Global Synthetic Lubricants Market Size, Share, And Enhanced Productivity By Product (PAO, Esters, PAG), By Application (Engine Oil, Heat Transfer Fluids (HTFs), Transmission Fluids, Metalworking Fluids, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, and Forecast 2026-2035

- Published date: March 2026

- Report ID: 180044

- Number of Pages: 211

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

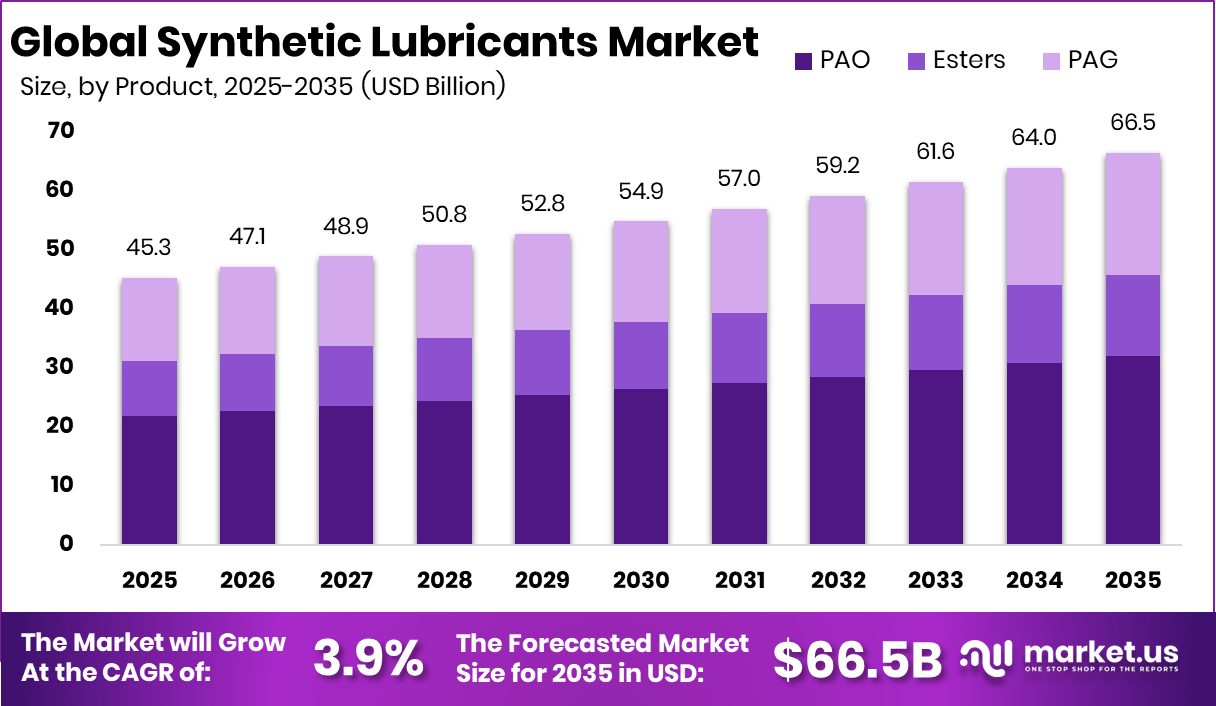

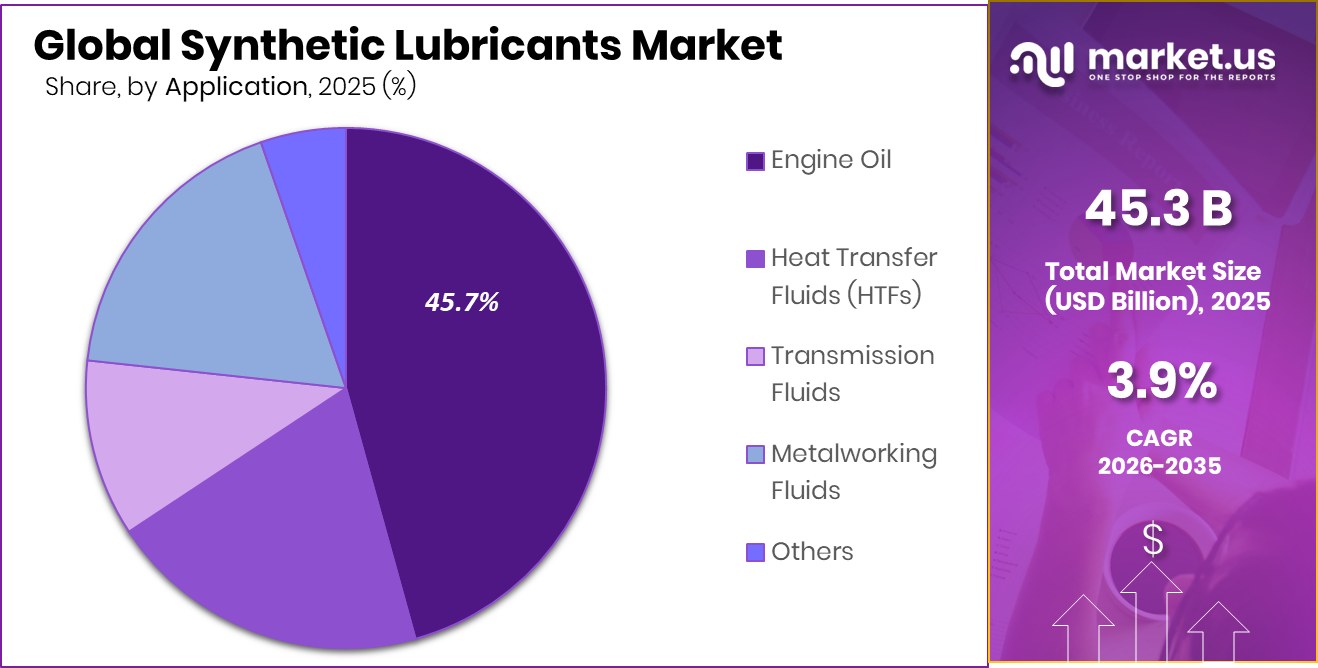

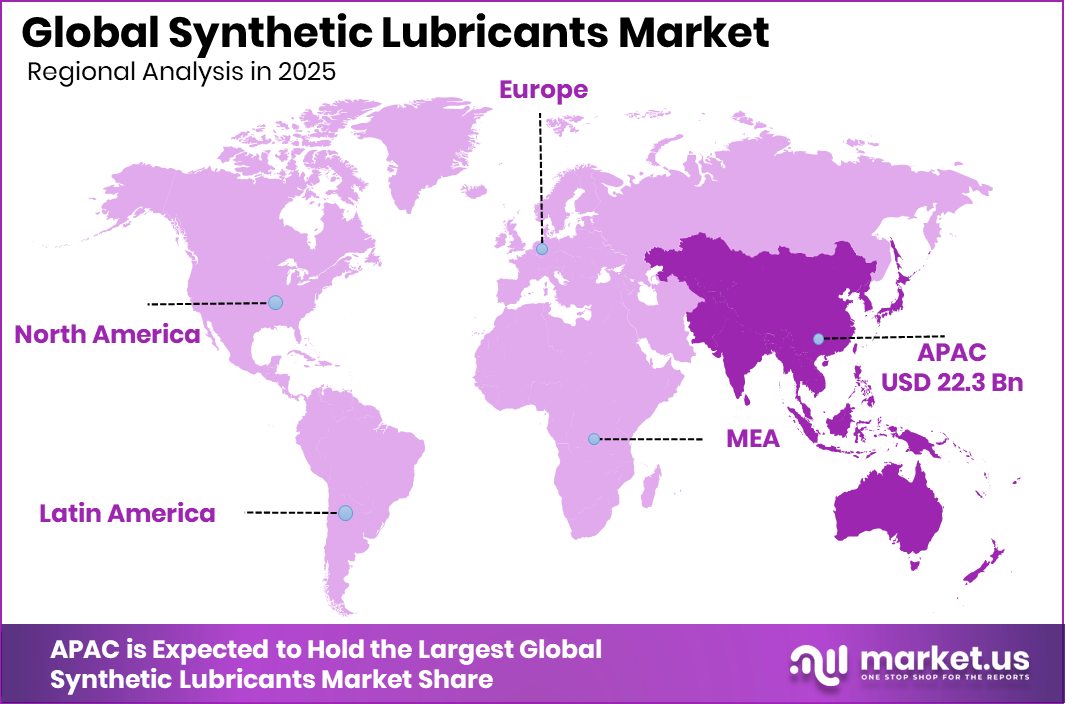

The Global Synthetic Lubricants Market is expected to be worth around USD 66.5 billion by 2035, up from USD 45.3 billion in 2025, and is projected to grow at a CAGR of 3.9% from 2026 to 2035. Region Asia Pacific dominates at 49.3%, worth USD 22.3 Bn today.

The Global Synthetic Lubricants Market is shaped by its key product categories—PAO, esters, and PAG—and their use across engine oil, heat transfer fluids, transmission fluids, metalworking fluids, and other critical industrial systems. These lubricants are engineered fluids made through controlled chemical processes rather than crude-based refining, giving them higher purity and performance. They are widely used in machinery, vehicles, and thermal systems that require stability under extreme temperatures, cleaner operation, and longer service intervals. As industries modernize and equipment loads increase, synthetic lubricants continue to replace conventional oils in both automotive and industrial environments.

Synthetic lubricants are high-performance fluids created to provide better thermal resistance, reduced oxidation, smoother operation, and longer equipment life. Their market refers to the global demand, production, and use of these engineered oils across industries that depend on reliable lubrication for engines, transmissions, industrial machinery, and heat-intensive processes. The market expands as more sectors adopt advanced fluids to reduce downtime and improve operating efficiency.

Growth in this market is supported by cleaner energy initiatives, such as Greece approving €111.7 million in EU funding for Motor Oil’s green hydrogen plant, which encourages industries to rely on more efficient lubricants. Market demand also benefits from rising transportation electrification, highlighted by 80% funding for E-fleet bus locations, increasing the need for specialized fluids.

Opportunities emerge as advanced engine and power technologies evolve, reflected in calls like Rolls-Royce urging the UK to support a £3 billion engine project, and further reinforced by €111.7 million granted for a 50MW hydrogen project at a Greek refinery, all signaling deeper industrial investment that ultimately drives wider adoption of synthetic lubricants.

Key Takeaways

- The Global Synthetic Lubricants Market is expected to be worth around USD 66.5 billion by 2035, up from USD 45.3 billion in 2025, and is projected to grow at a CAGR of 3.9% from 2026 to 2035.

- Synthetic Lubricants Market sees PAO leading with 48.1% share, driven by superior thermal stability.

- Engine oil segment holds 45.7% share in the Synthetic Lubricants Market due to rising vehicle maintenance.

- Synthetic Lubricants Market in Asia Pacific hits USD 22.3 Bn with 49.3%.

By Product Analysis

Synthetic Lubricants Market sees PAO dominate with a strong 48.1% share.

In 2025, the Synthetic Lubricants Market continues to strengthen as industries push for cleaner, longer-lasting, and high-performance lubrication solutions across automotive, manufacturing, and energy sectors. Polyalphaolefin (PAO) remains the leading product category with a 48.1% share, driven by its stability, oxidation resistance, and suitability for extreme temperatures. Companies and fleet operators are increasingly shifting to synthetic oils to reduce maintenance downtime and improve equipment reliability.

Growing urban mobility, expanding logistics, and rising premium vehicle sales are further supporting steady adoption rates. At the same time, regulatory pressure for lower emissions and better fuel economy is encouraging OEMs to endorse synthetic-grade lubricants. This combination of technology, efficiency expectations, and environmental alignment keeps PAO-based formulations firmly at the forefront.

By Application Analysis

Engine oil holds 45.7% share within the expanding Synthetic Lubricants Market globally.

In 2025, the Synthetic Lubricants Market sees strong momentum in application demand, with engine oil holding a 45.7% share, reflecting its essential role in both conventional and modern powertrains. The shift toward high-performance engines, turbocharged systems, and longer oil-change intervals is reinforcing the need for synthetic blends that can withstand heat, reduce wear, and maintain viscosity stability.

Commercial fleets, passenger cars, and heavy-duty equipment operators are adopting synthetics to minimize operational costs and extend engine life. Rising consumer awareness about cleaner lubrication choices and the push for reduced carbon footprints also contribute to consistent demand growth. As hybrid and advanced combustion engines expand globally, synthetic engine oils continue to anchor the market as the most trusted and widely used application segment.

Key Market Segments

By Product

- PAO

- Esters

- PAG

By Application

- Engine Oil

- Heat Transfer Fluids (HTFs)

- Transmission Fluids

- Metalworking Fluids

- Others

Driving Factors

Rising equipment efficiency needs boost demand

Rising equipment efficiency needs boost demand across manufacturing, automotive, and heavy engineering, creating a steady push toward higher-grade synthetic lubricants that can handle greater thermal loads and longer operating cycles. Industries aiming to reduce downtime are shifting away from conventional oils and choosing engineered fluids that maintain stability under stress.

However, broader energy sector developments also shape lubricant consumption patterns, such as the setback faced by the Sea Lion initiative after financing delays affected the $1.4 billion Falkland Islands oil project. These disruptions highlight how large-scale upstream investments influence downstream product demand, including synthetic lubricants used in drilling equipment, power systems, and support machinery that rely on consistent, high-performance lubrication.

Restraining Factors

Higher synthetic oil prices limit adoption

Higher synthetic oil prices limit adoption among cost-sensitive users, particularly in regions where conventional lubricants remain widely available and more affordable for routine maintenance. Small operators and budget-restricted industries often defer upgrades to synthetic options even when performance benefits are clear.

External financial influences also shape market restraints, illustrated by reports showing oil interests contributing over $75 million to Trump PACs, a reminder of how political and economic decisions can redirect investment priorities. Such funding patterns may slow modernization efforts in some sectors, delaying transitions toward advanced lubricants as industries reassess spending and operational costs.

Growth Opportunity

Industrial automation increases advanced lubricant usage

Industrial automation increases advanced lubricant usage as factories adopt more robotics, precision machinery, and high-speed systems requiring stable, long-life fluids. Synthetic lubricants support efficient operations by reducing friction and extending component life, creating an opening for broader adoption across automated production lines.

Opportunity expansion is also reflected in innovation-driven investments, such as GrainCorp’s VC arm backing a synthetic palm oil startup with a $1.2 million pre-Seed round. Although unrelated to petroleum-based lubricants, this funding highlights the rising interest in engineered alternatives, biotechnology, and performance-focused fluids—an environment that indirectly supports growth for synthetic lubricant manufacturers developing next-generation formulations.

Latest Trends

Shift toward low-emission synthetic formulations

A shift toward low-emission synthetic formulations is becoming more visible as industries align with cleaner operational standards and environmental expectations. Companies are prioritizing lubricants that reduce carbon footprints, offer improved oxidation resistance, and support longer drain intervals. This trend mirrors broader financial movements within the energy ecosystem, including Golden Oil Funding SPV seeking ₦5 billion through an asset-backed commercial paper, signaling ongoing capital flows into oil-related ventures.

Such funding activity showcases the continued relevance of lubricant-dependent industries, where high-performance synthetic solutions play a role in improving equipment reliability and operating efficiencies as markets transition toward more sustainable practices.

Regional Analysis

Asia Pacific holds 49.3% market share, reaching USD 22.3 Bn value.

The Synthetic Lubricants Market shows varied performance across major regions, reflecting differences in industrial strength, vehicle ownership, and manufacturing activity. Asia Pacific remains the dominant region with 46.5% and USD 1.8 Bn, supported by strong automotive production, expanding industrial output, and rising equipment servicing needs in countries across the region.

North America continues to demonstrate steady demand for premium-grade synthetic oils, driven by a mature automotive sector and consistent usage across commercial fleets. Europe maintains stable adoption levels as manufacturers emphasize efficiency and adherence to stringent lubrication standards. Meanwhile, the Middle East & Africa region benefits from ongoing industrial operations and growing machinery usage, contributing to a gradual rise in synthetic lubricant consumption.

Latin America shows moderate but reliable demand as automotive maintenance services expand and industrial facilities increasingly shift toward higher-performance synthetic formulations. Across all regions, Asia Pacific clearly leads the market, accounting for the largest share and value contribution among global segments.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

In 2025, BP Lubricants Pvt. Ltd. continues to strengthen its position by focusing on advanced synthetic formulations designed for reliable performance across modern automotive and industrial systems. The company’s broad portfolio supports customers looking for cleaner, longer-drain oils, especially in regions where rising vehicle ownership and equipment usage demand higher-grade lubrication. Its emphasis on efficiency, durability, and better thermal stability allows BP Lubricants to appeal to both fleet operators and individual consumers seeking consistent output under varying operating conditions.

Chevron Corporation maintains a strong global footprint in synthetic lubricants through its focus on technology-driven blends engineered for heavy-duty engines, high-temperature operations, and long service intervals. The company leverages extensive refining and additive expertise to deliver synthetic oils that support engine cleanliness and reduce wear. Chevron’s continued investment in performance-oriented formulations positions it as a key supplier for markets prioritizing operational reliability, including transportation, industrial machinery, and energy-driven sectors that rely on stable lubrication under tough conditions.

LANXESS plays a strategic role in the value chain with its specialty chemical capabilities supporting the development of high-quality synthetic lubricant components. Its focus on additives that enhance oxidation stability, viscosity behavior, and material compatibility reinforces its importance to lubricant manufacturers worldwide. In 2025, LANXESS benefits from rising demand for premium synthetic oils requiring tailored chemical performance, making the company a critical contributor to the technological progression of next-generation lubricants.

Top Key Players in the Market

- BP Lubricants Pvt. Ltd.

- Chevron Corporation

- LANXESS

- Valvoline

- FUCHS

- Pennzoil

- Phillips 66 Company

- Motul

- AMSOIL INC.

- Agip

Recent Developments

- In December 2025, global parent BP agreed to sell a 65% stake in its Castrol lubricants business to Stonepeak for about USD 10.1 billion, while retaining a 35% minority interest as part of a new joint venture. This transaction affects the wider lubricants network and global supply landscape.

- In July 2025, Chevron completed its acquisition of Hess Corporation, bringing new oil and gas assets into the company and expanding its global portfolio. This large merger strengthens Chevron’s overall production, which indirectly supports its lubricant and fuel businesses by increasing the base oil and product supply it can offer.

Report Scope

Report Features Description Market Value (2025) USD 45.3 Billion Forecast Revenue (2035) USD 66.5 Billion CAGR (2026-2035) 3.9% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product (PAO, Esters, PAG), By Application (Engine Oil, Heat Transfer Fluids (HTFs), Transmission Fluids, Metalworking Fluids, Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA Competitive Landscape BP Lubricants Pvt. Ltd., Chevron Corporation, LANXESS, Valvoline, FUCHS, Pennzoil, Phillips 66 Company, Motul, AMSOIL INC., Agip Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Synthetic Lubricants MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample

Synthetic Lubricants MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- BP Lubricants Pvt. Ltd.

- Chevron Corporation

- LANXESS

- Valvoline

- FUCHS

- Pennzoil

- Phillips 66 Company

- Motul

- AMSOIL INC.

- Agip

Our Clients

- 180044

- March 2026