Global Parmesan Cheese Market Size, Share, And Enhanced Productivity By Source (Animal-based, Plant-based), By Type (Conventional, Organic), By Form (Block, Powdered, Shredded, Grated, Others), By Product (Domestic Parmesan, Parmesan-Style Cheese (Non-PDO), PDO Parmigiano Reggiano), By Rennet Type (Animal Rennet, Microbial/Vegetarian Rennet), By Distribution Channel (Supermarkets/Hypermarkets, Specialty Stores, Convenience Stores, Online Retail, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, and Forecast 2025-2034

- Published date: December 2025

- Report ID: 168993

- Number of Pages: 272

- Format:

-

keyboard_arrow_up

Quick Navigation

- Report Overview

- Key Takeaways

- By Source Analysis

- By Type Analysis

- By Form Analysis

- By Product Analysis

- By Rennet Type Analysis

- By Distribution Channel Analysis

- Key Market Segments

- Driving Factors

- Restraining Factors

- Growth Opportunity

- Latest Trends

- Regional Analysis

- Key Players Analysis

- Recent Developments

- Report Scope

Report Overview

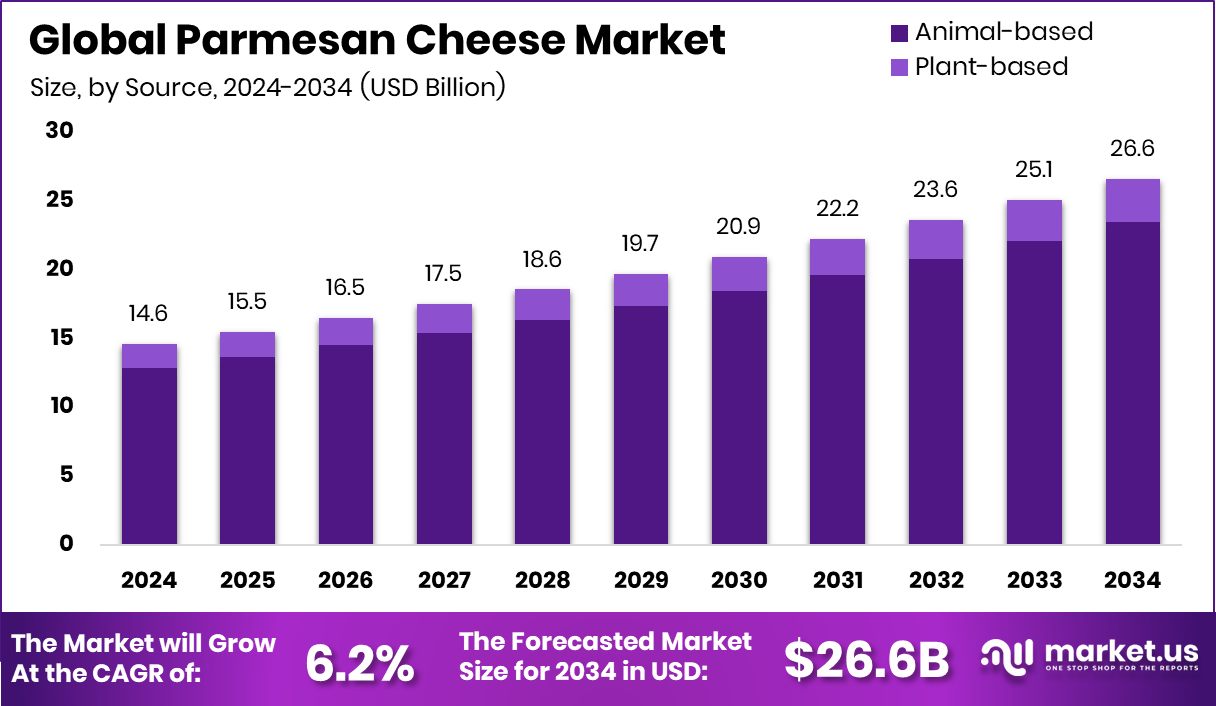

The Global Parmesan Cheese Market is expected to be worth around USD 26.6 billion by 2034, up from USD 14.6 billion in 2024, and is projected to grow at a CAGR of 6.2% from 2025 to 2034. Europe’s 49.2% share equals USD 7.1 Bn, making the region the most influential globally today.

Parmesan cheese is a hard, aged cheese traditionally made from cow’s milk. It is known for its grainy texture, rich umami taste, and long aging period, which can range from one year to several years. It is widely used for grating over pasta, soups, and salads, and is also eaten in small chunks because of its deep, nutty flavor and long shelf life.

The Parmesan cheese market covers the production, distribution, and consumption of this aged cheese across foodservice, retail, and ingredient use. It includes traditional dairy-based Parmesan as well as newer styles inspired by Parmesan flavor and texture, including premium, artisanal, and alternative formulations used in modern cooking.

One major growth factor is the rising global interest in premium and aged cheeses. Consumers are cooking more at home, exploring Italian-style meals, and valuing strong flavors that last longer in storage. Parmesan fits well into this shift because small quantities deliver strong taste and versatility.

Demand is also being supported by innovation around cheese alternatives and fermentation. New food startups are attracting strong backing, such as $12 million in seed funding for launching plant-based cheese in U.S. cities, €5 million raised in Italy for fermented vegan cheese, and $17 million in Series A funding to scale solid-state fermentation technologies.

A key opportunity lies in premium positioning and lifestyle branding. High-end food culture is gaining attention, seen even in luxury trends like a $400 block of cheese featured alongside a $4.5 million residence, while Europe continues backing food innovation with investments such as a €20 million EU bank deal supporting plant-based food expansion.

Key Takeaways

- The Global Parmesan Cheese Market is expected to be worth around USD 26.6 billion by 2034, up from USD 14.6 billion in 2024, and is projected to grow at a CAGR of 6.2% from 2025 to 2034.

- Animal-based sources dominate the Parmesan Cheese Market, holding 88.1% share due to traditional production preferences.

- Conventional Parmesan Cheese leads market types with 88.3% share, driven by familiar taste expectations globally.

- Block form accounts for 33.7% in the Parmesan cheese market due to longer shelf stability.

- Domestic Parmesan products hold a 56.5% share as local production supports freshness and pricing control efficiency.

- Animal rennet dominates the Parmesan Cheese Market rennet types with 73.4% share, reflecting authentic methods standards.

- Supermarkets and hypermarkets lead distribution with a 48.9% share, offering wide access to Parmesan Cheese consumers.

- In Europe, the Parmesan Cheese Market reached USD 7.1 Bn, driven by foodservice demand.

By Source Analysis

Animal-based sources dominate the Parmesan Cheese Market, holding 88.1% due to traditional production.

In 2024, Animal-based held a dominant market position in the By Source segment of the Parmesan Cheese Market, with an 88.1% share. This strong position reflects deep consumer trust in traditional dairy-based Parmesan, which is closely linked with authentic taste, aging quality, and established culinary usage.

Animal-based Parmesan continues to be widely preferred due to its rich umami flavor, firm texture, and compatibility with classic Italian and international recipes. The long-standing presence of dairy Parmesan in households, restaurants, and foodservice kitchens supports steady volume consumption. Its suitability for shredding, grating, and direct consumption further strengthens demand across retail and commercial channels.

Consistent availability of milk supply, matured processing techniques, and consumer familiarity help sustain market stability. As a result, the animal-based source remains the backbone of the Parmesan cheese market, securing the majority share within the source-based segmentation.

By Type Analysis

Conventional Parmesan leads the market by type, capturing 88.3% preference globally.

In 2024, Conventional held a dominant market position in the By Type segment of the Parmesan Cheese Market, with an 88.3% share. This dominance is mainly driven by strong consumer preference for traditionally produced Parmesan that aligns with familiar taste, texture, and usage expectations.

Conventional Parmesan continues to be widely adopted across households, restaurants, and institutional kitchens due to its reliable aging process and consistent flavor profile. Buyers often associate conventionally produced cheese with better availability and stable pricing, making it a regular choice for everyday cooking and foodservice applications.

Its long shelf life and ease of storage also support repeated purchase behavior. As a result, the conventional type remains the primary contributor within this segment, anchoring overall market demand and reinforcing its leading position in the Parmesan cheese landscape.

By Form Analysis

Block form accounts for a 33.7% share, favored for freshness and greater flexibility.

In 2024, Block held a dominant market position in the By Form segment of the Parmesan Cheese Market, with a 33.7% share. This leadership is largely supported by consumer preference for authentic presentation and freshness associated with whole cheese blocks.

Block Parmesan allows users to grate or slice according to specific culinary needs, which makes it highly favored in both home kitchens and professional foodservice settings. Many buyers perceive block form as offering better flavor retention and longer usability compared to pre-processed options.

Its suitability for controlled portioning also reduces waste, adding to its practical appeal. Consistent demand from retail and hospitality channels helps maintain steady sales volumes. As a result, block-form Parmesan continues to act as a core contributor within form-based segmentation, reinforcing its dominant market position.

By Product Analysis

Domestic Parmesan products represent 56.5% of the Parmesan Cheese Market.

In 2024, Domestic Parmesan held a dominant market position in the By Product segment of the Parmesan Cheese Market, with a 56.5% share. This dominance is supported by strong local production capacity and steady consumption across everyday food applications.

Domestic Parmesan benefits from shorter supply chains, which help ensure consistent availability and fresher product access for retailers and foodservice buyers. Consumers often prefer domestically produced cheese due to familiarity with taste profiles and easier access through local distribution networks.

Competitive pricing within home markets further supports repeat purchasing. Its broad presence across supermarkets, restaurants, and institutional kitchens strengthens volume sales. As a result, domestic Parmesan continues to anchor the product-based segmentation, maintaining a leading role in supporting overall market stability and consumption patterns.

By Rennet Type Analysis

Animal rennet remains widely used, contributing 73.4% share in production methods.

In 2024, Animal Rennet held a dominant market position in the By Rennet Type segment of the Parmesan Cheese Market, with a 73.4% share. This leading position reflects the strong reliance on traditional cheesemaking practices, where animal rennet is valued for its proven ability to deliver consistent curd formation and desired texture.

Parmesan produced using animal rennet is widely associated with authentic taste, firm structure, and reliable aging performance. These characteristics align closely with long-established production standards and consumer expectations for classic Parmesan.

Continued use of animal rennet also supports uniform quality across large production volumes. As a result, animal rennet remains the preferred choice within this segment, reinforcing its dominant role and sustained importance in shaping overall Parmesan cheese production trends.

By Distribution Channel Analysis

Supermarkets and hypermarkets lead distribution, holding 48.9% market share.

In 2024, Supermarkets/Hypermarkets held a dominant market position in the By Distribution Channel segment of the Parmesan Cheese Market, with a 48.9% share. This dominance is driven by their wide product visibility, convenient purchasing experience, and strong penetration across urban and suburban areas.

Large retail formats allow consumers to compare packaging forms and select products based on daily cooking needs, supporting regular purchases. Supermarkets and hypermarkets also benefit from established cold-chain infrastructure, which helps maintain product quality and shelf stability.

High footfall and routine grocery shopping behavior further strengthen sales volumes through this channel. As a result, supermarkets and hypermarkets continue to serve as the primary access point for Parmesan cheese, anchoring distribution strength and supporting consistent market reach.

Key Market Segments

By Source

- Animal-based

- Plant-based

By Type

- Conventional

- Organic

By Form

- Block

- Powdered

- Shredded

- Grated

- Others

By Product

- Domestic Parmesan

- Parmesan-Style Cheese (Non-PDO)

- PDO Parmigiano Reggiano

By Rennet Type

- Animal Rennet

- Microbial/Vegetarian Rennet

By Distribution Channel

- Supermarkets/Hypermarkets

- Specialty Stores

- Convenience Stores

- Online Retail

- Others

Driving Factors

Rising Consumer Preference for Premium Protein Foods

One key driving factor in the Parmesan cheese market is the growing consumer focus on protein-rich and premium food choices. People are paying closer attention to nutrition, ingredient quality, and taste, especially in everyday foods used for home cooking. Parmesan cheese fits well into this shift because it offers strong flavor with small portions and adds natural protein to meals.

Shoppers are also more willing to explore innovative protein-backed foods, which supports overall interest in cheese and cheese-inspired products. This trend is reinforced by strong investor confidence in alternative and high-quality protein solutions.

For example, The Every Company secured $55 million in funding as animal-free egg protein expanded into large retail chains. Such funding highlights rising demand for protein-focused foods, indirectly strengthening consumer openness toward premium cheese categories like Parmesan.

Restraining Factors

High Production Complexity Limits Market Expansion

A key restraining factor in the Parmesan cheese market is the complex and time-intensive production process. Traditional Parmesan requires long aging periods, careful quality control, and steady raw material supply, all of which increase production costs. These challenges limit flexibility for producers and make it harder to quickly respond to changes in demand.

Price sensitivity among consumers can also restrict wider adoption during periods of economic pressure. At the same time, investors are actively supporting alternatives that aim to remove these bottlenecks. For instance, Change Foods secured $15.3 million in seed funding to develop fermentation-based dairy products that reduce aging time and production constraints.

Such developments highlight how complexity in conventional Parmesan manufacturing can restrain faster market growth, as innovation looks for simpler solutions.

Growth Opportunity

Animal-Free Cheese Innovation Creates New Growth Paths

One major growth opportunity for the Parmesan cheese market comes from rising innovation in animal-free and fermentation-based dairy solutions. Consumers are becoming more open to cheese alternatives that offer a familiar taste with fewer environmental and ethical concerns. This shift creates room for new Parmesan-style products that can reach flexitarian and plant-focused buyers without replacing traditional demand. Strong investor support confirms this opportunity.

Change Foods closed a record $12 million seed extension to scale animal-free cheese made through precision fermentation. Such funding highlights growing confidence in next-generation cheese technologies. These innovations can shorten production timelines, improve supply consistency, and open access to new retail and foodservice channels, creating additional market expansion opportunities around Parmesan-style offerings.

Latest Trends

Fermentation Technology Redefines Future Parmesan Cheese Market

One of the latest trends shaping the Parmesan cheese market is the growing use of fermentation technology to recreate traditional cheese flavors without relying fully on animal farming. This approach focuses on developing familiar taste, aroma, and texture while improving production efficiency and sustainability.

Consumers are increasingly curious about cheeses made through advanced fermentation processes, especially those looking for modern dairy options with traditional flavor profiles. Investor activity strongly reflects this trend.

Better Dairy secured US$2.1 million in seed funding to advance its animal-free fermentation-based dairy products. This funding highlights rising interest in technology-driven cheese innovation, signaling that fermentation-led development is becoming an important trend influencing the future evolution of Parmesan-style cheeses.

Regional Analysis

Europe leads the Parmesan Cheese Market with 49.2% share, reflecting strong regional consumption patterns.

Europe held the dominant position in the global Parmesan cheese market, accounting for 49.2% of the total market share and reaching a value of USD 7.1 Bn. This leadership is strongly linked to deep-rooted culinary traditions, widespread use of aged cheeses in daily cooking, and high per capita consumption across households and foodservice outlets. Strong regional familiarity with Parmesan-style cheeses supports consistent demand across retail and professional kitchens.

North America represents a mature and stable regional market, driven mainly by strong adoption of Parmesan in home cooking, dining chains, and packaged food applications. Consumer preference for convenient meal preparation and Italian-inspired cuisines continues to support steady usage patterns in the region.

Asia Pacific is gradually emerging due to changing food preferences and growing exposure to Western-style dishes, particularly in urban areas. Expanding retail availability and rising interest in premium food ingredients are aiding gradual market development.

The Middle East & Africa region shows selective growth, largely supported by the increasing presence of international foodservice formats and evolving consumption habits. Meanwhile, Latin America reflects moderate demand, driven by urban consumption and growing acceptance of European-style cheese in cooking applications.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

The Kraft Heinz Company plays a significant role in the global Parmesan cheese market through its strong brand presence and wide retail penetration. In 2024, the company continues to benefit from its large-scale manufacturing capabilities and efficient distribution networks across multiple regions. Its focus on consistent taste, long shelf life, and convenient packaging formats supports steady demand from households and foodservice buyers. Kraft Heinz’s strength lies in meeting everyday consumption needs while maintaining reliability, making it a familiar choice for regular cooking and meal preparation.

Sargento Foods maintains a solid position in the Parmesan cheese market by emphasizing product quality and consumer trust. In 2024, the company’s operations reflect a clear focus on natural cheese offerings and controlled sourcing practices. Sargento’s approach centers on delivering dependable flavor and texture, which aligns well with consumer expectations for grated and block Parmesan used in home kitchens. Its ability to adapt packaging and portion sizes also helps address changing buying habits.

Zanetti S.p.A. is closely associated with traditional cheese expertise and strong European roots. In 2024, Zanetti continues to leverage its experience in aged cheese production, supporting its reputation for authentic Parmesan-style products. The company’s emphasis on traditional processing and export-oriented growth helps strengthen its presence in international markets, particularly where demand for classic European cheese profiles remains strong.

Top Key Players in the Market

- The Kraft Heinz Company

- Sargento Foods

- Zanetti S.p.A.

- Bertinelli

- Fonterra Co-operative Group Limited

- Arla Foods amba

- FrieslandCampina

- Saputo Inc.

- Organic Valley

- SAVENCIA SA

Recent Developments

- In August 2025, Kraft Heinz launched new mayonnaise-style sauces under its HEINZ brand, including a “Garlic Parmesan” flavor. This indicates an extension of its cheese-flavored offerings beyond traditional cheese products, tapping into consumer appetite for convenience and familiar cheesy taste in condiments.

- In March 2024, Sargento expanded its natural cheese portfolio with new products, including its “Fun! Balanced Breaks®” line and two new flavored string-cheese snacks (Smokehouse String Cheese™ and Fiesta Pepper String Cheese™).

Report Scope

Report Features Description Market Value (2024) USD 14.6 Billion Forecast Revenue (2034) USD 26.6 Billion CAGR (2025-2034) 6.2% Base Year for Estimation 2024 Historic Period 2020-2023 Forecast Period 2025-2034 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Source (Animal-based, Plant-based), By Type (Conventional, Organic), By Form (Block, Powdered, Shredded, Grated, Others), By Product (Domestic Parmesan, Parmesan-Style Cheese (Non-PDO), PDO Parmigiano Reggiano), By Rennet Type (Animal Rennet, Microbial/Vegetarian Rennet), By Distribution Channel (Supermarkets/Hypermarkets, Specialty Stores, Convenience Stores, Online Retail, Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA Competitive Landscape The Kraft Heinz Company, Sargento Foods, Zanetti S.p.A., Bertinelli, Fonterra Co-operative Group Limited, Arla Foods amba, FrieslandCampina, Saputo Inc., Organic Valley, SAVENCIA SA Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)  Parmesan Cheese MarketPublished date: December 2025add_shopping_cartBuy Now get_appDownload Sample

Parmesan Cheese MarketPublished date: December 2025add_shopping_cartBuy Now get_appDownload Sample -

-

- The Kraft Heinz Company

- Sargento Foods

- Zanetti S.p.A.

- Bertinelli

- Fonterra Co-operative Group Limited

- Arla Foods amba

- FrieslandCampina

- Saputo Inc.

- Organic Valley

- SAVENCIA SA

Our Clients

- 168993

- December 2025