Global Food Grade Alcohol Market Size, Share and Report Analysis By Type (Ethanol, Polyols), By Source (Molasses And Sugarcane, Fruits, Grains, Others), By Function (Coatings, Preservatives, Coloring And Flavoring Agent, Others), By Application (Healthcare And Pharmaceutical, Food, Beverages, Personal Care, Others) , By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2025-2035

- Published date: Mar 2026

- Report ID: 180227

- Number of Pages: 383

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

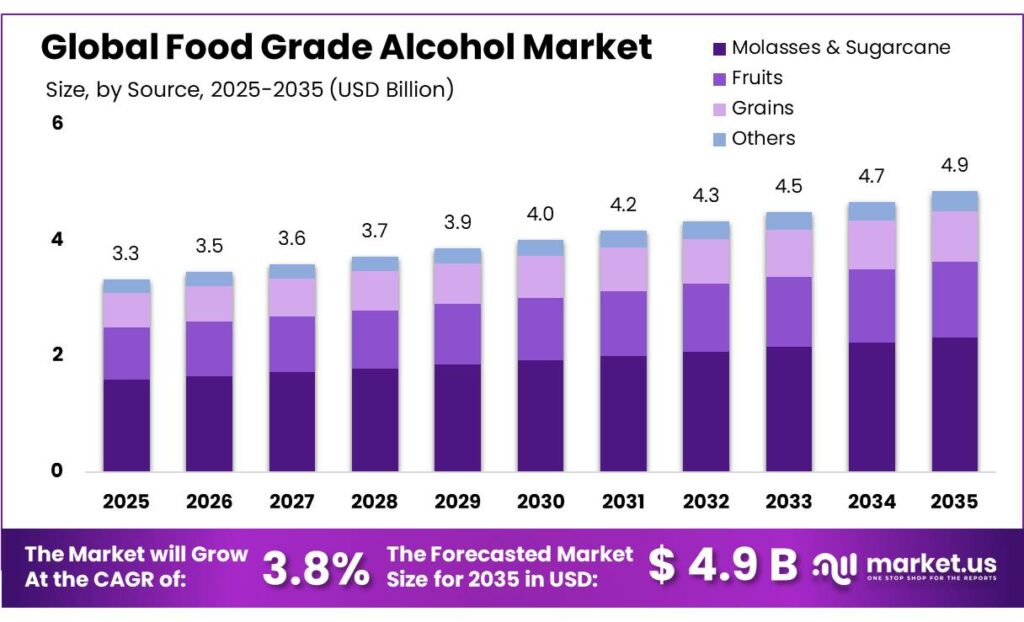

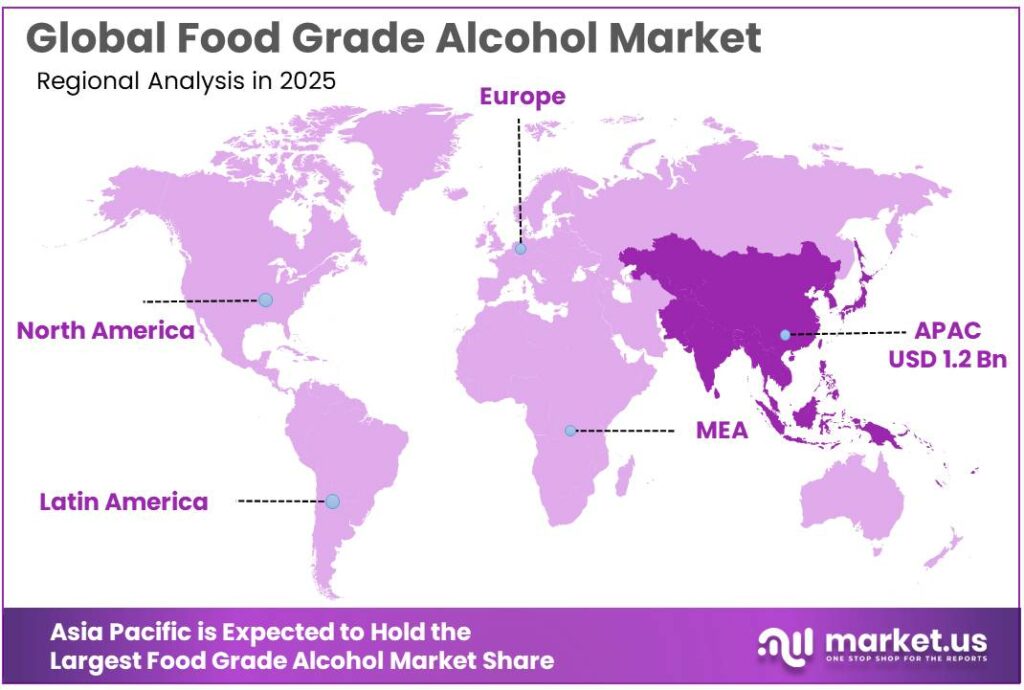

The Global Food Grade Alcohol Market is expected to be worth around USD 4.9 Billion by 2035, up from USD 3.3 Billion in 2025, at a CAGR of 3.8% from 2026 to 2035. The Asia Pacific segment maintained 39.1%, supporting a Food Grade Alcohol value of USD 1.2 Bn.

The food grade alcohol industry forms an important segment of the global fermentation and distillation sector, supplying high-purity ethanol used in food processing, beverages, pharmaceuticals, flavors, and preservatives. Food grade alcohol is typically produced through fermentation of agricultural feedstocks such as sugarcane molasses, corn, wheat, or other starch-rich crops, followed by multiple distillation and purification steps to achieve food-safe quality standards.

- According to the Food and Agriculture Organization (FAO) and OECD outlook, global ethanol production has been increasing consistently and was projected to rise from around 120 billion liters in 2017 to nearly 131 billion liters by the early 2020s, reflecting steady growth in fermentation-based alcohol production across industrial and food applications.

These industrial volumes support both fuel and food grade alcohol markets, with beverage and food applications representing a smaller but high-value share of ethanol utilization. Furthermore, the Renewable Fuels Association reported that the United States alone produced about 16,225 million gallons of ethanol in 2024, reflecting the large industrial infrastructure supporting fermentation-based alcohol production.

The demand outlook for food-grade alcohol is further supported by broader developments in global ethanol production and agricultural feedstock supply. According to projections by the Food and Agriculture Organization (FAO), global bio-ethanol production is expected to reach approximately 155 billion liters by 2034, indicating strong growth in fermentation-based alcohol production capacity worldwide. A portion of this production is used in food and beverage applications, especially for flavor extraction and beverage formulation.

Additionally, export statistics highlight the expanding scale of the ethanol industry; the U.S. ethanol sector exported about 1.91 billion gallons of ethanol in 2024, generating export revenues of nearly USD 7.5 billion, demonstrating the strong international trade of alcohol-based products and related ingredients.

Government initiatives and regulatory frameworks also play a critical role in shaping the industrial landscape of alcohol production. For example, India’s Ethanol Blended Petrol (EBP) programme aims to achieve around 20% ethanol blending with petrol by 2025, encouraging significant expansion of distillation capacity across the country. Such policies stimulate investments in ethanol plants and fermentation technologies, indirectly strengthening the supply chain for food grade alcohol as well.

Key Takeaways

- Food Grade Alcohol Market is expected to be worth around USD 4.9 Billion by 2035, up from USD 3.3 Billion in 2025, at a CAGR of 3.8%.

- Ethanol held a dominant market position, capturing more than a 86.5% share in the Food Grade Alcohol Market.

- Molasses & Sugarcane held a dominant market position, capturing more than a 48.2% share in the Food Grade Alcohol Market.

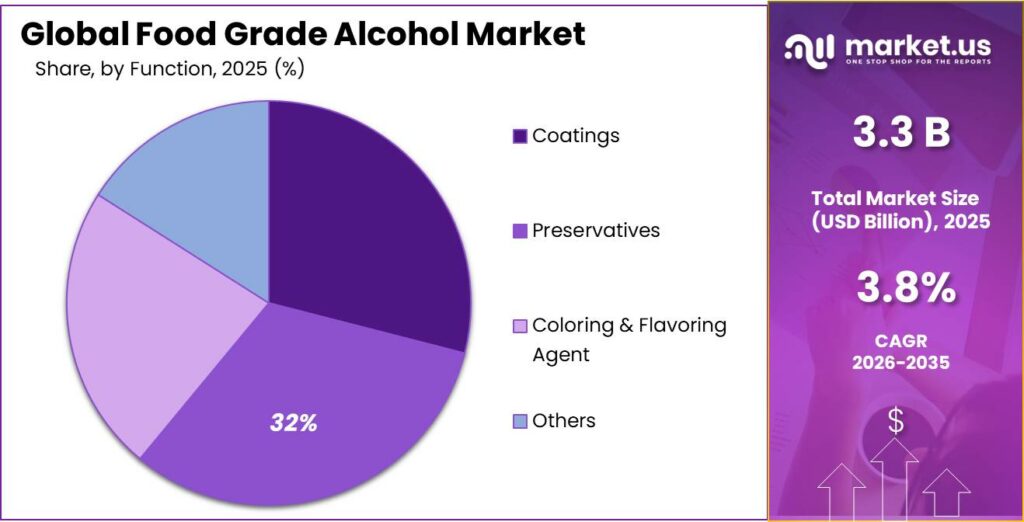

- Preservatives held a dominant market position, capturing more than a 32.8% share in the Food Grade Alcohol Market.

- Beverages held a dominant market position, capturing more than a 39.9% share in the Food Grade Alcohol Market.

- Asia Pacific region held the dominant position in the Food Grade Alcohol Market, accounting for around 39.1% share with an estimated value of about USD 1.2 billion.

By Type Analysis

Ethanol dominates with 86.5% share due to its extensive use in beverages and food processing

In 2024, Ethanol held a dominant market position, capturing more than a 86.5% share in the Food Grade Alcohol Market by type of ethanol. This strong presence is mainly linked to its widespread use across alcoholic beverages, food flavoring extracts, bakery ingredients, and food preservation processes. Ethanol is widely preferred in the food industry because of its high purity levels and its ability to dissolve and stabilize natural flavors such as vanilla, citrus, and herbal extracts. Beverage manufacturers particularly rely on ethanol as the key ingredient for producing spirits, wines, and ready-to-drink alcoholic beverages, which continue to see rising global demand.

By Source Analysis

Molasses & Sugarcane dominate with 48.2% share due to abundant agricultural availability

In 2024, Molasses & Sugarcane held a dominant market position, capturing more than a 48.2% share in the Food Grade Alcohol Market by source. This strong position is largely supported by the wide availability of sugarcane-based raw materials and the established fermentation infrastructure built around molasses processing. Molasses, a by-product of sugar production, contains high sugar content that makes it highly suitable for ethanol fermentation, allowing manufacturers to produce food-grade alcohol efficiently and at lower processing costs. Countries with strong sugar industries continue to rely on molasses as a primary feedstock for alcohol production, making it a reliable and scalable source for the food and beverage sector.

By Function Analysis

Preservatives dominate with 32.8% share due to longer shelf-life benefits in foods

In 2024, Preservatives held a dominant market position, capturing more than a 32.8% share in the Food Grade Alcohol Market by function. This leadership is mainly connected to the growing need for longer shelf life and improved product stability in processed food and beverage products. Food grade alcohol, especially ethanol, is widely used as a preservative because it helps slow down microbial growth and prevents spoilage in many food formulations. Manufacturers rely on alcohol-based preservation in products such as flavor extracts, sauces, bakery ingredients, confectionery fillings, and certain beverage concentrates where maintaining freshness is important during storage and transportation.

By Application Analysis

Beverages dominate with 39.9% share driven by strong global drink consumption

In 2024, Beverages held a dominant market position, capturing more than a 39.9% share in the Food Grade Alcohol Market by application. This leading position is mainly supported by the large-scale production of alcoholic beverages such as spirits, wines, beers, and ready-to-drink cocktails where food grade ethanol serves as a primary ingredient. Beverage manufacturers depend on high-purity alcohol to maintain product quality, flavor balance, and consistent formulation during production. As global consumer demand for premium spirits, flavored drinks, and craft beverages continues to rise, beverage companies are expanding their production capacities, which further increases the use of food grade alcohol in this segment.

Key Market Segments

By Type

- Ethanol

- Polyols

By Source

- Molasses & Sugarcane

- Fruits

- Grains

- Others

By Function

- Coatings

- Preservatives

- Coloring & Flavoring Agent

- Others

By Application

- Healthcare & Pharmaceutical

- Food

- Beverages

- Personal Care

- Others

Emerging Trends

Shift Toward Sustainable and Advanced Ethanol Production Technologies

One of the most important recent trends shaping the Food Grade Alcohol industry is the increasing focus on sustainable ethanol production and advanced fermentation technologies. Food grade alcohol, particularly ethanol, is traditionally produced from crops such as corn, wheat, and sugarcane through fermentation and distillation. However, industries and governments are now investing in more efficient and environmentally responsible production methods to improve yields and reduce the environmental footprint of alcohol manufacturing.

The global scale of ethanol production highlights why innovation in this area is becoming so important. According to the World Bioenergy Statistics Report, global ethanol production reached about 116 billion liters in 2023, making it the largest liquid biofuel produced worldwide. This massive production volume reflects the growing demand for ethanol not only in fuel markets but also in beverages, food processing, pharmaceuticals, and flavor extraction.

- Technological improvements are also influencing the future supply of ethanol. Research cited by energy and agricultural organizations indicates that global ethanol production could reach around 140 billion liters by 2024 as fermentation capacity expands and new technologies are introduced. These developments include improved yeast strains, advanced enzyme systems, and real-time monitoring of fermentation processes.

Another emerging trend is the diversification of raw materials used for ethanol production. Traditionally, most ethanol is produced from corn and sugarcane, but researchers and industries are exploring new feedstocks such as agricultural residues, lignocellulosic biomass, and waste sugars. Studies show that about 60% of global ethanol production currently comes from maize and about 25% from sugarcane, while smaller portions are produced from wheat, molasses, cassava, and other crops.

Government initiatives around biofuels are also encouraging modernization in ethanol production. Many countries are investing in fermentation infrastructure and agricultural processing to strengthen domestic ethanol supply. According to the International Energy Agency (IEA), global biofuel demand is expected to increase significantly, with total demand projected to rise by about 23% and reach around 200 billion liters by 2028.

Drivers

Rising Global Beverage Consumption Driving Demand for Food Grade Alcohol

One of the most significant factors supporting the growth of the food grade alcohol industry is the steady expansion of the global beverage sector. Food grade alcohol, particularly ethanol, is an essential ingredient used in the production of alcoholic beverages such as spirits, wine, beer, and ready-to-drink cocktails. As beverage consumption increases across both developed and emerging economies, the demand for high-purity alcohol used in beverage manufacturing also rises.

- According to the World Health Organization (WHO), worldwide alcohol consumption reached about 5.0 liters of pure alcohol per person aged 15 and above in 2022, reflecting the continued importance of alcoholic beverages in many societies. The WHO also reports that regular drinkers consume an average of 27 grams of pure alcohol per day, which is roughly equal to two glasses of wine or two bottles of beer.

The beer industry alone demonstrates the magnitude of alcohol-based beverage production. According to industry statistics published by Kirin Holdings, global beer consumption reached around 187.9 million kiloliters in 2023, indicating steady recovery in beverage consumption after earlier market disruptions. Beer production relies heavily on fermentation processes that generate alcohol, and large-scale brewing operations require consistent supplies of high-quality ethanol and fermentation inputs.

Another important factor strengthening this driver is the rapid expansion of ethanol production infrastructure worldwide. Governments and industries have invested heavily in fermentation facilities that convert agricultural feedstocks such as corn, wheat, and sugarcane into ethanol. For example, the United States produced about 16,225 million gallons of ethanol in 2024, reflecting the country’s strong distillation capacity and large agricultural supply chain.

Government initiatives also play an indirect but important role in strengthening this market driver. Several countries have implemented policies to expand ethanol production for energy and agricultural development. The International Energy Agency (IEA) notes that India has rapidly expanded its ethanol industry and has become one of the world’s major producers after nearly tripling its ethanol production over the past five years.

Restraints

Strict Government Regulations and Health Policies Limiting Alcohol Production and Consumption

One of the major restraining factors affecting the Food Grade Alcohol industry is the increasing level of government regulation and public health policies related to alcohol production, distribution, and consumption. Food grade alcohol is widely used in beverages and food formulations, but because it is essentially ethanol, it falls under the same regulatory framework that governs alcoholic beverages. Governments and global health organizations have introduced stricter rules to control alcohol consumption due to its potential health risks.

- According to the World Health Organization (WHO), alcohol consumption is associated with major health risks and contributes significantly to global disease burdens. In 2019, alcohol use was responsible for 6.7% of all deaths among men and 2.4% of all deaths among women worldwide, highlighting the health impact linked with alcohol consumption. Because of these risks, governments are increasingly introducing policies aimed at reducing alcohol intake.

In some regions, authorities also introduce minimum pricing rules to prevent the sale of extremely cheap alcoholic beverages. For example, Scotland implemented a legal minimum price of £0.50 per unit of alcohol to discourage excessive drinking and reduce alcohol-related health problems. Global alcohol consumption patterns also influence regulatory pressure. Research indicates that around 2.3 billion people worldwide consume alcoholic beverages, with an average intake of nearly 6 liters of ethanol per person annually.

Opportunity

Expanding Ready-to-Drink Beverage Industry Creating New Opportunities for Food Grade Alcohol

One of the strongest growth opportunities for the Food Grade Alcohol industry is the rapid expansion of the ready-to-drink (RTD) beverage segment. RTD beverages include canned cocktails, flavored spirits, hard seltzers, and other convenient alcohol-based drinks that require high-purity food grade ethanol for formulation and flavor stability. As consumer lifestyles change and demand shifts toward convenient and portable beverages, beverage companies are introducing a wide range of RTD products.

- The broader food and beverage industry also supports this opportunity. According to data from the Ministry of Food Processing Industries (India), alcoholic beverages account for around 26.6% of the total global food and beverage market in 2024, demonstrating the large role alcohol-based drinks play within the overall food sector.

Government initiatives supporting ethanol production are also helping create opportunities for this industry. Many countries have expanded ethanol manufacturing as part of agricultural and energy policies, which indirectly strengthens the supply chain for food-grade alcohol. For example, ethanol produced from crops such as corn, wheat, and sugarcane is widely used for fuel, food processing, and beverage production. The Food and Agriculture Organization (FAO) notes that ethanol is an important agricultural processing product used in food, industrial alcohol, and alcoholic beverages worldwide.

Consumer behavior is another factor supporting this growth opportunity. Many consumers are moving toward premium beverages, flavored cocktails, and convenient packaged drinks. These products require carefully formulated alcohol content and high-quality ingredients, which increases the demand for food grade alcohol used in beverage manufacturing. RTD cocktails, flavored spirits, and alcohol-infused beverages are becoming more common in supermarkets and restaurants, encouraging beverage producers to increase production capacity and introduce new product lines.

Regional Insights

Asia Pacific dominates with 39.1% share valued at about USD 1.2 Bn due to strong beverage production and fermentation capacity

The Asia Pacific region held the dominant position in the Food Grade Alcohol Market, accounting for around 39.1% share with an estimated value of about USD 1.2 billion. The region’s leadership is largely supported by its massive food and beverage manufacturing base, strong agricultural resources, and expanding consumer demand for alcoholic beverages and processed foods.

Countries such as China, India, Japan, and South Korea play a crucial role in regional production as they have well-established fermentation industries and large distillation capacities. In addition, the availability of key raw materials such as sugarcane, corn, rice, and molasses makes the region highly suitable for producing ethanol and other food-grade alcohols used in beverages, flavor extraction, and food preservation.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

MGP Ingredients, Inc., established in 1941, is headquartered in Atchison, Kansas, U.S. and operates in the production of distilled spirits and food-grade alcohol. In 2024, the company reported revenue of about USD 836 million and continues supplying high-purity ethanol used in beverage and food processing industries. MGP operates 3 major distillation facilities and distributes alcohol products in more than 30 countries. The company employs around 700+ people globally and produces several million proof gallons of food-grade alcohol annually for beverage, flavor extraction, and ingredient manufacturing applications.

Grain Processing Corporation (GPC), founded in 1943, is headquartered in Iowa, United States and specializes in corn-based ingredients and alcohol production. The company operates multiple production facilities in the United States and supplies alcohol ingredients globally. In 2024, GPC produced large volumes of food-grade alcohol used in beverages, pharmaceuticals, and food ingredients. The company employs around 1,000+ workers and processes millions of bushels of corn annually. Its ethanol and alcohol solutions are widely used by beverage manufacturers and food processing industries.

Wilmar International Ltd, established in 1991 and headquartered in Singapore, is one of Asia’s largest agribusiness companies. In 2024, the company recorded revenue of about USD 67 billion and operates in 50+ countries with more than 100 manufacturing facilities. Wilmar produces ethanol and food-grade alcohol derived from sugar and grain feedstocks used in beverages and food processing. The company employs approximately 100,000 people globally and maintains a strong presence across Asia’s food ingredient and agricultural processing industries.

Top Key Players Outlook

- MGP Ingredients, Inc.

- Cargill, Incorporated

- ADM

- Cristalco

- Grain Processing Corporation

- Wilmar International Ltd

- Pure Alcohol Solutions

Recent Industry Developments

In 2024, MGP Ingredients reported total revenue of about USD 703.6 million, reflecting its significant role in alcohol and ingredient production. The distilling solutions division alone generated around USD 332.2 million in sales in 2024.

In fiscal year 2024, Cargill reported total revenue of about USD 160 billion, reflecting its large presence across agricultural processing, food ingredients, and ethanol production sectors.

Report Scope

Report Features Description Market Value (2025) USD 3.3 Bn Forecast Revenue (2035) USD 4.9 Bn CAGR (2026-2035) 3.8% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Type (Ethanol, Polyols), By Source (Molasses And Sugarcane, Fruits, Grains, Others), By Function (Coatings, Preservatives, Coloring And Flavoring Agent, Others), By Application (Healthcare And Pharmaceutical, Food, Beverages, Personal Care, Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA Competitive Landscape MGP Ingredients, Inc., Cargill, Incorporated, ADM, Cristalco, Grain Processing Corporation, Wilmar International Ltd, Pure Alcohol Solutions Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- MGP Ingredients, Inc.

- Cargill, Incorporated

- ADM

- Cristalco

- Grain Processing Corporation

- Wilmar International Ltd

- Pure Alcohol Solutions

Our Clients

- 180227

- Mar 2026