Global Onshore Drilling Fluids Market Size, Share, And Enhanced Productivity By Product Type (Oil-based Drilling Fluid, Synthetic-based Drilling Fluid, Water-based Drilling Fluid), By Basin (Permian, Eagle Ford, Niobrara, Bakken, Appalachia, Others), By Well Type (HPHT, Conventional), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, and Forecast 2026-2035

- Published date: March 2026

- Report ID: 180032

- Number of Pages: 379

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

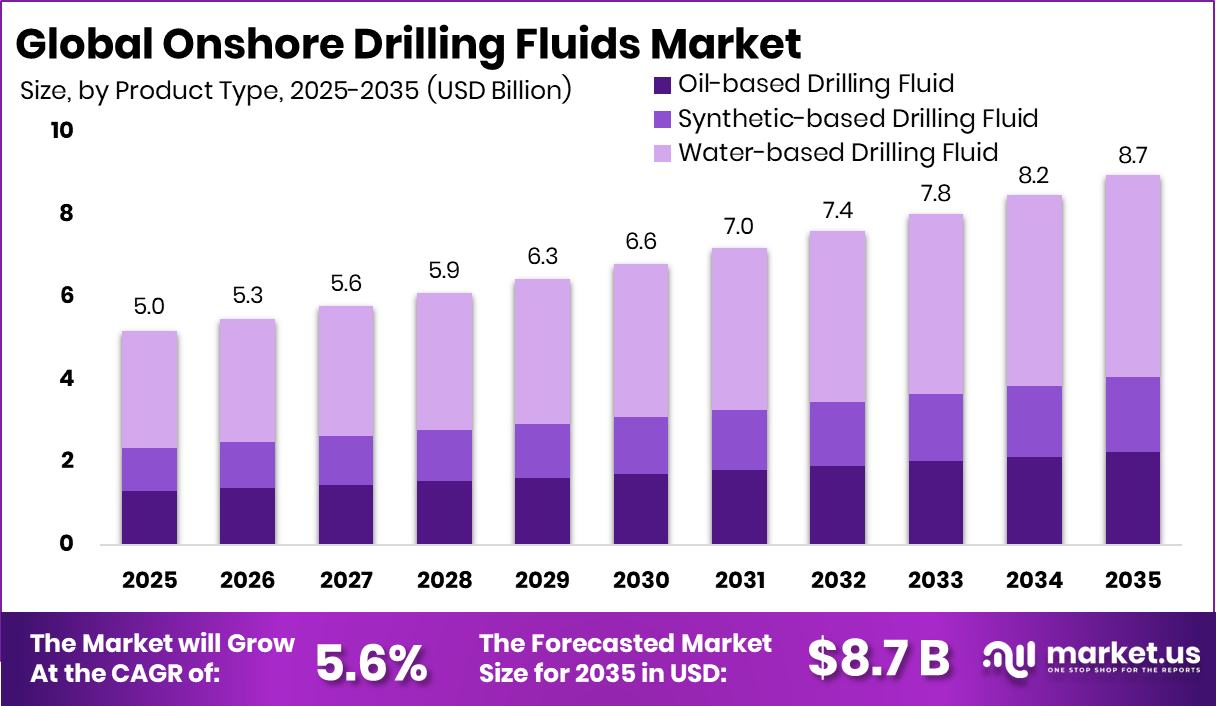

The Global Onshore Drilling Fluids Market is expected to be worth around USD 8.7 billion by 2035, up from USD 5.0 billion in 2025, and is projected to grow at a CAGR of 5.6% from 2026 to 2035. North America maintains dominance at 45.1% share, totaling USD 2.2 Bn.

The Onshore Drilling Fluids Market revolves around the use of specialized fluids that support drilling operations across land-based wells. Onshore drilling fluids are essential mixtures—ranging from oil-based and synthetic-based to widely used water-based systems—designed to cool drill bits, stabilize wellbores, transport cuttings, and maintain pressure control. The market covers major basins such as Permian, Eagle Ford, Niobrara, Bakken, Appalachia, and several emerging regions, with fluids adapted to both HPHT and conventional well environments.

Market growth is influenced by rising drilling activity across resource-rich basins, especially as dealmaking rebounds, illustrated by the $13bn Permian driller merger that strengthens onshore output momentum. Demand also benefits from stronger local involvement in upstream operations, supported by $1.98bn contracts awarded to local companies by Shell, reflecting continued investment in drilling programs.

Market challenges occasionally emerge from operational incidents and environmental responsibilities, such as the 6,000-barrel drilling fluid spill in Caddo County and $42 million in pollution fines linked to Mariner East II pipeline companies, reinforcing the need for safer and more efficient fluid systems.

Future opportunities are shaped by digitalization and evolving infrastructure, supported by funding trends like QumulusAI’s $500M blockchain-backed expansion facility and USD.AI’s $13M raise, which signal greater integration of advanced analytics into drilling fluid optimization.

Key Takeaways

- The Global Onshore Drilling Fluids Market is expected to be worth around USD 8.7 billion by 2035, up from USD 5.0 billion in 2025, and is projected to grow at a CAGR of 5.6% from 2026 to 2035.

- Onshore Drilling Fluids Market sees strong dominance as water-based drilling fluid captures 56.3% share.

- The Onshore Drilling Fluids Market benefits as the Permian Basin contributes 27.4% overall share.

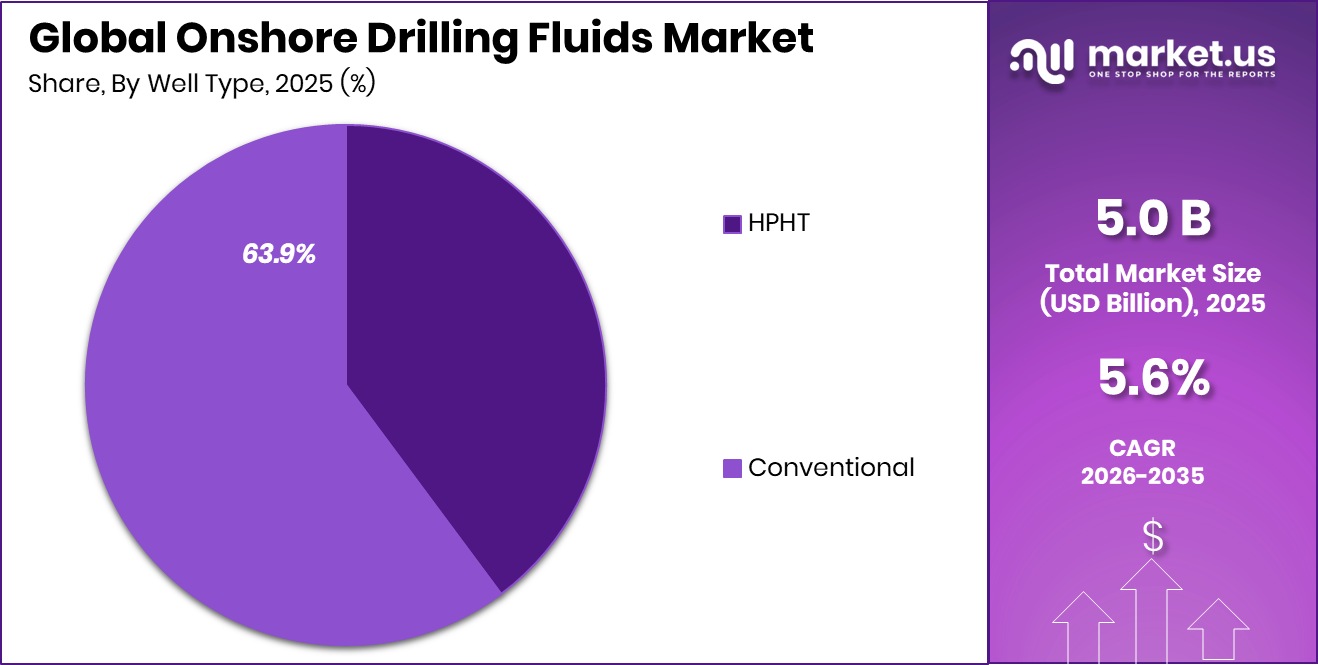

- The onshore drilling fluids market remains driven by conventional wells, representing a large 63.9% segment share.

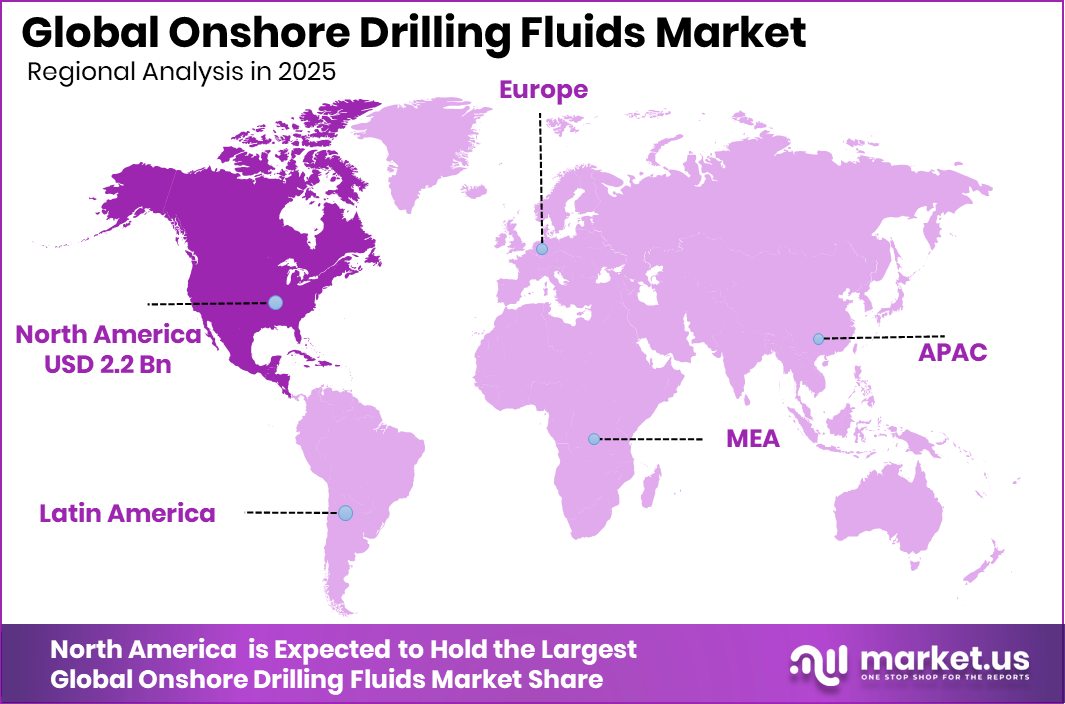

- The region of North America posts a 45.1% contribution valued at USD 2.2 Bn.

By Product Type Analysis

Water-based formulations lead the Onshore Drilling Fluids Market with a notable 56.3% share.

In 2025, the Onshore Drilling Fluids Market is expected to reflect strong operational momentum as producers continue optimizing drilling cycles across major oil-rich regions. Water-based drilling fluid remains the dominant product choice, accounting for 56.3%, driven by its cost efficiency, environmental compatibility, and ease of handling in high-activity basins. Onshore operators prefer these fluids for reducing formation damage and controlling wellbore conditions in routine drilling programs.

Continued investment in drilling automation, faster horizontal well completions, and sustainable fluid formulations strengthens adoption. As rig counts stabilize and service providers upgrade fluid performance with improved viscosifiers and shale inhibitors, the market shows consistent demand renewal, encouraging suppliers to expand portfolios targeting diverse lithologies and variable drilling depths.

By Basin Analysis

Permian basin drives the Onshore Drilling Fluids Market with its 27.4% contribution.

In 2025, basin-level activity continues to shape the Onshore Drilling Fluids Market, with the Permian Basin holding 27.4%, reinforcing its position as the most active and economically resilient U.S. shale region. High drilling intensity, longer laterals, and multi-well pad development contribute to sustained fluid consumption.

The Permian’s favorable geology and high recovery factors attract operators to maintain aggressive drilling schedules despite price fluctuations. This basin’s expanding infrastructure, improved water recycling systems, and rising adoption of advanced fluid chemistries support steady procurement of high-performance drilling fluids.

As operators focus on lowering operational downtime and enhancing borehole stability, fluid suppliers see continued opportunities to provide formulations tailored to unconventional reservoirs, ultimately reinforcing demand across all major sub-basins.

By Well Type Analysis

Conventional wells dominate the Onshore Drilling Fluids Market, holding a major 63.9% share.

In 2025, well-type preferences continue to influence the Onshore Drilling Fluids Market, with conventional wells representing 63.9% due to their lower operational complexity, predictable formations, and faster execution cycles. These wells rely heavily on consistent fluid properties to maintain wellbore integrity, manage pressures, and optimize penetration rates. Many mature fields undergoing redevelopment or infill drilling sustain steady demand for proven fluid systems.

Conventional onshore operations offer operators predictable cost structures, allowing service companies to deploy water-based and synthetic-enhanced blends that improve drilling efficiency. With many regions focusing on maximizing existing reserves and reducing non-productive time, the reliance on reliable drilling fluids remains strong, reinforcing the market’s stability and widening opportunities for incremental product innovations.

Key Market Segments

By Product Type

- Oil-based Drilling Fluid

- Synthetic-based Drilling Fluid

- Water-based Drilling Fluid

By Basin

- Permian

- Eagle Ford

- Niobrara

- Bakken

- Appalachia

- Others

By Well Type

- HPHT

- Conventional

Driving Factors

Rising basin drilling activity boosts demand

The Onshore Drilling Fluids Market continues to advance as basin activity rises across major regions, especially where higher rig counts and longer laterals require reliable and consistent fluid systems. This momentum is further supported by broader local and regional initiatives that reflect strengthening economic participation, such as UTPB Athletics surpassing the $1 million mark in its Champions Fund for the 2024–2025 fiscal year, signaling continued financial engagement in communities closely tied to drilling regions.

Growing onshore output, increasing redevelopment of mature wells, and expanded drilling intervals sustain fluid consumption across oil-based, synthetic-based, and water-based systems. As operators push for drilling stability and wellbore safety, the requirement for high-performance fluids remains a key driving force for the market.

Restraining Factors

Environmental penalties increase regulatory pressures

The Onshore Drilling Fluids Market faces ongoing regulatory headwinds as stricter environmental compliance measures shape operating conditions. Rising scrutiny of fluid handling, waste disposal, and contamination risks contributes to tighter monitoring across active basins. This is reinforced by economic indicators such as the Permian Basin’s oil and natural gas activity, contributing $181.8 billion in GDP, drawing greater attention toward sustainable operational practices.

Environmental penalties and remediation requirements can elevate project costs, influencing operator strategies and fluid selection. Incidents of spills and improper waste management further heighten regulatory sensitivity, encouraging companies to adopt safer and more transparent fluid systems. These pressures may limit growth pace in regions where operational compliance becomes increasingly demanding.

Growth Opportunity

Digital analytics improve fluid efficiency

Digital tools are opening meaningful opportunities for the Onshore Drilling Fluids Market by enhancing monitoring, viscosity control, real-time decision-making, and fluid optimization across various basins. The expansion of drilling footprints, particularly in high-activity regions, strengthens the need for smarter and more adaptive fluid systems. This aligns with financial activities such as EON Resources securing $52.8 million to expand its Permian footprint, reflecting ongoing investment in onshore development.

As digital platforms integrate with downhole sensing and surface analytics, operators gain the ability to reduce non-productive time, prevent wellbore instability, and maintain consistent performance in HPHT and conventional wells. These advancements create strong opportunities for next-generation fluid technologies and service-driven support models.

Latest Trends

Shift toward safer drilling fluid systems

A major trend shaping the Onshore Drilling Fluids Market is a broad shift toward safer, cleaner, and more operationally stable fluid systems. Operators increasingly seek formulations that minimize environmental exposure, improve handling safety, and support predictable rheological behavior in complex drilling conditions. This trend aligns with continued regional funding that strengthens workforce and operational development, such as the nearly $5 million contribution from PSP and the Scharbauer Foundation toward principal training, supporting broader skill-building within communities tied to onshore operations.

As safety expectations rise, interest grows in water-based systems, low-toxicity additives, and enhanced spill-prevention designs. Combined with improved monitoring tools, these trends continue to influence future product preferences and operational standards.

Regional Analysis

North America leads the market with 45.1% share, reaching USD 2.2 Bn.

The Onshore Drilling Fluids Market shows varied regional dynamics, with North America standing as the dominating region at 45.1% and valued at USD 2.2 Bn, supported by extensive drilling programs and consistent well development across mature and emerging basins. Europe maintains a stable demand as operators continue optimizing fluid performance for complex geological settings and environmentally sensitive zones, contributing to steady usage across its conventional and redevelopment projects.

In the Asia Pacific region, rising onshore drilling activities across developing economies support gradual growth as countries expand domestic energy exploration. The Middle East & Africa region sees continued reliance on drilling fluids for large-scale onshore operations in long-producing fields, sustaining recurring procurement needs.

Latin America remains an active market with fluid adoption tied to onshore exploration cycles and redevelopment initiatives. Across all these regions, operational consistency, wellbore stability requirements, and drilling efficiency goals continue to drive fluid consumption patterns, reinforcing steady market engagement.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

In 2025, Schlumberger continues to play a central role in shaping onshore drilling fluid performance through its strong operational footprint and advanced fluid engineering capabilities. The company’s consistent focus on enhancing rheology control, formation stability, and fluid recyclability helps operators achieve smoother drilling cycles across diverse onshore environments. Its integrated drilling support services further strengthen customer adoption by combining fluid optimization with real-time wellbore monitoring, making Schlumberger one of the most influential contributors to fluid innovation and field efficiency.

Halliburton maintains strong relevance in the 2025 landscape due to its extensive drilling fluid portfolios tailored for high-activity onshore wells. Its emphasis on improving fluid integrity, reducing non-productive time, and supporting reservoir-friendly formulations positions the company as a dependable partner for operators focused on maximizing drilling returns. Halliburton’s operational experience in both conventional and unconventional reservoirs allows it to deliver fluid systems that perform reliably under varying pressures, temperatures, and lithologies, reinforcing its competitive standing.

Baker Hughes demonstrates steady momentum within the global onshore drilling fluids space, driven by its approach to consistent fluid performance, wellbore stability enhancement, and operational cost optimization. The company’s emphasis on delivering adaptable fluid solutions supports operators managing different well designs and drilling depths. Baker Hughes benefits from strong field service capabilities and long-term operator relationships, enabling it to remain a key participant in aligning drilling fluid effectiveness with evolving onshore operational needs.

Top Key Players in the Market

- Schlumberger

- Halliburton

- Baker Hughes

- National Oilwell Varco

- Weatherford International

- Newpark Resources

- Aker Solutions

- Cimarex Energy

- Pioneer Natural Resources

Recent Developments

- In February 2025, SLB announced progress on acquiring ChampionX, a company known for drilling and production chemical solutions. This acquisition is aimed at strengthening SLB’s overall drilling and fluid service offerings, which could enhance its drilling fluids business over time. The deal was expected to close by early Q2 2025 after regulatory reviews. This move expands SLB’s capability in providing fluid-related products and services to oil and gas operators.

- In March 2024, Halliburton successfully deployed its BaraXtreme™ high-temperature, high-pressure drilling fluid system in a gas well under very tough downhole conditions. This fluid was designed to keep the wellbore stable and maintain performance where traditional fluids struggle, showing enhanced thermal tolerance and consistent rheological behavior. This real field application demonstrated Halliburton’s efforts to extend fluid performance in extreme drilling environments.

Report Scope

Report Features Description Market Value (2025) USD 5.0 Billion Forecast Revenue (2035) USD 8.7 Billion CAGR (2026-2035) 5.6% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product Type (Oil-based Drilling Fluid, Synthetic-based Drilling Fluid, Water-based Drilling Fluid), By Basin (Permian, Eagle Ford, Niobrara, Bakken, Appalachia, Others), By Well Type (HPHT, Conventional ) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA Competitive Landscape Schlumberger, Halliburton, Baker Hughes, National Oilwell Varco, Weatherford International, Newpark Resources, Aker Solutions, Cimarex Energy, Pioneer Natural Resources Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Onshore Drilling Fluids MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample

Onshore Drilling Fluids MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Schlumberger

- Halliburton

- Baker Hughes

- National Oilwell Varco

- Weatherford International

- Newpark Resources

- Aker Solutions

- Cimarex Energy

- Pioneer Natural Resources

Our Clients

- 180032

- March 2026