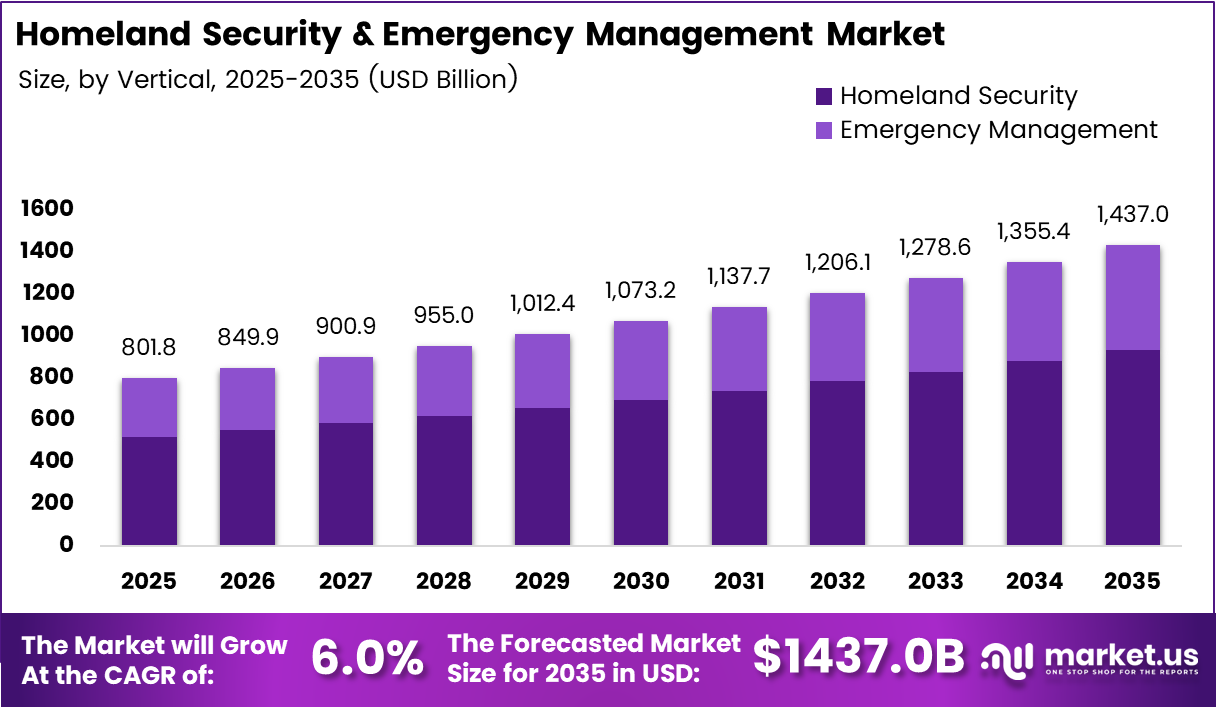

Global Homeland Security and Emergency Management Market size is expected to be worth around USD 1,437.0 Billion by 2035 from USD 801.8 Billion in 2025, growing at a CAGR of 6.0% during the forecast period 2026 to 2035.

The homeland security and emergency management market covers technology systems, services, and solutions that governments and agencies use to prevent threats, respond to crises, and protect critical infrastructure. This includes AI-based platforms, surveillance systems, border security tools, cybersecurity programs, and emergency response coordination networks deployed across federal, state, and local levels.

Federal budget commitments signal the structural scale of this market. FEMA actively uses machine learning combined with geospatial imaging to analyze pre- and post-disaster satellite photos, enabling faster identification of impacted zones and more precise resource deployment. This operational shift from manual assessment to automated analysis compresses response timelines and reduces human error in high-stakes environments.

Government investment continues to anchor market expansion. Defense procurement cycles, cybersecurity mandates, and interoperability requirements across law enforcement and emergency agencies create sustained, multi-year contract pipelines. This structure favors established vendors with federal certification histories over new entrants, making the competitive landscape relatively concentrated at the top tier.

The solutions segment, led by integrated systems covering surveillance, command-and-control, and biometrics, captures the largest share of expenditure. Agencies increasingly bundle hardware, software, and data analytics into unified procurement packages rather than buying point solutions. This trend toward integrated systems architectures raises switching costs and locks in long-term vendor relationships.

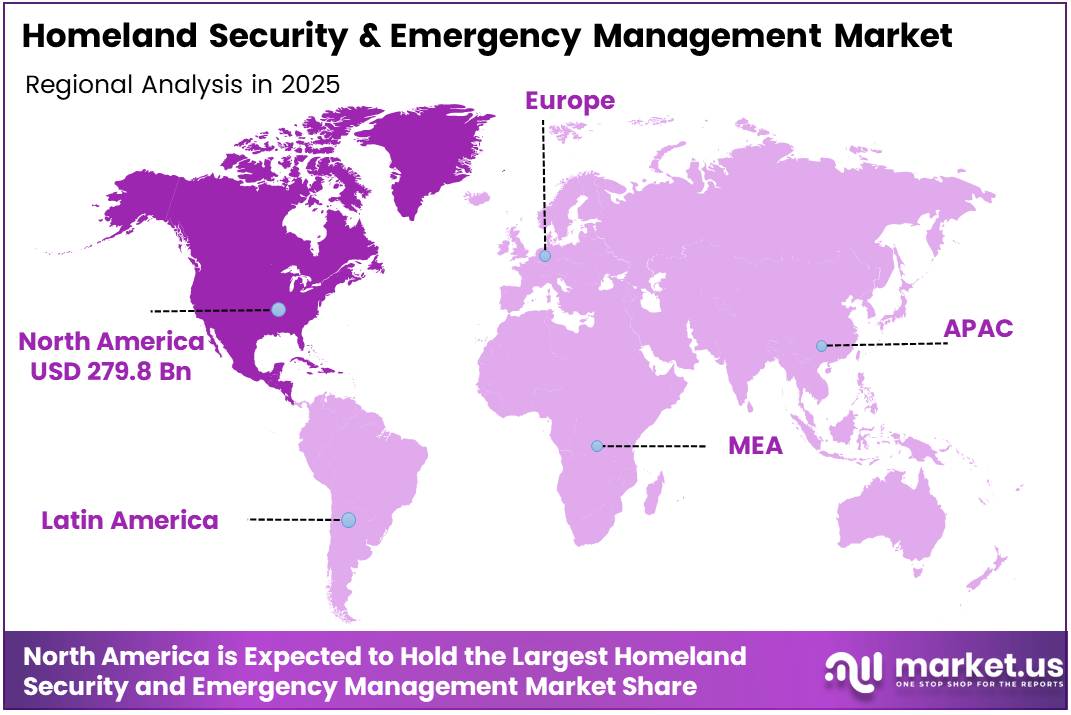

North America maintains a dominant position, accounting for 34.90% of global market value at USD 279.8 billion. Federal mandates, mature procurement frameworks, and high per-agency technology budgets create conditions that other regions are beginning to replicate, particularly Western Europe and select Asia-Pacific defense ministries.

According to the Deloitte-NEMA National Risk Study 2025, 64% of state emergency management directors identified funding as their most significant challenge, yet 97% said they would invest additional funds in workforce and 89% in technology and infrastructure if resources were available. This gap between intent and available funding explains why federal grant programs and public-private partnerships carry disproportionate influence over technology adoption timelines in this market.

According to govwhitepapers.com, the FY 2025 DHS budget allocates $112.4 billion total, including $3 billion specifically for cybersecurity — the largest cybersecurity allocation in agency history. This signals that cyber defense has shifted from a discretionary line item to a structural budget priority, which directly expands the addressable market for cybersecurity solution vendors serving federal clients.

Key Takeaways

- The global Homeland Security and Emergency Management Market is valued at USD 801.8 Billion in 2025 and is forecast to reach USD 1,437.0 Billion by 2035.

- The market advances at a CAGR of 6.0% during the forecast period 2026 to 2035.

- By Technology, Facial Recognition Cameras lead with a 21.3% share in 2025.

- By Vertical, Homeland Security dominates with a 68.4% share, reflecting its larger scale versus Emergency Management.

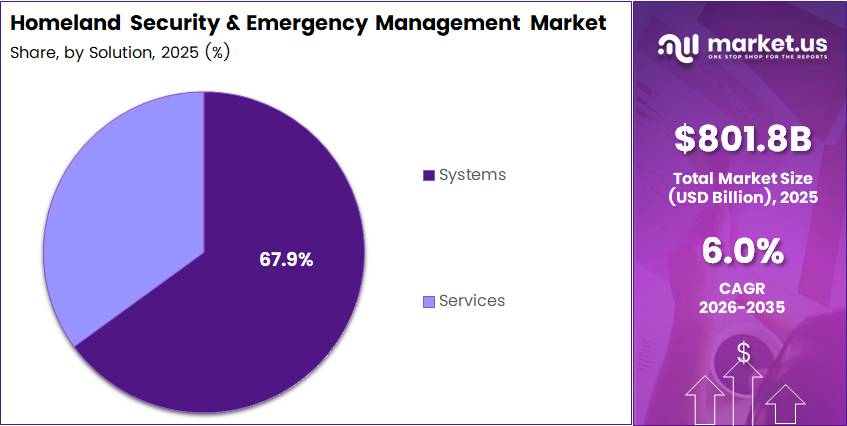

- By Solution, Systems hold a 64.1% share, outpacing Services in revenue contribution.

- By Installation, New Installation accounts for 62.6% of the market, indicating ongoing infrastructure build-out.

- By End-Use, Law Enforcement and Intelligence Gathering leads at 21.9% share.

- North America holds the largest regional share at 34.90%, valued at USD 279.8 Billion.

Technology Analysis

Facial Recognition Cameras dominate with 21.3% due to wide deployment across border and law enforcement.

In 2025, Facial Recognition Cameras held a dominant market position in the By Technology segment of the Homeland Security and Emergency Management Market, with a 21.3% share. Agencies prioritize biometric identity verification because it reduces manual processing time at borders and checkpoints while generating data trails for intelligence purposes. This drives sustained hardware and software procurement cycles tied to identity management platforms.

Thermal Imaging Technology serves as a force-multiplier for perimeter surveillance and search-and-rescue operations in low-visibility conditions. Law enforcement and border agencies deploy thermal sensors where standard cameras fail — night operations, smoke-filled environments, and dense vegetation zones. The technology’s reliability in degraded conditions makes it a standard complement to camera-based systems rather than a replacement.

AI-based Solutions carry the highest margin potential within the technology segment because they layer onto existing hardware infrastructure rather than requiring full system replacement. Agencies use AI for real-time threat scoring, pattern detection across surveillance feeds, and predictive resource allocation. The shift toward software-defined security creates recurring revenue streams for vendors beyond the initial hardware sale.

C2 Solutions (Command and Control) differentiate through integration depth — they connect disparate agency data streams into a single operational picture. Multi-agency deployments require C2 platforms that translate across incompatible legacy systems. Vendors with strong integration track records hold a structural advantage because agencies face high transition costs once a C2 platform is embedded in operations.

Blockchain Solutions represent an early-adoption segment within homeland security, primarily targeting secure data sharing between agencies and tamper-proof evidence chains. Adoption remains limited relative to AI and imaging, but federal interest in verifiable identity records and cross-agency audit trails positions blockchain as a longer-horizon growth area within the technology mix.

Others within the technology segment include drone detection systems, acoustic sensors, and radiation monitoring tools. These niche technologies serve specific threat environments — airports, ports, nuclear facilities — and are typically procured as point solutions rather than enterprise-wide deployments. However, integration with AI analytics platforms is expanding their operational value.

Vertical Analysis

Homeland Security dominates with 68.4% due to larger federal budget scale and broader mandate coverage.

In 2025, Homeland Security held a dominant market position in the By Vertical segment of the Homeland Security and Emergency Management Market, with a 68.4% share. Federal agencies under the DHS umbrella — including CBP, ICE, TSA, and CISA — operate across border security, aviation, cyber, and critical infrastructure, creating a spending base that Emergency Management cannot match in scale. This concentration of budget authority within a single department structure sustains predictable procurement volumes.

Emergency Management carries distinct procurement characteristics that differ structurally from Homeland Security. State and local agencies drive a significant portion of Emergency Management spending, creating a fragmented buyer landscape with varied budget cycles and technology maturity levels. According to the Deloitte-NEMA National Risk Study 2025, nearly 60% of state emergency management directors report only an intermediate level of technology capability, indicating that modernization demand remains deep but constrained by budget and workforce gaps rather than lack of need.

Solution Analysis

Systems dominate with 64.1% due to integrated hardware-software procurement preference among agencies.

In 2025, Systems held a dominant market position in the By Solution segment of the Homeland Security and Emergency Management Market, with a 64.1% share. Agencies prefer systems-based procurement because bundled solutions — combining surveillance hardware, data analytics, and command interfaces — reduce integration risk and consolidate vendor accountability. This purchasing logic creates large-value, long-cycle contracts that favor established systems integrators over specialist service providers.

Services represent a structurally important but secondary segment, covering maintenance, training, cybersecurity assessments, and managed operations. As deployed systems age and require continuous software updates and threat recalibration, services revenue grows alongside the installed base. Vendors who secure the initial systems contract position themselves to capture recurring services revenue, making the systems-to-services transition a core margin strategy.

Installation Analysis

New Installation dominates with 62.6% due to ongoing greenfield deployments in underserved security zones.

In 2025, New Installation held a dominant market position in the By Installation segment of the Homeland Security and Emergency Management Market, with a 62.6% share. Federal and state agencies continue to deploy security infrastructure in previously uncovered locations — particularly at soft-target venues, rural border zones, and emerging critical infrastructure sites. This greenfield activity sustains new installation demand independent of upgrade cycles.

Upgrade installations target the large installed base of legacy systems that agencies deployed over the prior two decades. Aging command-and-control platforms, first-generation biometric readers, and pre-IP surveillance networks require modernization to support AI integration and cloud connectivity. As the installed base ages, the upgrade segment’s share is expected to grow, narrowing the gap with new installations over the forecast period.

End-Use Analysis

Law Enforcement and Intelligence Gathering dominates with 21.9% due to largest federal operational workforce and technology budget.

In 2025, Law Enforcement and Intelligence Gathering held a dominant market position in the By End-Use segment of the Homeland Security and Emergency Management Market, with a 21.9% share. Federal law enforcement agencies — including the FBI, DEA, and DHS components — combine large operational workforces with technology-intensive intelligence missions. Surveillance platforms, data analytics tools, and mobile communication systems generate consistent procurement demand across this end-use category.

Cybersecurity as an end-use vertical reflects the shift in threat priorities toward digital infrastructure. Federal agencies now treat cyber operations as a core security function rather than a support activity. The FY 2025 DHS budget’s record cybersecurity allocation of $3 billion confirms this repositioning and signals growing procurement volumes for intrusion detection, network monitoring, and zero-trust architecture vendors.

Aviation Security spans airport screening technology, passenger identity verification, and cargo inspection systems. TSA budget allocations drive procurement cycles in this end-use category, and infrastructure upgrades at major airports generate multi-year equipment and integration contracts. Biometric screening investments are reshaping the checkpoint technology stack at high-volume air travel facilities.

Maritime Security covers port surveillance, vessel tracking, and coastal border monitoring systems. The distributed geography of maritime infrastructure — across thousands of miles of coastline and hundreds of commercial ports — requires networked sensor arrays and real-time data fusion platforms. This structural complexity supports higher per-installation system values than many other end-use categories.

Critical Infrastructure Security addresses protection of power grids, water systems, transportation networks, and financial systems. Agencies responsible for these sectors increasingly deploy AI-driven anomaly detection and physical access control systems. The interdependency between digital and physical infrastructure within this category creates demand for integrated solutions rather than standalone tools.

Risk and Emergency Services encompasses the technology stack used by FEMA and state emergency management agencies — including alert systems, situational awareness platforms, and interoperable communications networks. This end-use category benefits directly from federal grant programs that fund technology modernization at the state and local level.

Border Security combines physical surveillance infrastructure — towers, sensors, aerial systems — with data analytics platforms for tracking cross-border movement patterns. Federal investment in border technology has remained consistent across administrations, reflecting bipartisan recognition of border management as a core national security function. AI-based anomaly detection at border crossings is becoming standard procurement across this category.

CBRNE Security (Chemical, Biological, Radiological, Nuclear, and Explosive) targets specialized threat environments including research facilities, military installations, and mass-gathering venues. Detection equipment, protective systems, and decontamination technologies form the procurement core. Incident response training and simulation platforms complement the hardware segment within this high-consequence end-use category.

Key Market Segments

By Technology

- Facial Recognition Cameras

- Thermal Imaging Technology

- AI-based Solutions

- C2 Solutions

- Blockchain Solutions

- Others

By Vertical

- Homeland Security

- Emergency Management

By Solution

- Systems

- Services

By Installation

- New Installation

- Upgrade

By End-Use

- Law Enforcement and Intelligence Gathering

- Cybersecurity

- Aviation Security

- Maritime Security

- Critical Infrastructure Security

- Risk and Emergency Services

- Border Security

- CBRNE Security

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

Drivers

Federal Cybersecurity Mandates and Escalating Threat Environments Drive Security Technology Budgets

Natural disaster frequency and domestic threat complexity are pushing emergency preparedness spending beyond traditional planning cycles. Agencies now treat disaster response as a continuous operational posture rather than an event-triggered function. This structural shift converts what were once discretionary preparedness budgets into recurring technology investment lines that sustain multi-year vendor contracts.

Cross-border threat intelligence sharing requires interoperable communication systems and unified data standards across agencies that historically operated in silos. Federal procurement guidelines increasingly mandate interoperability compliance as a contract condition. According to GovWin, DHS’s FY 2026 budget request allocates $10.7 billion for total IT investment and $3.1 billion specifically for cybersecurity activities — confirming that digital infrastructure is now the central procurement battleground, not just a supporting capability.

Domestic terrorism risk accelerates demand for predictive threat monitoring platforms that process large volumes of behavioral and communications data. Federal cybersecurity mandates extend these requirements to critical infrastructure operators beyond government agencies, broadening the total addressable market. This regulatory expansion means that private-sector operators of power, water, and transport networks now enter the same procurement pipeline as federal agencies.

Restraints

Jurisdictional Fragmentation and Budget Constraints Slow Technology Deployment at State and Local Levels

Multi-agency jurisdictional conflicts create deployment bottlenecks that delay contract execution even when technology budgets exist. When federal, state, and local agencies share operational territory but not authority, procurement decisions require multi-stakeholder approval chains. This extends contract timelines and raises implementation risk for vendors dependent on on-schedule revenue recognition.

According to the Deloitte-NEMA National Risk Study 2025, 85% of state emergency management directors cited infrastructure limitations, limited familiarity, constrained financial resources, and procurement challenges as barriers to AI adoption — despite 85% also agreeing that AI and machine learning would greatly benefit their organizations. This paradox reveals a market where demand intent and purchasing capacity are significantly misaligned, creating execution risk for vendors targeting state-level contracts.

Additionally, according to the Deloitte-NEMA National Risk Study 2025, only 25% of state emergency management directors indicated their employees possess the skills needed to effectively manage emergency conditions. Workforce capability gaps translate directly into technology underutilization — agencies that procure advanced platforms cannot extract full value without trained operators. This dynamic slows procurement decision cycles and increases the cost of deployment for solution providers who must bundle training into their contracts.

Growth Factors

Smart City Integration, Public-Private Partnerships, and AI Triage Tools Expand the Addressable Security Market

Smart city IoT infrastructure creates new data streams — connected sensors, traffic systems, utility monitors — that emergency management agencies can integrate into real-time situational awareness platforms. Municipalities investing in smart city frameworks generate simultaneous demand for public safety data fusion technology. This convergence positions security technology vendors to capture municipal infrastructure budgets alongside traditional federal contracts.

Public-private partnerships accelerate deployment of next-generation emergency alert and communication systems that governments cannot fund unilaterally. Private sector investment supplements constrained public budgets while enabling faster technology cycles than traditional federal procurement. According to GovWin, TSA’s FY 2026 budget increased by $226 million from FY 2025, with $215 million allocated for the Checkpoint Property Screening System and $20 million in new funding for Biometrics Technology R&D — signaling that aviation security modernization represents a near-term procurement opportunity with confirmed federal funding.

AI triage tools that reduce decision time in mass casualty incidents address one of the highest-cost operational failures in emergency response — delayed resource allocation. Portable communication kits designed for disaster-affected and remote zones extend emergency response reach into environments where fixed infrastructure fails. Both categories serve agencies that face increasing operational demands with constrained personnel, making automation and portability high-priority procurement criteria.

Emerging Trends

Autonomous Systems, AI Monitoring, and Cloud-Native Platforms Redefine Emergency Operations Architecture

Autonomous ground vehicles for hazardous environment reconnaissance eliminate personnel exposure in chemical, radiological, and structural collapse scenarios. Agencies deploying these systems reduce casualty risk in first-response operations while maintaining real-time ground-level intelligence collection. This creates a new procurement category that sits at the intersection of robotics, communications, and CBRNE response capabilities.

Social media AI monitoring for early civil unrest detection and cloud-native incident command platforms are replacing legacy emergency operations center systems that require physical co-location and manual data entry. According to Acuity International, a UN-affiliated AI solution reduced the time required to produce satellite imagery damage assessments after disasters to under one day — compared to multi-day timelines under traditional methods. This speed advantage directly translates to faster resource deployment and measurably better population outcomes in disaster scenarios.

Digital twin simulations for disaster planning and responder training allow agencies to rehearse complex multi-hazard scenarios without the cost and logistics of physical exercises. These platforms generate data on decision-making patterns and resource bottlenecks that agencies use to redesign response protocols. Early adopters of simulation-based training gain a structural preparedness advantage that creates differentiated procurement demand for immersive training technology vendors.

Regional Analysis

North America Dominates the Homeland Security and Emergency Management Market with a Market Share of 34.90%, Valued at USD 279.8 Billion

North America holds 34.90% of the global market at a value of USD 279.8 billion, anchored by the scale and complexity of the U.S. federal security apparatus. The DHS alone oversees dozens of agencies with distinct technology procurement cycles, creating consistent contract volumes across surveillance, cybersecurity, border security, and emergency management. Mature procurement infrastructure and mandatory compliance frameworks sustain technology refresh demand that other regions have not yet replicated.

Europe Homeland Security and Emergency Management Market Trends

Europe drives security technology adoption through NATO interoperability mandates and cross-border intelligence coordination requirements. Member states align procurement toward shared surveillance standards and cyber defense frameworks, creating demand for systems that integrate across jurisdictions. Defense spending increases across EU members, particularly in response to evolving eastern border security requirements, are expanding technology budgets for surveillance, communications, and critical infrastructure protection.

Asia Pacific Homeland Security and Emergency Management Market Trends

Asia Pacific represents the fastest-expanding geographic market, driven by government modernization programs in China, India, Japan, and South Korea. High urbanization rates, large-scale public infrastructure investments, and rising cyber threat awareness push national security agencies to upgrade legacy systems. Regional governments allocate increasing shares of defense and interior ministry budgets toward biometric identity systems, AI surveillance, and disaster preparedness platforms.

Middle East and Africa Homeland Security and Emergency Management Market Trends

The Middle East invests heavily in border protection technology, critical infrastructure defense, and counterterrorism platforms, supported by sovereign wealth fund-backed government budgets. GCC nations prioritize advanced surveillance and AI-integrated security systems as part of broader national modernization agendas. Africa presents a growing market for emergency communication infrastructure and disaster response technology, with international aid programs and multilateral security partnerships funding technology deployments.

Latin America Homeland Security and Emergency Management Market Trends

Latin America’s security technology market concentrates around urban public safety systems, border monitoring, and natural disaster preparedness — particularly in Brazil and Mexico. High rates of organized crime and recurrent climate-related disasters sustain government demand for surveillance infrastructure and emergency coordination platforms. International security cooperation programs, including U.S. and EU partnerships, supplement domestic procurement budgets and drive standards alignment.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

BAE Systems Plc positions itself at the intersection of defense electronics and homeland security analytics, competing for large-scale intelligence and surveillance contracts that require integration across classified and unclassified networks. Its strength in electronic warfare and sensor systems translates directly into border and maritime security applications, where multi-domain threat detection requires hardware-software integration depth that few competitors can match at comparable certification levels.

CACI International Inc. builds its competitive position on deep federal agency relationships and a professional services model that converts technology deployments into long-term managed services contracts. Its focus on intelligence, defense, and federal IT modernization aligns closely with DHS and CISA spending priorities. CACI’s ability to combine cleared personnel with software development capabilities gives it access to sole-source contract opportunities that commercial technology vendors cannot pursue.

Collins Aerospace leverages its aviation heritage to dominate the airport security technology segment, particularly biometric passenger processing and checkpoint systems. As TSA directs new budget allocations toward Biometrics R&D and screening infrastructure, Collins Aerospace’s existing relationships with airport operators and federal aviation authorities create a structural first-mover advantage in capturing next-generation checkpoint modernization contracts.

Elbit Systems Ltd. differentiates through its dual role as both a technology developer and an operational integrator across border, land, and naval security domains. Its border surveillance systems — combining unmanned platforms, sensors, and command software — address the multi-layer architecture that large-border-nation governments increasingly require. Elbit’s track record in deployed conflict environments provides credibility that competitive procurement evaluations in demanding security contexts prioritize.

Key Players

- BAE Systems Plc

- CACI International Inc.

- Collins Aerospace

- Elbit Systems Ltd.

- General Dynamics Corporation

- L3Harris Technologies Inc.

- Lockheed Martin Corporation

- Northrop Grumman Corporation

- SAAB AB

- Thales Group

Recent Developments

- September 2024 — Strategic Innovation Group acquired Excelicon, a Washington, D.C.-based IT consulting firm with deep experience supporting DHS, FEMA, and CISA missions. The acquisition expanded SIG’s capabilities across enterprise architecture, cyber policy, DevSecOps, and IT modernization for federal homeland security clients.

- December 2024 — Axon completed its acquisition of Dedrone, integrating the counter-UAS airspace security platform into the Axon public safety ecosystem. The deal strengthens drone-as-first-responder programs and supports protection of critical infrastructure, airports, and military installations from unauthorized drone threats.

- May 2025 — DHS canceled a $2.4 billion cybersecurity services contract previously awarded to Leidos, which had been intended to support CISA with cybersecurity solution deployment and sustainment. The cancellation followed a procurement dispute and a reorganization of DHS’s cyber acquisition strategy.

- August 2025 — FEMA released nearly $1 billion in disaster preparedness and homeland security grants to U.S. communities, including over $500 million through the Urban Areas Security Initiative. The release followed an internal program review aligned to updated DHS priorities covering soft-target security, cybersecurity, and border resilience.

- February 2026 — DHS awarded Palantir Technologies a five-year blanket purchasing agreement worth up to $1 billion to deploy its Gotham and Foundry AI platforms across DHS agencies including CBP, ICE, FEMA, TSA, and CISA. Deployment targets investigative case management, threat detection, logistics coordination, and emergency response planning.

Report Scope

Report Features Description Market Value (2025) USD 801.8 Billion Forecast Revenue (2035) USD 1,437.0 Billion CAGR (2026-2035) 6.0% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Technology (Facial Recognition Cameras, Thermal Imaging Technology, AI-based Solutions, C2 Solutions, Blockchain Solutions, Others), By Vertical (Homeland Security, Emergency Management), By Solution (Systems, Services), By Installation (New Installation, Upgrade), By End-Use (Law Enforcement and Intelligence Gathering, Cybersecurity, Aviation Security, Maritime Security, Critical Infrastructure Security, Risk and Emergency Services, Border Security, CBRNE Security) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape BAE Systems Plc, CACI International Inc., Collins Aerospace, Elbit Systems Ltd., General Dynamics Corporation, L3Harris Technologies Inc., Lockheed Martin Corporation, Northrop Grumman Corporation, SAAB AB, Thales Group Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Homeland Security and Emergency Management MarketPublished date: Apr 2026add_shopping_cartBuy Now get_appDownload Sample

Homeland Security and Emergency Management MarketPublished date: Apr 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- BAE Systems Plc

- CACI International Inc.

- Collins Aerospace

- Elbit Systems Ltd.

- General Dynamics Corporation

- L3Harris Technologies Inc.

- Lockheed Martin Corporation

- Northrop Grumman Corporation

- SAAB AB

- Thales Group

Our Clients

- 184103

- Apr 2026