Global Hirsutism Market By Treatment Type (Pharmacological Therapy (Oral Contraceptives, Anti-androgens and Insulin Sensitizers), Cosmetic Procedures (Laser Hair Removal and IPL) and Mechanical and Physical Methods (Electrolysis, Waxing and Shaving)), By Application (Upper Lip, Chin, Chest, Arms and Others (Back, Abdomen, Thighs)), By End User (Hospitals, Dermatology Clinics, Cosmetic Centers, Home Care Settings and Others), Region and Companies – Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2026-2035

- Published date: March 2026

- Report ID: 182166

- Number of Pages: 301

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

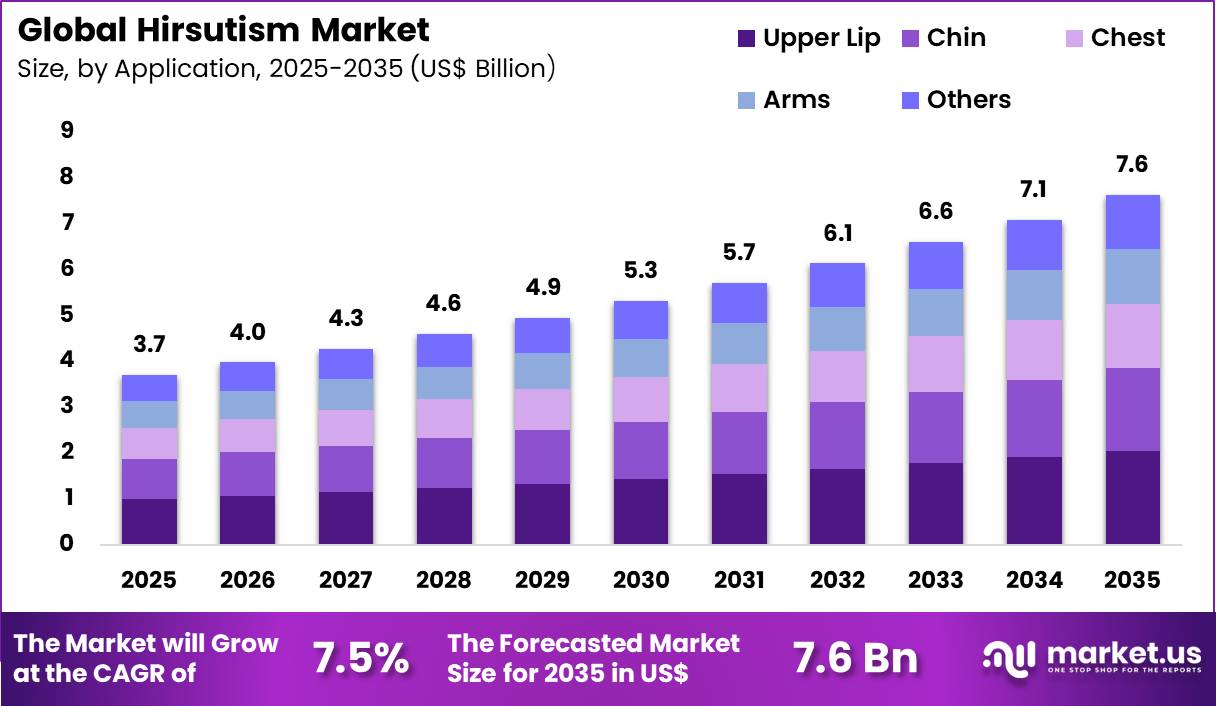

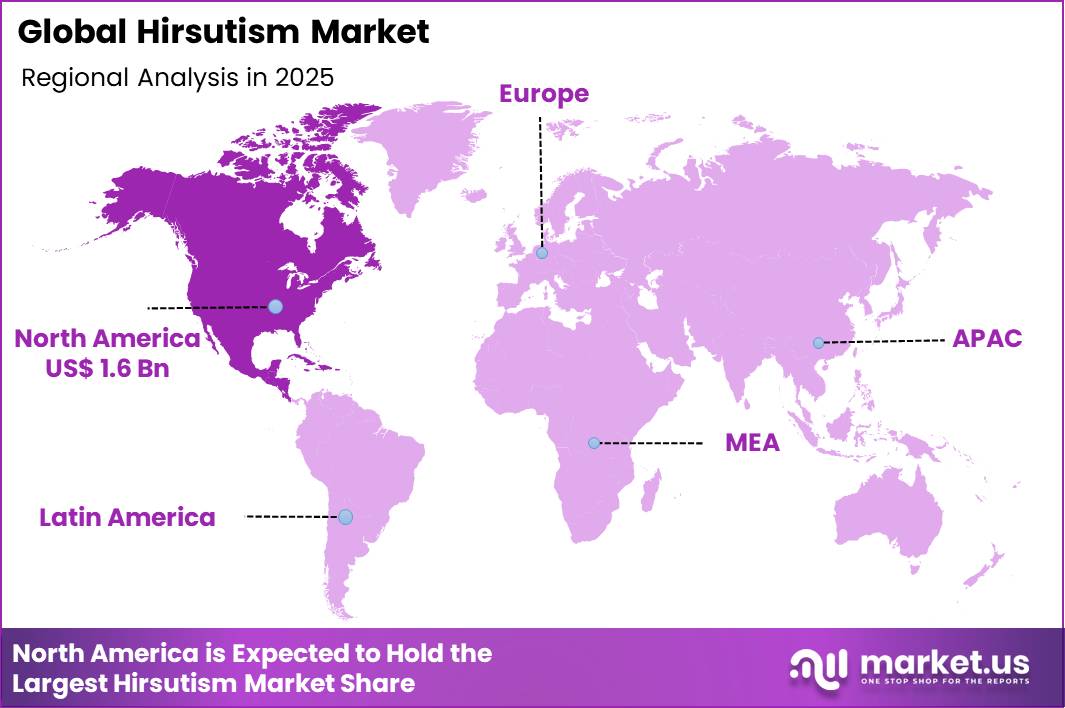

The Global Hirsutism Market size is expected to be worth around US$ 7.6 Billion by 2035 from US$ 3.7 Billion in 2025, growing at a CAGR of 7.5% during the forecast period 2026-2035. In 2025, North America led the market, achieving over 42.5% share with a revenue of US$ 1.6 Billion.

Rising prevalence of polycystic ovary syndrome and other endocrine disorders fuels the Hirsutism market as women seek effective, long-term solutions to manage excessive terminal hair growth and associated psychological distress.

Dermatologists increasingly prescribe anti-androgen therapies such as spironolactone and cyproterone acetate to suppress ovarian and adrenal androgen production, reducing hair density and coarseness on the face, chest, and abdomen over several months of consistent use.

These medications support combination regimens with oral contraceptives to regulate menstrual cycles and further lower free testosterone levels in patients with PCOS-related hirsutism. Cosmetic approaches include laser hair removal and intense pulsed light treatments that target melanin in hair follicles, achieving permanent reduction in unwanted facial and body hair for women who prefer non-systemic options.

Electrolysis provides permanent follicle destruction for small, localized areas such as the upper lip and chin, offering precise results in patients with lighter hair colors or those intolerant to light-based therapies. Topical eflornithine cream slows facial hair growth by inhibiting ornithine decarboxylase, serving as an adjunctive treatment to delay regrowth between laser sessions or in patients awaiting systemic therapy response.

Manufacturers pursue opportunities to develop novel anti-androgen formulations with improved tolerability and fewer side effects, expanding applications in adolescents and women planning pregnancy who require safer alternatives to traditional agents. These advancements support integration of metabolic therapies such as GLP-1 receptor agonists, which address underlying insulin resistance in PCOS to enhance hormonal balance and amplify anti-androgen efficacy.

By early 2026, clinical practice began incorporating GLP-1 receptor agonists alongside traditional therapies for hirsutism, particularly in patients with polycystic ovary syndrome. Studies conducted during 2025 suggest that managing metabolic factors such as weight can improve hormonal balance and enhance the effectiveness of anti-androgen treatment strategies.

In late 2025, Philips and other consumer device manufacturers expanded their smart IPL product lines with integrated sensing technologies. These systems automatically adjust energy levels based on skin tone and treatment area, improving usability and helping at-home devices deliver more consistent maintenance results closer to professional standards.

Recent trends emphasize combination therapies, at-home maintenance devices with smart features, and holistic approaches targeting metabolic contributors, positioning the market for growth in comprehensive, patient-centered hirsutism management focused on efficacy, tolerability, and quality of life.

Key Takeaways

- In 2025, the market generated a revenue of US$ 3.7 Billion, with a CAGR of 7.5%, and is expected to reach US$ 7.6 Billion by the year 2035.

- The treatment type segment is divided into pharmacological therapy, cosmetic procedures and mechanical and physical methods, with pharmacological therapy taking the lead with a market share of 45.3%.

- Considering application, the market is divided into upper lip, chin, chest, arms and others. Among these, upper lip held a significant share of 26.9%.

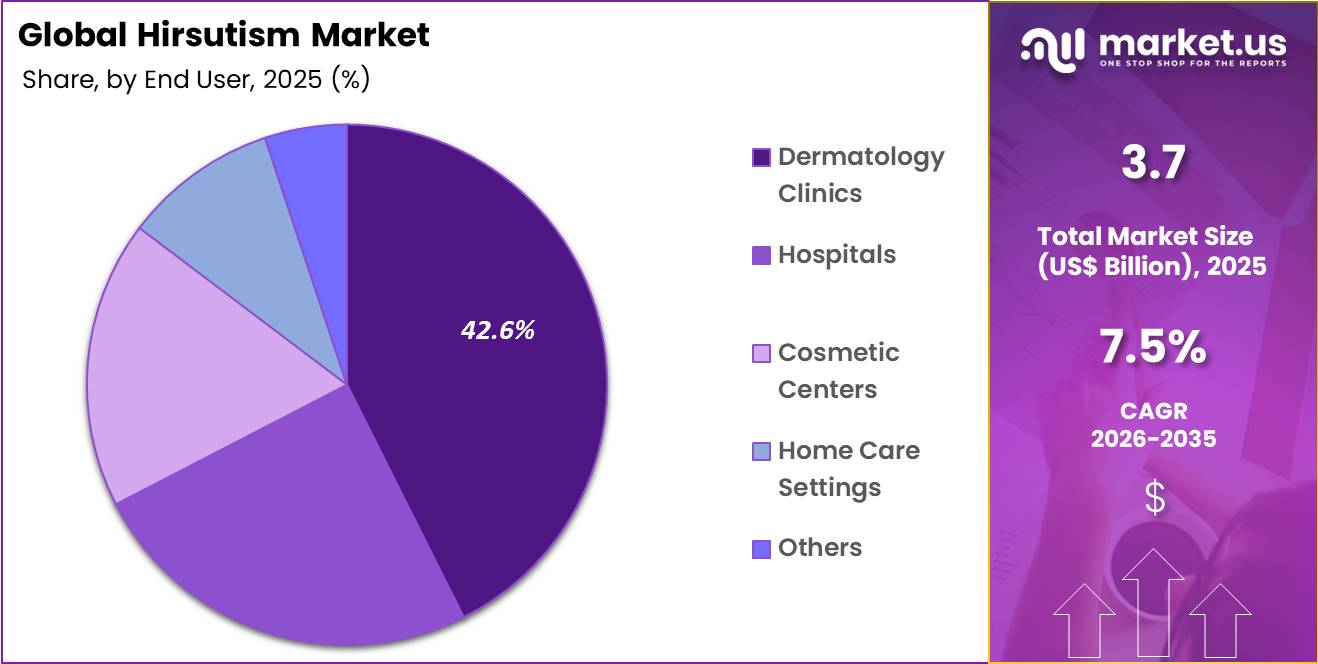

- Furthermore, concerning the end user segment, the market is segregated into hospitals, dermatology clinics, cosmetic centers, home care settings and others. The dermatology clinics sector stands out as the dominant player, holding the largest revenue share of 42.6% in the market.

- North America led the market by securing a market share of 42.5%.

Treatment Type Analysis

Pharmacological therapy accounted for 45.3% of growth within treatment type and dominates the hirsutism market because it addresses the hormonal basis of excessive hair growth rather than only removing visible hair.

Physicians frequently prescribe oral contraceptives, anti-androgens, insulin-sensitizing agents, and topical agents for women with androgen-related hair growth patterns. This treatment approach gains strong preference in patients with polycystic ovary syndrome, adrenal disorders, and other endocrine imbalances that trigger persistent hirsutism.

Clinical management often starts with drug therapy because it helps reduce new hair growth over time and supports longer-lasting improvement than short-term grooming methods. Hirsutism affects a meaningful share of women of reproductive age, and polycystic ovary syndrome remains one of the most common underlying causes, which continues to enlarge the eligible treatment pool.

Pharmacological therapy is expected to expand further as awareness of hormonal evaluation improves among gynecologists, dermatologists, and endocrinologists. Patients also prefer medical treatment when facial or body hair growth causes psychological stress, social discomfort, and repeated spending on temporary removal methods.

Drug-based management is projected to retain strong demand because it fits both mild and moderate disease pathways and integrates well with cosmetic support treatments. Improved diagnosis of insulin resistance, menstrual irregularity, and androgen excess is likely to increase prescription volumes in outpatient care.

Dermatologists increasingly recommend combined regimens that pair medication with laser or topical management, which strengthens the segment’s practical value. Broader access to women’s health consultations and hormonal screening is anticipated to support earlier intervention.

The segment also benefits from better adherence when clinicians explain that visible improvement usually requires several months of consistent treatment. As patients seek sustained reduction in unwanted hair growth and better control of recurrence, pharmacological therapy is estimated to remain the leading treatment category in this market.

Application Analysis

Upper lip accounted for 26.9% of growth within application and dominates the hirsutism market because even limited hair growth in this area becomes highly visible and often causes immediate cosmetic concern. Women usually notice upper lip hair earlier than growth on less visible body parts, which drives faster consultation and treatment seeking.

The facial location increases emotional sensitivity because patients perceive upper lip hair as socially disruptive and difficult to conceal in daily interactions. This area also requires frequent grooming, which raises frustration with shaving, threading, waxing, and bleaching over time. As a result, demand remains strong for both medical treatment and procedural intervention focused on upper lip management.

Dermatologists and cosmetic professionals often treat this site first because patients prioritize facial appearance before addressing chest, arms, or other body regions. The upper lip segment is expected to maintain leadership as aesthetic awareness continues to rise across younger and adult female populations.

Hormonal changes linked to polycystic ovary syndrome, obesity, insulin resistance, and menopause are likely to contribute to persistent facial hair complaints. The small surface area of the upper lip also makes it well suited for targeted laser sessions, topical therapy, and repeated clinic-based procedures, which improves treatment uptake.

Patients frequently assess treatment success by visible reduction in facial hair density, and that keeps the upper lip at the center of follow-up care. Social media influence, beauty standards, and rising acceptance of dermatologist-led aesthetic treatment are projected to reinforce this pattern.

Clinicians also find the upper lip clinically important because early facial involvement often prompts broader endocrine evaluation. As more women seek prompt and discreet solutions for visible facial hair, the upper lip application is anticipated to remain the most commercially significant segment in the hirsutism market.

End User Analysis

Dermatology clinics accounted for 42.6% of growth within end user and dominate the hirsutism market because they combine diagnostic expertise, procedural capability, and long-term skin and hair management in one specialized setting. Patients with unwanted hair growth often prefer dermatology clinics for accurate assessment of hair pattern, skin type, hormonal history, and treatment suitability.

These clinics manage both medical and cosmetic dimensions of hirsutism, which gives them a clear advantage over general care settings. Dermatologists prescribe topical and oral therapies, monitor adverse effects, and provide procedure-based options such as laser hair reduction and related skin treatments. This breadth of care is expected to sustain high patient inflow, especially among women seeking individualized treatment plans.

Dermatology clinics also attract patients because they offer privacy, specialist counseling, and repeat sessions in a focused outpatient environment. Many cases of hirsutism require ongoing review over several months, and clinics are well positioned to deliver consistent follow-up and treatment adjustment. The segment is projected to expand as aesthetic dermatology infrastructure grows in urban centers and as awareness of skin-focused specialty care improves.

Better access to advanced laser platforms, dermoscopy, and combination treatment protocols is likely to strengthen clinic-based management further. Patients also value shorter waiting times and more personalized attention compared with large hospital systems.

Dermatology clinics increasingly collaborate with gynecologists and endocrinologists when hirsutism presents alongside menstrual or metabolic abnormalities, which improves referral-driven growth. Rising concern over facial appearance, self-esteem, and quality of life is anticipated to keep specialty clinics at the forefront of treatment demand. As hirsutism care continues to shift toward specialized, procedure-enabled, and patient-centered models, dermatology clinics are estimated to remain the dominant end-user segment in this market.

Key Market Segments

By Treatment Type

- Pharmacological Therapy (Oral Contraceptives, Anti-androgens, Insulin Sensitizers)

- Cosmetic Procedures (Laser Hair Removal, IPL)

- Mechanical and Physical Methods (Electrolysis, Waxing, Shaving)

By Application

- Upper Lip

- Chin

- Chest

- Arms

- Others (Back, Abdomen, Thighs)

By End User

- Hospitals

- Dermatology Clinics

- Cosmetic Centers

- Home Care Settings

- Others

Drivers

Increasing prevalence of hirsutism associated with PCOS is driving the market.

A large-scale cross-sectional study published in 2025 documented hirsutism prevalence at 1.37% among sampled U.S. women. The same analysis reported a substantially higher rate of 19.12% among females diagnosed with polycystic ovary syndrome. This disparity underscores the strong link between hormonal disorders and excessive hair growth in female populations.

Healthcare providers observe rising patient presentations seeking management for facial and body hair concerns. The elevated prevalence in PCOS cases prompts greater clinical attention to underlying endocrine evaluation. Women across diverse ethnic groups demonstrate varying susceptibility, influencing targeted screening efforts.

The data highlight the need for integrated dermatologic and gynecologic care pathways. Public health initiatives increasingly address cosmetic and psychological impacts of the condition. Sustained awareness campaigns encourage early intervention to improve quality of life. This driver elevates demand for both pharmacologic and procedural treatment options nationwide.

Restraints

Absence of dedicated FDA-approved therapies specifically indicated for hirsutism is restraining the market.

Current management relies heavily on off-label use of medications originally developed for other endocrine or dermatologic conditions. Patients frequently encounter inconsistent responses due to variable hormonal profiles and individual tolerability. The restraint complicates standardized treatment protocols across clinical settings. Providers must navigate insurance coverage limitations for non-approved indications.

The factor contributes to delayed initiation of effective regimens in many cases. Long-term adherence suffers from side-effect profiles not optimized for cosmetic hair reduction. The dynamic limits investment in specialized formulation development.

Practices face challenges educating patients on realistic expectations without dedicated product labeling. This constraint slows overall therapeutic innovation tailored to hirsutism pathophysiology. The limitation persists in restricting widespread access to optimized solutions.

Opportunities

Emergence of targeted androgen-suppressing agents for underlying conditions is creating growth opportunities.

Novel therapies addressing excessive androgen production offer potential for more precise symptom control with fewer systemic effects. These agents support combination regimens that enhance cosmetic outcomes while treating root hormonal imbalances. Opportunities arise for integrated care models combining endocrinology and dermatology expertise.

The framework enables development of personalized protocols based on individual biomarker profiles. Developers can pursue expanded indications through well-designed clinical programs. The approach facilitates improved patient satisfaction and adherence metrics. Such advancements attract collaboration between pharmaceutical and device manufacturers.

The opportunity fosters differentiation through superior risk-benefit profiles. Stakeholders anticipate broader reimbursement discussions as evidence accumulates. This progression positions the sector for enhanced therapeutic relevance in hormonal hair disorders.

Impact of Macroeconomic / Geopolitical Factors

The hirsutism market responds closely to economic conditions as patients weigh spending on dermatology consultations, hormonal therapies, and cosmetic treatments. Rising living costs make many consumers delay elective procedures such as laser hair removal and premium prescription therapies. Higher financing costs also limit expansion of aesthetic clinics that offer advanced treatment options.

Geopolitical uncertainty affects the supply of pharmaceutical ingredients, laser components, and dermatology devices, which creates cost variability for providers. Current US tariffs on imported medical devices, cosmetic equipment, and certain pharmaceutical inputs increase treatment costs and reduce pricing flexibility for clinics.

These pressures can slow treatment adoption in cost-sensitive populations and emerging care settings. At the same time, providers focus on affordable treatment packages and localized sourcing strategies to maintain accessibility. Growing awareness of hormonal health conditions and rising demand for effective long-term solutions continue to support steady and positive market growth.

Latest Trends

FDA approval of crinecerfont for congenital adrenal hyperplasia is driving the market.

The U.S. Food and Drug Administration approved crinecerfont as adjunctive treatment to glucocorticoid replacement for control of androgens in adults and pediatric patients four years and older with congenital adrenal hyperplasia. This 2025 authorization targets excessive androgen production that commonly manifests as hirsutism in affected females.

The approval provides a new mechanism for modulating adrenal steroidogenesis without increasing glucocorticoid doses. Clinicians gain an option to address hyperandrogenism symptoms including excessive hair growth in CAH populations. The development aligns with efforts to improve long-term outcomes in rare endocrine disorders.

Facilities benefit from reduced reliance on high-dose steroids associated with additional side effects. The milestone stimulates multidisciplinary management approaches for patients presenting with hirsutism secondary to CAH. Early post-approval experience demonstrates potential for better symptom control. Overall, this regulatory advancement expands targeted treatment avenues for androgen-driven hair excess conditions.

Regional Analysis

North America is leading the Hirsutism Market

North America accounted for 42.5% of the hirsutism market in 2025 as dermatology clinics, endocrinology centers, and aesthetic treatment providers expanded diagnosis and treatment services for hormone-related hair growth disorders. Rising awareness of endocrine conditions such as polycystic ovary syndrome has encouraged more women to seek medical evaluation and treatment for excess hair growth.

According to the National Institutes of Health, polycystic ovary syndrome affects about 6% to 12% of women of reproductive age in the United States, creating a substantial patient population that often requires long-term hormonal and dermatological management.

Increasing availability of laser hair removal, topical treatments, and anti-androgen therapies has improved treatment accessibility and outcomes. Healthcare providers are integrating hormonal assessment with dermatological care to deliver more personalized treatment approaches. Growth in medical aesthetics and cosmetic dermatology clinics has also contributed to higher treatment uptake.

Pharmaceutical companies are expanding research in hormonal therapies that target underlying endocrine imbalances. Digital health platforms and teledermatology services are improving access to consultation and follow-up care. These developments collectively supported steady expansion of treatment solutions across North America in 2025.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is expected to experience strong growth during the forecast period as awareness of hormonal disorders and access to dermatological care increase across the region. Countries such as China, India, Japan, and South Korea are witnessing rising diagnosis of endocrine disorders linked to lifestyle changes, obesity, and urbanization.

The World Health Organization reported in 2022 that obesity rates have nearly tripled globally since 1975, contributing to increased prevalence of hormonal imbalances that can lead to excess hair growth conditions. Healthcare providers across the region are expanding endocrinology and dermatology services to address these conditions more effectively.

Growing middle-class income and increasing demand for aesthetic treatments are encouraging individuals to seek professional medical and cosmetic solutions. Clinics are adopting advanced laser technologies and combination therapies that improve treatment outcomes. Governments are strengthening women’s health programs that promote early diagnosis of endocrine disorders.

Pharmaceutical companies are expanding access to hormonal treatment options across emerging markets. These developments are expected to accelerate adoption of clinical and aesthetic treatment solutions across Asia Pacific in the coming years.

Key Regions and Countries

North America

- The US

- Canada

Europe

- Germany

- France

- The U.K.

- Italy

- Spain

- Russia & CIS

- Rest of Europe

Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia & New Zealand

- Rest of Asia Pacific

Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Latin America

- Brazil

- Mexico

- Rest of Latin America

Key Players Analysis

Key participants in the Hirsutism market expand growth by advancing hormonal therapies, strengthening dermatology partnerships, and developing targeted treatment solutions that address underlying endocrine disorders such as polycystic ovary syndrome. Companies invest in clinical research to improve efficacy of anti-androgen drugs and topical treatments while also expanding awareness programs that encourage early diagnosis and treatment adoption.

They collaborate with healthcare providers and aesthetic clinics to integrate medical and cosmetic approaches, including laser hair reduction and prescription therapies. Allergan Aesthetics, a division of AbbVie, represents a notable participant in the Hirsutism market and operates as a global pharmaceutical and aesthetics company headquartered in the United States that develops medical treatments and aesthetic solutions across dermatology and endocrinology segments.

The company focuses on innovative therapies and physician engagement programs to support patient-centric care. Industry competitors continue to expand product pipelines, strengthen clinical collaborations, and invest in advanced treatment modalities to improve long-term management outcomes.

Top Key Players

- Alma Lasers Ltd.

- Alpaya Dermaceuticals

- Cynosure Inc. (now Cynosure Lutronic)

- Lumenis Inc.

- Koninklijke Philips N.V.

- Merck & Co., Inc.

- Pfizer Inc.

- Cutera Inc.

Recent Developments

- In February 2026, Cynosure Lutronic secured regulatory approvals in both China and Japan for its Clarity II dual-wavelength laser system. The platform is designed for long-term hair reduction and supports treatment across a wide range of skin types by enabling precise energy delivery through combined wavelength technology.

- At the ASLMS 2025 conference in April, Lumenis presented updated clinical findings for its SPLENDOR X system. The device utilizes a dual-wavelength emission approach that allows practitioners to customize treatments for hirsutism across different skin tones, improving safety profiles and treatment consistency over extended use.

Report Scope

Report Features Description Market Value (2025) US$ 3.7 Billion Forecast Revenue (2035) US$ 7.6 Billion CAGR (2026-2035) 7.5% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Treatment Type (Pharmacological Therapy (Oral Contraceptives, Anti-androgens and Insulin Sensitizers), Cosmetic Procedures (Laser Hair Removal and IPL) and Mechanical and Physical Methods (Electrolysis, Waxing and Shaving)), By Application (Upper Lip, Chin, Chest, Arms and Others (Back, Abdomen, Thighs)), By End User (Hospitals, Dermatology Clinics, Cosmetic Centers, Home Care Settings and Others) Regional Analysis North America – The US, Canada; Europe – Germany, France, The U.K., Italy, Spain, Russia & CIS, Rest of Europe; Asia Pacific – China, India, Japan, South Korea, ASEAN, Australia & New Zealand, Rest of Asia Pacific; Middle East & Africa – GCC, South Africa, Rest of Middle East & Africa; Latin America – Brazil, Mexico, Rest of Latin America Competitive Landscape Alma Lasers Ltd., Alpaya Dermaceuticals, Cynosure Inc., Lumenis Inc., Koninklijke Philips N.V., Merck & Co., Inc., Pfizer Inc., Cutera Inc. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- Alma Lasers Ltd.

- Alpaya Dermaceuticals

- Cynosure Inc. (now Cynosure Lutronic)

- Lumenis Inc.

- Koninklijke Philips N.V.

- Merck & Co., Inc.

- Pfizer Inc.

- Cutera Inc.

Our Clients

- 182166

- March 2026