Global Hair Color Market Size, Share, Growth Analysis By Ingredients (Non-organic, Organic), By Product (Permanent, Temporary, Others), By Formulation (Cream, Powder, Liquid, Others), By End User (Women, Men), By Distribution Channel (Offline, Online), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Feb 2026

- Report ID: 179516

- Number of Pages: 395

- Format:

-

keyboard_arrow_up

Quick Navigation

- Report Overview

- Key Takeaways

- Ingredients-Based Analysis

- Product-Based Analysis

- Formulation-Based Analysis

- End User-Based Analysis

- Distribution Channel-Based Analysis

- Key Market Segments

- Drivers

- Restraints

- Growth Factors

- Emerging Trends

- Regional Analysis

- Key Regions and Countries

- Key Company Insights

- Recent Developments

- Report Scope

Report Overview

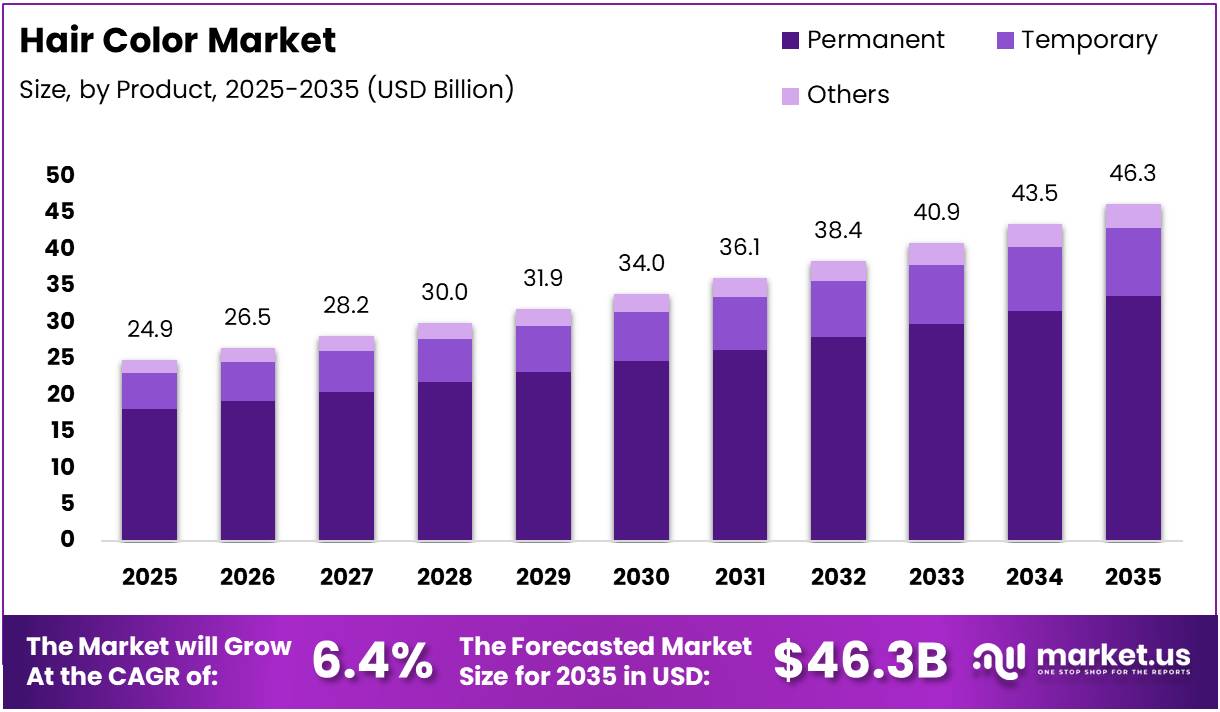

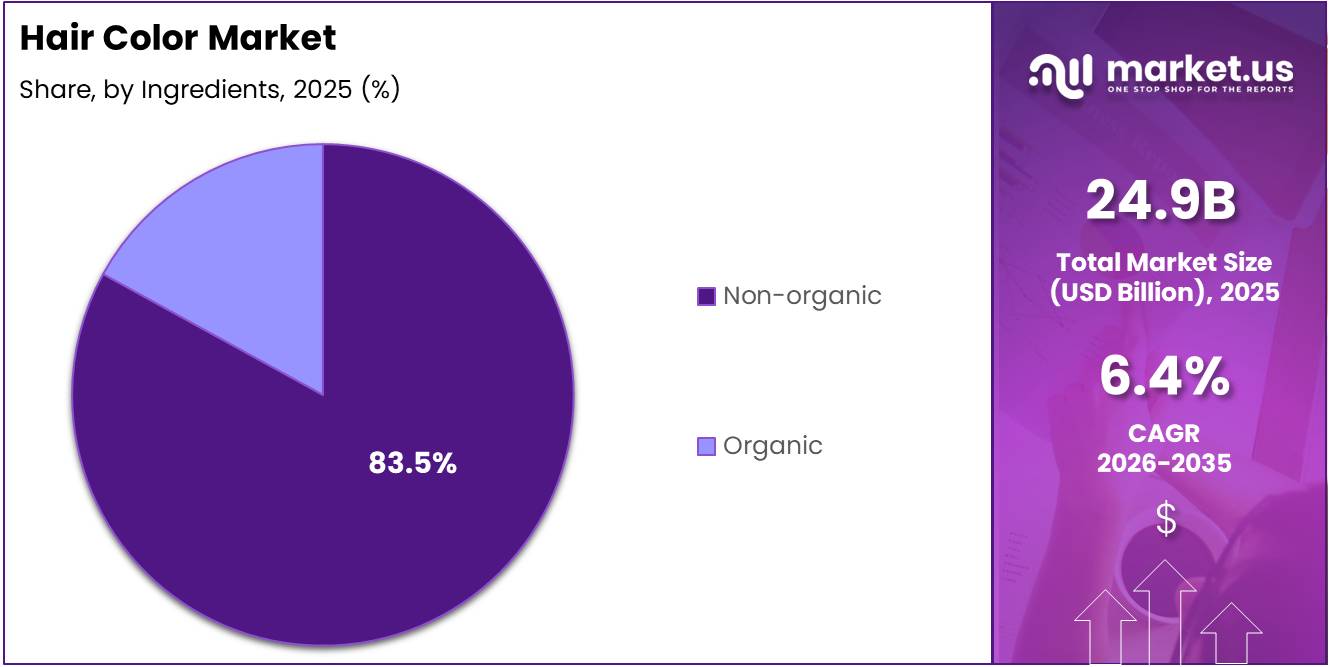

The Global Hair Color Market size is expected to be worth around USD 46.3 Billion by 2035 from USD 24.9 Billion in 2025, growing at a CAGR of 6.4% during the forecast period 2026 to 2035.

The hair color market refers to the global industry that produces and distributes products used to change, enhance, cover, or restore hair color. These products include permanent dyes, semi-permanent formulas, temporary colors, bleaches, and conditioning color treatments. The market serves both individual consumers and professional salon channels across all regions.

Growing consumer interest in personal grooming and aesthetic self-expression is a core driver of this market. Premature graying among younger populations has further increased demand for effective color solutions. Additionally, product innovations including ammonia-free and multi-dimensional formulas are attracting a broader and more diverse consumer base.

The market is supported by strong global expansion in both offline retail and e-commerce distribution. Manufacturers are investing in organic and plant-based alternatives to meet shifting consumer preferences toward safer, cleaner beauty products. Moreover, premium positioning and personalized shade matching are expanding revenue opportunities across established and emerging markets.

Government bodies in Europe and North America have implemented stricter safety regulations on chemical ingredients used in hair color formulations. Regulatory agencies require comprehensive ingredient disclosure and compliance with established safety thresholds. Consequently, these guidelines are accelerating industry shifts toward gentler, better-labeled, and more transparent product formulations.

According to Wikipedia, hair coloring is widely practiced, with 50 to 80% of women in the United States, Europe, and Japan reported using hair dye. According to the European Commission, over 60% of women in the European Union dye their hair, while 5 to 10% of men do the same.

According to ResearchGate, in Denmark, 74.9% of women and 18.4% of men had at some point dyed their hair, with the median age for first use occurring during the teenage years. Additionally, according to Cosmetic Business, 35% of Germans prefer brown hair on themselves, closely followed by blonde at 32%.

Key Takeaways

- The global Hair Color Market is valued at USD 24.9 Billion in 2025 and is projected to reach USD 46.3 Billion by 2035.

- The market is expected to grow at a CAGR of 6.4% during the forecast period 2026 to 2035.

- By Ingredients, Non-organic holds the dominant position with a market share of 83.5% in 2025.

- By Product, Permanent hair color leads the segment with a 72.8% market share in 2025.

- By Formulation, Cream formulations dominate with a 54.3% share in 2025.

- By End User, Women account for the largest segment with a 73.7% market share in 2025.

- By Distribution Channel, Offline channels hold a dominant 73.9% share in 2025.

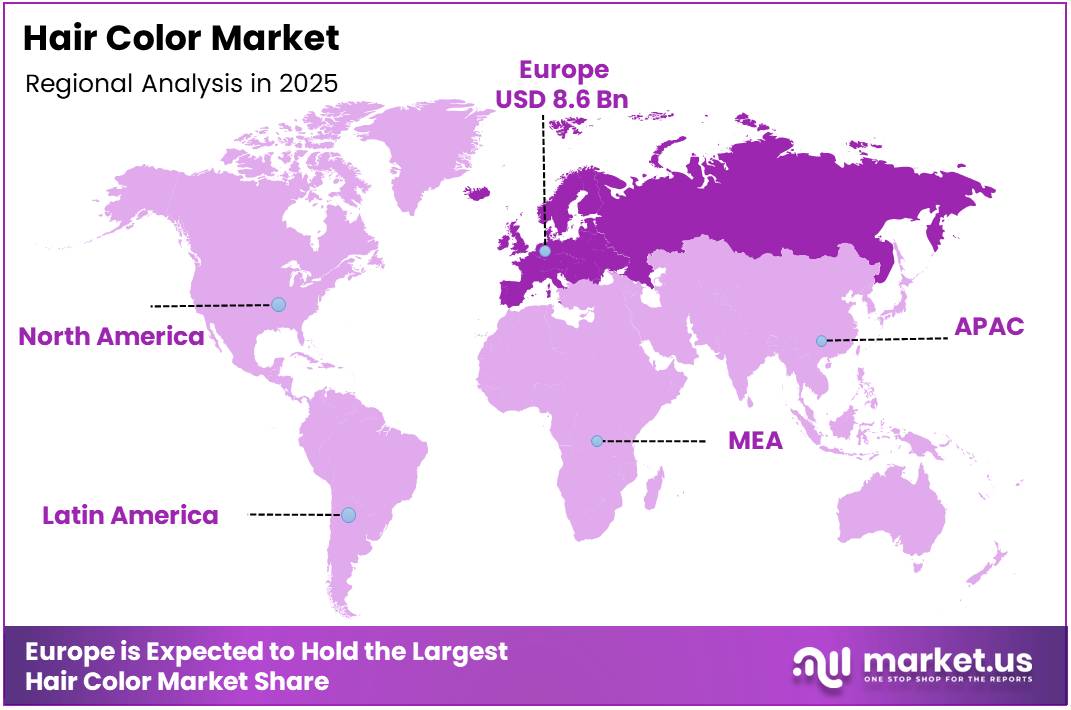

- Europe leads the regional landscape with a market share of 34.70%, valued at USD 8.6 Billion in 2025.

Ingredients-Based Analysis

Non-organic dominates with 83.5% due to widespread availability, proven color performance, and affordability.

In 2025, Non-organic held a dominant market position in the By Ingredients segment of the Hair Color Market, with a 83.5% share. These products offer a wide variety of shades, reliable color longevity, and cost-effective pricing. Moreover, their deep-rooted retail availability and established manufacturing infrastructure continue to reinforce their leadership across all major markets.

Organic hair color segment, while smaller in share, is growing at a notable pace. Consumers are increasingly drawn to plant-based and chemical-free formulations due to health, safety, and sustainability concerns. Consequently, brands are expanding their organic portfolios with improved shade variety and gentler ingredient profiles to address this rising wellness-driven demand.

Product-Based Analysis

Permanent dominates with 72.8% due to long-lasting results and strong consumer preference for durable color solutions.

In 2025, Permanent hair color held a dominant market position in the By Product segment of the Hair Color Market, with a 72.8% share. Permanent products deliver full gray coverage and lasting color, making them the preferred choice for most consumers. Additionally, continuous innovations in damage-reducing and conditioning formulas have further strengthened this segment’s market dominance.

Temporary hair color is gaining significant consumer interest, particularly among younger demographics seeking bold, fashion-forward looks without long-term commitment. These products are widely used for events, festivals, and seasonal trends. Moreover, the rise of at-home DIY kits has made temporary color more accessible and appealing to a broader audience.

Others sub-segment includes semi-permanent dyes, glazes, and color-depositing treatments. These products appeal to consumers seeking a middle ground between full commitment and completely washable color. Therefore, this category is expanding steadily, supported by growing demand for low-damage, transitional color solutions in both salon and retail settings.

Formulation-Based Analysis

Cream dominates with 54.3% due to ease of application, smooth consistency, and widespread consumer preference.

In 2025, Cream held a dominant market position in the By Formulation segment of the Hair Color Market, with a 54.3% share. Cream formulations are favored for their easy application, minimal drip, and uniform color coverage. Additionally, their compatibility with conditioning agents makes them a preferred format among both professional stylists and at-home users.

Powder formulations are commonly used in bleaching and lightening applications. They are preferred by professional colorists for their precision and higher lifting capacity. However, powder formats require careful mixing and application techniques, which limits their adoption among general consumers compared to ready-to-use cream or liquid alternatives.

Liquid hair color formulations offer quick penetration and are widely used for rinses and semi-permanent applications. They are easy to distribute evenly and often used for glossing treatments. Consequently, liquid formats appeal to consumers seeking lighter, temporary color enhancement without heavy chemical processing or long development times.

Others category includes gel, foam, and spray-based formulations. These formats are gaining popularity for their user-friendly application and minimal mess. Moreover, foam and spray colors are particularly well-suited for at-home use, and their growing consumer adoption is expanding product variety within the broader hair color formulation landscape.

End User-Based Analysis

Women dominate with 73.7% due to historically higher consumption and wider product range tailored to female consumers.

In 2025, Women held a dominant market position in the By End User segment of the Hair Color Market, with a 73.7% share. Women represent the largest consumer base, driven by strong grooming habits, fashion trends, and the desire for gray coverage. Moreover, a wider range of shades and formulas specifically designed for women reinforces their leading market position.

Men segment is growing steadily as grooming awareness rises across global markets. Increasing acceptance of hair coloring among men, combined with targeted product lines for gray coverage and natural-looking results, is driving this growth. Consequently, brands are launching gender-specific and gender-neutral hair color products to capture the expanding male consumer segment.

Distribution Channel-Based Analysis

Offline dominates with 73.9% due to strong salon presence, product trials, and established retail infrastructure.

In 2025, Offline held a dominant market position in the By Distribution Channel segment of the Hair Color Market, with a 73.9% share. Physical stores, salons, supermarkets, and specialty beauty retailers continue to be the primary purchase points for hair color products. Moreover, in-store consultations and product sampling experiences contribute significantly to offline channel dominance.

Online distribution channel is growing rapidly, supported by expanding e-commerce platforms and direct-to-consumer brand strategies. Consumers increasingly prefer the convenience of online shopping, along with access to wider product ranges and competitive pricing. Therefore, brands are investing in digital retail capabilities and subscription-based models to capture the growing online consumer base.

Key Market Segments

By Ingredients

- Non-organic

- Organic

By Product

- Permanent

- Temporary

- Others

By Formulation

- Cream

- Powder

- Liquid

- Others

By End User

- Women

- Men

By Distribution Channel

- Offline

- Online

Drivers

Rising Consumer Demand for Grooming, Gray Coverage, and Innovative Hair Color Technologies Drives Market Growth

Growing consumer inclination toward personal grooming and aesthetic self-expression is a primary driver of the hair color market. Across all age groups, individuals are increasingly using hair color as a tool for identity and style. Moreover, increased social media influence and beauty content have significantly heightened awareness and purchase intent globally.

The rising prevalence of premature graying, particularly among younger adults, has created strong and consistent demand for effective gray coverage solutions. Consumers are actively seeking products that deliver natural-looking, long-lasting results. Consequently, manufacturers are developing advanced formulations that target this need while simultaneously reducing hair damage and improving scalp health.

Continuous innovation in ammonia-free, conditioning, and multi-dimensional hair color technologies is attracting new consumer segments. These advancements address longstanding concerns about chemical damage and allergic reactions. Therefore, next-generation formulations that combine vibrant color performance with hair care benefits are expanding the overall appeal and accessibility of hair color products worldwide.

Restraints

Chemical Safety Concerns and Regulatory Compliance Challenges Restrain Hair Color Market Growth

Consumer concerns about hair damage, allergic reactions, and long-term exposure to chemical ingredients remain a significant barrier to market growth. Many users report scalp sensitivity and adverse reactions following prolonged use of conventional hair dyes. Consequently, these concerns are limiting repeat purchases and encouraging some consumers to seek alternatives or reduce coloring frequency.

Stringent regulatory restrictions on chemical ingredients used in hair color products present considerable compliance challenges for manufacturers. Regulatory bodies in Europe, North America, and other regions enforce strict guidelines on the use of certain compounds, including resorcinol and paraphenylenediamine. Additionally, evolving compliance requirements add to formulation costs and extend product development timelines significantly.

The dual pressure of consumer safety demands and regulatory oversight requires continuous reformulation investment from manufacturers. Smaller brands in particular face significant financial and technical barriers in meeting these requirements. Therefore, regulatory complexity and compliance costs are acting as restraining factors, especially for emerging and mid-market players seeking to compete in this space.

Growth Factors

Natural Formulations, AI-Driven Personalization, and Men’s Grooming Expansion Accelerate Market Growth

The expansion of natural, organic, and plant-based hair color formulations is a major growth opportunity for the market. Consumer preference for cleaner beauty products is driving manufacturers to innovate with botanical ingredients and reduced chemical profiles. Moreover, the natural hair dye growing appeal is attracting new consumer groups previously hesitant to use conventional hair dye products.

The rapid growth of personalized and AI-driven custom shade matching solutions is transforming the hair color industry. Technology-enabled tools allow consumers to find their ideal shade digitally before purchasing, improving satisfaction and reducing returns. Consequently, brands investing in digital personalization platforms are gaining a competitive edge in both online and in-store retail environments.

Rising demand for men’s grooming products and gender-neutral hair color solutions is opening a significant untapped growth segment. As grooming norms evolve globally, men are increasingly comfortable exploring hair color options. Therefore, brands that develop targeted, easy-to-use formulations for male and gender-neutral consumers are well-positioned to capture substantial incremental market share.

Emerging Trends

Fashion Colors, DIY Kits, and Multi-Benefit Formulations Reshape the Hair Color Market Landscape

The surge in demand for bold, pastel, and temporary fashion hair colors is reshaping the market. Younger consumers in particular are embracing vibrant shades as a form of personal expression. Moreover, seasonal and event-driven color trends are driving repeat purchases and encouraging experimentation among consumers who prefer non-permanent, low-commitment options.

The increasing popularity of at-home DIY hair color kits offering salon-quality results is transforming consumer behavior. Technological improvements in kit formulations and application tools have made professional-level color more accessible and affordable. Consequently, a growing number of consumers are shifting from salon services to home use, expanding the direct-to-consumer segment of the market.

Integration of bond-building, repair, and scalp-care benefits within hair color products is a fast-growing trend addressing consumer demand for multifunctional solutions. Brands are increasingly combining color with conditioning, protein-repair, and scalp-soothing properties in a single product. Therefore, these value-added formulations are gaining strong traction among health-conscious consumers who want color without sacrificing hair integrity.

Regional Analysis

Europe Dominates the Hair Color Market with a Market Share of 34.70%, Valued at USD 8.6 Billion

Europe holds the leading position in the global hair color market, accounting for a 34.70% share valued at USD 8.6 Billion in 2025. The region’s dominance is driven by high consumer grooming standards, strong salon culture, and well-established retail channels. Additionally, stringent EU regulations are pushing innovation toward safer, higher-quality product formulations across the region.

North America Hair Color Market Trends

North America is a key market for hair color products, supported by high consumer spending on beauty and personal care. The United States leads regional demand, driven by a strong culture of self-expression and the growing popularity of at-home coloring. Moreover, the expansion of premium and organic product lines is further fueling market value in this region.

Asia Pacific Hair Color Market Trends

Asia Pacific is the fastest-growing region in the global hair color market, led by China, Japan, South Korea, and India. Rising disposable incomes, urbanization, and increasing beauty consciousness are driving product adoption. Consequently, international and domestic brands are expanding their presence across this region with locally tailored shades and formulations.

Latin America Hair Color Market Trends

Latin America represents a growing market for hair color, with Brazil and Mexico as the primary revenue contributors. A strong beauty culture and increasing middle-class spending power are supporting market expansion. However, economic volatility and import dependency for premium products present ongoing challenges for consistent growth across the region.

Middle East and Africa Hair Color Market Trends

The Middle East and Africa market is developing steadily, supported by a young and growing population with rising beauty awareness. GCC countries, particularly Saudi Arabia and the UAE, show strong demand for premium and professional-grade products. Additionally, increasing retail infrastructure and e-commerce adoption are improving product accessibility across both urban and developing markets in the region.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Coty Inc. is a global beauty company with a significant presence in the hair color segment through its broad brand portfolio. The company focuses on mass-market and professional hair color solutions. Moreover, Coty’s distribution strength across multiple retail and salon channels positions it as a key competitive player in the global hair color market.

L’Oréal S.A. is one of the world’s largest beauty companies and a dominant force in the hair color industry. The company operates across professional, mass, and luxury segments, offering a comprehensive range of coloring solutions. Additionally, L’Oréal’s strong investment in research and development continues to produce innovative, high-performance hair color technologies.

Estée Lauder Companies Inc. maintains a premium positioning within the beauty and hair care sector. While primarily known for skincare and cosmetics, the company’s portfolio includes hair care and color-adjacent products that serve the high-end consumer market. Furthermore, its global distribution network and strong brand equity support continued expansion in the premium personal care space.

Revlon, Inc. has long been recognized as a key player in the consumer hair color market with its widely accessible product lines. The brand serves a broad demographic with affordable and reliable coloring options available through mass retail channels. Consequently, Revlon’s established consumer trust and wide retail reach continue to support its competitive position in the market.

Key Players

- Coty Inc.

- L’Oréal S.A.

- Estée Lauder Companies Inc.

- Revlon, Inc.

- Avon Products Inc.

- Unilever PLC

- Shiseido Company, Limited

- Godrej

- Procter & Gamble

- Combe Inc.

Recent Developments

- February 2026 – Manic Panic launched Inter-Gel-Actic™, described as the hair color collection of the future, marking the brand’s first ever complete DIY Box Set offering consumers an all-in-one at-home professional coloring experience.

- January 2026 – Sally Beauty debuted ion® 24K, an advanced haircare collection powered by proprietary TRICHOPOWER™ science, designed to deliver enhanced hair strength, shine, and color vibrancy for professional-quality results at home.

- December 2025 – Coty Inc. sold its remaining stake in Wella in a $750 Million deal with KKR, completing its full exit from the professional hair care brand and allowing the company to refocus its investment strategy on core beauty categories.

- August 2025 – Arctic Fox partnered with Dye Candy in a limited-edition collaborative collection, combining bold fashion color expertise from both brands to deliver a highly anticipated co-branded hair color range targeting trend-driven consumers.

- July 2025 – L’Oréal acquired Color Wow, a fast-growing professional haircare brand known for its innovative styling and treatment products, strengthening L’Oréal’s portfolio in the premium hair care and color-adjacent product categories.

Report Scope

Report Features Description Market Value (2025) USD 24.9 Billion Forecast Revenue (2035) USD 46.3 Billion CAGR (2026-2035) 6.4% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Ingredients (Non-organic, Organic), By Product (Permanent, Temporary, Others), By Formulation (Cream, Powder, Liquid, Others), By End User (Women, Men), By Distribution Channel (Offline, Online) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Coty Inc., L’Oréal S.A., Estée Lauder Companies Inc., Revlon, Inc., Avon Products Inc., Unilever PLC, Shiseido Company, Limited, Godrej, Procter & Gamble, Combe Inc. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- Coty Inc.

- L'Oréal S.A.

- Estée Lauder Companies Inc.

- Revlon, Inc.

- Avon Products Inc.

- Unilever PLC

- Shiseido Company, Limited

- Godrej

- Procter & Gamble

- Combe Inc.

Our Clients

- 179516

- Feb 2026