Global Sulfur Hexafluoride Market Size, Share and Report Analysis By Product (Electronic Grade, UHP Grade, Standard Grade), By Application (Power And Energy, Medical, Metal Manufacturing, Electronics, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2025-2035

- Published date: Mar 2026

- Report ID: 179933

- Number of Pages: 269

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

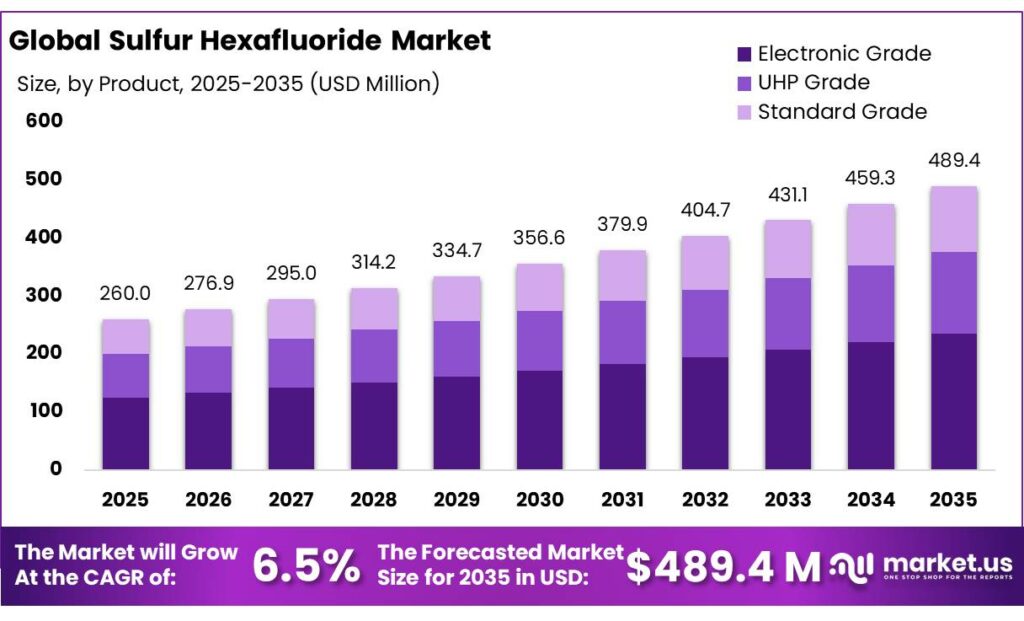

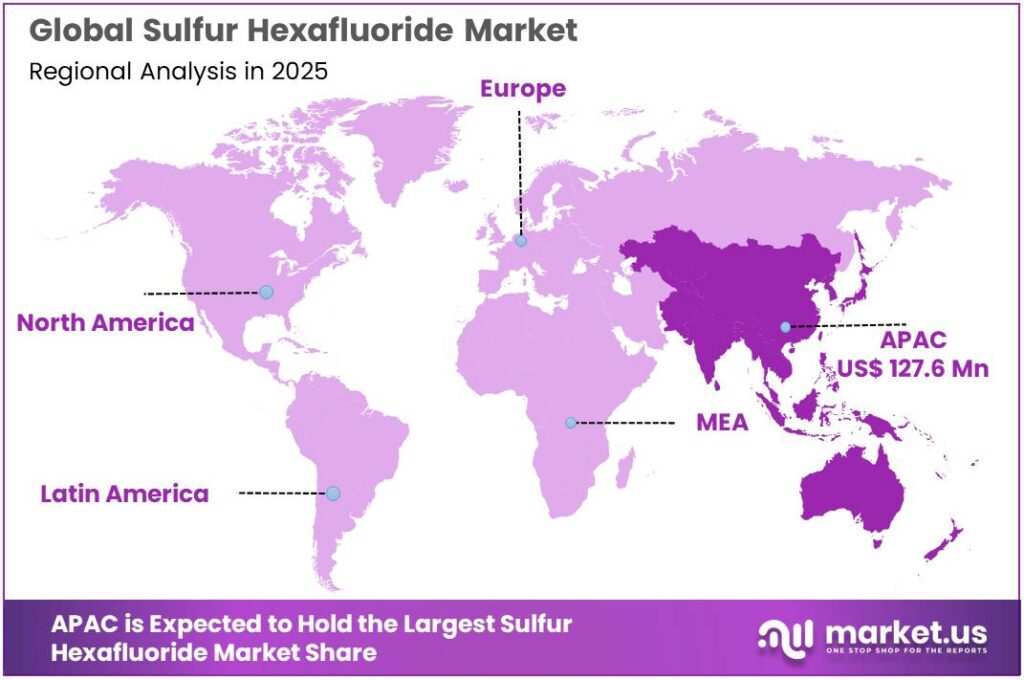

The Global Sulfur Hexafluoride Market is expected to be worth around USD 489.4 Million by 2035, up from USD 260.0 Million in 2025, at a CAGR of 6.5% from 2026 to 2035. The Asia Pacific segment maintained 49.1%, supporting a Sulfur Hexafluoride value of USD 127.6 Mn.

Sulfur hexafluoride (SF₆) is a synthetic, odorless, non-flammable gas best known as a high-performance electrical insulator. Its exceptional dielectric strength and arc-quenching capability have made it the benchmark gas for high- and medium-voltage switchgear, circuit breakers, gas-insulated substations (GIS), and transmission lines. However, SF₆ also has an extremely high climate impact: the latest IPCC values compiled by the Greenhouse Gas Protocol put its 100-year global warming potential at 24,300 times that of CO₂.

- In the European Union, Regulation (EU) 2024/573 over fluorinated greenhouse gases introduces binding phase-out dates for new SF₆-filled medium-voltage switchgear, with ratings up to and including 24 kV banned from January 2026, and units above 24 kV up to 52 kV restricted from January 2030, provided SF₆-free alternatives are available.

The demand side for SF₆ is tied directly to the “Age of Electricity”. The International Energy Agency (IEA) expects global electricity consumption to have grown by about 4.3% in 2024 and to continue rising at an average 3.9% annually through 2027, driven by electrification, data centres, EVs and cooling. In developing Asia alone, almost 1 billion people have gained access to electricity since 2010, with access rising from 79% to 97% by 2023, implying substantial investment in high-voltage networks that historically rely on SF₆-based GIS.

Regulation is now re-defining the long-term outlook. The European Union’s revised F-Gas framework (Regulation (EU) 2024/573) introduces binding phase-out dates for new SF₆-filled medium-voltage switchgear, with bans for certain equipment classes starting from January 2026.

- The European Commission aimed at a 90% reduction in overall F-gas usage by 2050, and forbade the use of gases with a GWP above 10 in most new switchgear from 2026–2031, depending on voltage level. In parallel, several U.S. state-level programs cap SF₆ emission rates from electric utilities at 1% of nameplate capacity and progressively restrict purchases of new SF₆ equipment after 2025.

Key Takeaways

- Sulfur Hexafluoride Market is expected to be worth around USD 489.4 Million by 2035, up from USD 260.0 Million in 2025, at a CAGR of 6.5%.

- Electronic Grade held a dominant market position, capturing more than a 48.3% share.

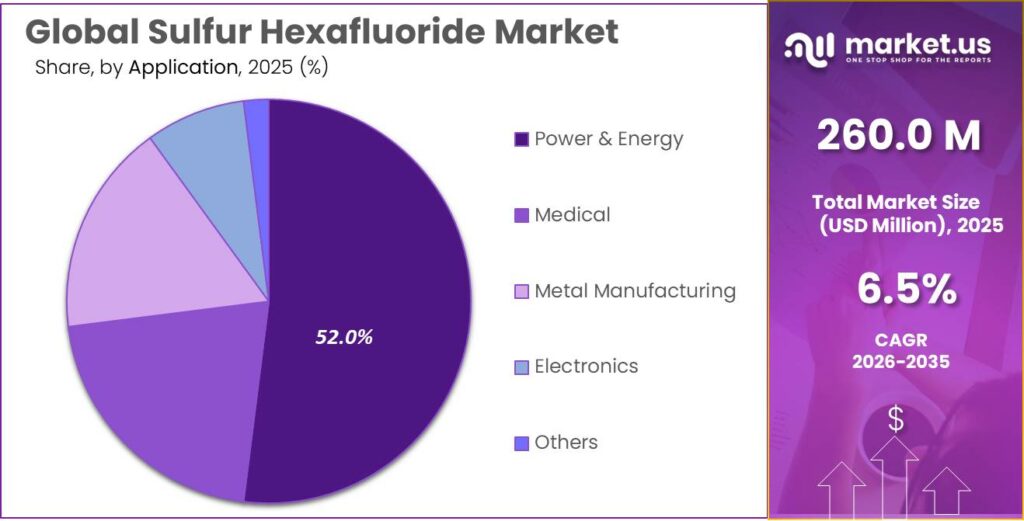

- Power & Energy held a dominant market position, capturing more than a 52.8% share.

- Asia Pacific held a dominant position in the sulfur hexafluoride market, accounting for 49.1% of global revenue, or about USD 127.6 million.

By Product Analysis

Electronic Grade SF₆ leads the market with a strong 48.3% share in 2024

In 2024, Electronic Grade held a dominant market position, capturing more than a 48.3% share, driven largely by the rapid expansion of semiconductor manufacturing and high-precision electronic components. As chipmakers continued scaling production for advanced nodes, the demand for ultra-pure SF₆ increased noticeably because it is essential for plasma etching, chamber cleaning, and high-voltage insulation inside sensitive fabrication equipment.

This rise was particularly visible across Asia, where new fabs announced in 2024 led to higher procurement of high-purity gases to meet stricter etching and deposition quality standards. The segment’s performance in 2024 also reflected stronger investments from global electronics firms upgrading clean-room infrastructure to meet next-generation chip requirements.

By Application Analysis

Power & Energy dominates with a solid 52.8% share in 2024

In 2024, Power & Energy held a dominant market position, capturing more than a 52.8% share, mainly because sulfur hexafluoride remains one of the most reliable insulating gases for high-voltage transmission and distribution systems. Utilities across developing and developed regions continued upgrading substations, circuit breakers, and GIS units, and these upgrades naturally increased the use of SF₆ due to its strong dielectric strength and long service life.

The push to stabilize grids, integrate more renewable power, and strengthen cross-country transmission lines further supported demand in 2024, as electrical networks required durable insulation solutions that could handle high loads and fluctuating power conditions.

Key Market Segments

By Product

- Electronic Grade

- UHP Grade

- Standard Grade

By Application

- Power & Energy

- Medical

- Metal Manufacturing

- Electronics

- Others

Emerging Trends

Power grids are moving toward SF₆-free, climate-smart equipment around food and cold-chain hubs

One of the strongest recent trends around sulfur hexafluoride is a steady move away from “business as usual” toward SF₆-free or ultra-low-leak switchgear, especially in the places where electricity demand is growing fastest: food processing zones, logistics hubs, and cold-chain infrastructure. This shift is not only about power engineering; it is driven by climate goals that now put agrifood systems under the spotlight.

- The Food and Agriculture Organization (FAO) estimates that global agrifood systems emitted 16.2 billion tonnes of CO₂-equivalent in 2022, roughly one-third of all human-made greenhouse gas emissions worldwide.

Cold chains are a good example of why this matters. A joint UNEP–FAO assessment shows that 526 million tonnes of food production are lost every year because of poor or missing refrigeration, equal to about 12% of global food output, enough to feed around 1 billion people. At the same time, only about 45% of the food that needs refrigeration actually gets it in practice.

What is changing is the type of switchgear being ordered. Regulators, especially in Europe and some US states, are tightening the rules on SF₆ because of its very high global warming potential.

- The European Union’s new F-gas Regulation (EU 2024/573) sets binding phase-out dates for SF₆ in medium-voltage switchgear: new equipment up to 24 kV can no longer use SF₆ from 1 January 2026, and units from >24 kV up to 52 kV face bans from 2030.

Drivers

Rising power demand for food systems is a key driver for sulfur hexafluoride

One major driving factor for sulfur hexafluoride (SF₆) is the rapidly growing need for reliable electricity to run modern agrifood systems and cold chains. Around the world, food does not move from farm to plate without a lot of energy. The Food and Agriculture Organization (FAO) estimates that producing the world’s food and getting it from “farm to fork” uses about 30% of global energy consumption and contributes roughly 31% of global greenhouse gas emissions. This energy is not only used on the farm.

Cold chains give a very concrete picture of this link. A joint assessment by UNEP and FAO reports that a lack of effective refrigeration leads to the loss of about 526 million tonnes of food production each year, equal to around 12% of the global total. According to the same sources, that lost food could feed roughly 1 billion people in a world where hundreds of millions are still hungry.

- The International Energy Agency notes that global electricity demand rose by about 4.3% in 2024, and is expected to continue growing at close to 4% per year through 2027, driven by electrification, air conditioning, industry and digital infrastructure. A mid-year update from the IEA projects electricity demand growth of roughly 3.3% in 2025 and 3.7% in 2026, still among the fastest rates seen in the last decade.

Restraints

Environmental impact and strict greenhouse gas regulations limit sulfur hexafluoride use

One of the biggest restraining factors for sulfur hexafluoride (SF₆) in industry today is its exceptionally high global warming impact and the resulting push from governments and regulators to reduce or phase out its use wherever possible. SF₆ is not just another industrial gas; it is one of the most powerful greenhouse gases ever identified.

- According to the U.S. Environmental Protection Agency, SF₆ has a global warming potential (GWP) 23,500 times greater than carbon dioxide over 100 years and remains in the atmosphere for more than a thousand years if released, contributing to long-term climate change.

This environmental reality has made SF₆ the focus of increasing regulatory scrutiny around the world. Governments in the European Union have adopted new F-Gas regulations that plan to phase out SF₆ in new electrical installations by around 2032, while also mandating leak minimisation, strict reporting of procurement and emissions, and certification for technicians who handle the gas. These kinds of policies are designed to limit the future use of SF₆ significantly, because even small releases have a disproportionately large impact on the climate.

The restraining effect of these environmental regulations is compounded by the growing awareness of climate change in sectors that indirectly rely on electricity. The Food and Agriculture Organization (FAO) estimates that about 30% of global energy used in food systems occurs after the farm gate, in these energy-dependent stages of the agrifood value chain.

Opportunity

Expanding clean power and cold chains opens real growth space for SF₆

One clear growth opportunity for sulfur hexafluoride lies in the massive build-out of reliable, modern electricity networks for food systems and cold chains, especially in emerging economies. Agrifood systems today are a major part of the climate and energy story. FAO estimates that agrifood systems account for about one-third of total human-made greenhouse gas emissions, with 16.2 billion tonnes of CO₂-equivalent emitted in 2022 alone.

Cold chains show how this becomes a practical opportunity. A joint UNEP–FAO technical brief finds that lack of effective refrigeration leads to the loss of about 526 million tonnes of food production each year, roughly 12% of global food output – enough to feed an estimated 1 billion people. That kind of loss is no longer seen as acceptable in a world where more than 3 billion people cannot afford a healthy diet.

Electricity demand trends add another layer to this opportunity. The International Energy Agency reports that global electricity consumption rose by about 4.3% in 2024, with demand expected to keep growing at roughly 3.9% per year on average between 2025 and 2027.

The IEA analysis suggests electricity use will increase by 3.3% in 2025 and 3.7% in 2026, more than twice as fast as overall energy demand. A lot of that growth will be in regions where food demand, urbanisation and industrialisation are rising together. At the same time, a World Bank background paper highlights that around 732 million people in rural areas still lacked access to electricity in 2017, many of them in South Asia and Sub-Saharan Africa.

Regional Insights

Asia Pacific leads sulfur hexafluoride demand with a 49.1% share in 2024

In 2024, Asia Pacific held a dominant position in the sulfur hexafluoride market, accounting for 49.1% of global revenue, or about USD 127.6 million, underpinned by rapid grid expansion and strong industrial activity across China, India, Japan, South Korea and Southeast Asia. The region’s power sector is expanding quickly as governments work to secure reliable electricity for fast-growing cities, data centres, transport and food systems.

The International Energy Agency (IEA) notes that almost 1 billion people in developing Asia gained access to electricity between 2010 and 2023, lifting regional access from 79% to 97% and driving a massive build-out of transmission and distribution infrastructure where SF₆-insulated switchgear is widely used.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Fujian Shaowu Yongfei is a leading Chinese sulfur hexafluoride producer, operating modern gas-manufacturing lines with annual output capacities exceeding 8,000–10,000 tonnes across its facilities. Serving domestic switchgear manufacturers and export clients in Asia, Middle East and Europe, the company ensures SF₆ purity levels above 99.95%. Its strong regional distribution network and participation in China’s expanding high-voltage grid projects support steady demand. With continued investment in gas-recycling and emission-control technologies, the company maintains relevance in both domestic and international markets.

Solvay is a major specialty-chemicals producer offering high-purity sulfur hexafluoride for electrical, semiconductor and aerospace applications. Operating in 60+ countries with revenue around EUR 5–6 billion, the company maintains strong R&D capabilities and advanced purification infrastructure. Solvay manages multiple specialty-gas units and operates 20+ innovation centers, ensuring strict quality control and regulatory alignment. Its technical support and supply reliability make it a preferred vendor for industries requiring stable dielectric-grade SF₆, particularly in high-voltage switchgear manufacturing and engineered industrial solutions.

Advanced Specialty Gases focuses on high-purity electronic and industrial gases, including sulfur hexafluoride for semiconductor and high-voltage applications. The company operates advanced purification systems delivering gas purity above 99.99%, catering to microelectronics and precision industries. With distribution networks across multiple U.S. states and supply volumes reaching several hundred metric tons annually, the company provides stable SF₆ availability. Its emphasis on specialty-gas customisation and long-term technical partnerships reinforces its role as a trusted supplier in high-performance industrial environments.

Top Key Players Outlook

- Linde Group

- Solvay

- Concorde Specialty Gases

- Advanced Specialty Gases

- Fujian Shaowu Yongfei

- Showa Denko

- Huaneng Fluorin

- Kanto Denka Kogyo

- Matheson

- Qinghai Xinhe

Recent Industry Developments

In 2024, Linde generated about USD 33 billion in sales and remained the world’s largest industrial gas supplier, reaching operations in over 100 countries with more than 65,000 employees working across atmospheric, specialty and process gases.

By 2025, Solvay reported underlying net sales of around €4,300 million and an underlying EBITDA of €881 million, reflecting a resilient performance amid market shifts.

Report Scope

Report Features Description Market Value (2025) USD 260.0 Mn Forecast Revenue (2035) USD 489.4 Mn CAGR (2026-2035) 6.5% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product (Electronic Grade, UHP Grade, Standard Grade), By Application (Power And Energy, Medical, Metal Manufacturing, Electronics, Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA Competitive Landscape Linde Group, Solvay, Concorde Specialty Gases, Advanced Specialty Gases, Fujian Shaowu Yongfei, Showa Denko, Huaneng Fluorin, Kanto Denka Kogyo, Matheson, Qinghai Xinhe Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- Linde Group

- Solvay

- Concorde Specialty Gases

- Advanced Specialty Gases

- Fujian Shaowu Yongfei

- Showa Denko

- Huaneng Fluorin

- Kanto Denka Kogyo

- Matheson

- Qinghai Xinhe

Our Clients

- 179933

- Mar 2026