Global Marine Lubricants Market Size, Share, And Enhanced Productivity By Base Oil (Mineral Oil, Synthetic Oil, Bio-based Oil), By Product Type (Engine Oil, Hydraulic Fluid, Compressor Oil, Others), By Ship Type (Bulk Carriers, Tankers, Container Ships, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, and Forecast 2026-2035

- Published date: January 2026

- Report ID: 179416

- Number of Pages: 351

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

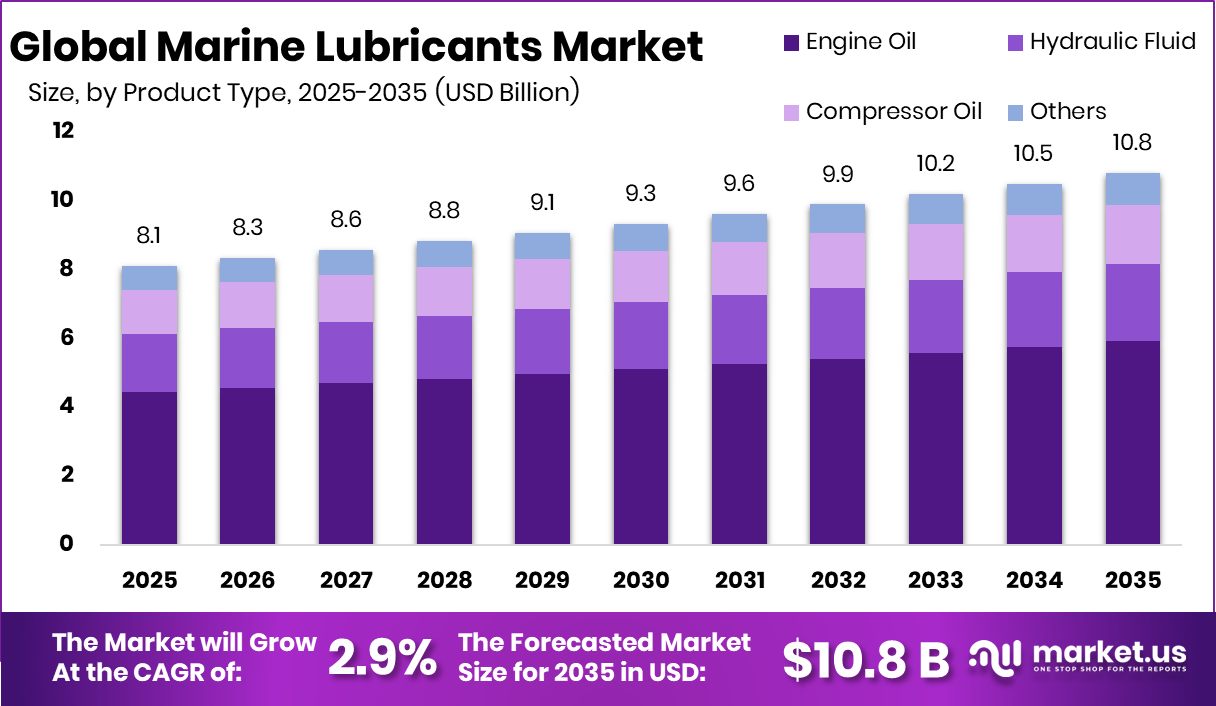

The Global Marine Lubricants Market is expected to be worth around USD 10.8 billion by 2035, up from USD 8.1 billion in 2025, and is projected to grow at a CAGR of 2.9% from 2026 to 2035. Asia Pacific maintains 49.4% share, pushing marine lubricants value toward USD 4.0 Bn.

Marine lubricants are specialized oils and fluids used to protect and maintain the moving parts of marine engines, hydraulic systems, compressors, and onboard machinery. They reduce friction, prevent corrosion, manage heat, and ensure smooth functioning even under heavy loads and long operating hours at sea. The Marine Lubricants Market covers the supply, demand, and development of these products across vessel categories such as bulk carriers, tankers, container ships, and others, segmented by base oil types—mineral, synthetic, and bio-based—and product types including engine oils, hydraulic fluids, and compressor oils.

Growth in the market is supported by rising global shipping activity and the modernization of fleets, which increases demand for durable lubrication solutions across all base-oil segments. Environmental transitions also influence demand as stricter compliance encourages better-performing fluids. A notable driver comes from national funding efforts, including South Korea launching a USD 680 million green-fuel infrastructure fund, encouraging cleaner marine operations that indirectly expand lubricant upgrade opportunities.

Opportunities continue to emerge through restoration and maritime protection projects, such as NOAA’s USD 210 million allocation for the Gulf of Mexico restoration, which supports long-term marine activity and raises maintenance requirements for vessels working in the region.

Geopolitical pressures, including sanctions by the United States and United Kingdom on “shadow fleet” vessels, reshape trade flows and create shifting demand patterns for lubricants as fleets reroute and operate under tighter scrutiny.

Market integrity also gains attention after cases like the Shell fuel-siphoning heist, which highlighted the need for tighter supply-chain monitoring—an area where lubricant suppliers can expand service-based opportunities.

Key Takeaways

- The Global Marine Lubricants Market is expected to be worth around USD 10.8 billion by 2035, up from USD 8.1 billion in 2025, and is projected to grow at a CAGR of 2.9% from 2026 to 2035.

- Mineral oil holds 74.5% share, reflecting strong reliance in the global marine lubricants market.

- Engine oil leads with 54.7% share, highlighting its dominance in the marine lubricants market.

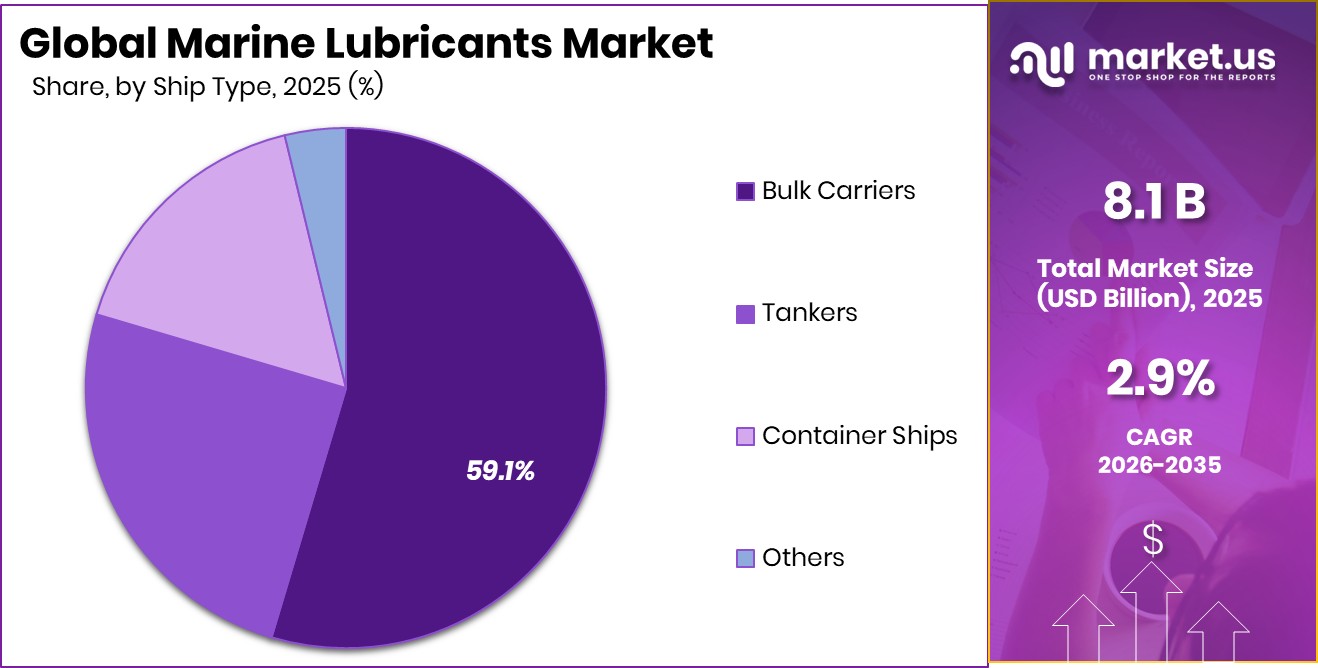

- Bulk carriers represent 59.1% of demand, making them key consumers in the marine lubricants market.

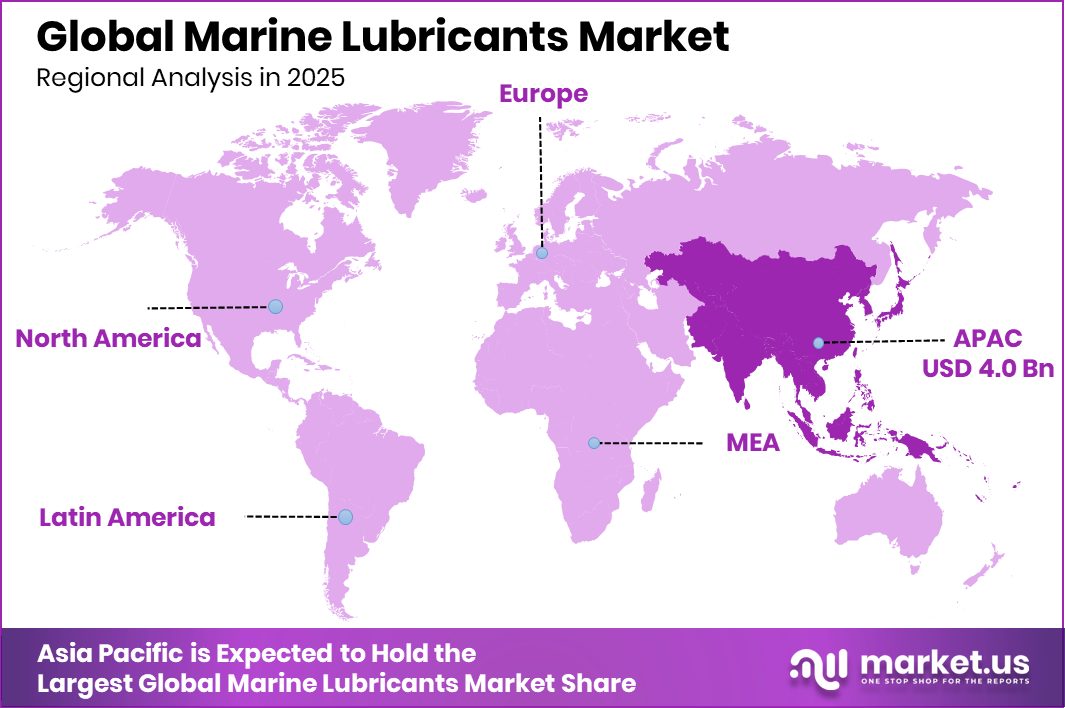

- Marine lubricants in Asia Pacific reach USD 4.0 Bn, supported by 49.4% dominance.

By Base Oil Analysis

Marine Lubricants Market prefers mineral oil, holding 74.5% share across global fleets.

In 2025, the Marine Lubricants Market continues to be strongly driven by mineral-oil-based formulations, which hold a dominant 74.5% share. This large share reflects the ongoing reliance of global fleets on cost-effective lubricants that offer stable performance in heavy-duty marine engines. Ship operators in commercial cargo, offshore services, and regional transport still prefer mineral oils due to their wide availability, consistent viscosity behavior, and compatibility with existing engine designs.

Even with rising interest in bio-based and synthetic options, mineral oils remain firmly established because many fleets operate older vessels that depend on conventional lubrication systems. As ports expand and sea freight volumes rise, this dominance of mineral-based lubricants is expected to remain an essential foundation of marine maintenance operations.

By Product Type Analysis

Marine Lubricants Market engine oil segment leads strongly with 54.7% dominant usage rate.

In 2025, engine oil holds a strong 54.7% share in the Marine Lubricants Market, emphasizing its critical role in maintaining the performance and longevity of marine propulsion systems. Marine engines operate under extreme conditions, including high loads, long operational hours, and variable fuel quality, making high-grade engine oils essential for reducing wear, controlling deposits, and boosting fuel efficiency.

With commercial vessels continuing long-distance operations and stricter emission norms pushing for cleaner combustion, the demand for engine oils remains central to fleet management budgets. Ports across Asia, Europe, and the Middle East are witnessing consistent service cycles, further supporting this demand. As global trade routes stabilize and shipping activities normalize, engine oil remains the most consumed lubricant category across fleets worldwide.

By Ship Type Analysis

Marine Lubricants Market demand grows as bulk carriers represent 59.1% lubricant consumption worldwide.

In 2025, bulk carriers represent the leading consumer base in the Marine Lubricants Market, accounting for 59.1% of total usage. These vessels handle long-haul transport of commodities such as coal, grains, iron ore, and fertilizers, requiring continuous engine operation for extended periods. Their heavy-duty propulsion systems and auxiliary machinery rely heavily on reliable lubrication to ensure uninterrupted performance across global routes.

Bulk carriers also experience significant mechanical stress during port operations and cargo handling, increasing the need for timely lubricant replenishment. As commodity trade remains robust and new shipping lanes expand, these carriers maintain the highest lubricant consumption among vessel categories. Their large fleet size and longer operational cycles reinforce their dominance in the marine lubrication ecosystem.

Key Market Segments

By Base Oil

- Mineral Oil

- Synthetic Oil

- Bio-based Oil

By Product Type

- Engine Oil

- Hydraulic Fluid

- Compressor Oil

- Others

By Ship Type

- Bulk Carriers

- Tankers

- Container Ships

- Others

Driving Factors

Rising forestry activities boost chainsaw adoption

Rising global seaborne trade continues to push the need for dependable marine lubricants, as ships operating longer routes require steady engine protection and efficient mechanical performance. Growing vessel movements across major shipping lanes also increase lubrication cycles, supporting higher consumption across bulk carriers, tankers, and container ships. A notable development influencing long-term demand comes from Greece approving €111.7m ($116.6m) in grants for a 50MW green hydrogen project, signalling stronger investment in cleaner maritime supporting infrastructure.

Although the project focuses on fuel transition, it indirectly strengthens marine operational activity and future lubricant needs by modernizing port-adjacent energy systems. Together, rising trade volumes and green-energy funding continue to shape demand patterns across the Marine Lubricants Market.

Restraining Factors

Stricter emission rules limit lubricant consumption.

Stricter global emission rules reduce lubricant usage by pushing ships toward cleaner fuels and newer engines that often require lower consumption volumes or optimized formulations. These environmental measures encourage operators to shift toward engines with tighter burn efficiencies, limiting the frequency of certain lubricant applications.

Additionally, market uncertainty increases as major companies adjust their portfolios, such as BP deciding to sell the majority stake of its $10bn Castrol lubricants business to reduce debt. This realignment contributes to caution across distributors and fleets that depend on stable supply chains. Regulatory pressure combined with corporate restructuring influences purchasing strategies and can delay bulk procurement, making these two forces key restraints on the Marine Lubricants Market.

Growth Opportunity

Expansion of eco-friendly lubricant formulations globally.

There is growing room for expansion in eco-friendly and high-performance lubricant formulations as vessel owners look for solutions that reduce environmental impact while supporting heavy-duty marine engines. The shift toward sustainability encourages suppliers to upgrade base-oil blends, improve additive packages, and develop bio-based alternatives for auxiliary and propulsion systems.

Growth sentiment is strengthened by clean-energy investments, including Motor Oil securing a €111.7m EU grant for a 50MW hydrogen project at a Greek refinery, which showcases rising regional focus on modernizing port-linked energy infrastructure. These developments support maritime transitions and open the door for advanced lubricants that align with cleaner operations. As fleets modernize, demand for environmentally improved fluids becomes a growing opportunity.

Latest Trends

Shift toward synthetic marine lubricant solutions.

The market continues to trend toward synthetic marine lubricant solutions, driven by their better oxidation resistance, longer service intervals, and ability to support engines operating under variable fuel regimes. More operators are shifting to high-performance synthetic blends to manage higher efficiency engines and unpredictable load cycles.

A parallel trend is the rise in hydrogen-related maritime investments, including the EU’s approval of €111.7m in state aid for Motor Oil Hellas to expand renewable hydrogen production. While hydrogen itself is a fuel transition pathway, such investments encourage technological upgrades in vessels and supporting infrastructure, further increasing the relevance of modern synthetic lubricants. These shifts define the evolving direction of the Marine Lubricants Market.

Regional Analysis

Asia Pacific holds 49.4% market share, driving marine lubricants demand to USD 4.0 Bn.

In 2025, the Marine Lubricants Market shows steady regional variation across North America, Europe, Asia Pacific, the Middle East & Africa, and Latin America, with each region influenced by fleet size, port activity, and vessel maintenance cycles.

Asia Pacific remains the dominant region, holding 49.4% of the market and reaching USD 4.0 Bn, supported by large commercial fleets and major shipping hubs. North America sees stable demand due to strong maritime trade on both the Atlantic and Pacific coasts, while Europe maintains consistent consumption driven by active cargo movement and established port infrastructure.

The Middle East & Africa region benefits from continuous marine traffic linked to energy exports and strategic waterways, contributing to steady lubricant usage. Latin America experiences moderate growth, supported by increasing port modernization and expanding bulk carrier operations.

Across all regions, the reliance on marine lubricants remains tied to vessel maintenance spending, operational hours, and the ongoing importance of marine transportation in global trade flows.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

In 2025, BP p.l.c. continues to strengthen its role in the Marine Lubricants Market by focusing on performance-driven formulations aligned with operational reliability. The company remains known for supplying marine oils designed for heavy-duty engine protection, helping fleets manage long operational hours and varying fuel qualities. Its continued emphasis on dependable lubrication solutions keeps it well-positioned among ship operators looking for consistency and efficient maintenance planning across global trade routes.

Chevron Corporation maintains a strong market presence by leveraging its long-standing expertise in lubricant chemistry and its established distribution network. The company continues to support marine customers with oils built to reduce engine wear, stabilize viscosity, and support durable performance in demanding maritime environments. Its product focus remains aligned with vessel operators that require a reliable lubricant supply across major ports, reinforcing its credibility in the marine operational ecosystem.

Exxon Mobil Corporation retains a leading position by emphasizing high-performance marine lubricants designed for both modern and legacy marine engines. In 2025, the company continues to meet customer needs through formulations that support engine cleanliness, efficient combustion, and lower maintenance downtime. Its strong brand reputation and technical support offerings help it remain a preferred partner for fleets seeking proven solutions that match long-haul shipping demands and global operational consistency.

Top Key Players in the Market

- BP p.l.c.

- Chevron Corporation

- Exxon Mobil Corporation

- Shell plc

- TotalEnergies SE

- Petronas

- LUKOIL

- Idemitsu Kosan Co., Ltd

- China Petroleum & Chemical Corporation

- ENEOS Holdings, Inc.

Recent Developments

- In May 2025, BP started the formal sale process of its global lubricants division, Castrol, which produces engine oils and industrial lubricants used in marine, automotive, and industrial sectors. This strategic move aimed to refocus BP’s business and reduce debt by selling a major portion of its lubricants operations. The potential transaction was valued at around US$10 billion, making it one of the company’s largest divestments. This step reflects BP’s shift in priorities towards its core energy operations while still maintaining a presence through specialty products.

- In November 2024, Chevron Marine Lubricants, part of Chevron Corporation, expanded its global supply network to include Port Elizabeth in South Africa. This step means ships calling at this major port will now have better access to Chevron’s marine lubricant products, including popular engine oils like the Taro Ultra range. The move supports vessels taking longer routes around southern Africa and improves Chevron’s service and reliability in a key Southern Hemisphere port.

Report Scope

Report Features Description Market Value (2025) USD 8.1 Billion Forecast Revenue (2035) USD 10.8 Billion CAGR (2026-2035) 2.9% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Base Oil (Mineral Oil, Synthetic Oil, Bio-based Oil), By Product Type (Engine Oil, Hydraulic Fluid, Compressor Oil, Others), By Ship Type (Bulk Carriers, Tankers, Container Ships, Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA Competitive Landscape BP p.l.c., Chevron Corporation, Exxon Mobil Corporation, Shell plc, TotalEnergies SE, Petronas, LUKOIL, Idemitsu Kosan Co., Ltd, China Petroleum & Chemical Corporation, ENEOS Holdings, Inc. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Marine Lubricants MarketPublished date: January 2026add_shopping_cartBuy Now get_appDownload Sample

Marine Lubricants MarketPublished date: January 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- BP p.l.c.

- Chevron Corporation

- Exxon Mobil Corporation

- Shell plc

- TotalEnergies SE

- Petronas

- LUKOIL

- Idemitsu Kosan Co., Ltd

- China Petroleum & Chemical Corporation

- ENEOS Holdings, Inc.

Our Clients

- 179416

- January 2026