Global Nanoceramic Powder Market By Type (Oxide Powder, Carbide Powder, Nitride Powder, Boron Powder, and Others), By Synthesis Technology (Electrical And Electronics, Industrial, Transportation, Medical, Chemical, Defense, and Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2026-2035

- Published date: April 2026

- Report ID: 183567

- Number of Pages: 370

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

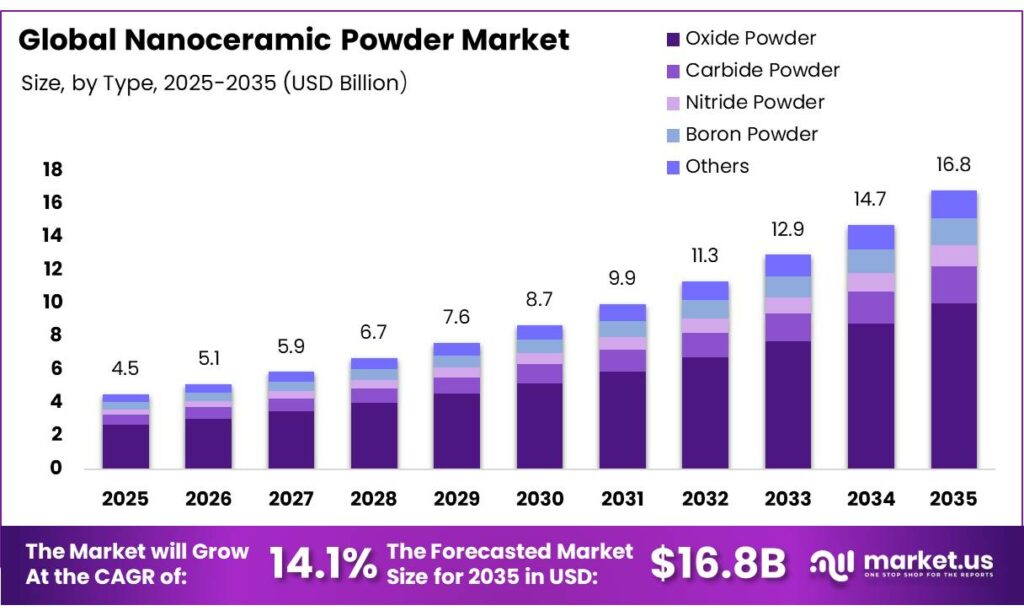

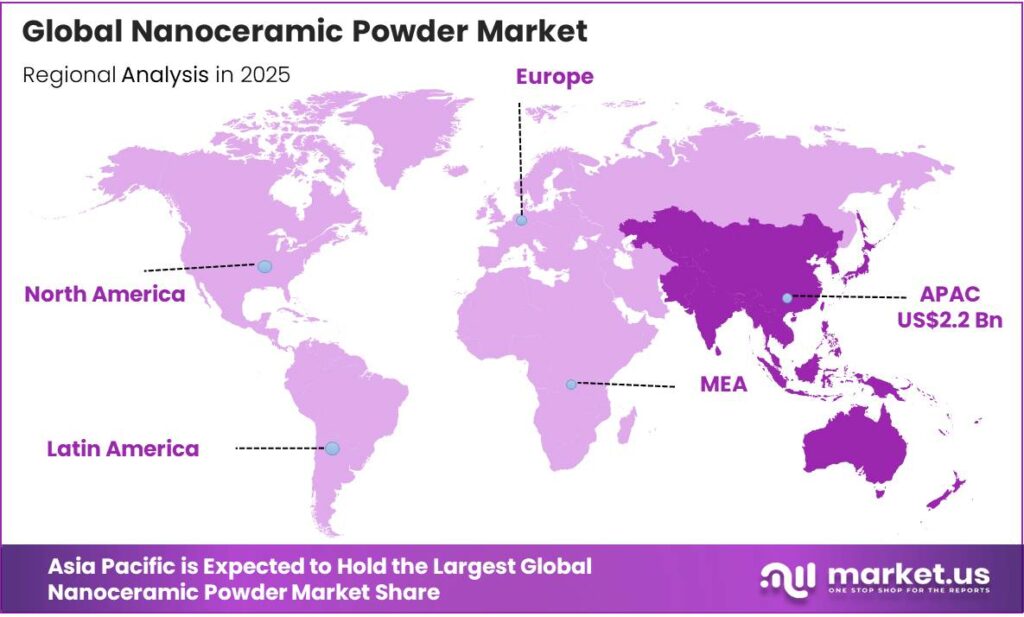

The Global Nanoceramic Powder Market size is expected to be worth around USD 16.8 Billion by 2035, from USD 4.5 Billion in 2025, growing at a CAGR of 14.1% during the forecast period from 2026 to 2035. In 2025, Asia Pacific held a dominant market position, capturing more than a 48.9% share, holding USD 2.2 Billion revenue.

Nanoceramic powder consists of ceramic particles engineered at the nanoscale, typically ranging from 1 to 100 nanometers in size. At this microscopic scale, these materials exhibit physical and chemical properties that are vastly superior to their bulk counterparts, such as enhanced mechanical strength, high thermal stability, and unique electrical behavior. The nanoceramic powder market is driven by the growing demand for high-performance materials across various sectors, particularly electronics and energy.

Nanoceramic powders, including oxides such as alumina and zirconia, offer unique advantages such as high electrical insulation, thermal stability, and mechanical strength, making them ideal for applications in semiconductors, capacitors, and energy storage devices.

Asia Pacific stands as the largest market, with countries such as China, Japan, and South Korea leading in the adoption of these materials for electronics, renewable energy, and biomedical sectors. However, challenges persist, including the high energy consumption of production processes and environmental concerns, particularly regarding the use of toxic solvents and metal precursors.

Geopolitical tensions, such as trade restrictions and sanctions, further impact the supply chain. Despite these challenges, nanoceramic powders continue to gain traction in additive manufacturing, medical devices, and aerospace applications, driven by advancements in material properties and manufacturing techniques.

Key Takeaways:

- The global nanoceramic powder market was valued at USD 4.5 billion in 2025.

- The global nanoceramic powder market is projected to grow at a CAGR of 14.1% and is estimated to reach USD 16.8 million by 2035.

- Based on the types of nanoceramic powder, oxide powder dominated the market, with a market share of around 59.5%.

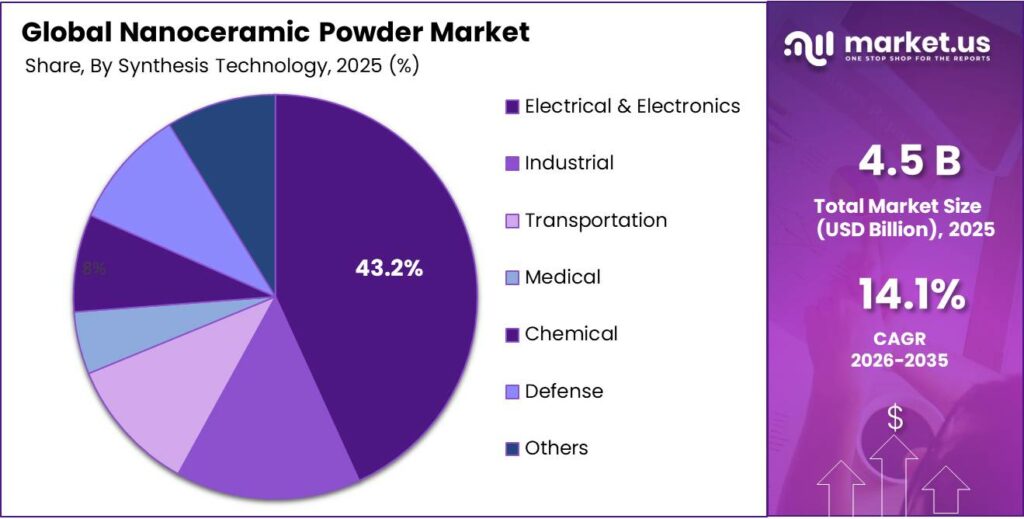

- Among the synthesis technologies, the electrical & electronics industry held a major share in the market, 43.2% of the market share.

- In 2025, the Asia Pacific was the most dominant region in the nanoceramic powder market, accounting for around 48.9% of the total global consumption.

Type Analysis

Nanoceramic Oxide Powder Held the Largest Share in the Market.

The nanoceramic powder market is segmented based on type into oxide powder, carbide powder, nitride powder, boron powder, and others. The nanoceramic oxide powder dominated the market, comprising around 59.5% of the market share, primarily due to its superior versatility, cost-effectiveness, and availability. Oxides such as alumina (Al₂O₃) and zirconia (ZrO₂) offer excellent electrical insulation, high thermal stability, and mechanical strength, making them ideal for a wide range of applications, including electronics, energy storage, and biomedical implants.

Additionally, their relatively simpler synthesis processes and lower material costs compared to carbides and nitrides further enhance their accessibility. In contrast, carbides and nitrides are more prone to high reactivity during synthesis and processing, which can complicate their use in certain applications. Similarly, oxides are generally more stable and less toxic, making them more suitable for industries with stringent safety and environmental regulations, such as healthcare and consumer electronics.

Synthesis Technology Analysis

Nanoceramic Powder is Mostly Utilized in the Electrical & Electronics Industry.

Based on the synthesis technology, the market is divided into electrical & electronics, industrial, transportation, medical, chemical, defense, and others. The electrical & electronics industry dominated the nanoceramic powder market, with a market share of 43.2%, due to the powder’s properties, such as high electrical insulation, thermal stability, and mechanical strength, which are critical in high-performance electronic components. Nanoceramics are ideal for applications such as capacitors, semiconductors, and insulating substrates, where reliability and precision are essential.

The demand for miniaturized, energy-efficient, and durable devices in consumer electronics, such as smartphones, wearables, and computers, has fueled the use of nanoceramics in this sector. While nanoceramics have potential in industrial, medical, and defense applications, the electronics sector’s rapid innovation, combined with the relatively lower cost and easier integration of nanoceramics into mass-produced electronic devices, makes it the dominant field for their use.

Key Market Segments:

By Type

- Oxide Powder

- Carbide Powder

- Nitride Powder

- Boron Powder

- Others

By Synthesis Technology

- Electrical & Electronics

- Industrial

- Transportation

- Medical

- Chemical

- Defense

- Others

Drivers

Growth in the Electronics Industry Drives the Nanoceramic Powder Market.

The expansion of the electronics industry serves as a primary catalyst for the nanoceramic powder market, driven by the technical requirements of next-generation semiconductors, dielectric components, and thermal management systems. As electronic devices become more compact, energy-efficient, and high-performance, the need for advanced materials such as nanoceramics has risen. For instance, the increasing miniaturization of semiconductors requires high-performance insulators and substrates, where nanoceramics, particularly aluminum oxide and zirconium oxide, offer enhanced electrical insulation, high thermal stability, and mechanical strength.

Similarly, modern smartphones utilize over 1,000 MLCCs per device to manage power distribution in increasingly dense circuitries. Nanoceramic powders, specifically barium titanate and hafnium oxide, are critical for multi-layer ceramic capacitors (MLCCs). Further, according to the U.S. Department of Energy (DOE), advanced ceramics are essential for improving the efficiency of wide-bandgap semiconductors, which are projected to see increased adoption in renewable energy grids. There is a rise in the incorporation of nanoceramics into electronic packaging systems as part of efforts to enhance device performance and lifespan. The expansion of the electronics sector directly correlates with a growing demand for nanoceramic materials.

- According to the Bureau of Labor Statistics (BLS), the semiconductor and related device manufacturing industry had 1,876 establishments in the first quarter of 2020, and by the first quarter of 2024, this figure had increased to 2,545 establishments in the US alone.

Restraints

Production Hurdles and Environmental Concerns Might Hamper the Demand for Nanoceramic Powder.

The nanoceramic powder market faces significant scalability and sustainability challenges rooted in high-energy synthesis requirements and the complex environmental fate of ultra-fine particles. The synthesis of high-quality nanoceramics often requires high-energy-consuming processes, such as sol-gel or chemical vapor deposition, which are energy-intensive and environmentally taxing. These processes can result in significant emissions of greenhouse gases, contributing to the carbon footprint of nanoceramic production.

Additionally, the use of certain precursor materials, such as toxic solvents and metals, raises concerns regarding environmental pollution. Nanoceramics can migrate into surface and ground waters via wastewater effluents or accidental spillages. In aquatic systems, concentrations exceeding 100 mg/L near industrial discharge sites have been identified as potentially toxic to organisms such as zebrafish embryos. Furthermore, achieving uniform particle size and consistency in nanoceramic powders remains difficult.

The scaling up of production from lab-scale to industrial levels often leads to variations in powder quality, which can affect the performance of end-use products, especially in high-precision applications such as semiconductors and medical devices. Environmental regulations in regions such as the European Union, which have stringent directives on hazardous materials, further complicate the production process, necessitating costly compliance measures.

Opportunity

Energy Sector and Biomedical Applications Create Opportunities in the Nanoceramic Powder Market.

The nanoceramic powder market is increasingly leveraged by strategic transitions in global energy infrastructure and advanced medical therapeutics, where nanoscale material properties fulfill critical performance requirements. In the energy sector, nanoceramic powders, such as yttria-stabilized zirconia (YSZ) and gadolinium-doped ceria (GDC), are essential for high-temperature electrolysis.

The reversible SOFC technology aims to reduce clean hydrogen production costs to US$1/kg by 2030, a goal dependent on nanostructured electrolytes that maintain ionic conductivity while operating at lower temperatures. Similarly, the incorporation of alumina nanoparticles in spacecraft cooling systems has demonstrated a 29% reduction in temperature and approximately 45% power savings, highlighting the efficiency gains available for terrestrial high-power electronics and energy grids.

Furthermore, in the biomedical field, nanoceramics are utilized in implants and prosthetics for their biocompatibility and strength. The FDA classifies nanoceramic-based bone grafts as class II (filling voids) or class III (containing drugs) devices, providing a standardized regulatory pathway for bioceramic powders such as hydroxyapatite (HAp) and tricalcium phosphate (TCP). Additionally, the National Institutes of Health (NIH) has funded research on the use of nanoceramic coatings for improving the performance and longevity of medical devices, such as joint replacements.

Trends

Adoption in Additive Manufacturing (3D Printing) Applications.

The integration of nanoceramic powders into additive manufacturing (AM) represents a shift from rapid prototyping to the production of high-performance, functional end-use components. This trend is characterized by the use of nanoscale reinforcements to overcome traditional ceramic processing limitations, such as high brittleness and sintering challenges. The trend is driven by the material’s high precision, strength, and thermal stability.

The use of nanoparticles in AM processes, such as directed energy deposition (DED), allows for the simultaneous fusion of ceramics and metal alloys, creating composites with localized material property alterations. Similarly, nanoceramic powders, including silicon carbide and alumina, enable the fabrication of complex internal lattice structures and hollow parts that are infeasible via traditional subtractive methods.

Additionally, organizations such as the National Aeronautics and Space Administration (NASA) and various aerospace manufacturers utilize nanoceramic-reinforced 3D printing to create lightweight, load-bearing parts with high thermal stability. The use of 3D printing allows for the precise control of microstructure, improving the mechanical properties and biocompatibility of nanoceramic components. This technological integration has prompted increasing interest from various sectors seeking enhanced material performance in additive manufacturing.

Geopolitical Impact Analysis

Geopolitical Tensions Accelerate Strategic Domestic Investment in Nanoceramic Technologies.

Current geopolitical instability functions as a dual-force mechanism, simultaneously disrupting supply chains and accelerating strategic domestic investment in nanoceramic technologies. Rising tensions have triggered a wave of export restrictions on critical minerals. As nanoceramic powders rely on high-purity precursors such as lithium, cobalt, and rare earth elements, these measures directly impact availability. For instance, tensions between the U.S. and China have led to the imposition of tariffs on rare earth minerals that are essential in the production of high-performance nanoceramics. This has prompted concerns about potential price volatility and shortages of key raw materials.

Additionally, the European Union has taken steps to reduce its dependency on foreign suppliers of critical materials through the European Commission’s Action Plan on Raw Materials, which includes strategies to ensure supply security in response to geopolitical uncertainties. The European Space Agency (ESA) has expressed concerns about the impact of supply chain disruptions on the production of high-tech ceramics used in aerospace technologies.

Moreover, sanctions on Russia have affected the availability of certain ceramic materials and processing technologies, as Russia is a key producer of zirconium, a material commonly used in nanoceramics. These geopolitical shifts are likely to affect the cost and availability of nanoceramic powders in various high-tech sectors.

Regional Analysis

Asia Pacific Held the Largest Share of the Global Nanoceramic Powder Market.

In 2025, the Asia Pacific dominated the global nanoceramic powder market, holding about 48.9% of the total global consumption, driven by rapid industrialization, technological advancements, and significant demand from electronics, energy, and biomedical sectors. The countries such as China, Japan, and South Korea are at the forefront of nanoceramic applications in electronics, particularly for semiconductors and capacitors.

China’s role as a global manufacturing hub has bolstered the demand for high-performance ceramics, particularly in microelectronics and battery technologies. According to the Japan Fine Ceramics Association (JFCA), Japan’s fine ceramics industry accounts for 40% of the global production market, with domestic production reaching approximately JPY4 trillion. This has supported the integration of nanoceramics in renewable energy technologies, such as solar panels, contributing to the region’s significant use of these materials.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Manufacturers of nanoceramic powders focus on several strategic activities, such as investment in research and development (R&D) to innovate and enhance the material properties, such as improving thermal stability, electrical insulation, and mechanical strength, which are critical for applications in electronics, energy, and biomedical sectors. Additionally, manufacturers prioritize optimizing production processes to increase efficiency and reduce costs, using techniques such as sol-gel synthesis or chemical vapor deposition.

Similarly, they focus on expanding production capabilities and achieving consistent quality, as uniformity in particle size is crucial for performance in high-precision industries. Moreover, strategic partnerships with industries such as aerospace, healthcare, and energy help secure long-term supply contracts. Furthermore, manufacturers are increasingly emphasizing sustainability by adopting eco-friendly production practices and complying with environmental regulations to appeal to environmentally-conscious consumers and meet regulatory standards.

The Major Players in The Industry

- ABM Advance Ball Mill Inc.

- American Elements

- Beijing DK Nano Technology Co., Ltd.

- Cerion LLC

- Inframat Advanced Materials LLC

- Innovnano – Materiais Avançados SA

- IoLiTec Ionic Liquids Technologies GmbH

- Nanografi

- Nanophase Technologies Corporation

- Nanoshel LLC

- Nanostructured & Amorphous Materials, Inc.

- NYACOL Nano Technologies Inc.

- PlasmaChem GmbH

- Resonac Corporation

- Saint-Gobain

- Sumitomo Chemical Co., Ltd.

- Tosoh Corporation

- TRUNNANO

- Other Key Players

Key Development

- In May 2025, Nanoe, located in Ballainvilliers, France, acquired the Upryze-Shock ceramic powder line from Saint-Gobain ZirPro, which is based in Le Pontet, France. The agreement encompasses the transfer of technology, a roster of current clients, and an exclusive license for the related patent and trademark.

- In February 2026, TRUNNANO, a top international provider of industrial ceramic materials, reported a major advancement in the research, development, and production of its flagship product, reaction sintered silicon carbide (SiSiC).

Report Scope

Report Features Description Market Value (2025) US$4.5 Bn Forecast Revenue (2035) US$16.8 Bn CAGR (2025-2035) 14.1% Base Year for Estimation 2025 Historic Period 2021-2024 Forecast Period 2025-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Type (Oxide Powder, Carbide Powder, Nitride Powder, Boron Powder, and Others), By Synthesis Technology (Electrical & Electronics, Industrial, Transportation, Medical, Chemical, Defense, and Others) Regional Analysis North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA Competitive Landscape ABM Advance Ball Mill Inc., American Elements, Beijing DK Nano Technology Co., Ltd., Cerion LLC, Inframat Advanced Materials LLC, Innovnano – Materiais Avançados SA, IoLiTec Ionic Liquids Technologies GmbH, Nanografi, Nanophase Technologies Corporation, Nanoshel LLC, Nanostructured & Amorphous Materials, Inc., NYACOL Nano Technologies Inc., PlasmaChem GmbH, Resonac Corporation, Saint-Gobain, Sumitomo Chemical Co., Ltd., Tosoh Corporation, TRUNNANO, and Other Players. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)  Nanoceramic Powder MarketPublished date: April 2026add_shopping_cartBuy Now get_appDownload Sample

Nanoceramic Powder MarketPublished date: April 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- ABM Advance Ball Mill Inc.

- American Elements

- Beijing DK Nano Technology Co., Ltd.

- Cerion LLC

- Inframat Advanced Materials LLC

- Innovnano – Materiais Avançados SA

- IoLiTec Ionic Liquids Technologies GmbH

- Nanografi

- Nanophase Technologies Corporation

- Nanoshel LLC

- Nanostructured & Amorphous Materials, Inc.

- NYACOL Nano Technologies Inc.

- PlasmaChem GmbH

- Resonac Corporation

- Saint-Gobain

- Sumitomo Chemical Co., Ltd.

- Tosoh Corporation

- TRUNNANO

- Other Key Players

Our Clients

- 183567

- April 2026