Global Fracking Chemicals And Fluids Market Size, Share and Report Analysis By Product (Water Based Fluids, Oil Based Fluids, Synthetic Based Fluids, Foam Based Fluids), By Well Type (Horizontal Well, Vertical Well), By Application (Friction Reducer, Clay Control Agent, Gelling Agent, Cross-Linkers, Breakers, Others) , By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2025-2035

- Published date: Mar 2026

- Report ID: 179872

- Number of Pages: 368

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

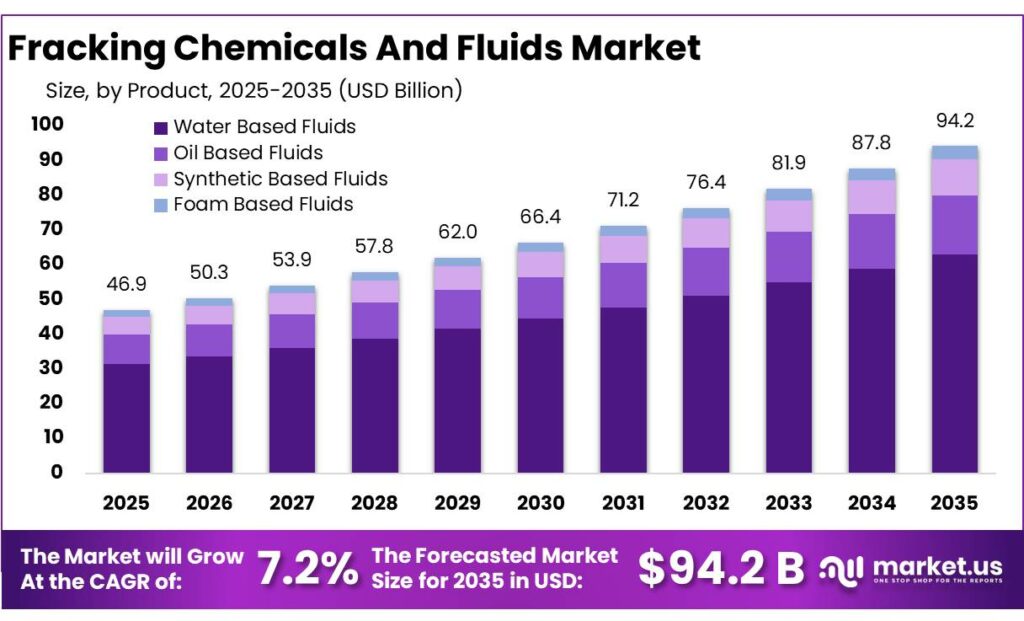

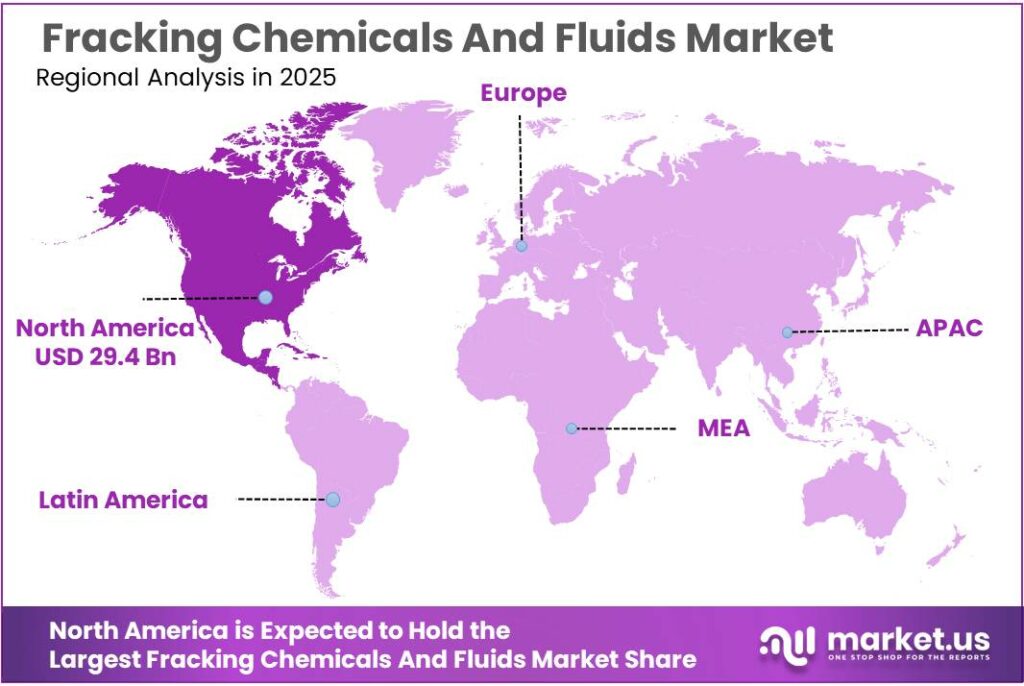

The Global Fracking Chemicals And Fluids Market is expected to be worth around USD 94.2 Billion by 2035, up from USD 46.9 Billion in 2025, at a CAGR of 7.2% from 2026 to 2035. The North America segment maintained 62.8%, supporting a Fracking Chemicals And Fluids value of USD 29.4 Bn.

The fracking chemicals and fluids industry sits at the heart of the modern unconventional oil and gas value chain, supplying water-based, oil-based and synthetic formulations that carry proppants, control friction, inhibit corrosion and manage reservoir chemistry. The scale of hydraulic fracturing activity is immense.

- According to the U.S. Energy Information Administration (EIA), U.S. shale gas production in the Haynesville play alone averaged 14.6 billion cubic feet per day in 2023, equal to about 14% of total U.S. dry natural gas output, underlining the large and sustained demand for stimulation fluids in key basins.

At the well level, studies cited by the U.S. Environmental Protection Agency (EPA) indicate that a single shale gas well typically requires between 2.3 and 3.8 million gallons of water for fracturing operations, and in some regions average use has risen above 5 million gallons per frack, driving strong volume pull for chemical additives that are dosed per unit of fluid.

Industrial dynamics are closely tied to shale development in North America and, increasingly, in emerging plays such as Saudi Arabia’s Jafurah Basin. In the United States, the EIA reports that associated natural gas production increased by 7.9% in 2023 to an average of 17.1 billion cubic feet per day, largely from tight oil fields that rely on intensive fracturing campaigns.

- The International Energy Agency (IEA) projects that global oil demand will increase by around 2.5 million barrels per day between 2024 and 2030, reaching roughly 105.5 million barrels per day, while production capacity rises to about 114.7 million barrels per day by 2030.

Key demand drivers for fracking chemicals and fluids include regional gas transition policies and energy-security agendas. For example, the IEA forecasts India’s natural gas demand to rise nearly 60% by 2030 compared with current levels, as infrastructure and policy support shift the fuel mix towards gas; this underpins interest in domestic unconventional resources and associated fracturing-fluid supply chains.

In the U.S., the EIA’s Annual Energy Outlook projects natural gas production to peak around 119.0 Bcf/d in 2032, with demand peaking at 92.4 Bcf/d in the same year; such long-term plateaus still imply sustained drilling and completion activity requiring large volumes of water and chemicals per well.

Key Takeaways

- Fracking Chemicals And Fluids Market is expected to be worth around USD 94.2 Billion by 2035, up from USD 46.9 Billion in 2025, at a CAGR of 7.2%.

- Water Based Fluids held a dominant market position, capturing more than a 67.3% share.

- Horizontal Well held a dominant market position, capturing more than an 81.2% share.

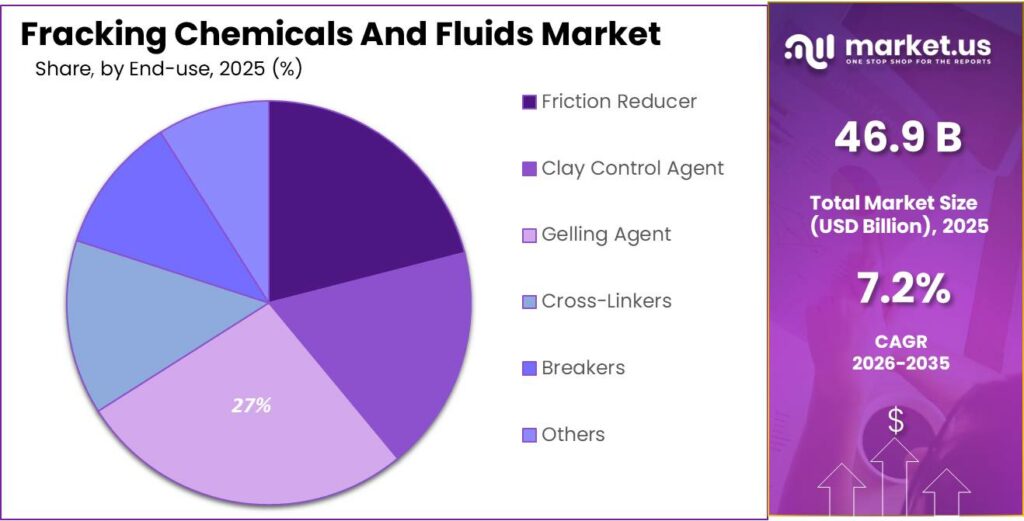

- Gelling Agent held a dominant market position, capturing more than a 27.4% share.

- North America stands as the dominant region, accounting for 62.8% of global revenues, equivalent to about USD 29.4 billion.

By Product Analysis

Water Based Fluids lead the market with a strong 67.3% share in 2024

In 2024, Water Based Fluids held a dominant market position, capturing more than a 67.3% share, reflecting their continued preference across major shale basins and tight-oil fields. This segment maintained its strength largely because water-based systems offer easier handling, lower environmental impact, and better cost control compared with oil-based or synthetic alternatives.

Operators in regions such as North America, China, and the Middle East continued to increase their use of slickwater and gel-based formulations for both new well completions and refracturing work. Their ability to support high-rate pumping, improve proppant transport, and reduce overall friction loss kept them as the first choice for large-volume fracturing jobs.

By Well Type Analysis

Horizontal Wells dominate with 81.2% share as operators prioritize deeper and longer shale development

In 2024, Horizontal Well held a dominant market position, capturing more than an 81.2% share, showing how strongly the global fracking industry depends on long-reach horizontal drilling to unlock shale gas and tight-oil formations. Most new unconventional wells drilled in regions such as the U.S., Canada, China, and parts of the Middle East followed the horizontal format because it allows operators to stimulate much larger contact areas, reduce the number of surface locations, and boost hydrocarbon recovery from deeper layers.

This high share reflects a clear operational shift—producers increasingly focus on multi-stage fracturing across extended laterals that can now exceed several kilometers, leading to significantly higher usage of fracking chemicals and fluids per well.

By Application Analysis

Gelling Agents lead the market with 27.4% share due to their strong role in fluid performance

In 2024, Gelling Agent held a dominant market position, capturing more than a 27.4% share, highlighting their essential role in improving the viscosity and stability of fracking fluids during high-pressure operations. These agents—commonly derived from guar, modified polymers, or synthetic formulations—help suspend and carry proppants deep into the rock formation, which is critical for keeping fractures open and improving long-term hydrocarbon flow.

Their strong presence in the market also reflects the widespread use of gel-based and crosslinked fluid systems across shale basins, where operators need reliable viscosity control to handle deeper wells, longer laterals, and complex multi-stage fracturing designs.

Key Market Segments

By Product

- Water Based Fluids

- Oil Based Fluids

- Synthetic Based Fluids

- Foam Based Fluids

By Well Type

- Horizontal Well

- Vertical Well

By Application

- Friction Reducer

- Clay Control Agent

- Gelling Agent

- Cross-Linkers

- Breakers

- Others

Emerging Trends

Fracking moves toward ‘water-smart’ and cleaner chemical systems

One of the strongest recent trends in fracking chemicals and fluids is a shift toward water-smart, lower-toxicity formulations, driven by concern over water scarcity and its impact on food production. Around the world, agriculture already takes the largest share of water: FAO and UN water reports show that farming accounts for about 70–72% of global freshwater withdrawals. In low-income countries this share is even higher, reaching about 90% of all water withdrawals, according to a World Bank analysis of food and water use.

These pressures are not theoretical. UN-backed assessments warn that the world is sliding into a kind of “water bankruptcy”. A recent United Nations University report estimates that nearly 75% of the global population now lives in countries classified as water-insecure or critically water-insecure, and about 4 billion people face severe water scarcity for at least one month every year. The same report notes that more than 170 million hectares of irrigated farmland are under high water stress and that the economic impact of land degradation and water mismanagement exceeds USD 300 billion a year, disrupting more than half of global food production.

UN Environment Programme has explicitly warned that fracking can compete with land and water needed for food production, highlighting risks from chemicals released into air, soil and water. At the same time, FAO and World Bank data show how much is at stake: irrigated land represents only about 20% of global cropland, yet this small share produces around 40% of the world’s food.

Drivers

Rising natural gas demand keeps fracking chemicals and fluids in high gear

One of the clearest driving forces for fracking chemicals and fluids is the steady rise in natural gas demand and production, especially from shale and tight formations. Around the world, gas is being used as a “bridge fuel” to support economic growth while countries try to cut coal use and lower emissions. The International Energy Agency (IEA) estimates that global natural gas demand reached a new all-time high in 2024, increasing by about 2.7%, or 115 billion cubic metres (bcm) in a single year.

- On the supply side, producers are responding with record levels of gas output that rely heavily on hydraulic fracturing. In the United States, the Energy Information Administration (EIA) reports that dry natural gas production climbed from 103.1 billion cubic feet per day (Bcf/d) in 2024 to 107.7 Bcf/d in 2025, a rise of about 4.5% in just one year. This was the highest annual production level since the EIA began tracking the data.

Government policies are reinforcing this pattern. In India, for example, the government has set an ambitious goal to raise the share of natural gas in the primary energy mix to 15% by 2030, up from about 6% in 2022, according to an IEA report prepared with the support of the Ministry of Petroleum and Natural Gas. The same analysis notes that India’s gas demand is expected to grow by nearly 60% between 2023 and 2030, driven by city gas distribution, industry and fertiliser plants.

The scale of fracking in mature markets also keeps the base level of chemical demand high. Industry data compiled by the Colorado Oil & Gas Association, drawing on official sources, show that over 95% of wells in the United States are hydraulically fractured at some point in their lifetime. Earlier EIA analysis found that by 2015, hydraulically fractured wells were already contributing more than 4.3 million barrels per day of oil, about 50% of total U.S. oil output at the time.

Restraints

Growing environmental and regulatory concerns over chemical contamination slow fracking market progress

One of the most significant restraining factors for the fracking chemicals and fluids industry today is the increasing environmental concern and regulatory scrutiny related to how these chemicals interact with water resources and ecosystems. Hydraulic fracturing fluid is largely water mixed with a variety of chemical additives.

In shale gas operations, water makes up around 97% of the fluid, but that small percentage of chemicals can still amount to hundreds of thousands of litres injected into the ground at each well due to the millions of litres of fluid used per job.

The United States Environmental Protection Agency (EPA) has long studied the potential for fracking activities to affect drinking water resources. In its comprehensive assessment, the EPA acknowledged that hydraulic fracturing can impact drinking water resources under certain conditions, such as spills during handling, poor well integrity, or inadequate wastewater treatment.

Chemical transparency itself remains a major issue. Analyses of disclosure data submitted to chemical tracking systems showed that over 70% of fracking chemical forms listed at least one substance as “confidential business information,” and an estimated 1,084 unique chemicals were reported used in fracking formulations over a multi-year period.

In some cases, environmental activists and food and water advocacy organizations have called for sweeping bans or stricter controls over shale gas development due to these concerns. For example, Food & Water Europe and allied groups pushed for a full EU-wide ban on shale gas extraction, gathering signatures from 1,250 anti-fracking organizations globally to support their message that fracking risks outweigh potential benefits.

Opportunity

Growing gas demand for food and fertilizer creates new space for fracking chemicals and fluids

A powerful growth opportunity for fracking chemicals and fluids sits at the intersection of energy and food. Modern agriculture runs on nitrogen and phosphate fertilizers, and those fertilizers, in turn, are built on natural gas. The Food and Agriculture Organization (FAO) notes that natural gas is a key building block for all nitrogen fertilizers and for two of the most widely used phosphate products, mono-ammonium phosphate (MAP) and di-ammonium phosphate (DAP).

- A recent FAO-linked market update explains that about 80% of global ammonia production — roughly 152 million tonnes — is processed into fertilizers that support global crop yields.

Natural gas demand is rising fastest in large, fast-growing economies that are also worried about feeding more people. India is a clear example. The International Energy Agency (IEA) projects that India’s natural gas consumption will grow by nearly 60% between 2023 and 2030, reaching around 103 billion cubic metres per year by the end of the decade. Much of that growth is expected to come from city-gas networks, industry and fertilizer plants.

On the supply side, producing countries are responding with record gas output, much of it from shale and tight reservoirs that cannot flow without hydraulic fracturing. In the United States, dry natural gas production increased 4.5% in 2025, rising from 103.1 billion cubic feet per day (Bcf/d) in 2024 to 107.7 Bcf/d, according to the U.S. Energy Information Administration. That is the highest annual level since records began in 1930 and underlines how deeply fracking is embedded in the gas system.

- In China, domestic shale gas production averaged 2.51 Bcf/d in 2023, up sharply from just 0.02 Bcf/d in 2013, as companies improved their understanding of shale formations and deployed more advanced hydraulic fracturing techniques.

Regional Insights

North America dominates fracking chemicals and fluids with 62.8% share and USD 29.4 Bn value

In the Fracking Chemicals and Fluids Market, North America stands as the dominant region, accounting for 62.8% of global revenues, equivalent to about USD 29.4 billion, reflecting the region’s deep reliance on shale gas and tight oil development. The United States is at the center of this dominance: the U.S. Energy Information Administration (EIA) reports that dry natural gas production reached around 118–120 billion cubic feet per day (Bcf/d) in 2024, with shale gas and tight formations providing the majority of that output.

Policy frameworks that support domestic energy security, LNG export growth, and industrial gas use keep drilling and completion activity structurally elevated, even through commodity cycles. At the same time, stronger environmental expectations in North America push service companies to introduce lower-toxicity, water-efficient fluid chemistries, which adds value intensity per well.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Akzo Nobel N.V. plays a steady role in supplying specialty chemicals used in friction reducers, clay control agents and additives for fracking fluids. The company operates in more than 150 countries, supported by over 33,000 employees and annual revenues above €10 billion. Its chemical portfolio helps improve fluid stability and performance in shale operations. The company’s R&D spending consistently exceeds €250 million per year, helping it introduce cleaner and more efficient formulations for oilfield applications.

Pioneer Engineering Services focuses on manufacturing and supplying equipment and precision-engineered components that support drilling and fracking operations. The company maintains production facilities with capacities exceeding 10,000 units per year across pumps, valves and engineered parts used in fluid handling. With over 25 years in industrial engineering and exports reaching more than 30 countries, Pioneer supports the fracking chemical ecosystem by enabling reliable mixing, pumping and deployment systems. Its workforce of 500+ employees continues expanding capabilities for energy-sector clients.

SLB remains a global leader in stimulation chemicals, slickwater systems and high-performance gelling technologies. With operations in 120 countries and revenues above $33 billion, SLB supports thousands of horizontal wells annually. The company employs more than 99,000 staff worldwide and invests over $1 billion in R&D to improve fluid efficiency, proppant transport and environmental safety. Its stimulation technology centers develop advanced additives that help operators reduce water use and minimize chemical footprints in complex shale reservoirs.

Top Key Players Outlook

- Akzo Nobel N.V.

- Pioneer Engineering Services.

- Halliburton Company

- Dow

- SLB

- Baker Hughes Company

- BASF

- DuPont

Recent Industry Developments

In 2024, Halliburton reported total annual revenue of USD 22.9 billion, with its fluids and stimulation technologies playing a key role in the Completion and Production segment that accounted for more than $12 billion of the business, showing how central these solutions are to its operations.

In 2024, Dow delivered about $43 billion in sales, reflecting its scale and diversified chemicals business.

Report Scope

Report Features Description Market Value (2025) USD 46.9 Bn Forecast Revenue (2035) USD 94.2 Bn CAGR (2026-2035) 7.2% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product (Water Based Fluids, Oil Based Fluids, Synthetic Based Fluids, Foam Based Fluids), By Well Type (Horizontal Well, Vertical Well), By Application (Friction Reducer, Clay Control Agent, Gelling Agent, Cross-Linkers, Breakers, Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA Competitive Landscape Akzo Nobel N.V., Pioneer Engineering Services., Halliburton Company, Dow, SLB, Baker Hughes Company, BASF, DuPont Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Fracking Chemicals And Fluids MarketPublished date: Mar 2026add_shopping_cartBuy Now get_appDownload Sample

Fracking Chemicals And Fluids MarketPublished date: Mar 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Akzo Nobel N.V.

- Pioneer Engineering Services.

- Halliburton Company

- Dow

- SLB

- Baker Hughes Company

- BASF

- DuPont

Our Clients

- 179872

- Mar 2026